Автор: Adhi Rajaprabhakaran

Компиляция: Цзя Хуань, ChainCatcher

Вечером 12 февраля на бирже, обычно слабо реагирующей на спортивные события, три матча НБА внезапно подожгли торговые объемы: «Даллас Маверикс» против «Лос-Анджелес Лейкерс», «Милуоки Бакс» против «Оклахома-Сити Тандер» и «Портленд Трэйл Блэйзерс» против «Юта Джаз». В течение этих трех игр было заключено более 13 миллионов контрактов. ForecastEx — это рынок прогнозов, управляемый Interactive Brokers и регулируемый Комиссией по торговле товарными фьючерсами США (CFTC). Это настоящая биржа с лицензией, но до того вечера у нее никогда не было сколько-нибудь значительных объемов торгов по НБА.

Я не думаю, что ForecastEx совершила какое-то чудо в привлечении клиентов за одну ночь. Она не улучшила продукт, не запустила маркетинговую кампанию и не увеличила ликвидность для углубления своего стакана заявок. Произошло нечто очень простое: Robinhood направил свои огромные потоки заказов на другую биржу, специально для этого вечера с тремя матчами НБА.

В настоящее время Robinhood является доминирующим дистрибьютором контрактов на прогнозных рынках для розничных инвесторов. Когда пользователь открывает приложение Robinhood, нажимает на матч НБА и делает ставку, эта сделка направляется для исполнения на регулируемую CFTC биржу. На протяжении большей части истории прогнозных рынков Robinhood этой биржей была Kalshi. Но пользователи не знают об этом, и им все равно. Независимо от того, какая биржа работает на заднем плане, интерфейс полностью идентичен: то же приложение, те же кнопки, те же коэффициенты. Биржа стала невидимой инфраструктурой.

