Автор: Thejaswini M A

Перевод: Block unicorn

Существует модель, которая повторяется в различных отраслях, в разные эпохи и на разных рынках. Сначала происходит взрывной рост. Появляются бесчисленные продукты, каждый из которых заявляет, что он в чём-то лучше любого другого. Возникают специализированные инструменты, появляются нишевые решения. Потребителям говорят, что выбор — это свобода, кастомизация — это сила, а будущее принадлежит тем, кто ломает традиционные монополии.

Затем, тихо, но неумолимо, маятник начинает движение в обратную сторону.

Не потому, что эксперты ошибались, и не потому, что система в целом была хороша, а потому, что издержки фрагментации накапливаются незаметно. Каждый новый инструмент — это ещё один пароль для запоминания, ещё один интерфейс для изучения, ещё одна точка отказа в системе, которую вы должны поддерживать. Суверенитет начинает становиться бременем, свобода — накладными расходами.

На этапе консолидации конечные победители — не те, кто делает всё идеально, а те, кто делает достаточно много вещей достаточно хорошо, чтобы трение ухода (и воссоздания всей системы в другом месте) стало непреодолимым. Они не связывают вас контрактами или условиями блокировки, они захватывают вас удобством. Удобством, которое проистекает из бесчисленных мелких интеграций и повышений эффективности, каждое из которых в отдельности, возможно, не стоит того, чтобы из-за него уходить, но вместе они образуют ров.

Мы уже видели, как это происходило в электронной коммерции, облачных вычислениях и стриминге. Теперь мы наблюдаем, как это происходит в сфере финансов.

Coinbase только что сделала ставку на то, с какой стороны цикла мы входим.

Позвольте мне сделать небольшой флешбэк.

