Bitcoin is facing renewed pressure as geopolitical tensions in the Middle East reshape the macro backdrop and weigh on risk assets. Rather than responding to isolated headlines, the market is reacting to a broader shift in uncertainty, liquidity expectations, and cross-asset positioning. Price remains fragile, with rallies struggling to gain traction as participants reassess exposure in an increasingly volatile environment.

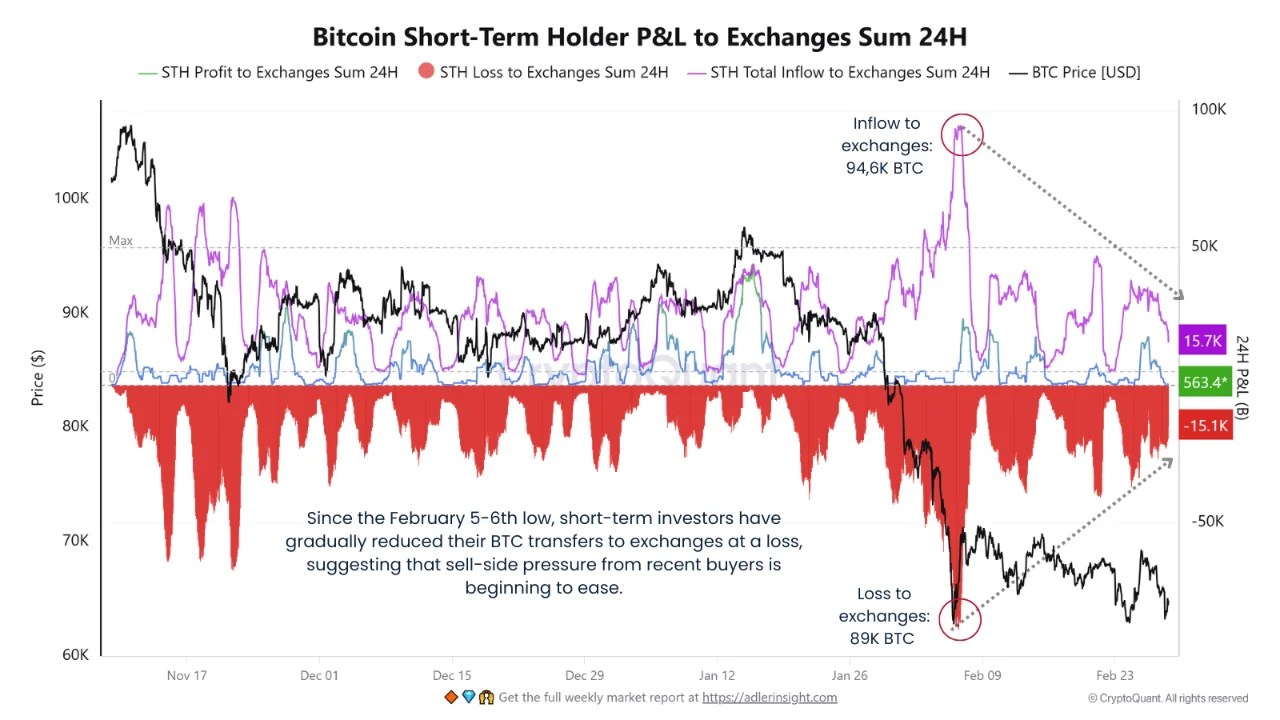

A recent CryptoQuant report sheds light on a critical behavioral shift through the Short-Term Holder (STH) P&L to Exchanges metric — a tool designed to track how the most reactive cohort is positioning. These investors, often responsible for amplifying short-term volatility, tend to transfer coins to exchanges when under stress, particularly during loss realization events.

During the February 5–6 capitulation episode, STHs sent approximately 89,000 BTC to exchanges at a loss within a single 24-hour window — a clear signal of panic-driven distribution. However, the dynamics have since evolved. Following that event, loss-driven inflows have steadily declined.

This suggests that immediate sell-side pressure from recent buyers is diminishing. The data indicate that acute panic has subsided. What remains is not aggressive accumulation, but a gradual transition from forced liquidation to relative exhaustion — a subtle yet important structural development.