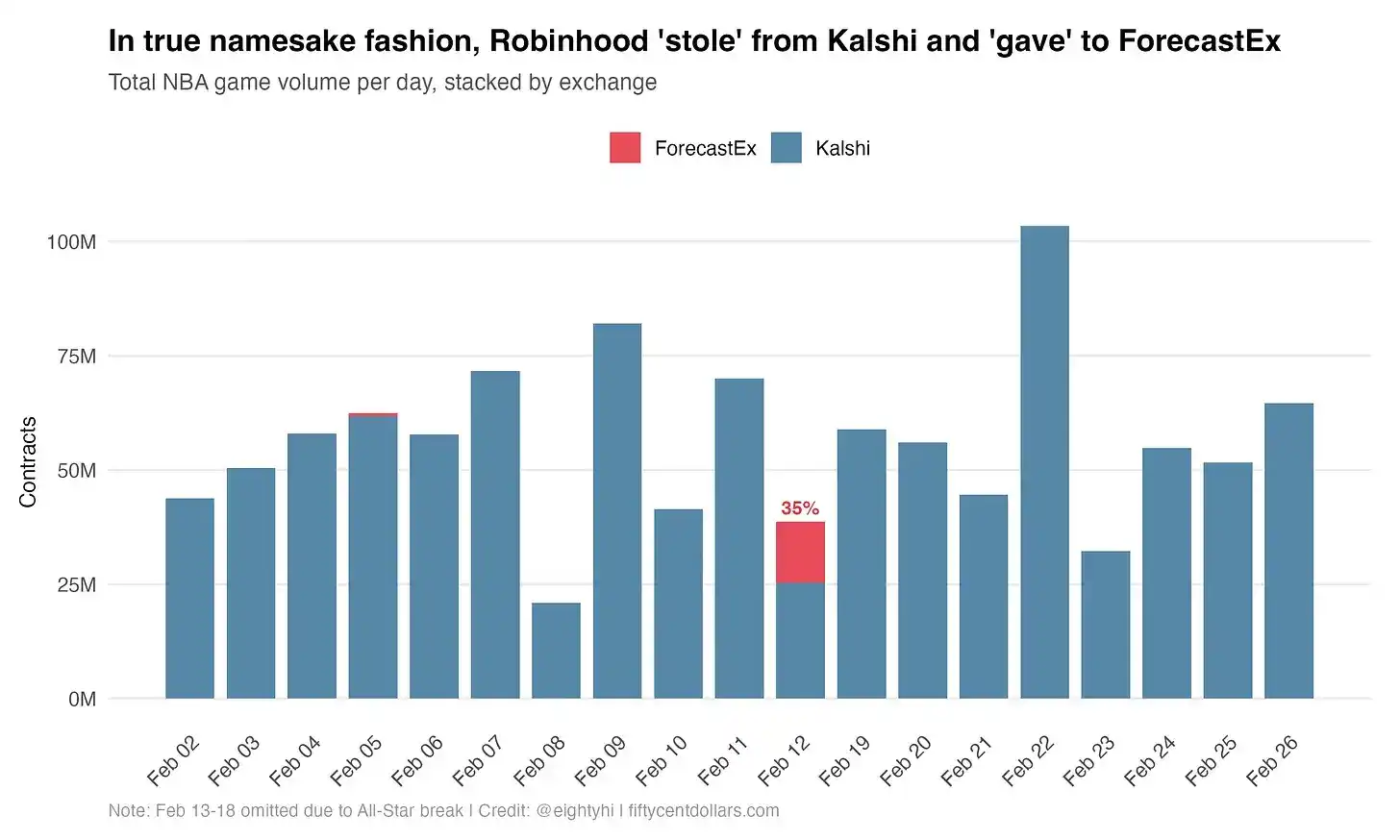

Мгновенная миграция 35% объема торгов

Каждый столбец представляет дневной объем торгов по матчам НБА, сгруппированный по биржам. Синий цвет представляет Kalshi, красный — ForecastEx. За исключением 12 февраля, каждый день был полностью синим, а в этот день 35% объема внезапно оказалось на ForecastEx. Затем все вернулось к полностью синему состоянию, как будто ничего и не происходило.

Красная часть 12 февраля — это те три матча: «Маверикс» против «Лейкерс», «Бакс» против «Тандер», «Трэйл Блэйзерс» против «Джаз». Вместе они принесли 13.4 миллиона контрактов на ForecastEx. Независимо от того, какая биржа обрабатывает сделки, пользовательский опыт в Robinhood одинаков: то же приложение, те же кнопки, те же коэффициенты. Пользователи просто не видят разницы. Потому что для них ее действительно нет.

Вот почему цифра 35% так важна, поскольку она является относительно чистым показателем доли рынка Robinhood в объемах торгов на исходы НБА между этими двумя биржами. У ForecastEx практически нет органически накопленных спортивных пользователей, поэтому можно с уверенностью предположить, что каждый контракт на ForecastEx в тот вечер поступил от заказов Robinhood.

И, учитывая, что интерфейс Robinhood в любом случае одинаков, эти пользователи делали ставки с точно такой же частотой, как и на Kalshi. Есть основания полагать, что примерно треть объема торгов Kalshi на исходы НБА в феврале пришлась на Robinhood.

Robinhood контролирует направление объемов и может переключить этот переключатель за одну ночь.

Похожая история на погодном направлении

Краткое и драматичное перенаправление заказов НБА представляет собой чрезвычайно четкий и убедительный естественный эксперимент для анализа. Но рост рынка погоды на ForecastEx в другом масштабе рассказывает похожую историю.

