Автор: José Sanchez & Kelvin Koh

Компиляция: Deep Tide TechFlow

Введение Deep Tide: В феврале 2026 года способ входа традиционных финансовых институтов в DeFi претерпел качественные изменения: это больше не заявления о стратегическом сотрудничестве, а прямая покупка управляющих токенов и маршрутизация продуктов на децентрализованную инфраструктуру.

За пять дней Citadel купила ZRO, BlackRock купила UNI и разместила BUIDL на UniswapX, Apollo обязалась в течение четырех лет приобрести до 9% предложения токенов Morpho. Spartan Group считает это настоящим переломным моментом в институционализации DeFi.

Полный текст如下:

Переломный момент институционализации DeFi

В феврале 2026 года, всего за пять дней, появилась серия знаковых институционально-криптографических сотрудничеств, которые, по нашему мнению, знаменуют качественное изменение способа участия традиционных финансов в ончейн-инфраструктуре.

Citadel Securities объявила об инвестициях в токен ZRO LayerZero; BlackRock разместила свой фонд BUIDL на сумму 2,5 миллиарда долларов на UniswapX и приобрела токены UNI; Apollo Global Management обязалась в течение четырех лет приобрести до 9% общего предложения управляющих токенов Morpho.

Ранее, 19 января, NYSE объявила о запуске платформы токенизированных ценных бумаг с поддержкой ончейн-расчетов 24/7. Модель ясна: институциональный капитал переходит от исследований к реальному ончейн-исполнению — покупке токенов, получению прав управления, маршрутизации продуктов на децентрализованную инфраструктуру.

Эта волна входа отличается от предыдущих циклов тремя моментами.

Во-первых, это прямые покупки токенов, создающие экономическое выравнивание, а не консультационные соглашения или пилотные заявления.

Во-вторых, связанные продукты являются активными и имеют реальный доход: BUIDL управляет 2,5 миллиардами долларов, Morpho поддерживает более 900 миллионов долларов активных кредитов Coinbase, LayerZero завершила расчеты кросс-чейн переводов USDT0 на сумму 700 миллиардов долларов.

В-третьих, институты выбирают публичные, разрешительные протоколы, а не проприетарные закрытые системы, что указывает на то, что компоновочность и сетевые эффекты существующей инфраструктуры DeFi более ценны, чем контроль, предлагаемый定制ными системами.

NYSE начала это представление 19 января, объявив о планах создания блокчейн-площадки для поддержки торговли токенизированными акциями и ETF 24/7 с мгновенными ончейн-расчетами, объединив свой движок сопоставления Pillar с блокчейн-системой пост-трейдинга. Хотя одобрение регуляторов все еще ожидается, а детали реализации относительно ограничены, это сигнал высшего уровня о направлении: самая знаковая фондовая биржа мира определяет ончейн-расчеты как ключевую инфраструктуру.

Затем LayerZero 10 февраля выпустила Zero, новый L1, разработанный specifically для институциональной финансовой инфраструктуры. Citadel Securities совершила стратегическую покупку токенов ZRO, что имеет большое значение для компании, обрабатывающей около 35% розничных акционных сделок в США.

DTCC исследует использование Zero для расширения своих возможностей токенизации и управления залоговыми активами; ICE оценивает использование этой цепи для инфраструктуры торговли 24/7; Google Cloud присоединяется для исследования микроплатежей AI Agent; ARK Invest одновременно владеет долей в акциях и токенах, Кэти Вуд加入顾问委员会.

Tether в тот же день также объявила об отдельной стратегической инвестиции в LayerZero Labs. Ожидается, что Zero запустится осенью 2026 года с тремя зонами: общей средой EVM, зоной платежей с акцентом на конфиденциальность и专用тной交易区.

