От редактора: Резкий рост акций Dell после закрытия торгов связан не просто с превышением ожиданий по отчетности, а с тем, что рынок переоценивает цепочку создания стоимости в инфраструктуре ИИ.

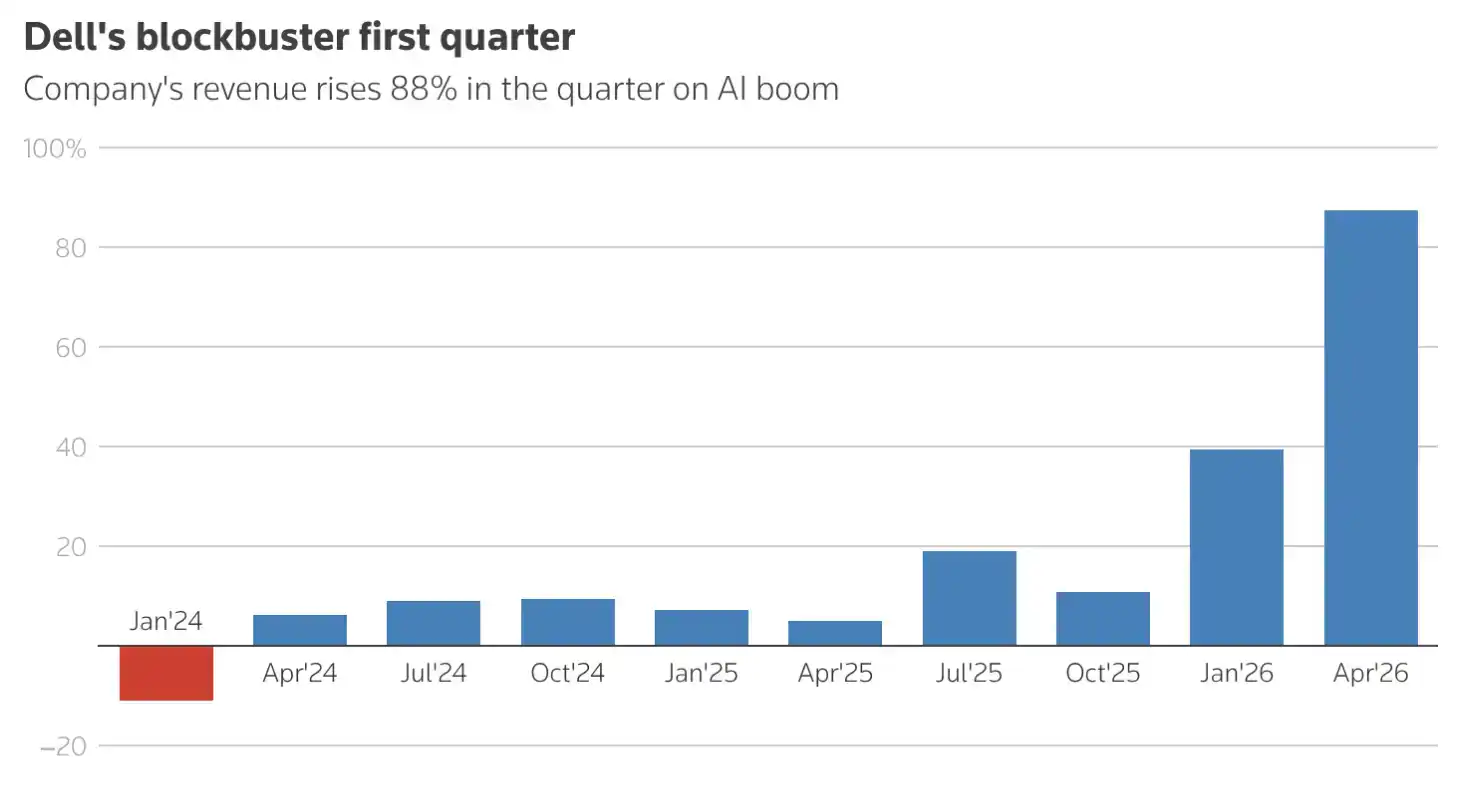

Благодаря спросу на строительство дата-центров для ИИ, выручка Dell в первом квартале выросла на 88% в годовом исчислении до 43,84 млрд долларов США, а прогноз по доходам от серверов для ИИ на 2027 финансовый год был повышен с 500 млрд долларов примерно до 600 млрд долларов. После публикации отчетов цена акций компании в ходе внебиржевых торгов выросла примерно на 39%.

