Несколько дней назад я прочитал о концепции из японской философии: басё (basho). Грубый перевод — «место», но философ Китаро Нисида придал ему значение, выходящее далеко за пределы географического положения, скорее напоминающее ситуацию: поле, в котором всё сущее может стать самим собой. Другими словами: человек не просто случайно оказывается где-то, а формируется тем местом, где находится. Сегодня я использую эту теорию для анализа Base.

В прошлом месяце количество активных адресов упало до минимума за 18 месяцев. Размышляя над этим явлением, я понял: Base построила лишь место, но так и не создала условий для роста и формирования вещей.

Когда Coinbase запустила Base в 2023 году, в крипто-нативном сообществе возникла редкая вера. Все считали, что она наконец решит самую старую проблему Ethereum: инфраструктура повсюду, но нет реальных пользователей. А у Coinbase есть 100 миллионов пользователей и непревзойдённые возможности дистрибуции — это уникальное преимущество. Двери открылись, и пользователи уже ждали за ними.

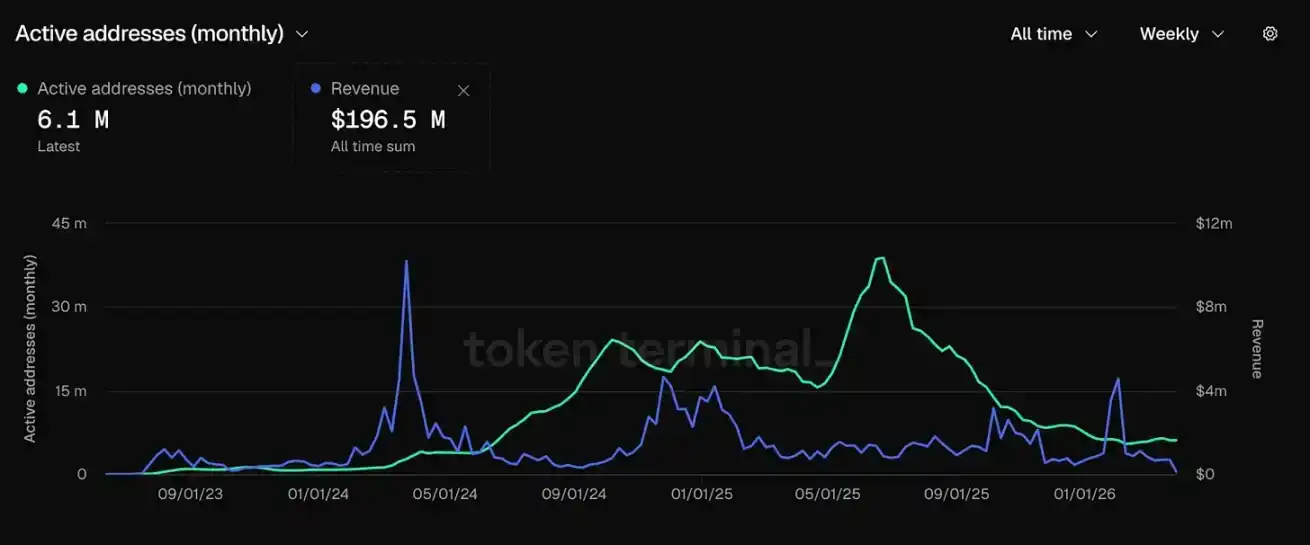

Какое-то время эта уверенность, казалось, подтверждалась. Base росла быстрее всех предыдущих Layer2. В октябре 2025 года её общая заблокированная стоимость (TVL) достигла 5,6 миллиардов долларов, а доходы от комиссий были непревзойдёнными во всей сфере L2. Таким образом, в сентябре 2025 года Base подтвердила выпуск токена, словно предвещая неизбежно успешный эксперимент. Да, место превращалось в басё (basho).

А потом пользователи ушли.

Посмотрите на данные — это нагляднее: Активные адреса Base вернулись к уровню июля 2024 года. Ожидание выпуска токена идеально удовлетворило потребности эйрдроп-охотников: получить последнюю выплату и уйти.

Ставка Base на экономику создателей в 2025 году также не сработала. Её核心 — это протокол Zora, который по умолчанию токенизирует контент. К концу года на Base через Zora было выпущено 6,52 миллиона токенов создателей и контента, из которых持续活跃 в течение всего года оставались лишь 17 800, что составляет 0,3%. Остальные 99,7% уже никому не интересны.

