Анализ: Macro_Lin

Недавно я прочитал специальный отчет, опубликованный Банком Кореи (BoK), под названием «Обзор устойчивости глобального подъема в полупроводниковой отрасли». Этот отчет особенный.

Южная Корея является крупным экспортером чипов памяти, и финансовые отчеты Samsung и SK Hynix в некотором роде являются отчетами о национальной экономике для BoK. Когда этот центральный банк лично берется серьезно обсуждать, как долго может продлиться нынешний суперцикл полупроводников, движимый ИИ, сама эта позиция заслуживает внимания. Отчеты продавцов имеют свою позицию, медвежьи отчеты полны эмоций, а документ BoK выдержан в сдержанном тоне центрального банка, с гораздо более высокой плотностью аргументов, чем плотностью эмоций.

Ключевой вывод

Банк Кореи считает, что масштабы и продолжительность дисбаланса спроса и предложения в текущем цикле памяти значительно превышают показатели трех предыдущих циклов, и расширение определенно продолжится как минимум до первой половины 2026 года. Однако, начиная с 2027 года, пять переменных будут совместно определять момент разворота, и два самых тревожных сигнала уже появились.

1. Чем этот цикл отличается от трех предыдущих

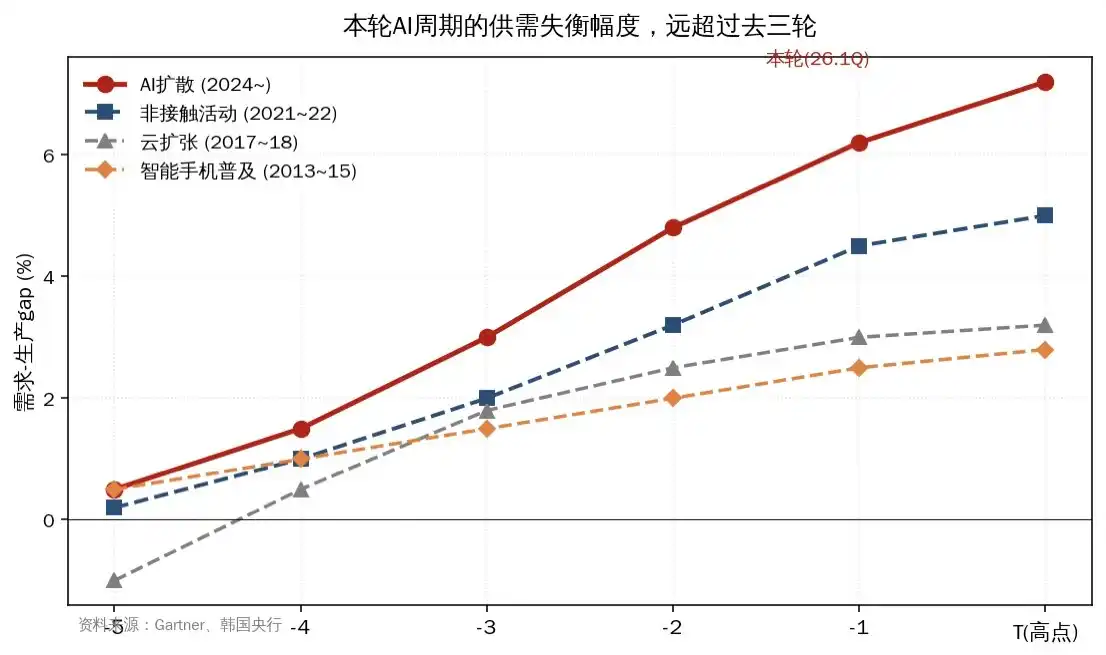

BoK разделяет циклы полупроводников с 2010 года на четыре этапа: распространение смартфонов (2013-2015), расширение облачных технологий (2017-2018), пандемийный бесконтактный период (2020-2021) и нынешний этап распространения ИИ (2024 г. по настоящее время).