Это говорит о том, что ажиотаж вокруг ИИ распространяется от моделей и чипов дальше — на серверы, память, системы хранения данных и оборудование для дата-центров. По мере того как технологические гиганты, такие как Alphabet и Amazon, продолжают наращивать инвестиции в инфраструктуру ИИ, аппаратные компании, подобные Dell, обладающие возможностями в цепочке поставок, клиентскими отношениями и способностью к поставкам, становятся прямыми бенефициарами нового цикла капитальных затрат на ИИ.

Кроме того, контракт Министерства обороны США на 9,7 млрд долларов, полученный подразделением Dell, еще больше укрепил рыночные ожидания относительно роста заказов и определенности доходов компании. Для инвесторов рост Dell означает, что торговля на теме ИИ переходит на более поздние и более материальные этапы: те, кто способен превратить чипы в поставляемую инфраструктуру для дата-центров, могут получить следующую переоценку.

Ниже представлен оригинальный текст:

Кратко

Dell повысила годовой прогноз по доходам от серверов для ИИ до 600 млрд долларов

Прогноз компании на второй квартал превысил рыночные ожидания

Выручка в первом квартале выросла на 88% в годовом исчислении до 43,84 млрд долларов

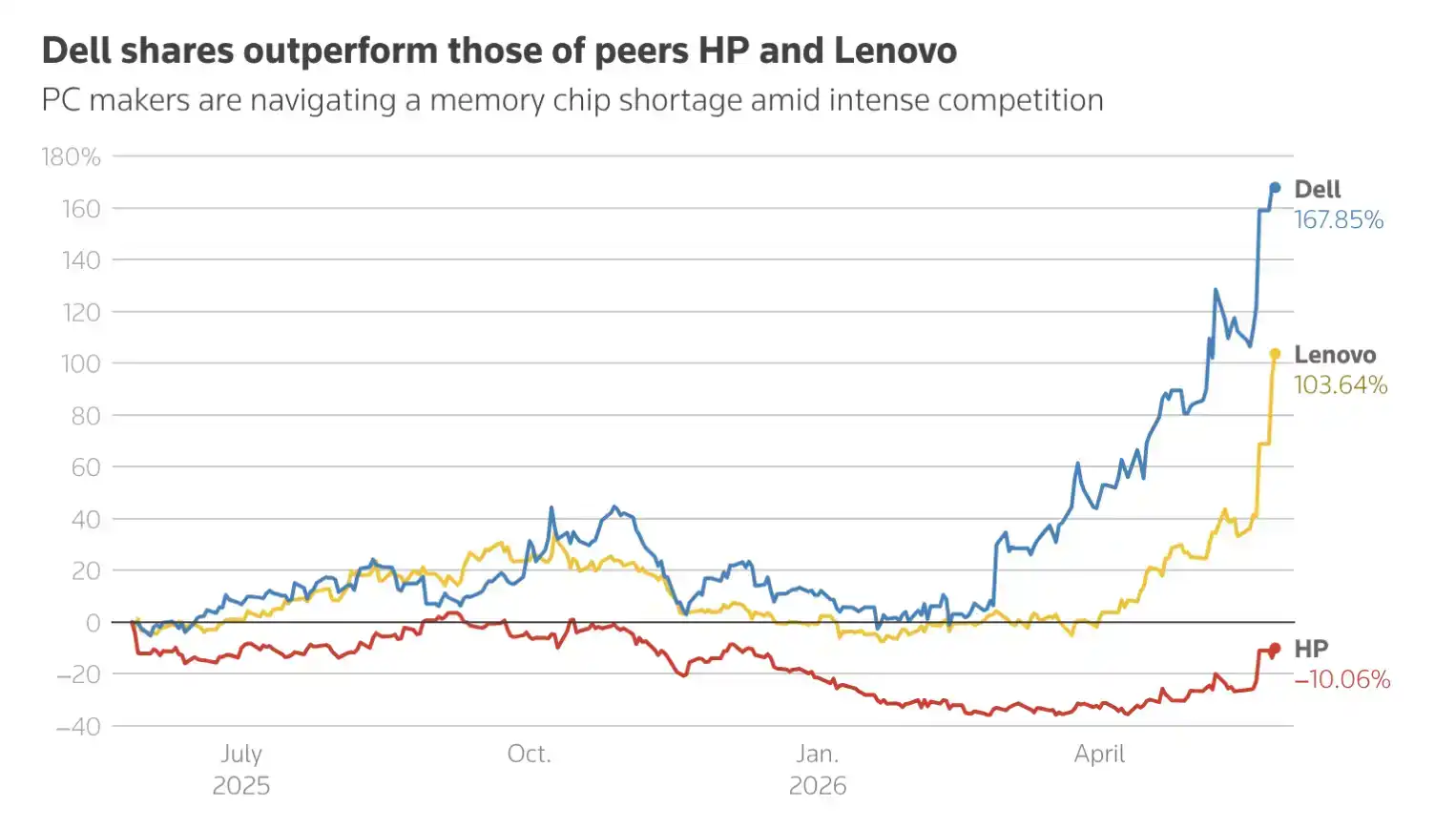

В ходе внебиржевых торгов акции компании выросли примерно на 39%

Подразделение Dell получило контракт Министерства обороны США на 9,7 млрд долларов

В четверг Dell повысила годовой прогноз по выручке и прибыли, что свидетельствует о росте спроса на оптимизированные для ИИ серверы со стороны клиентов, расширяющих свои дата-центры. Эти серверы оснащены передовыми чипами Nvidia.

Среди клиентов Dell — CoreWeave, Honeywell International и Samsung Electronics. После публикации отчетов цена акций компании в ходе внебиржевых торгов выросла примерно на 39%.

Американские технологические гиганты, включая Alphabet и Amazon, планируют в этом году инвестировать более 700 млрд долларов в инфраструктуру ИИ, что повысит спрос на серверы и оборудование для дата-центров у таких поставщиков, как Dell и Supermicro.