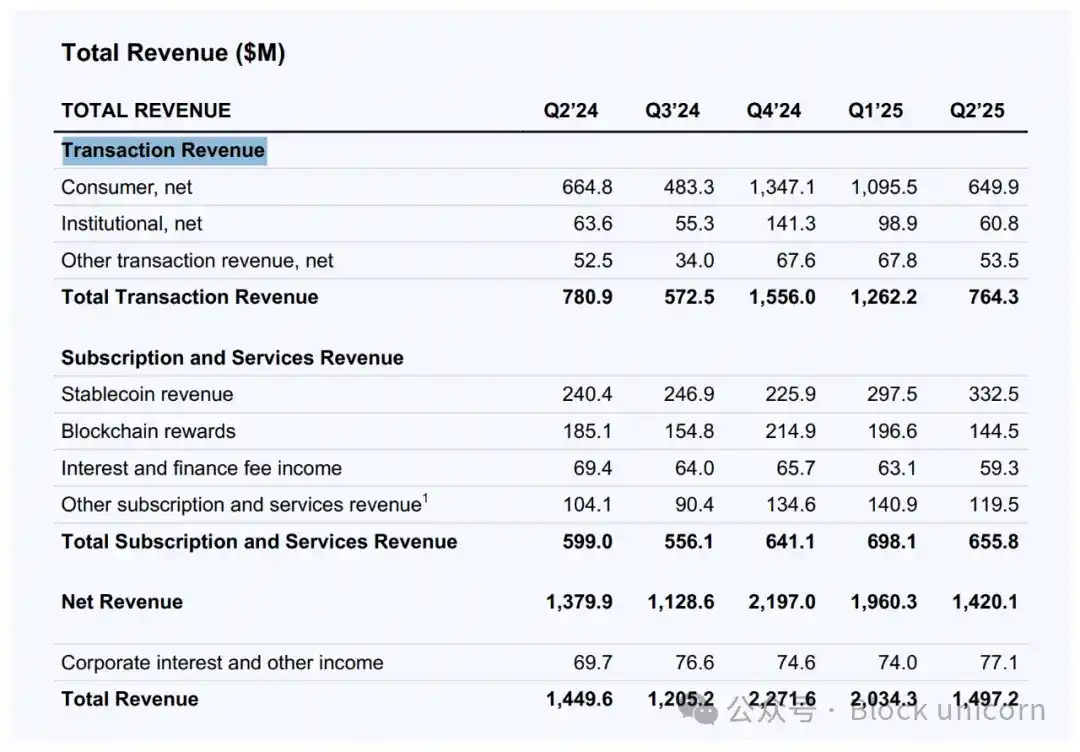

На протяжении большей части своей истории Coinbase была простой для понимания. Это был предпочтительный способ для американцев купить биткоин, не чувствуя, что они делают что-то сомнительное. У неё были регулируемые лицензии, чистый интерфейс, и служба поддержки, хотя часто работала плохо, но хотя бы теоретически существовала. Компания вышла на биржу в 2021 году с оценкой в 65 миллиардов долларов, и её основная идея — быть входной дверью в криптовалюты — какое-то время действительно работала.

Но к 2025 году позиционирование «входа в криптовалюты» начало выглядеть не очень хорошо. Комиссии за спотовые сделки сжимались. Розничные объёмы торгов демонстрировали резкие циклические колебания, взлетая на бычьем рынке и падая на медвежьем. Крупные держатели биткоина всё чаще предпочитали использовать самокастодиальные кошельки. Регуляторы всё ещё подавали на компанию в суд. А Robinhood, которая начинала как приложение для торговли акциями, а затем вышла на крипторынок, внезапно взлетела до рыночной капитализации в 105 миллиардов долларов, что почти вдвое больше капитализации Coinbase. В 2021 году более 90% выручки Coinbase приходилось на торговлю. Ко второму кварталу 2025 года эта доля упала ниже 55%.

Итак, когда основной продукт оказался под давлением, Coinbase поступила так, как поступили бы вы: она попыталась стать всем остальным.

Они называют это теорией «биржи всего», которая предполагает, что агрегация побеждает специализацию.

Торговля акциями означает, что пользователи теперь могут реагировать на отчёты Apple в полночь с помощью USDC, не выходя из приложения. Рынки предсказаний означают, что они могут проверять цену «Снизит ли ФРС ставки?» во время обеда. Бессрочные фьючерсы означают, что они могут использовать 50-кратное плечо по позициям в Tesla в воскресенье. Каждый новый рынок — это повод открыть приложение, возможность получить спред, комиссию или проценты на стабильной монете с незадействованного баланса.

Стратегия заключается в «давайте станем Robinhood» или «давайте сделаем так, чтобы пользователям никогда не понадобился Robinhood»?

В финтехе всегда существовало мнение, что пользователям нужны специализированные приложения. Одно для инвестиций, одно для банковских операций, одно для платежей, одно для торговли криптовалютами. Coinbase идёт в противоположном направлении: они считают, что после того, как пользователь один раз пройдёт KYC и привяжет один банковский счёт, ему не нужно делать это ещё девять раз в других местах.

Вот в чём заключается тезис «агрегация лучше специализации». В мире, где базовые активы всё больше становятся просто токенами в блокчейне, это имеет смысл. Если акции — это токены, контракты на рынках предсказаний — это токены, мемкоины — это токены, почему они все не могут торговаться на одной и той же площадке?

Механика такова: вы вносите доллары (или USDC), торгуете всеми активами и выводите доллары (или USDC). Никаких переводов средств между платформами. Никаких минимальных депозитов на нескольких счетах. Только один пул ликвидности, текущий между всеми классами активов.

Чем больше Coinbase становится похожей на традиционного брокера, тем больше ей приходится конкурировать по правилам традиционных брокеров. У Robinhood 27 миллионов фондируемых счетов, а у Coinbase около 9 миллионов активных пользователей в месяц. Таким образом, дифференциация Coinbase не может заключаться только в «мы теперь тоже предлагаем торговлю акциями», она должна заключаться в самой торговой платформе.

