In April 1976, three men signed the partnership agreement for Apple Inc. in a California garage. Twelve days later, one of them withdrew from the partnership. If he had not quit and endured the long half-century, his 10% stake would be worth $400 billion today. That sum would be enough for him to buy half of the oil empires in the Middle East, or to rub Elon Musk into the ground twice on the Forbes rich list.

This man's name is Ronald Wayne. When the public discusses the 50-year history of Apple, they tend to deify the persistence of Steve Jobs and Steve Wozniak, and then casually mock Wayne's cowardice and shortsightedness for selling his shares for a mere $800.

However, Wayne, then 41, was the only one among the three who had a proper job, assets, and even a family. Jobs, at the time, was willing to mortgage everything just to borrow money for parts. Looking at this long-haired young man with a dazed look in his eyes, Wayne felt nothing but unease. Because if this company went bankrupt, under the partnership laws of the time, creditors would let go of the two penniless young men and legally take every car, every house, and every cent of savings under Wayne's name.

Wayne's exit was a rational calculation by an ordinary person facing "extreme uncertainty." He retreated to his safe life.

Wayne withdrew from Apple out of fear of risk, and the irony of history is that Apple, over the next 50 years, became another Wayne.

This company表面上 shouts "Think Different," but its bones are极其 averse to risk. Wayne left Apple because he disliked risk, and from then on, geniuses were responsible for creating myths, while the system was responsible for eliminating uncertainty. Apple's 50 years is not just a story about "genius changing the world," but also a victory of the system over the individual, of calculation replacing inspiration.

If the early Apple relied on Jobs's personal heroism to combat risk, then how did this behemoth, once truly grown, use hundreds of billions of real dollars to buy absolute security in the capital markets?

A "Hedge Fund" Disguised as a Tech Company

Jobs极度 hated dividends and stock buybacks. In his view, every penny Apple earned should be reinvested in R&D. Even in 2010, when Apple's cash reserves were already enormous, he stubbornly refused to budge under pressure from Wall Street.

But after Jobs's death, the new CEO, Tim Cook, succumbed to shareholder pressure and on March 19, 2012, announced Apple's first-ever dividend and a stock buyback plan worth tens of billions of dollars. From that day on, in the eyes of Wall Street, Apple gradually transformed from a world-changing tech company into a "hedge fund" disguised as a tech company.