Сильные результаты показывают, что Dell стала одним из крупнейших бенефициаров бума генеративного ИИ. Компании удалось успешно справиться с дефицитом чипов памяти благодаря повышению цен и корректировкам цепочки поставок.

Главный операционный директор Dell Джефф Кларк во время телефонной конференции, посвященной отчетности, заявил: «У нас ощущение, что мы переоцениваем почти каждый день. Я уверен, что клиенты тоже это чувствуют. К сожалению, учитывая инфляционную среду, в которой мы сейчас находимся, я не думаю, что это изменится».

Dell заявила, что теперь ожидает, что выручка от серверов для ИИ в 2027 финансовом году составит около 600 млрд долларов, что выше предыдущего прогноза в 500 млрд долларов.

Компания также повысила годовой прогноз по выручке до 165–169 млрд долларов, что значительно выше предыдущего прогноза в 138–142 млрд долларов.

Кроме того, Dell повысила годовой прогноз по скорректированной прибыли на акцию с 12,90 доллара до 17,90 доллара.

В первом квартале выручка Dell выросла на 88% в годовом исчислении до 43,84 млрд долларов, что значительно превышает средние ожидания аналитиков, собранные LSEG, в размере 35,43 млрд долларов. Скорректированная прибыль на акцию составила 4,86 доллара, что также выше рыночных ожиданий в 2,94 доллара.

Мелисса Отто, директор по исследованиям в S&P Global Visible Alpha, заявила: «Благодаря преимуществам масштаба, отношениям с поставщиками и способности удовлетворять приоритетный спрос, Dell находится в более выгодном положении по сравнению с конкурентами, что помогло ей увеличить долю рынка в период дефицита памяти».

Квартальная выручка подразделения Infrastructure Solutions Group, которое включает хранение данных, программное обеспечение и серверы, выросла на 181%. В то же время продажи подразделения Client Solutions Group, включающего бизнес по ПК, выросли на 17%.

Компания также дала прогноз по выручке и скорректированной прибыли на акцию на второй квартал, превышающий рыночные ожидания.

В среду Министерство обороны США предоставило подразделению Dell пятилетний контракт на сумму 9,7 млрд долларов на помощь в управлении лицензиями на программное обеспечение Microsoft.