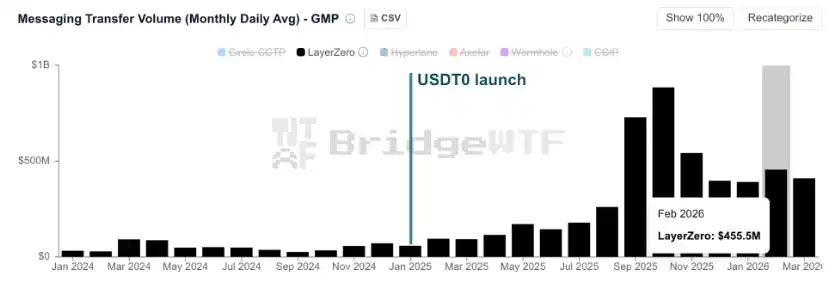

Институциональный интерес отражает уже доказанную пропускную способность. USDT0 — полноцепной стейблкоин Tether, построенный на стандарте OFT LayerZero, — с января 2025 года способствовал более чем 700 миллиардам долларов кросс-чейн переводов.

Как показано на рисунке ниже, ежедневная расчетная стоимость резко ускорилась после запуска USDT0, превратив LayerZero из уровня передачи сообщений в ключевую финансовую инфраструктуру.

Рис.: USDT0 способствовал более чем 700 миллиардам долларов кросс-чейн переводов с момента запуска

Источник: BridgeWTF

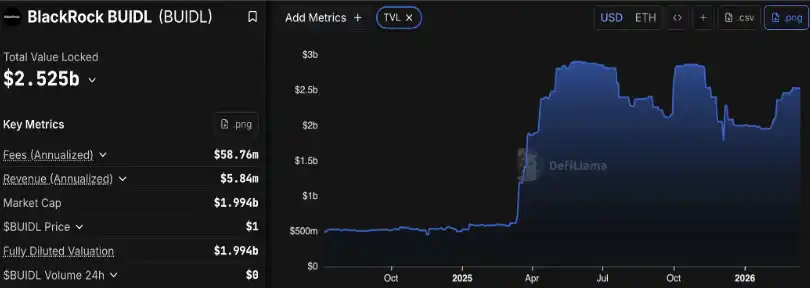

На следующий день фонд BUIDL BlackRock на сумму 2,4 миллиарда долларов (крупнейший продукт токенизированных казначейских облигаций США) был размещен и стал доступен для торговли на UniswapX, что впервые сделало продукт BlackRock доступным через инфраструктуру децентрализованной биржи.

Securitize отвечает за соответствие требованиям и белые списки, Wintermute, Flowdesk и Tokka Labs конкурируют за котировки через фреймворк RFQ UniswapX. BlackRock также раскрыла информацию о стратегической покупке токенов UNI (конкретные условия еще не公开чны), что является первым управляющим токеном DeFi в ее балансе.

Хотя порог доступа к BUIDL по-прежнему ограничен квалифицированными покупателями с минимум 5 миллионами долларов, генеральный директор Securitize Карлос Доминго заявил, что инфраструктура разработана для масштабирования до розничных продуктов с течением времени.

Решение о размещении на Uniswap отражает эволюцию BUIDL от нишевого эксперимента до продукта институционального уровня. С момента запуска в марте 2024 года с объемом 40 миллионов долларов фонд достиг пика почти в 2,9 миллиарда долларов в середине 2025 года, в настоящее время TVL составляет около 2,5 миллиарда долларов.

Рис.: Текущий TVL фонда BlackRock BUIDL составляет 2,5 миллиарда долларов

Источник: Defillama

13 февраля Apollo Global Management подписала соглашение о сотрудничестве, обязавшись в течение 48 месяцев приобрести до 90 миллионов токенов MORPHO, что составляет примерно 9% от общего предложения.

Помимо приобретения токенов (оцененных примерно в 110 миллионов долларов по ценам середины февраля), Apollo также будет сотрудничать в создании ончейн-рынков кредитования, расширяя свое присутствие в блокчейне — часть ее кредитных стратегий уже токенизирована через Securitize (ACRED) и Anemoy (ACRDX).