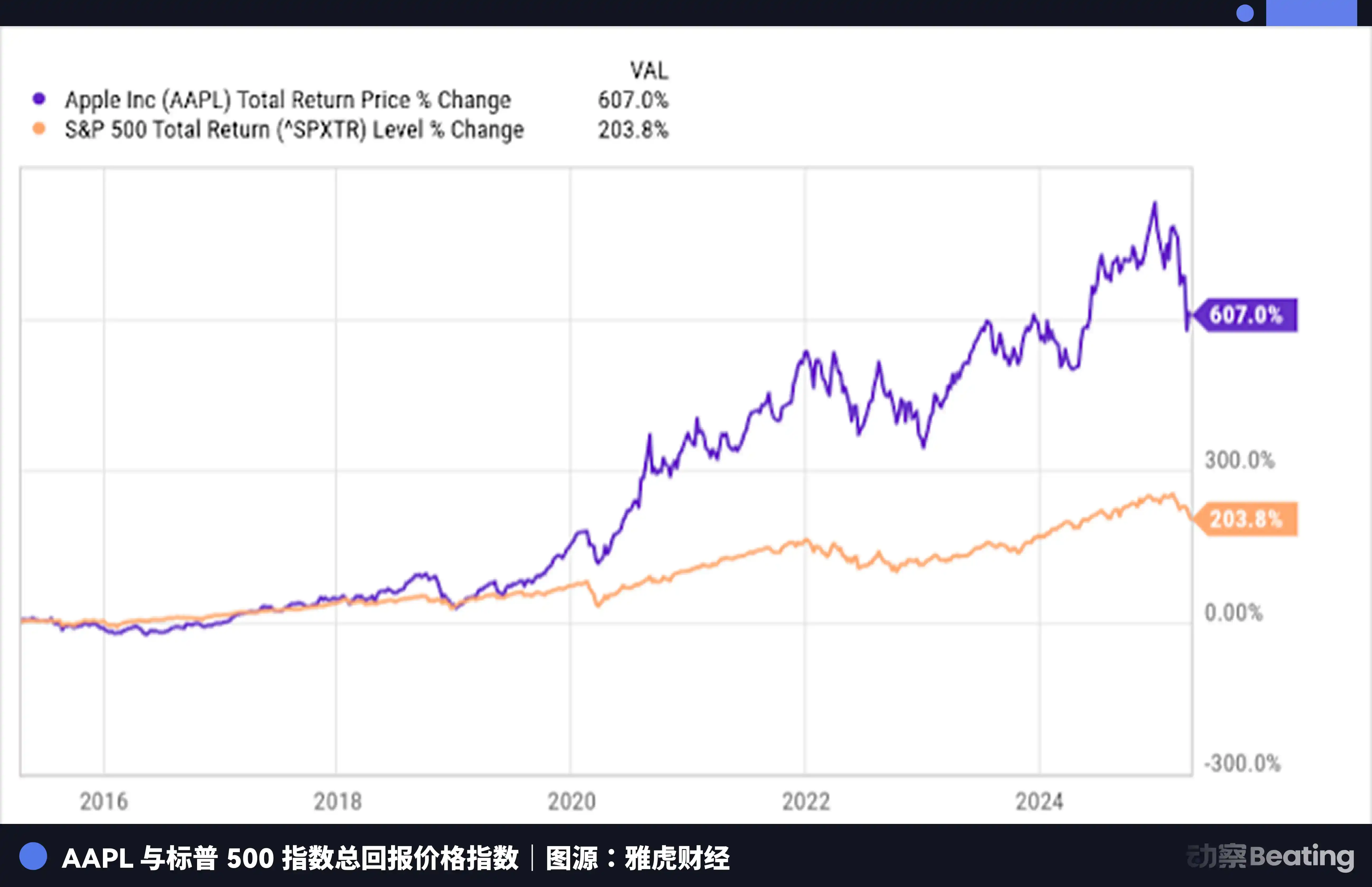

According to statistics from Creative Planning and major financial institutions, from 2013 to the end of 2024, Apple's total stock buybacks reached $700.6 billion.

Among the constituents of the S&P 500 index, this figure exceeds the total market capitalization of 488 of them. In other words, the money Apple used to buy its own stock is enough to directly buy any listed company outside the top 13 in the global market cap rankings, such as Eli Lilly, Visa, or Netflix.

And when we look at the current AI frenzy, where Amazon, Google, and Meta are burning through nearly $700 billion疯狂 on AI large language models and computing power, trying to gamble on an uncertain future at a table where the cards are unclear, Apple is using a comparable amount of money to buy its own stock.

Technological innovation is risky; you might throw down a hundred billion and not even hear a sound. But reducing the number of shares outstanding and boosting earnings per share is 100% certain on the financial statements. Over the past decade, although Apple's net profit growth has slowed, its EPS has been artificially inflated by nearly 280% through疯狂 buybacks.

Warren Buffett heavily invested in Apple in recent years, even making it the absolute heavyweight in Berkshire Hathaway's portfolio, accounting for over 20% at one point. The old man wasn't buying the growth potential of a tech stock; he was buying the absolute certainty provided by this精密 machine during a period of technological平庸. In the mature stage of an industry cycle, financial engineering makes money much faster and more steadily than technological R&D.

It no longer needs a earth-shattering product to astonish the world; it just needs to act like a tireless pump, siphoning up profits and then precisely channeling them into Wall Street's reservoir.

On the financial statements, Apple bought absolute certainty with $700 billion. But the profits that support this massive numbers game—how are they squeezed out from the assembly lines in the physical world?

The Great Supply Chain Migration

In March, Tim Cook appeared in China once again, beaming. He drank Chinese afternoon tea and said to the camera with a smile: "China's supply chain is critical to Apple. We could not have achieved what we have today without Chinese suppliers."

But behind this warm and fuzzy PR rhetoric, Apple is quietly carrying out an epic supply chain migration.

In 2025, the number of iPhones assembled in India reached 55 million, a暴增 of 53% from the previous year. This means that now, one out of every four iPhones produced globally comes from India.

Tata Group just built a huge new factory in Hosur, Tamil Nadu, southern India, planning to double its workforce to 40,000 people; and Foxconn's factory in India exported $4.4 billion worth of iPhones to the US in just the first five months of 2025. The latest iPhone 17 series has even achieved the breakthrough of having all models assembled in India.

The reason behind the supply chain shift is not as simple as "searching for cheaper labor." It is surgery performed by the Apple system to eliminate geopolitical uncertainty and single-node risk. Apple treats the global supply chain like a motherboard design—wherever there is risk, it pulls out the capacitor from there and plugs it into a safer place.

In this process, whether it's the workers on the Foxconn assembly lines in China who once created "Zhengzhou speed," or the young labor force in the Hosur factory in India who have just put on anti-static clothing, there is essentially no difference within Apple's system. They are all just gears on this庞大 machine, replaced seasonally.