Сценарий предыдущих трех циклов был одинаковым. Новые технологии стимулировали спрос, предложение с запаздыванием подтягивалось, после концентрированного ввода расширенных мощностей предложение превышало спрос, накапливались запасы, цены падали, и цикл разворачивался. После 2017 года эта точка разворота сильно совпадала с переломным моментом в CAPEX крупных американских технологических компаний.

Отличия этого цикла заключаются в трех моментах.

Во-первых, самый быстрый рост спроса в истории. HBM взлетел вместе с взрывным ростом установок AI-акселераторов, а универсальный DRAM также поднялся благодаря спросу на inference, происходит синхронный рост по всем категориям.

Во-вторых, самая низкая эластичность предложения в истории. Техпроцесс HBM сложен, цикл расширения производства длительный. Производители памяти, пережившие кровавую баню 2022-2023 годов, консервативны в расширении производства. Линии по производству универсального DRAM перепрофилируются под HBM, что еще больше усугубляет дефицит универсальной продукции.

В-третьих, результат. BoK создал ключевой график, на котором разрыв между спросом и производством (demand-production gap) для четырех циклов изображен в одной системе координат, масштабы и продолжительность дисбаланса в текущем цикле значительно превышают показатели трех предыдущих циклов. Уровень запасов на стороне производства и спроса DRAM снижается, признаков накопления нет.

Рис. 1: Сравнение разрыва между спросом и производством в предыдущих циклах полупроводников, масштабы текущего цикла ИИ значительно превосходят исторические

2. Пять переменных, определяющих, как далеко зайдет цикл

BoK предоставляет четкую framework из пяти факторов: три со стороны спроса, два со стороны предложения. Я расскажу в порядке важности.

1. Сроки проверки рентабельности инвестиций в ИИ. Сейчас OpenAI, Anthropic работают в убыток, оценки и инвестиции поддерживаются ожиданиями рынка относительно будущего доминирования. Суждение BoK очень тонкое: начиная со следующего года, внимание рынка сместится с захвата территории на возможность зарабатывать деньги. В сочетании с такими рисками, как ограничения по электроэнергии в дата-центрах, ускоренная амортизация GPU и недостаточная загрузка, темпы роста CAPEX будет трудно поддерживать в текущем ритме.