Обещание круглосуточной ликвидности для всех видов торговли. Никаких торговых часов, никаких задержек с расчётами, никакой необходимости ждать одобрения маржинальной заявки от брокера, пока сделка идёт против вас.

Важно ли это для большинства пользователей? Возможно, пока нет. Большинству людей не нужно торговать акциями Apple в три часа ночи в субботу. Но некоторым — нужно. Если вы предоставляете платформу, которая позволяет им это делать, вы получаете их торговый поток. Получив их торговый поток, вы получаете их данные. Получив их данные, вы можете создавать лучшие продукты. Имея лучшие продукты, вы получаете больше торгового потока.

Это маховик, при условии, что он начнёт вращаться.

Игра на рынках предсказаний

Рынки предсказаний — самая необычная часть этого набора и, возможно, самая важная. Это не «торговля» в традиционном смысле, а структурированные ставки на бинарные исходы. Например: победит ли Трамп? Повысит ли ФРС ставку? Попадёт ли «Лейкерс» в плей-офф?

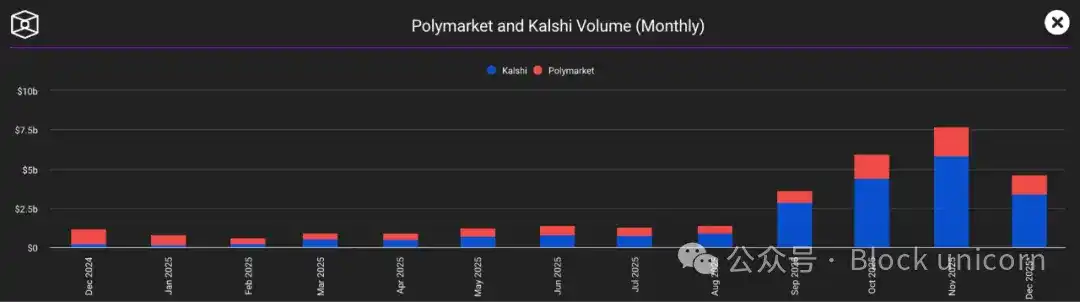

Эти контракты исчезают после расчёта, поэтому нет долгосрочной базы держателей. Ликвидность зависит от событий, что означает, что она резко колеблется и её трудно предсказать. Тем не менее, такие платформы, как Kalshi и Polymarket, в ноябре увидели всплеск объёмов торговли до более чем 7 миллиардов долларов.

Почему? Потому что рынки предсказаний — это социальный инструмент. Они позволяют людям выражать своё мнение и нести соответствующий риск. Они заставляют людей проверять телефон в четвёртой четверти игры или в ночь выборов.

Для Coinbase рынки предсказаний решают конкретную проблему: вовлечённость пользователей. Когда цены на криптовалюты находятся в боковом тренде, пользователям может стать скучно. Когда ваш портфель акций не двигается, торговля акциями тоже может стать скучной. Но всегда происходят какие-то события, которые привлекают внимание. Интеграция с Kalshi даёт пользователям повод оставаться в приложении, даже если цена биткоина не движется.

Ставка заключается в том, что пользователи, пришедшие из-за рынков выборов, будут продолжать торговать акциями, и наоборот. Ставка заключается в том, что чем шире охват, тем выше удержание.

Бизнес-модель, ориентированная на маржу

Отбросьте инновационный нарратив, и вы увидите, что это компания, которая пытается получать прибыль с одного и того же пользователя большим количеством способов. Комиссии за торговлю акциями, спреды на свопах децентрализованных бирж (DEX), проценты на остатках стейблкоинов, комиссии за крипто-кредитование, доход от подписки Coinbase One и плата за инфраструктуру от разработчиков, использующих блокчейн Base.