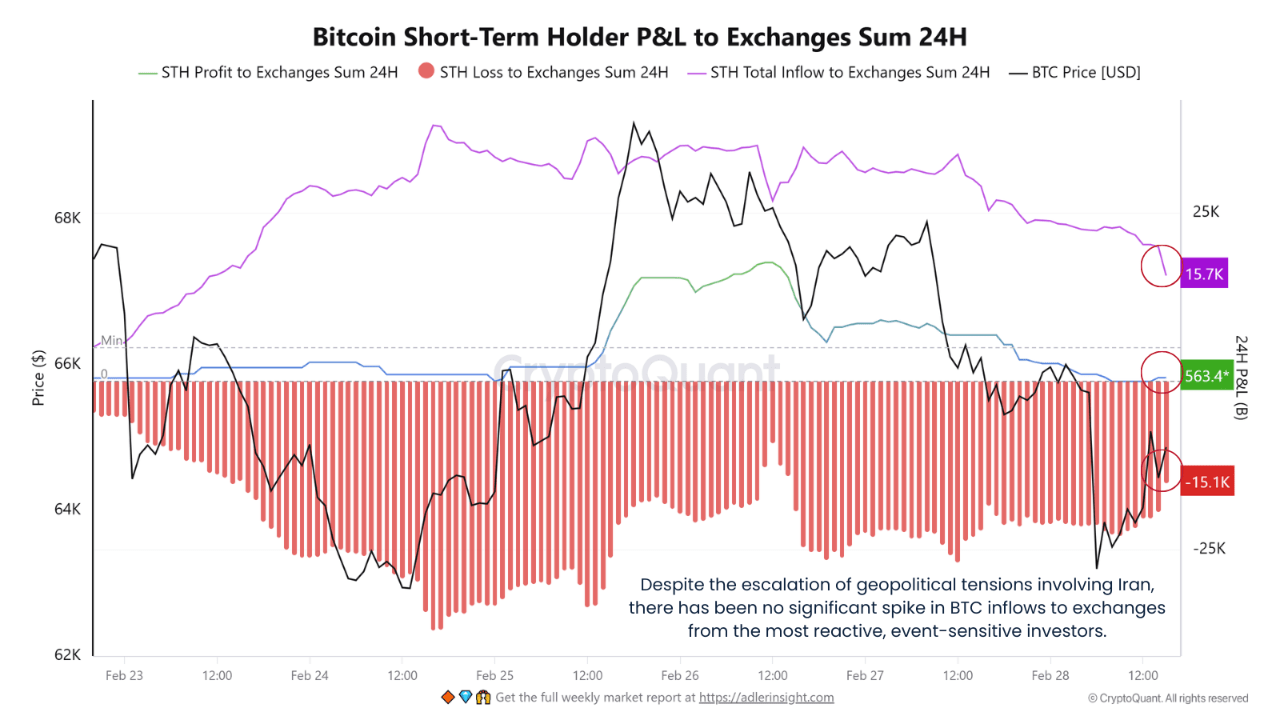

The granular view of the Short-Term Holder P&L to Exchanges metric adds nuance to the broader picture. Even amid the recent geopolitical escalation involving Iran — an event class that has historically triggered reactive risk-off flows — exchange inflows from short-term holders did not materially expand. As Bitcoin probed the $63,000–$64,000 zone, there was no corresponding spike in realized-loss transfers. For a cohort typically hypersensitive to volatility, this restraint is notable.

This behavior suggests a shift from reflexive panic to conditional holding. In prior stress episodes, similar price shocks produced visible surges in exchange-bound coins as weak hands rushed to de-risk. The absence of that pattern now implies that a meaningful portion of forced selling may already have occurred during the early-February capitulation phase.

Markets tend to stabilize only after marginal sellers are exhausted. The progressive decline in loss-driven transfers supports the thesis that liquidation pressure is being absorbed rather than re-accelerating.

Going forward, the signal to monitor is persistence. If short-term holder inflows remain muted, it would reinforce the case for seller fatigue and base-building conditions. Conversely, a renewed spike in realized-loss transfers would indicate that capitulation is incomplete, reopening the path for further downside volatility.