Эта сделка является одним из самых важных на сегодняшний день сотрудничеств между институтами и нативными протоколами DeFi.

Возможности институтов внутри Morpho не ограничиваются владением токенами. Архитектура протокола позволяет любому实体 стать куратором хранилищ для создания рынков кредитования с定制ными параметрами риска. Кураторы могут получать绩效тные сборы с генерируемого дохода и взимать управленческие сборы с AUM (上限 5%), создавая устойчивую модель дохода для институциональных участников.

Возможно, наиболее убедительной валидацией инфраструктуры является модель CeFi-DeFi «Могавк», pioneered Coinbase: розничные пользователи берут кредиты под залог BTC и ETH через интерфейс Coinbase, а Morpho выступает в качестве кредитного движка на backend, в настоящее время поддерживая более 900 миллионов долларов активных кредитов и 1,7 миллиарда долларов залога.

Это доказывает, что институциональный DeFi может быть абстрагирован и масштабирован за знакомыми потребительскими интерфейсами, и пользователям не нужно взаимодействовать с базовым протоколом.

Для Apollo экономика кураторства хранилищ, проверенные каналы распространения Coinbase и влияние на управление, полученное за счет накопления токенов, вместе составляют сильную позицию в сфере ончейн-кредитования.

Такая конвергенция подтверждает выбор дизайна разрешительных, компоновочных протоколов и указывает на устойчивый спрос на управляющие токены проектов уровня инфраструктуры.

Основные риски остаются в исполнении: одобрение регуляторов платформы NYSE и Zero еще待完成, институциональные покупки токенов могут проверить управление протоколами, разрыв между заявлениями и постоянной ончейн-активностью все еще велик. Тем не менее, направленный сигнал unmistakably clear.

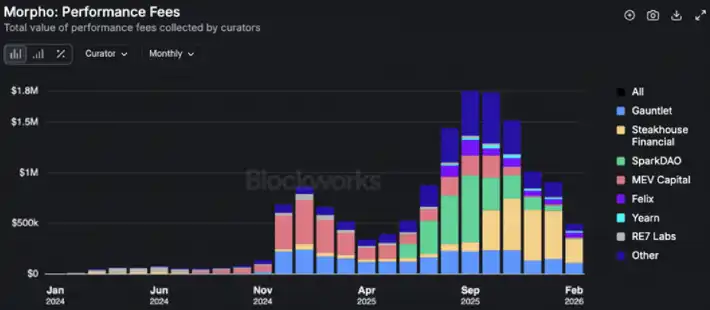

Рис.: Кураторы хранилищ Morpho уже генерируют значительный доход от сборов

Источник: Blockworks Research

В перспективе мы ожидаем углубления этих партнерских отношений после принятия закона CLARITY Act. Этот закон был принят Палатой представителей в июле 2025 года со счетом 294 против 134 и в настоящее время проходит в Сенате, где банковский комитет и комитет по сельскому хозяйству должны согласовать свои проекты до голосования в полном составе.

Основной спорный момент — обработка доходов от стейблкоинов: банковский сектор добивается ограничения выплаты процентов по остаткам стейблкоинов, в то время как криптокомпании считают, что это отправит инновации за границу.

Июль широко считается ключевым крайним сроком до августовских каникул; если он будет пропущен, следующее окно отложится до осени. После принятия CLARITY Act предоставит первую в США всеобъемлющую нормативную базу для цифровых активов, прояснит юрисдикцию SEC/CFTC, установит путь регистрации для бирж цифровых товаров и обеспечит правовую определенность для токенизированных продуктов.

Для таких протоколов, как Morpho и Uniswap, это устранит нормативную неопределенность, которая в настоящее время ограничивает масштабы институционального сотрудничества. Мы считаем, что это откроет вторую, более широкую волну интеграции TradFi-крипто.