Editor's Note: Dell's after-hours stock surge is not merely due to earnings beating expectations, but rather the market is re-pricing the value of the AI infrastructure chain.

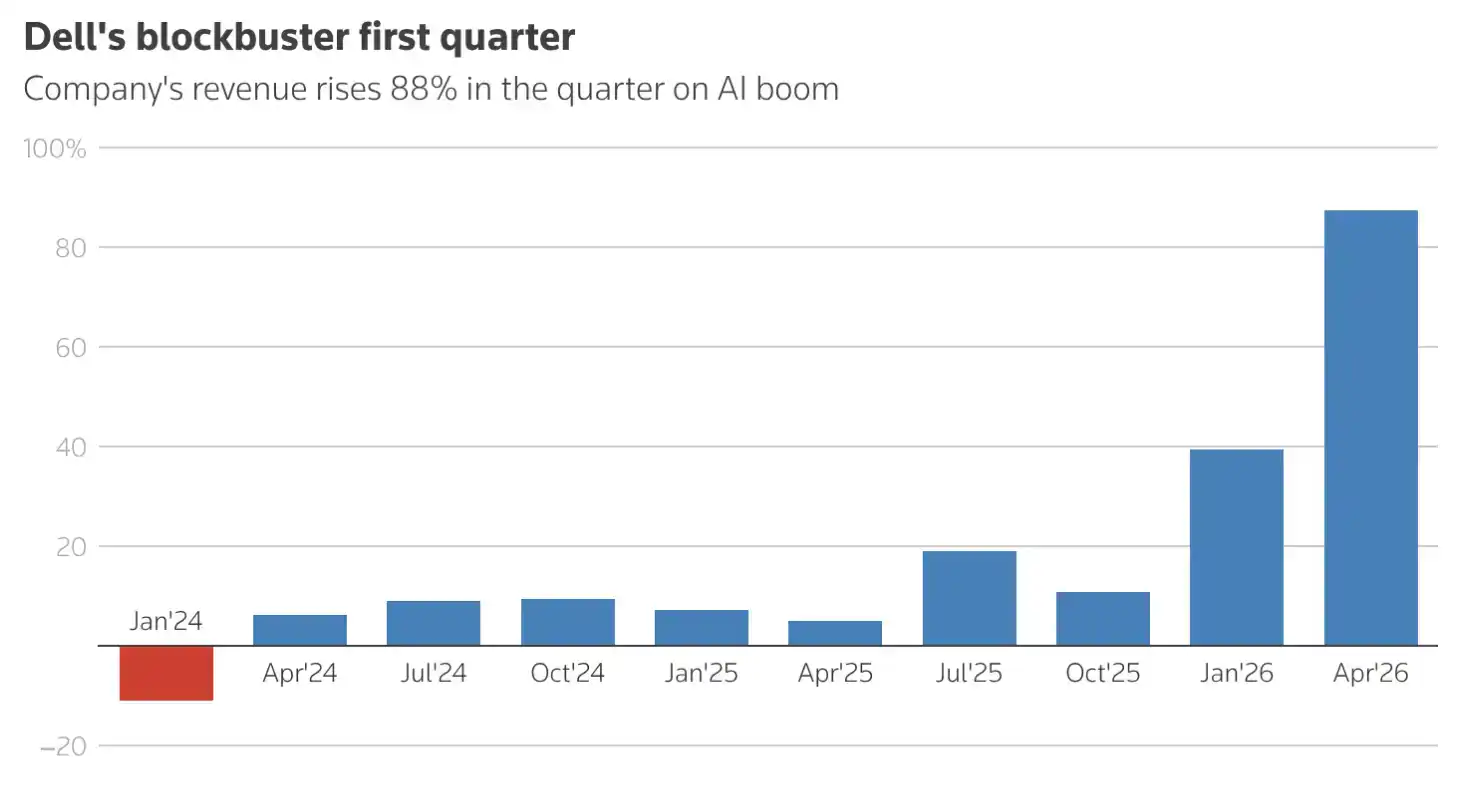

Driven by demand for AI data center construction, Dell's first-quarter revenue increased 88% year-over-year to $43.84 billion, and the company raised its fiscal 2027 AI server revenue expectation from $50 billion to approximately $60 billion. After the earnings release, the company's stock price rose about 39% in after-hours trading.

This indicates that the AI boom is further extending from models and chips to servers, memory, storage, and data center equipment. As tech giants like Alphabet and Amazon continue to increase their investments in AI infrastructure, hardware vendors like Dell, which possess supply chain capabilities, customer relationships, and delivery strength, are becoming direct beneficiaries in this new cycle of AI capital expenditure.

Additionally, a subsidiary of Dell securing a $9.7 billion contract with the U.S. Department of Defense has further strengthened market expectations for its order growth and revenue certainty. For investors, Dell's rise signifies that the AI trade is entering a more downstream and tangible phase: those who can turn chips into deliverable data center infrastructure are likely to receive the next round of valuation re-rating.

