Monera Digital|Ежемесячный отчет о крипторынке за май: четыре причины ускоренного падения крипторынка

Май стал месяцем, когда крипторынок ускорил падение, столкнувшись с четырьмя ключевыми факторами.

Во-первых, произошла смена драйверов ценообразования: сначала безрисковые процентные ставки отняли право на ценообразование у криптонарративов, а затем, в конце месяца, отток капитала и распродажи инвесторов продолжили давить на цены, несмотря на смягчение макрофакторов.

Во-вторых, произошло резкое ухудшение внутренних показателей рынка. BTC-ETF в мае зафиксировали чистый отток в $24,25 млрд, третий по величине с момента запуска. Одновременно сократилась общая ликвидность в стейблкоинах.

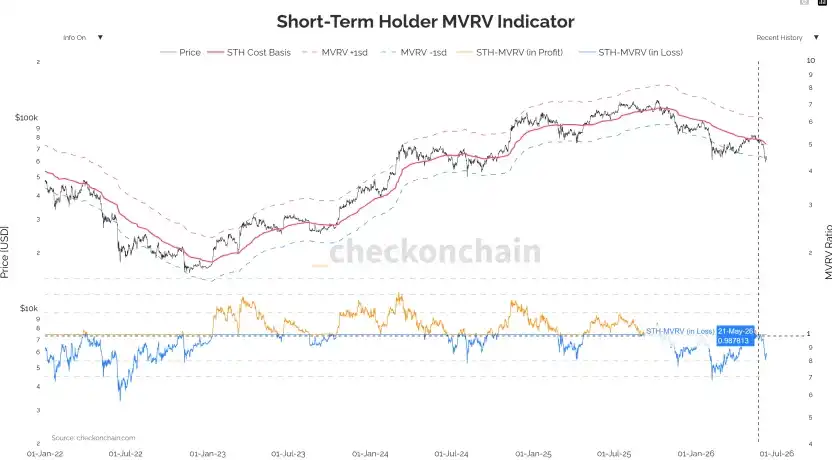

В-третьих, наступила "капитуляция" краткосрочных держателей. Показатель MVRV для краткосрочных держателей упал ниже 1,0, что сигнализирует об их совокупных убытках и является классическим признаком распродаж.

В-четвертых, деривативы сыграли негативную роль: открытый интерес и финансирование фьючерсов росли на фоне падения, что привело к масштабной ликвидации длинных позиций на сумму $3,07 млрд.

В результате BTC, начав месяц около $82,850, завершил его на уровне $73,674, потеряв ключевой уровень поддержки в $77,5 тыс. Рынок перестал реагировать на позитивные макросигналы, что указывает на доминирование внутренних процессов распродаж. Анализ показывает, что с текущими уровнями BTC вошел в историческую "зону ценности", однако для разворота тренда требуется время (3-6 месяцев) для завершения смены держателей и восстановления притока капитала.

marsbit06/09 07:49