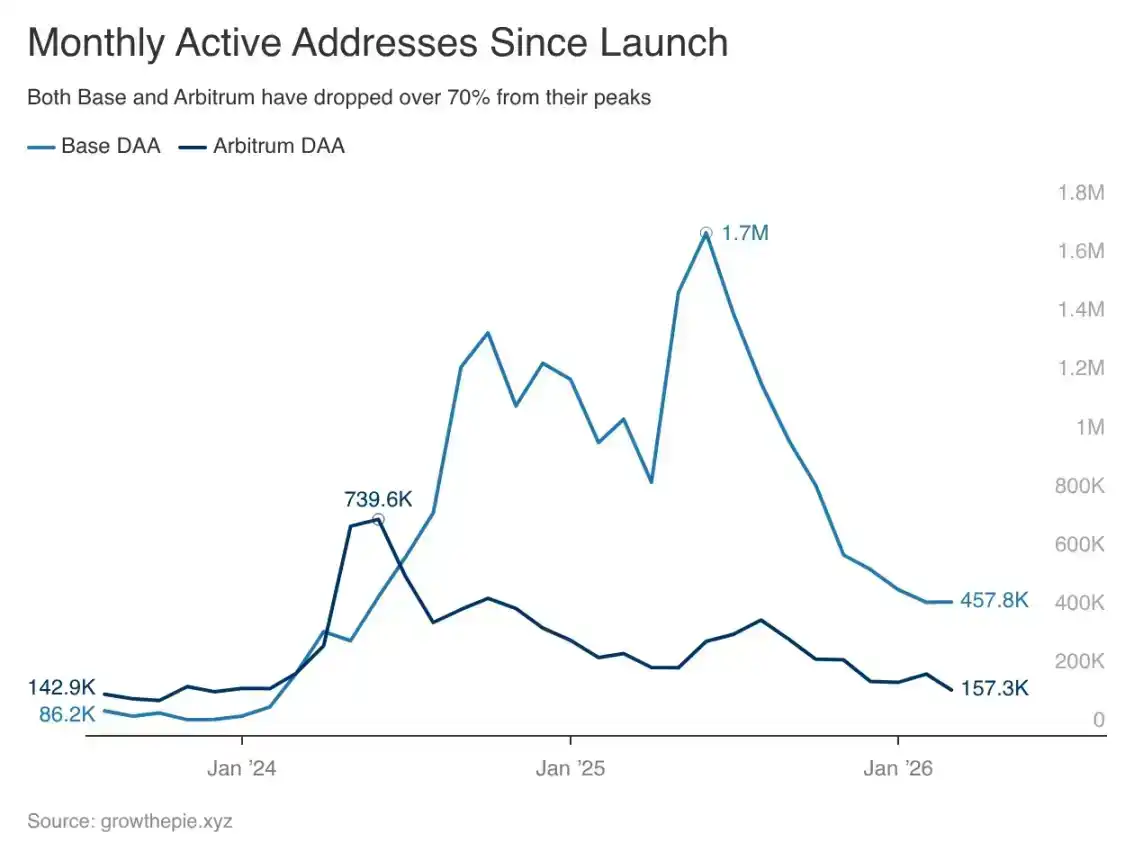

Пиковое значение ежедневных активных адресов Base пришлось на июнь 2025 года — 1,72 миллиона. К марту 2026 года осталось лишь 458 000, что означает резкое падение на 73% с пика. После того как Армстронг в сентябре 2025 года объявил, что Base рассматривает возможность выпуска токена, всего за шесть месяцев количество активных адресов сократилось на 54%, что означает полный уход спекулятивных средств.

Социолог Рэй Олденбург изучал: что заставляет людей снова и снова возвращаться в одно и то же место без всякого вознаграждения. Он называл это третьим пространством, например, бары, парикмахерские, городские площади. Это не пространства для эффективного производства, но они дают людям причину возвращаться, не связанную со стимулами. Суть в том, что желание вернуться не может быть создано искусственно, оно может только естественным образом вырасти из возможностей,长期 предоставляемых местом. Криптовалютная индустрия проектирует места с целью извлечения выгоды от пользователей, а потом удивляется, почему никто не остаётся.

Вот что такое место без басё (basho): люди заходят, берут то, что им нужно, и уходят, потому что уйти ничего не стоит. Здесь не формируется идентичность, не создаются способности, которые нельзя скопировать в другом месте за три недели, нет ничего, что сделало бы уход потерей. Существуют ли на этом блокчейне уникальные отношения? Мы никогда не строили вещи, исходя из такой логики, не так ли?