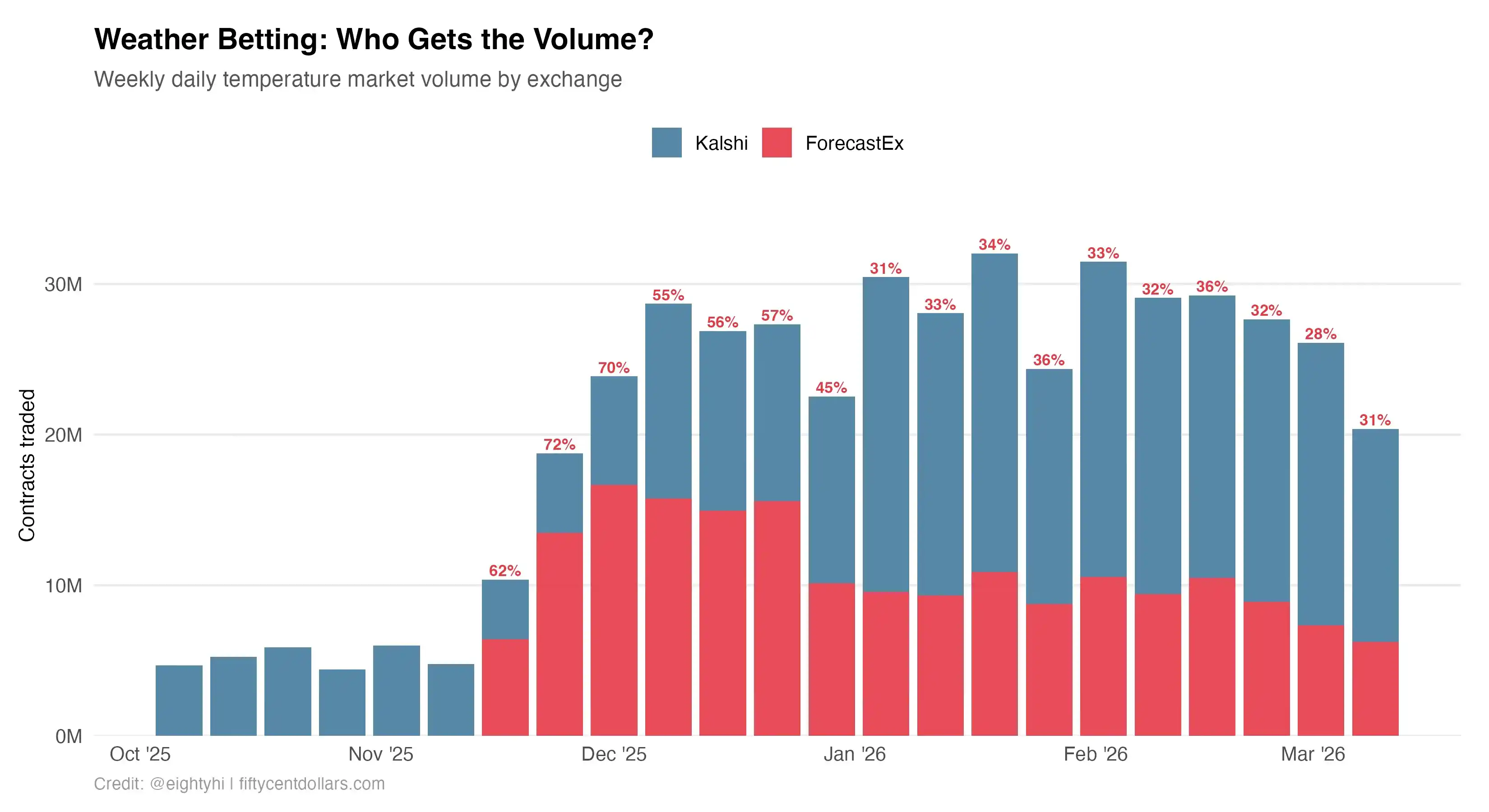

И ForecastEx, и Kalshi предлагают контракты на максимальную дневную температуру: бинарные опционы на то, превысит ли максимальная температура в данном городе заданный порог в определенный день. Эти два рынка представляют собой одинаковый продукт, включающий одинаковые города и одинаковые даты. Единственная реальная разница заключается в бирже, которая сводит сделки.

До 18 ноября 2025 года торговая активность на погодных рынках ForecastEx была нулевой. Затем объемы торгов взорвались за одну ночь, без органического переходного периода, без постепенной кривой внедрения. Этот ступенчатый паттерн полностью соответствует характеристикам НБА. Чтобы измерить пересечение, я сопоставил рынки с одинаковыми парами «город-дата» на ForecastEx и Kalshi, исключив города, присутствующие только на одной бирже. Это дало 454 совпадающих данных «город-дата».

Кстати, этот график предоставляет интересный пример того, как конкуренция платформ является чистым благом для объемов торгов во всей отрасли. Открытие Robinhood крана погодных рынков в целом увеличило активность на обеих биржах, вероятно, из-за арбитража между биржами. Маркет-мейкеры, участвующие в такой деятельности, эффективно распределяют ликвидность по всей экосистеме.