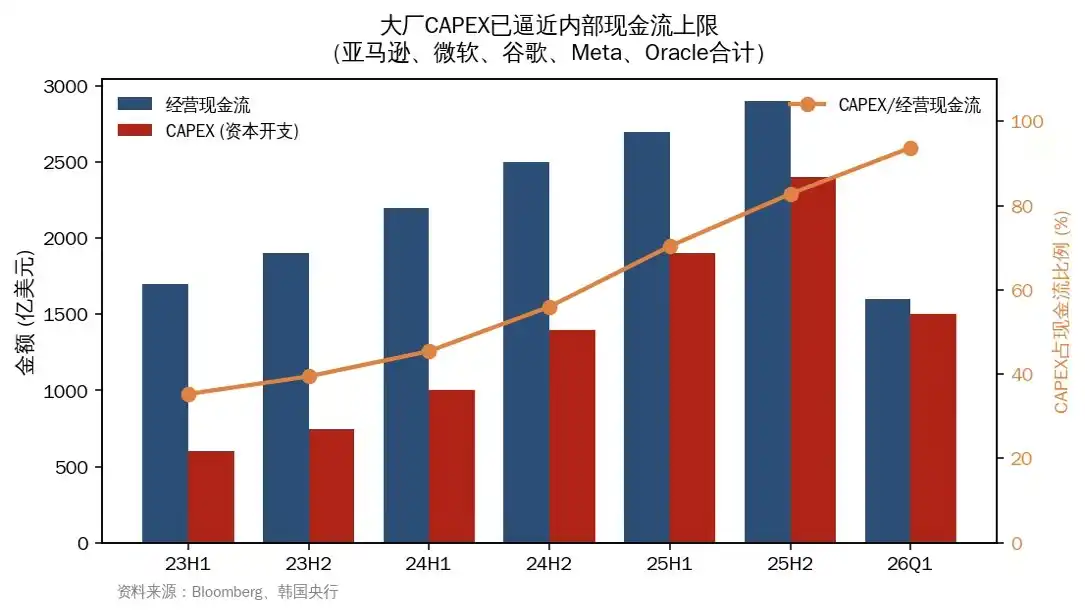

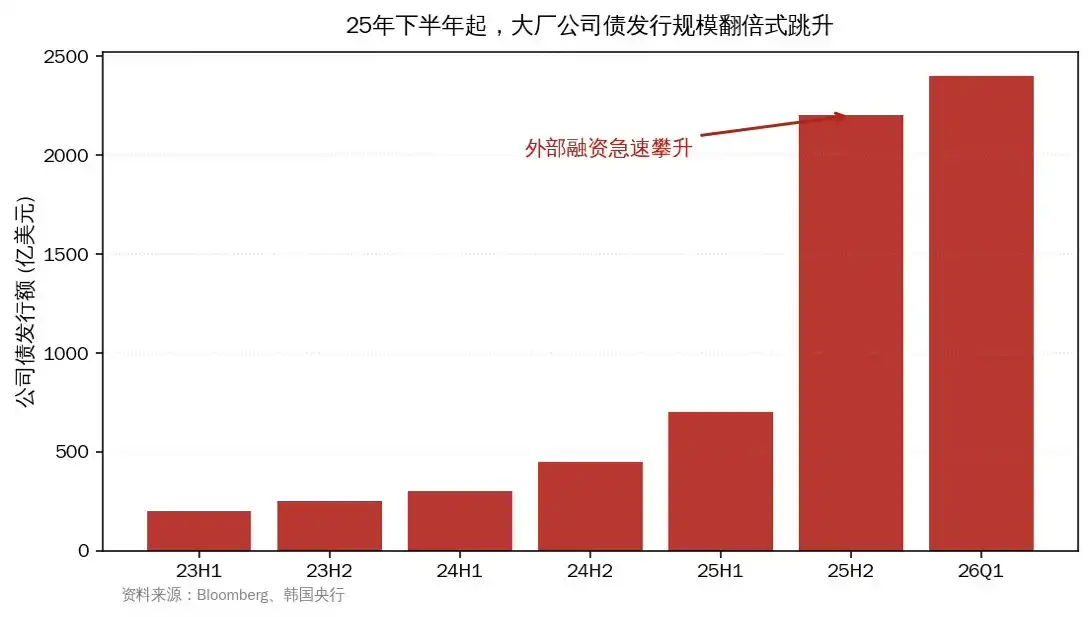

2. Сможут ли крупные компании продолжать привлекать финансирование. Эта часть является самой информативной во всем отчете. BoK прямо проводит параллель между настоящим моментом и пузырем телекоммуникаций конца 1990-х годов и указывает на ухудшающийся факт: внутренних денежных потоков крупных компаний уже недостаточно для поддержки CAPEX такого масштаба. Со второй половины прошлого года крупные компании сократили выкуп акций, значительно увеличили выпуск корпоративных облигаций, спреды CDS некоторых компаний уже расширились.

Рис. 2: Операционный денежный поток крупных компаний уже не покрывает CAPEX, доля выросла с 25% до почти 100%

Рис. 3: Со второй половины 2025 года объем выпуска корпоративных облигаций резко вырос, внешнее финансирование стало основным источником пополнения

Еще более тревожным является само поведение в области финансирования. Компании Neocloud (например, CoreWeave) намного меньше крупных компаний, но они вынуждены постоянно закупать GPU и строить AI-дата-центры, NVIDIA предоставляет им кредитную поддержку для стимулирования продаж своих GPU. Эта структура highly similar to тому, как Cisco, Lucent предоставляли vendor financing новым телекоммуникационным компаниям.