Нельзя построить басё (basho) с помощью финансовых стимулов. Стимулы, конечно, могут заманить людей внутрь, но не могут заставить их захотеть остаться. Желание остаться должно проистекать из возможностей,长期孕育ряемых местом. Нисида Китаро называл это «логикой места», referring to how the relational field shapes the things that emerge within it. Криптоиндустрия спроектировала поле для извлечения выгоды и в итоге с удивлением обнаружила, что рождается только оно.

Брайан Армстронг публично заявил, что Base App теперь сосредоточена на том, чтобы стать self-custody, торговой версией Coinbase.

Тот прежний видение социальной вовлечённости, позволяющее пользователям создавать в блокчейне идентичность, которую стоит защищать, — видение социального взаимодействия и создателей — исчезло. Судя по данным, это рациональное решение, но оно также признаёт: такое видение так и не сформировалось по-настоящему. У Base есть место, и теперь оно ориентировано только на обслуживание прошлых пользователей, потому что это всё, что оно может предложить.

Один блокчейн, одна гонка

Base — это самый заметный缩影 модели L2.

С июня 2025 года использование небольших и средних L2 в целом сократилось на 61%. Большинство сетей beyond the top three превратились в зомби-сети: достаточно активные, чтобы не закрываться, но слишком тихие, чтобы иметь значение. Соотношение ежедневной активности L2 к L1 снизилось с 15 раз в середине 2024 года до 10–11 раз сегодня. Использование большинства новых L2 резко падает после окончания цикла стимулирования. Вся экосистема L2 остывает, не только Base.

Дорожная карта, ориентированная на Rollup, когда-то была теорией о пользовательском adoption: снизить стоимость участия → приток пользователей → формирование экосистемы → сложный рост. Фонд Ethereum в этом году выпустил 38-страничный документ с изложением видения будущего направления Ethereum. Крупнейший по активности L2 достиг дна и покинул OP Stack, а второй по величине L2 остановился в росте.

Снижение входного барьера не равно созданию условий для формирования вещей. Отрасль решила проблему «входа», но приняла как должное, что «чувство принадлежности» появится само собой. Оно не появляется автоматически, потому что принадлежность — это не функция, которую можно запустить.

Farcaster — это продукт, наиболее близкий к построению басё (basho) в криптомире. Потому что определённая группа людей создала на нём определённую культуру: разработчики делятся работами, обсуждают Ethereum, формируют мнения друг о друге в течение месяцев. На это нужно время, конкуренты не могут скопировать это более высокими вознаграждениями. Friend.tech пытался сделать то же самое с помощью激励机制, достиг вершины за неделю, умер за месяц. Те же механизмы, но культура не сформировалась. Разница не в продукте, а в том, остался ли кто-то достаточно надолго, чтобы что-то真正 сформировалось.

Что может удержать людей?

Цепочки, которые удерживают пользователей в условиях зимы, полагаются не на более щедрые стимулы.

Пик ежедневных активных адресов Arbitrum пришёлся на июнь 2024 года — 740 000, сейчас их 157 000, что также означает резкое падение на 79%. Обе цепи идут на спад, но лежащая в основе логика完全不同.