Первые пять недель была только Kalshi, это базовый уровень. Затем появился ForecastEx и сразу же захватил 60% совокупного дневного объема торгов на рынках температуры. В конце ноября он достиг пика в 72%, и с тех пор в целом держится в диапазоне от 53% до 67%.

Ключевая деталь: когда появился ForecastEx, объемы торгов погодой на Kalshi не рухнули. Синие столбцы остались примерно стабильными. Поэтому я интерпретирую это так, что объемы ForecastEx были добавлены поверх существующих потоков Kalshi. Скорее всего, Robinhood впервые открыл погодные рынки и с самого начала направлял свой трафик на ForecastEx, а его пользователи даже не подозревали об этом.

Это различие важно. В случае с НБА в январе Robinhood временно перенаправил объемы, которые изначально шли в Kalshi. На рынках погоды Robinhood, по-видимому, добавил ForecastEx в качестве параллельного направления, сохраняя при этом первоначальные потоки Kalshi нетронутыми. Оба случая доказывают одну и ту же структурную точку зрения: Robinhood решает, куда направляются объемы. Биржи могут только пассивно получать заказы, которые Robinhood выбирает для отправки.

Абсолютное усиление продуктовых инноваций каналами дистрибуции

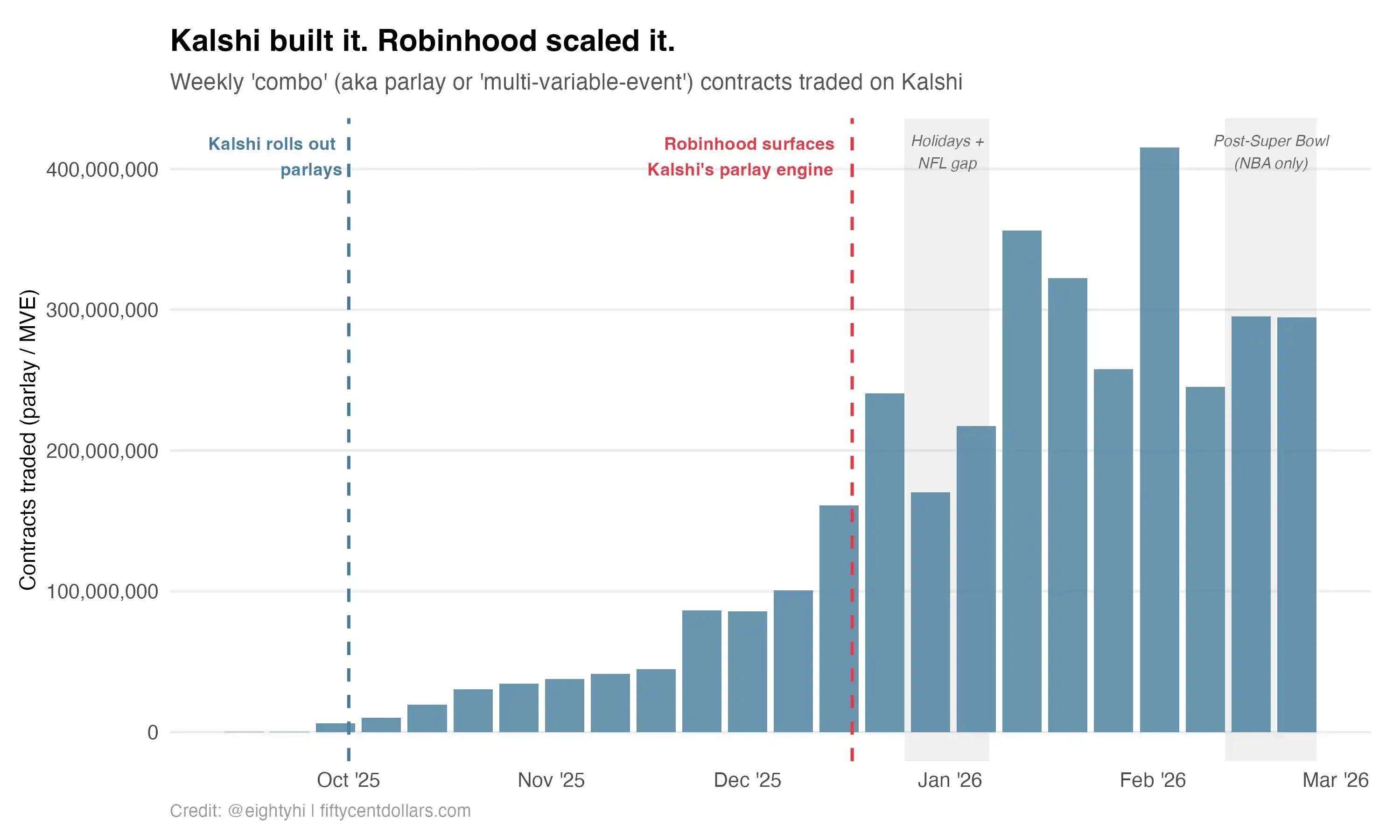

Данные по НБА и погоде показывают, что Robinhood может направлять трафик. А экспрессы (ставка, которая объединяет два или более независимых прогноза в одну ставку. Игрок выигрывает приз только в случае, если все прогнозы верны; если ошибается хотя бы один, вся ставка проигрывается. Из-за повышенной сложности коэффициенты и выплаты обычно очень высоки.) показывают, что он может масштабировать и без того растущий спрос.

