DeFi is addressing a key inefficiency as protocols move to reclaim value once captured by external Maximal Extractable Value (MEV) bots during liquidations.

For years, bots exploited liquidation windows, extracting profits while value leaked from users and weakened protocol sustainability over time.

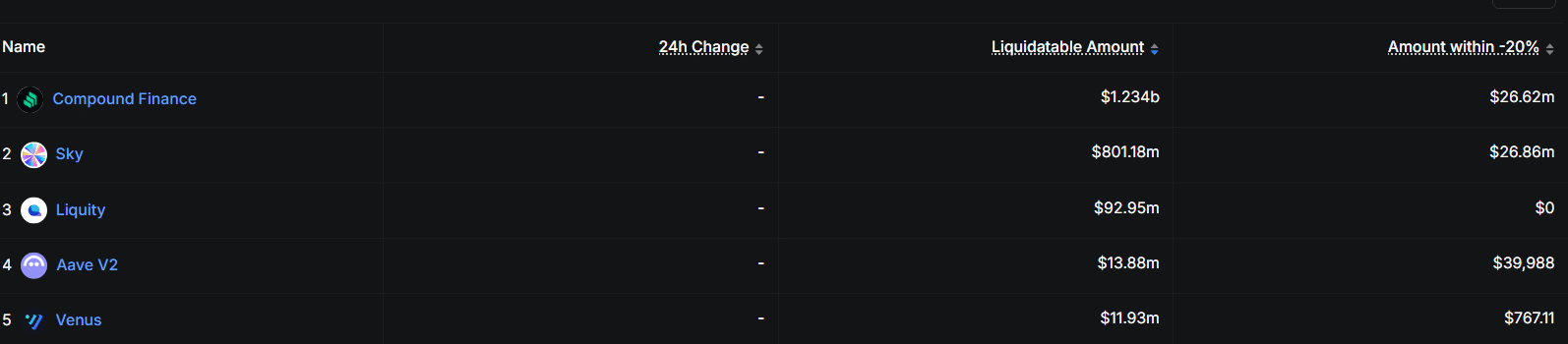

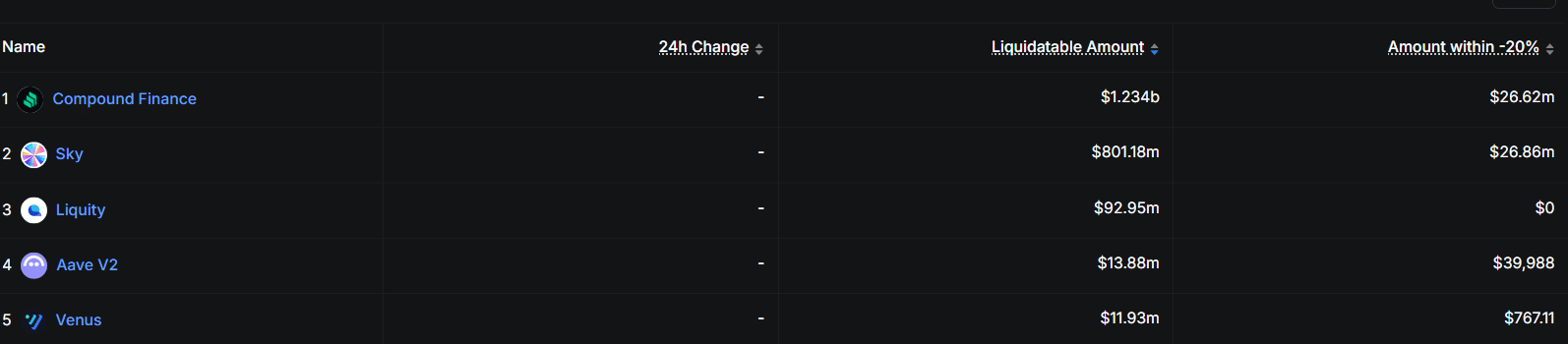

As this leakage grew too large to ignore, Ethereum’s [ETH] lending markets started holding about $2.16 billion in liquidatable positions.

Within this, Compound accounted for $1.23 billion, while Sky held around $801 million, highlighting persistent extraction opportunities during volatility.

However, protocols are redesigning mechanisms through auctions and controlled liquidations to retain value internally rather than letting it escape. This shift changes who benefits from market stress, allowing protocols to capture and recycle value instead of losing it.

As a result, DeFi strengthens its economic structure, improving sustainability and reinforcing long-term resilience