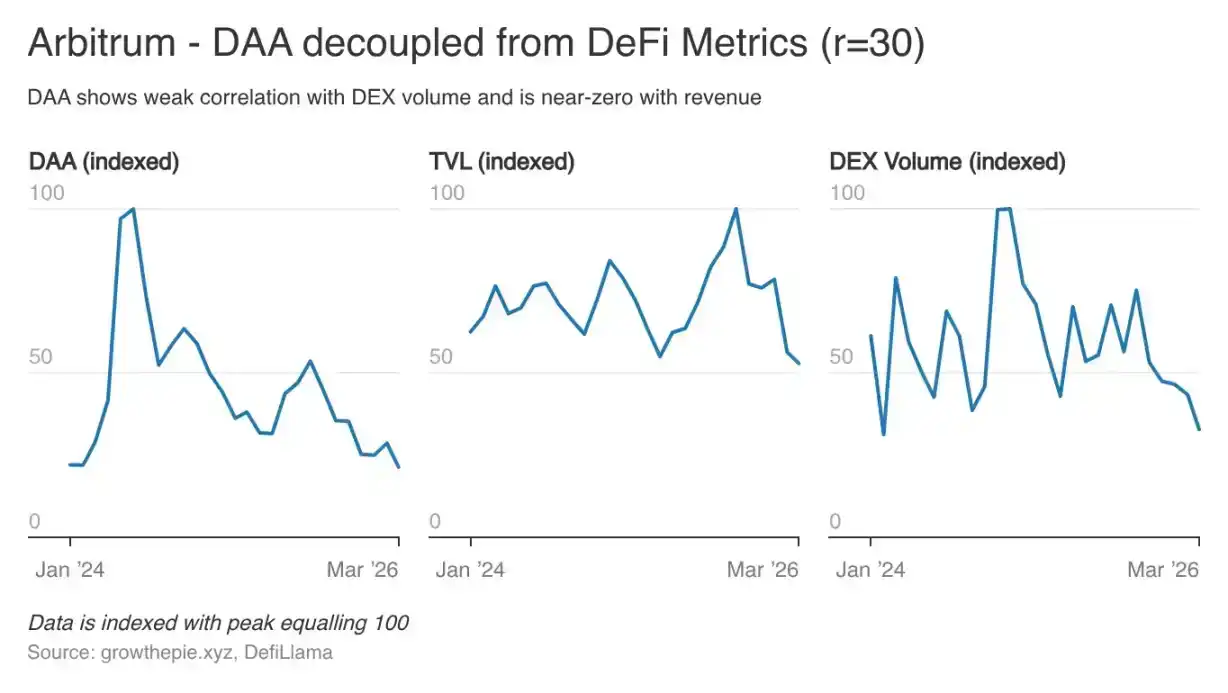

Пользователи Base заходят, чтобы торговать, и когда объёмы торгов падают, они уходят. А на пользователей Arbitrum уровень комиссий не влияет, корреляция между количеством пользователей и доходами от комиссий几乎 равна нулю. Base привлекает туристов, а Arbitrum почему-то сумел удержать пользователей.

Hyperliquid устоял, потому что его торговый опыт уникален, и сообщество сформировало идентичность, которой нет больше нигде. Стимулы в виде токенов几乎 не имеют значения, пребывание в нём стало частью их поведения и идентичности. Вещи формируют пользователей, а пользователи, в свою очередь, формируют вещи.

Криптоиндустрия всё ещё оптимизирует «как заставить людей прийти», а вопрос «как создать ситуацию» вспоминают только после обвала данных, его никогда не учитывают при проектировании цепи с самого начала.

Я считаю, что Base обладала самой сильной в истории способностью к дистрибуции и могла бы решить эту проблему лучше любой другой цепи.

Теперь это торговое приложение. Это разумное направление продукта, но это то, чем уже занимаются более 40 продуктов. Торговое приложение не может породить басё (basho), оно может порождать только сессии: пользователи заходят, когда есть потребность торговать, и уходят после завершения.

Чтобы стать по-настоящему успешным приложением, необходимо установить持续ную связь. Нужно, чтобы пользователи建立или отношения между每一次访问ами, чтобы下一次访问 ощущался как возвращение, а не просто прибытие.

Трансформация Армстронга во многом основана на уроках, извлечённых Base из данных. Социальный слой, экономика создателей, ончейн-идентичность — всё это, что должно было превратить Base из «используемого» в «обитаемое», — требовало терпения, а система не вознаграждала терпение.

Экосистеме Ethereum нужно, чтобы Base была не просто местом для торговли. Основа整个叙事 L2 заключается в том, что цепи могут стать инфраструктурой, вокруг которой люди строят свою жизнь. Если L2 с самыми сильными в истории криптовалют возможностями дистрибуции в конечном итоге довольствуется ролью более быстрой Coinbase, то сама эта叙事 несостоятельна.

Нисида Китаро считал, что самый глубокий басё (basho) — это место, где границы между self и местом начинают растворяться. Вы не можете полностью отделить «кто вы» от «где вы сформированы». Это звучит абстрактно, но применительно к публичному блокчейну это означает: пользователь не может представить свою финансовую жизнь вне определённой цепи; все инструменты разработчика основаны на какой-то экосистеме; их идентичность几乎 не может существовать в другом месте.

Насколько мне известно, такое никогда не строилось ни на одном L2. Возможно, это вообще невозможно построить в рамках программ стимулирования.

Даже если у вас есть 100 миллионов потенциальных пользователей, но нет ничего, ради чего стоит остаться, в конечном счёте место опустеет. Теперь Base это поняла.