Kalshi запустила контракты на мультивариативные события (т.е. «комбо» или «экспрессы») в сентябре 2025 года, как раз к открытию сезона NFL. Продукт сразу же получил признание: еженедельный объем торгов вырос с почти нуля в сентябре до примерно 45 миллионов контрактов к началу декабря. Этот рост был самостоятельным и напрямую относился к платформе Kalshi. Kalshi создала продукт, подала заявку на сертификацию CFTC и внедрила начальную ликвидность. Рынок отреагировал положительно.

Затем вмешался Robinhood.

17 декабря Robinhood объявил о запуске предустановленных экспресс-ставок и ставок на статистику игроков в своем приложении. Всего за несколько недель еженедельный объем торгов взорвался, подскочив с диапазона 45-60 миллионов до почти 100 миллионов, а затем в конце января достиг 300 миллионов в неделю. Затененная область справа отмечает период после Суперкубка, когда экспрессы NFL исчезли, и продукт поддерживался только НБА. Даже без футбола объемы оставались на уровне около 260-290 миллионов в неделю.

Kalshi проделала тяжелую работу по созданию новой продуктовой категории. Канал дистрибуции Robinhood вывел ее на совершенно другой масштаб. Оба вклада реальны. Вопрос в том, какой из них обладает большим структурным рычагом.