The following is the original text:

TL;DR

Dell raises full-year AI server revenue expectation to $60 billion

The company's Q2 guidance is higher than market expectations

Q1 revenue grew 88% YoY to $43.84 billion

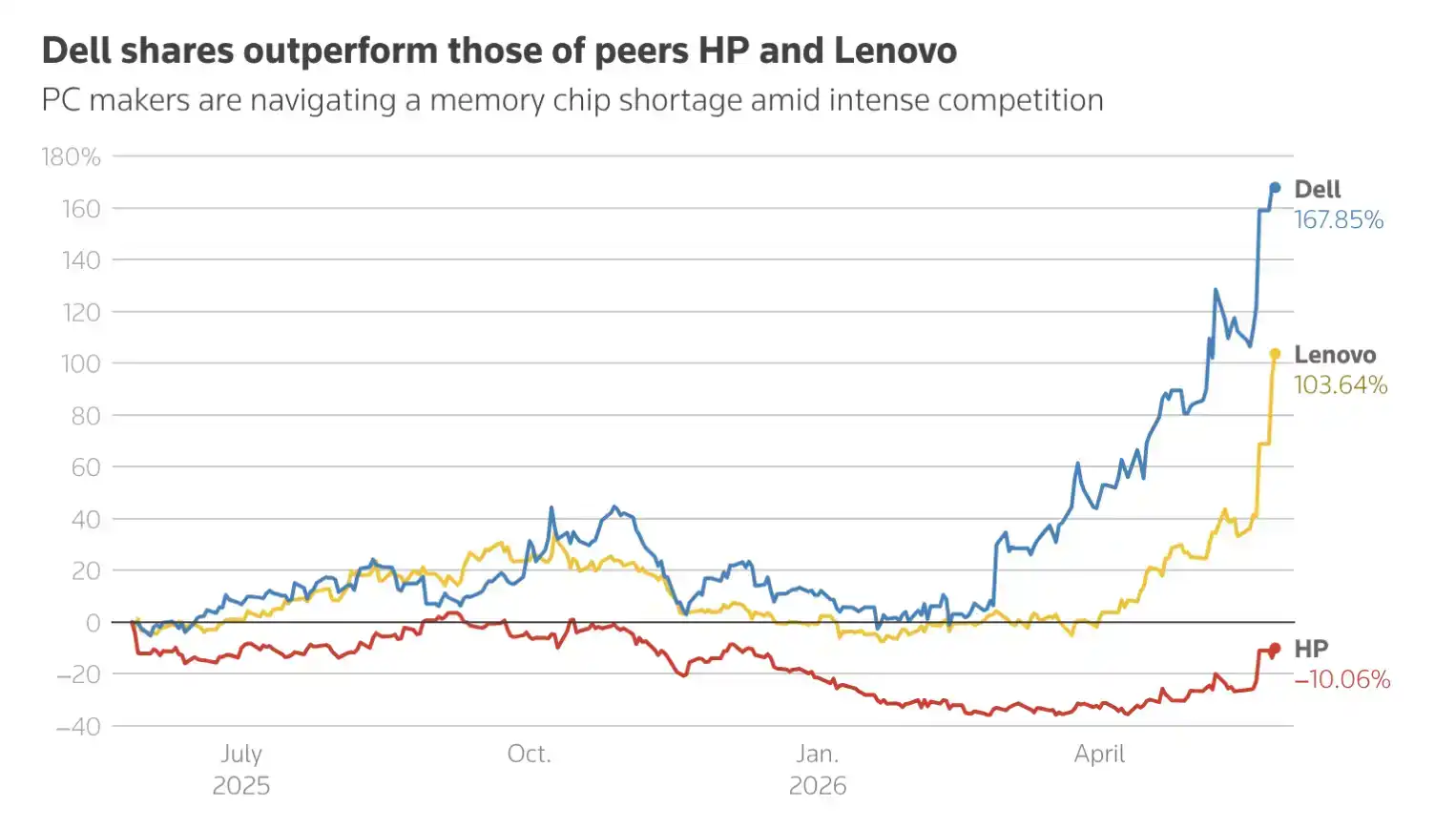

Stock price rose about 39% in after-hours trading

A Dell subsidiary secures a $9.7 billion contract from the U.S. Department of Defense

Dell (Dell) on Thursday raised its full-year revenue and profit forecasts, showing that customer data center expansion is driving demand for its AI-optimized servers. These servers are equipped with Nvidia's advanced chips.

Dell's clients include CoreWeave, Honeywell International, and Samsung Electronics. After the earnings release, the company's stock rose about 39% in after-hours trading.

U.S. tech giants including Alphabet and Amazon plan to invest over $700 billion in AI infrastructure this year, which will boost demand for servers and data center equipment from suppliers like Dell and Super Micro Computer.

The strong results show that Dell has become one of the biggest beneficiaries of the generative AI boom. The company has navigated the memory chip shortage crisis relatively well through price increases and supply chain adjustments.

Dell's Chief Operating Officer, Jeff Clarke, said on the earnings call: "We feel like we're repricing almost daily. I think customers feel that too. Unfortunately, I don't think that's going to change, given the inflationary environment we're in."

Dell stated that it now expects fiscal 2027 AI server revenue to be approximately $60 billion, up from its previous expectation of $50 billion.

The company also raised its full-year revenue forecast to $165 billion - $169 billion, a significant increase from the previous forecast of $138 billion - $142 billion.

Concurrently, Dell raised its full-year adjusted EPS forecast from $12.90 to $17.90.

In the first quarter, Dell's revenue grew 88% year-over-year to $43.84 billion, significantly higher than the LSEG consensus analyst estimate of $35.43 billion. Adjusted EPS was $4.86, also above the market expectation of $2.94.

Melissa Otto, Head of Research at S&P Global Visible Alpha, said: "Dell is in a better position relative to competitors due to its scale, supplier relationships, and ability to prioritize demand, which has helped it gain market share during the memory shortage."

Revenue for Dell's Infrastructure Solutions Group, which includes storage, software, and server businesses, grew 181% for the quarter. Meanwhile, sales for the Client Solutions Group, which includes the PC business, increased 17%.

The company also provided Q2 revenue and adjusted EPS guidance that exceeded market expectations.

On Wednesday, the U.S. Department of Defense awarded a five-year, $9.7 billion contract to a Dell subsidiary to assist with managing Microsoft software licenses.