Aave reclaims MEV as SVR reshapes liquidation flows

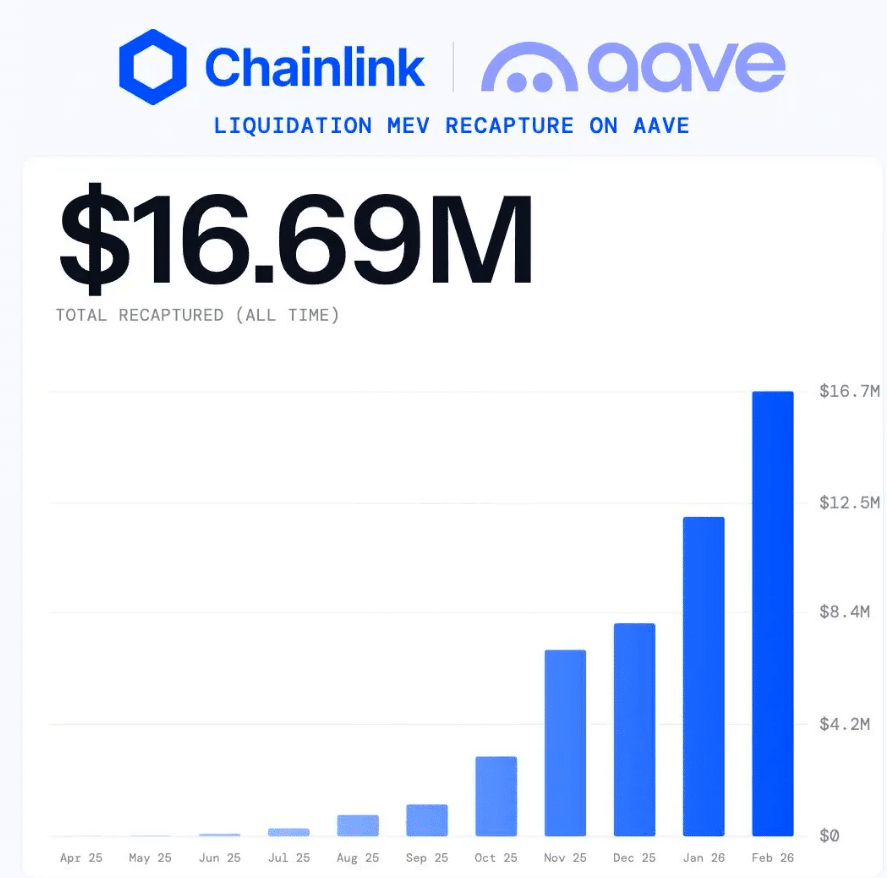

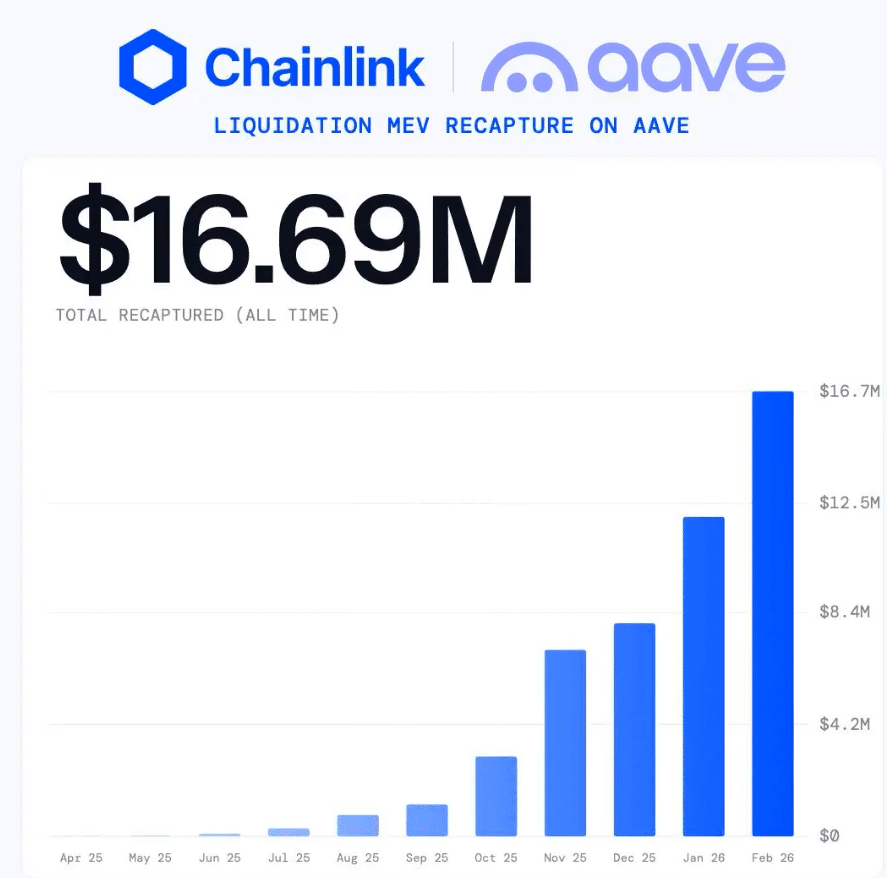

Aave [AAVE] is not just refining its system; it is expanding a model that is already changing how value moves during liquidations. After proving effective on Ethereum, where Aave recaptured over $16.7 million in MEV, the protocol now extends SVR to Arbitrum and Base.

This expansion is happening because the previous model left too much value on the table. Bots consistently captured liquidation profits, especially during volatility, while protocols saw little benefit. SVR changes this by redirecting that flow back into Aave’s ecosystem.

As this rollout scales across chains, liquidation events no longer act as pure extraction points. Instead, they become controlled revenue channels that strengthen the protocol.

The implication of these changes is clear. Aave is turning volatility into income, which improves sustainability and sets a precedent for how DeFi protocols capture value going forward.

SVR boosts revenue, but sustainability remains uncertain

As SVR begins to scale across networks, the focus shifts from early success to whether these gains can actually hold over time. The initial results look strong, yet they raise a deeper question about durability.

Aave now sits near $23.87 billion in TVL, while revenue reaches $6.24 million over 30 days, pointing to a $76 million annual run rate. This growth is not accidental, since liquidation activity is now feeding directly into protocol income.

This shift happens because value no longer escapes to bots and instead flows back into the ecosystem, strengthening internal cash flow. However, this strength is conditional. Revenue rises with volatility and lending demand, yet fades when activity slows.

All in all, this approach leaves a clear outcome. SVR improves Aave’s economics, but only sustained market activity can turn these gains into durable value growth.

Final Summary

- The Aave protocol internalizes MEV through SVR, strengthening DeFi’s shift toward sustainable value capture.

- AAVE shows rising revenue and improved efficiency, yet long-term growth remains dependent on volatility.