Не только Kalshi

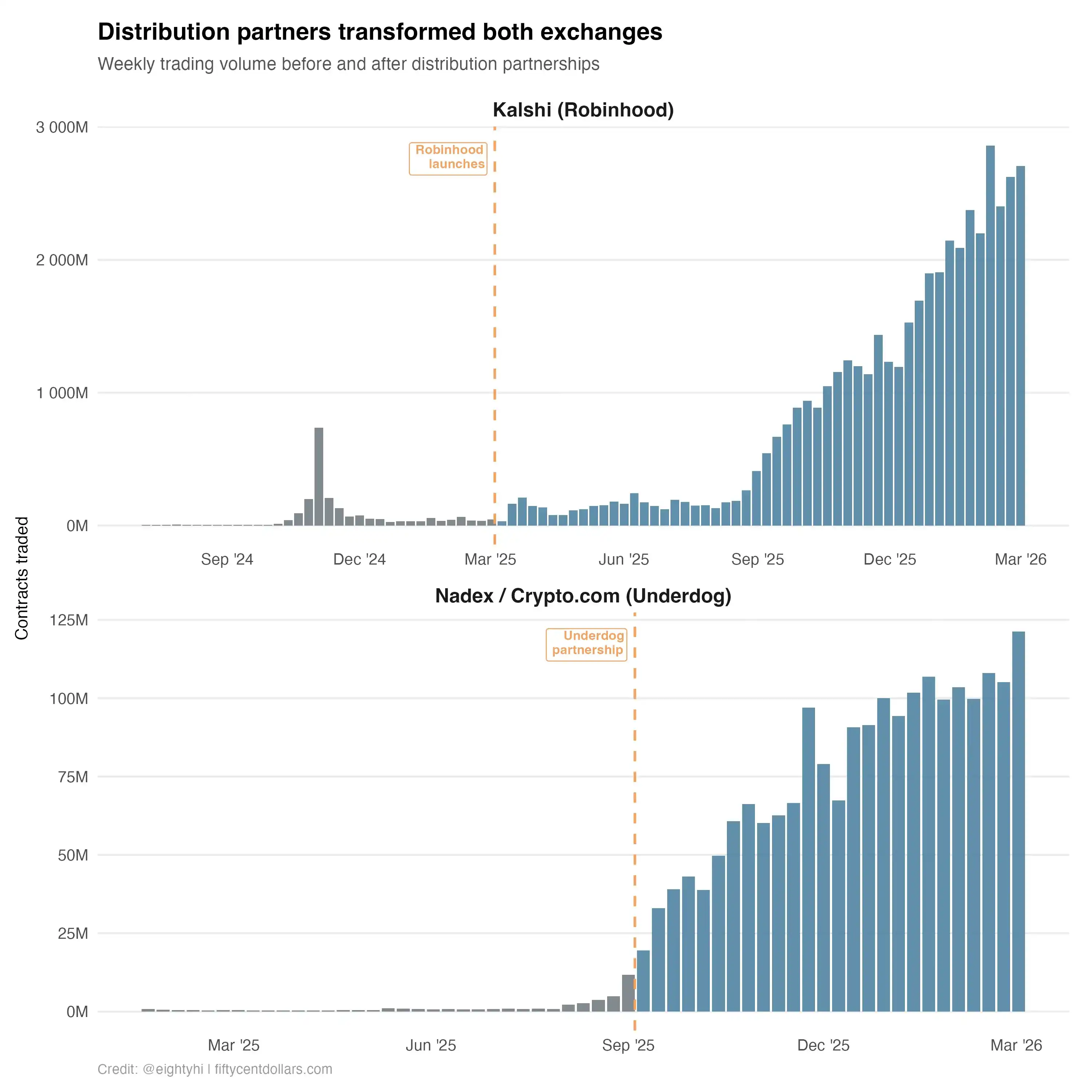

Kalshi добилась огромного роста за последний год, увеличившись с примерно 7 миллионов контрактов в день в конце 2024 года до более чем 100 миллионов к концу 2025 года. Это не полностью заслуга Robinhood. Kalshi создала реальный прямой спрос: новые продуктовые категории, растущая собственная пользовательская база, API-трейдеры и участие институциональных игроков. Год назад широко распространено мнение, что Robinhood приходится подавляющая часть объема торгов Kalshi. Сегодня данные НБА показывают, что на Robinhood приходится около 35% объема торгов на исходы. Такая исполнительская дисциплина по снижению рисков действительно вызывает восхищение.

Но Kalshi — не единственная биржа, которая строит свою историю роста на каналах дистрибуции.

Nadex, работающая как Crypto.com Derivatives и регулируемая CFTC биржа, рассказывает поразительно похожую историю. До интеграции Underdog с Crypto.com в сентябре 2025 года объемы торгов на Nadex были посредственными. После того как Underdog вмешался и начал направлять спортивные ставки своих пользователей на эту биржу, еженедельные объемы торгов взорвались на порядки. Та же модель, разные имена. Underdog для Nadex — это то же самое, что Robinhood для Kalshi: тот слой дистрибуции, который превращает пустующую биржу в оживленный центр.

Самое интересное: оба дистрибьюторских гиганта теперь предприняли шаги, чтобы полностью владеть своими биржами. Robinhood приобрела свою собственную регулируемую CFTC биржу, а Underdog сделал то же самое на прошлой неделе. Две компании, на параллельных trajectories, независимо пришли к одному и тому же выводу.

Это не совпадение. Это теория игр. Если вы дистрибьютор, направляющий миллионы сделок на сторонние биржи, вы делитесь прибылью за каждый контракт с инфраструктурой, которую ваши пользователи даже не могут отличить от white-label API. Вы также отдаете данные, объемы торгов и регуляторную историю потенциальным конкурентам — именно те элементы, которые делают их биржу ценной. Когда вы достигаете достаточного масштаба, рациональным шагом является интернализация этой инфраструктуры. Биржа из чужого profit center превращается в ваш cost center.