Есть также уровень внебалансового финансирования. Дата-центр Meta Hyperion через SPV и частный кредит, обязательства на 29,5 миллиарда долларов не попали в баланс Meta. Oracle Stargate объемом 66 миллиардов долларов, xAI Colossus на 20 миллиардов долларов используют similar структуры. BoK упоминает деталь: в феврале-марте 2026 года такие учреждения, как Blue Owl, BlackRock, Morgan Stanley, Cliffwater, уже приостановили погашение паев некоторых фондов частного кредитования из-за опасений disruption от ИИ. Это трещина.

3. Прогресс в эффективности ИИ-моделей. После DeepSeek быстро появились технологии экономии памяти, такие как квантовое сжатие, MoE, Mamba, CMX от NVIDIA, TurboQuant от Google. BoK честно признает неопределенность двунаправленного воздействия. Повышение технологической эффективности может как снизить удельный спрос, так и, благодаря парадоксу Джевонса, увеличить общий спрос. В общей таблице оценок BoK этот фактор помечен двунаправленной стрелкой, это единственный из пяти факторов, который нельзя定向 определить.

4. Скорость расширения мощностей основных производителей памяти. В этом году Samsung P4, SK Hynix M15X уже исчерпали существующие чистые комнаты, но этого仍然不足. Реальное окно высвобождения предложения — вторая половина 2027 года. SK Hynix в Йонгине, новый завод Micron заработают во втором полугодии 2027 года, Samsung P5 — в 2028 году. Это жесткое ограничение со стороны предложения, которое можно внести в календарь.

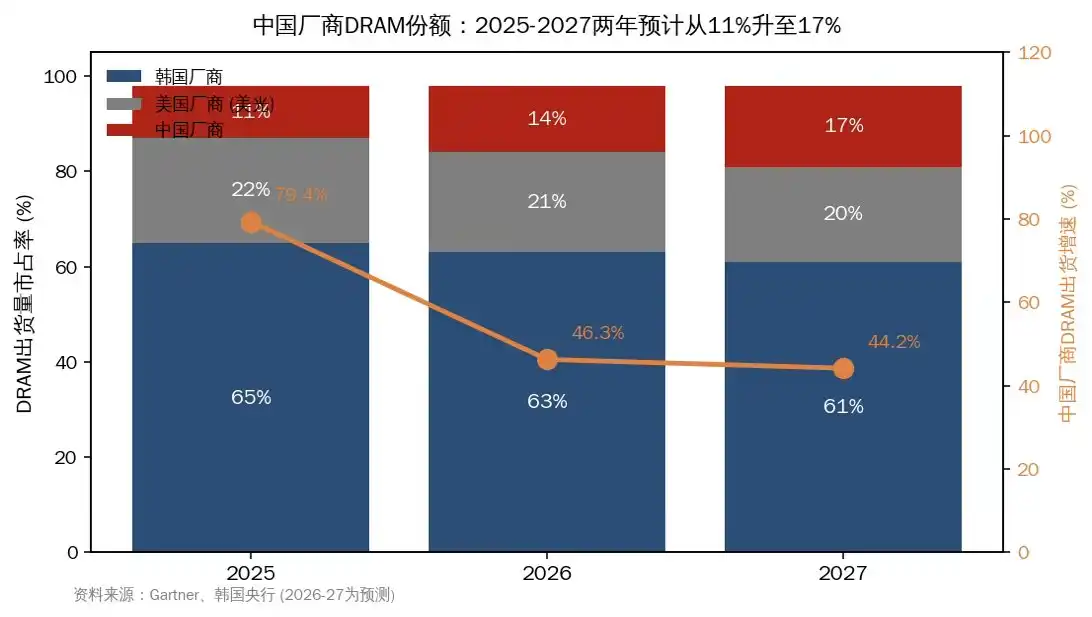

5. Скорость догоняющего развития китайских производителей. BoK оценивает технологический разрыв между Китаем и Кореей примерно в 4 года, как для HBM, так и для универсального DRAM. Поэтому ситуация на высоком конце в краткосрочной перспективе не изменится. Но есть цифра, на которую стоит обратить внимание: доля китайских производителей в поставках DRAM может вырасти с 10,5% в 2025 году до 17% в 2027 году, темпы роста в течение следующих двух лет более чем в 3 раза выше, чем у основных производителей памяти. Эта доля будет давить на цены универсального DRAM, ускоряя момент выравнивания дисбаланса.