Я не критикую. Так работают биржи. Лучшие биржи — не те, у которых самые низкие комиссии, а те, от которых пользователям жалко уходить, потому что уход означает необходимость воссоздавать всю систему в другом месте.

Coinbase строит замкнутую экосистему, но эти стены предназначены не для блокировки пользователей, а для предоставления удобства. Вы по-прежнему можете вывести свои криптовалюты, вы всё ещё можете перевести свои акции в Fidelity. Просто вы, вероятно, не станете этого делать, потому что зачем?

Преимущество Coinbase заключается в её ончейн-технологии, которая может обеспечить токенизированные акции, мгновенные расчёты и программируемые деньги. Но на данный момент её торговля акциями очень похожа на торговлю акциями в Robinhood, только с более длинными торговыми часами. Её рынки предсказаний также очень похожи на Kalshi, просто встроенные в другое приложение.

Реальное дифференцирующее преимущество — это Level 2 блокчейн Base, который Coinbase построила и которым управляет. Если торговля акциями действительно будет происходить в цепи, платежи действительно будут осуществляться стейблкоинами, а ИИ-агенты действительно начнут автономно торговать по протоколу x402, то Coinbase создаст продукт, который Robinhood будет нелегко скопировать.

Но это долгосрочная перспектива. В краткосрочной перспективе конкуренция сводится к тому, чьё приложение имеет наибольшую вовлечённость. И добавление большего количества функций не обязательно автоматически увеличивает вовлечённость в приложение. Вместо этого оно может сделать интерфейс приложения более загромождённым, сложным и подавляющим для новых пользователей, которые просто хотят купить биткоин.

Часть пользователей криптовалют будет недовольна этим. Они — истинные верующие. Они хотят, чтобы Coinbase была входом в децентрализованные финансы, а не централизованным супер-приложением, в котором некоторые функции DeFi спрятаны в подменю.

Coinbase явно выбрала масштаб, а не чистоту. Она хочет получить миллиард пользователей, а не миллион пуристов. Она хочет стать финансовой платформой по умолчанию для масс, а не предпочтительной биржей для тех, кто запускает собственные ноды.

Возможно, это правильное бизнес-решение. Массовый рынок не заботится о децентрализации. Он заботится об удобстве, скорости и избежании финансовых потерь. Если Coinbase может обеспечить это, то лежащая в основе философия не имеет значения.

Но это создаёт своеобразное противоречие. Coinbase пытается одновременно быть инфраструктурой для ончейн-мира и централизованной биржей, конкурирующей с Charles Schwab. Она пытается одновременно быть сторонником криптовалют и компанией, которая делает криптовалюты невидимыми. Она пытается быть одновременно мятежной и регулируемой.

Может быть, так и будет. Может быть, будущее — это регулируемая ончейн-биржа, которой так же легко пользоваться, как Venmo. Или, возможно, попытка угодить всем в конечном итоге сделает вас никому не нужным.

Это стратегия Amazon. Amazon не является лучшей ни в одной отдельной области. Это не лучший книжный магазин, не лучший бакалейный магазин и не лучший стриминговый сервис. Но она достаточно хороша во всём, чтобы большинству людей было лень идти куда-то ещё.

Однако многие компании пытались создать приложение для всего, и большинство в итоге создало беспорядочное приложение.

Если Coinbase сможет контролировать полный цикл от заработка, торговли, хеджирования, займов до платежей, то не будет иметь значения, что определённые функции немного уступают специализированным конкурентам. Издержки переключения и хлопоты управления несколькими счетами будут удерживать пользователей в её экосистеме.

Вот и всё, что касается универсальной биржи Coinbase.

Рекомендуемая литература:

Почему крупнейшая азиатская биткоин-казначейская компания Metaplanet не покупает на дне?

Multicoin Capital: наступает эра FinTech 4.0

Корнерстоун a16z, единорог Web3 Farcaster вынужден трансформироваться: является ли Web3-социальность ложной предпосылкой?