The Blockchain Association led a broad industry push this week, asking Senate Banking leaders to resist efforts that would widen a ban on stablecoin yields beyond what Congress wrote into law.

According to the association, the letter was signed by more than 125 crypto and fintech groups and companies and was sent to lawmakers to warn against reinterpreting the new rules in a way that would also bar exchanges and apps from offering rewards tied to stablecoin holdings.

Preserving Platforms’ Ability To Offer Rewards

The coalition’s argument rests on the text of the GENIUS Act, which was signed into law earlier this year by US President Donald Trump and explicitly bars permitted stablecoin issuers from paying interest or yield directly to holders.

Reports have disclosed that the statute nevertheless leaves room for third-party platforms to provide incentives, a distinction industry groups say is intentional and important for competition.

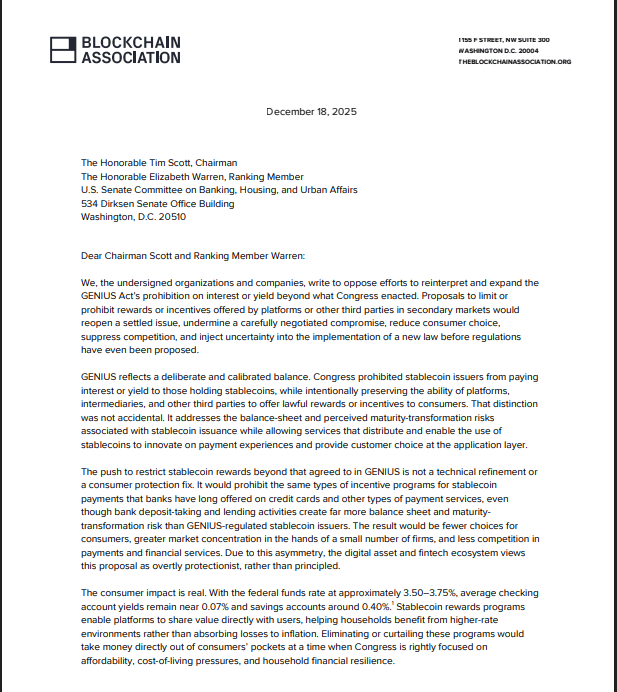

The letter pushes back against attempts to bar crypto platforms from offering yield to customers. Source: The Blockchain Association

Banks Call For Closing A Loophole

Banking groups have pushed back hard. A coalition led by the American Bankers Association and other banking trade groups asked Congress to clarify that the prohibition should extend to partners and affiliates, arguing that third-party rewards could circumvent the law and drain deposits from traditional banks.

According to recent coverage, Treasury analyses cited by bank advocates estimate that stablecoins could, in some scenarios, pull over $6 trillion from bank deposits — a figure that has become central to the banks’ case for tightening the rules.

What Industry Leaders Say

Industry spokespeople say expanding the ban would chill new services that rely on stablecoins and would tilt the market toward larger, incumbent financial firms that already control many payment rails.

Based on reports, the Blockchain Association and partner groups contend that changing the law’s interpretation now would reopen negotiations the GENIUS Act resolved and would sow regulatory confusion before agencies finish writing implementing rules.

Competition And Consumer Choice At Stake

Supporters of stronger limits say the aim is consumer protection — to stop stablecoin arrangements from becoming de-facto interest accounts that could undermine the banking system and reduce loans to households and businesses.

Other observers point out the issue could also shape which firms win in payments going forward, since restrictions on rewards would affect the commercial incentives of exchanges and fintechs.

Next Steps In Washington

Senate Banking staff are weighing letters from both sides as they consider potential fixes or clarifying language during upcoming hearings.

Regulators who must implement the GENIUS Act have been urged to issue rules that prevent evasion of the ban, and lawmakers may face pressure to either leave the law as written or to craft narrow changes aimed at banks’ concerns.

Featured image from Unsplash, chart from TradingView