Данные по погоде и НБА объясняют, почему с точки зрения биржи так трудно защититься от этой динамики. Даже при доле в 35% объема Robinhood может за одну ночь добавить параллельную биржу для погодных рынков и сразу же направить на нее большую часть нового трафика. Он может во вторник направить три матча НБА на другую биржу, и эти матчи принесут такой же объем торгов, как и в любом другом месте. Пользователи ничего не замечают. Они не выбирают биржу. Они выбирают Robinhood или Underdog.

Я ошибался

В прошлом году, когда ходили слухи, что Robinhood рассматривает возможность приобретения собственной регулируемой CFTC биржи, я публично заявлял, что этого не произойдет.

Я был так уверенно неправ по двум причинам.

Во-первых, из моего опыта работы в Kalshi я на собственном опыте знаю, насколько невероятно сложно создавать и управлять регулируемой биржей деривативов: инфраструктура соответствия, системы мониторинга, отчетность CFTC и так далее. Robinhood получал огромные доходы от прогнозных рынков, выполняя лишь около 1% работы. Биржа делала тяжелую работу, а Robinhood собирал дистрибьюторские сборы — это было самым идеальным партнерством в финтехе за многие годы! Зачем разрушать такую хорошую ситуацию?

Во-вторых, я применял традиционное мышление о структуре рынка деривативов за последние пятьдесят лет. Брокеры не приобретают биржи. В том мире, который я знал, вся суть биржи заключалась в том, что она была незаменимым торговым каналом. CME — это компания стоимостью 90 миллиардов долларов с чистой рентабельностью, уступающей только Visa и Mastercard, потому что «глубина ликвидности» является ее неприступным рвом.

Институциональный трейдер, которому нужно разместить позицию на 50 миллионов долларов по Brent crude, будет очень заботиться о глубине стакана, проскальзывании и концентрации контрагентов. Эту глубину чрезвычайно трудно построить и почти невозможно скопировать, особенно на рынках деривативов, где контракты не являются взаимозаменяемыми между биржами. В том мире биржи заслужили свое структурное положение сами по себе. Брокеры были взаимозаменяемым товаром.

Прогнозные рынки перевернули это с ног на голову. В Robinhood средняя спортивная ставка — это просто обычный пользователь, нажимающий кнопку, чтобы поставить 10 долларов на «Лейкерс». Этому пользователю абсолютно все равно до глубины стакана. Черт возьми, они даже не знают, что такое стакан. Когда размер сделок очень мал, а пользователи недостаточно искушены, глубина ликвидности перестает быть рвом. Robinhood поменял底层管道 во вторник вечером, но с другого конца по-прежнему шел тот же объем торгов.

Когда размер сделок очень мал, а пользователи недостаточно искушены, глубина ликвидности перестает быть рвом.

Я ошибался, потому что все еще ориентировался по старым картам. Структурный рычаг прогнозных рынков находится не там, куда указывает история деривативов последних пятидесяти лет. Он буквально находится в руках тех, кто в конечном итоге владеет пользователями.

На самом деле, я уже написал довольно критическую статью о том, как ForecastEx провалил спортивные события. Это, возможно, нашло отклик... И еще была очень небольшая активность на ForecastEx 5 февраля, которую я не могу объяснить. Возможно, это было раннее тестирование Robinhood. Также возможно, что Robinhood распределяет трафик между несколькими биржами, но внешние аналитики не могут этого знать. Я считаю, что этот пример спорный, потому что система RFQ (запрос котировок) Kalshi и ее огромный пул маркет-мейкеров здесь действительно трудно скопировать. Там есть极其深厚的技术护城河. Кроме того, вопрос «насколько важна ликвидность на прогнозных рынках» все еще остается открытым. Это заставляет меня задуматься: приведет ли нас логика теории игр к homogenized конечной игре — все биржи погрязнут в mutual имитации, стремясь запустить каждый рынок, представленный на рынке.