Рис. 4: Доля китайских производителей DRAM выросла с 11% до 17%, темпы роста поставок намного опережают основные компании по производству памяти

3. Относительно войны на Ближнем Востоке, оценка BoK более冷静, чем можно представить

В настоящее время нет никаких признаков отсрочки строительства дата-центров или замедления предложения памяти. Цикл инвестиций в ИИ主导ляется крупными американскими компаниями, 74% строящихся дата-центров находятся в Америке, корреляция между глобальной экономикой и полупроводниками за последние два года значительно ослабла.

Но BoK перечисляет несколько потенциальных каналов transmission. Рост цен на нефть увеличивает операционные расходы дата-центров, ужесточение финансовых условий повышает сложность привлечения financing для крупных компаний, перебои с поставками сырья и оборудования (бром, гелий) с Ближнего Востока, если Тайвань из-за энергетических проблем повлияет на производство системных чипов, это затормозит и память. Самое прямое негативное воздействие — на стороне потребления, Gartner уже прогнозирует, что в 2026 году из-за роста цен на память поставки ПК сократятся на 10,4% в годовом исчислении, смартфонов — на 8,4%.

4. Собираем временную шкалу

В конце BoK использовал матрицу цветных блоков, чтобы визуализировать силу влияния пяти факторов в 2026, 2027 и 2028 годах. Я переведу содержание этой таблицы в временную narrative.

2026 год, структура, где спрос доминирует, а предложение ограничено, продолжается. Это самый определенный год.

2027 год, противоречия начинают накапливаться. Давление на financing крупных компаний растет, расширение производства в Китае ускоряется, новые заводы еще не запущены, но уязвимость в financing уже暴露лена.

2028 год, Samsung P5, SK Hynix в Йонгине, новый завод Micron集中释放, риски со стороны предложения значительно放大.

Небольшое продолжение

По-настоящему интересное в этом отчете — это его narrative方式. Центральный банк, для которого память является национальным достоянием, не восхваляет собственную отрасль, а тратит много места на обоснование хрупкости структуры financing, двунаправленной неопределенности технологической эффективности и微妙转折点 2027 года на временной шкале. Эта сдержанность сама по себе является позицией.

Проведенное им сравнение с телекоммуникационным пузырем — это часть отчета, которую я перечитал несколько раз. Сценарий тех времен был таков: сильный первоначальный спрос в сочетании с конкурентным расширением производства, плюс более быстрая, чем ожидалось, технологическая инновация (WDM Wave Division Multiplexing), в конечном итоге pushed отрасль в состояние быстрого перепроизводства. Сегодня в индустрии ИИ присутствуют все три условия, разница лишь в том, что еще не появилась та критическая технология, эквивалентная WDM.

Когда внутренние инвесторы关注于 индустриальную цепочку памяти, фокус привычно падает на такие вещи со стороны предложения, как выход годных HBM, прогресс CXMT. Этот отчет BoK возвращает взгляд на другую сторону: настоящая переменная этого цикла находится на стороне спроса, точнее, скрыта в устойчивости финансирования индустрии ИИ. Vendor financing Neocloud, внебалансовый leverage SPV, приостановка погашения паев фондов частного кредитования — эти сигналы deserve более пристального внимания, чем любой график расширения производства.

По крайней мере, до первой половины 2026 года история продолжается. Последующий сценарий будет зависеть от того, как разыграются пять упомянутых выше переменных.