Apple cares about the stability and cost of the gears' operation. It死死 holds the product design rights in its spaceship headquarters in California, but perfectly outsources the dirty and hard work of production and management conflicts to Foxconn and Tata. In this impregnable supply chain system, all suppliers and workers are just consumables that can be replaced at any time.

After achieving this窒息 control in the physical world, how will this behemoth apply its old tricks to the most ferocious AI wave in the digital world?

The Toll Booth on the Road to the Gold Mine

In 2024, the generative AI wave swept across, and ChatGPT made the whole Silicon Valley exclaim that the "iPhone moment" had arrived again. Analysts were嘲笑 Apple: Siri is like an idiot, Apple is落后 in the AI era, Apple is finished.

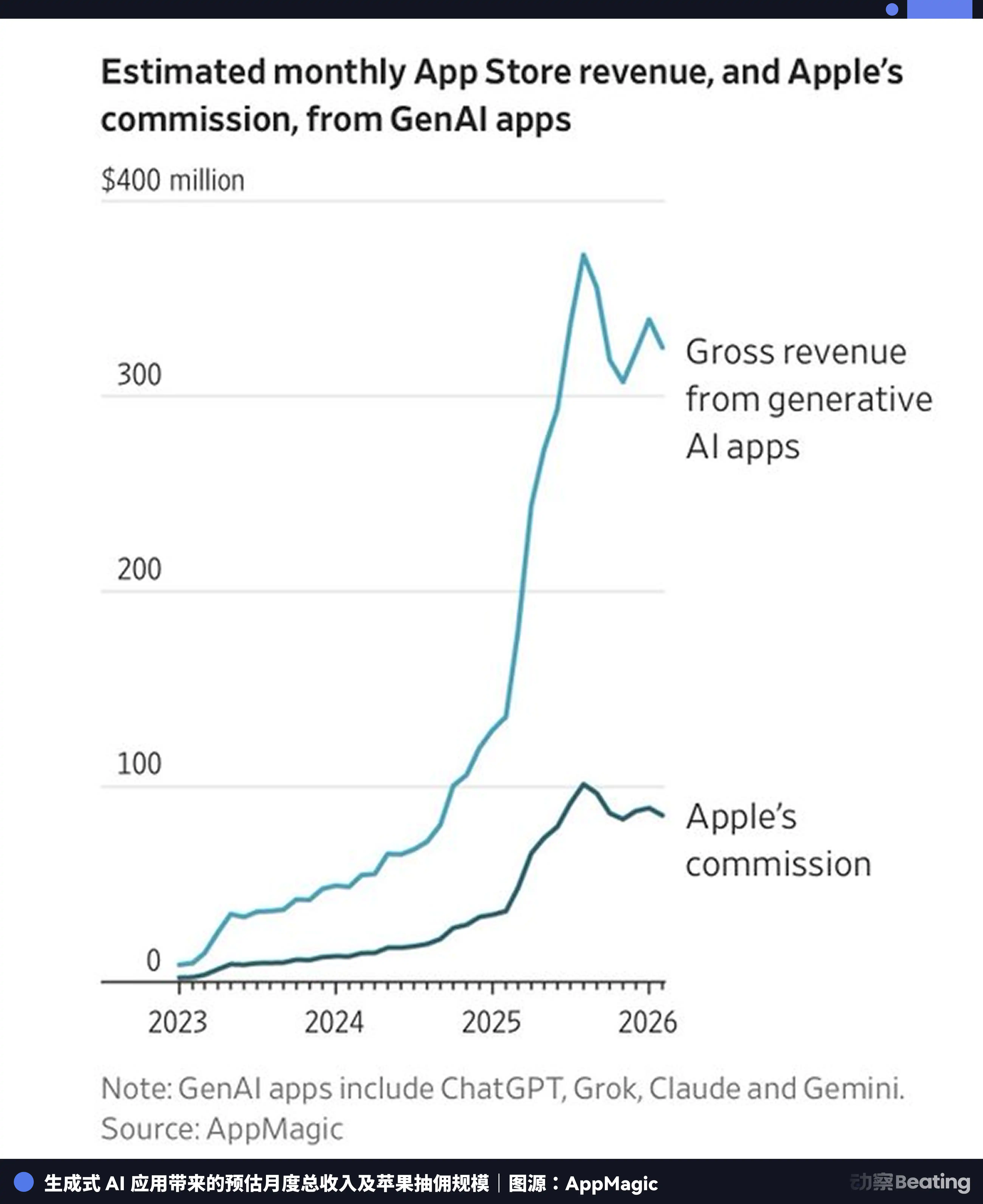

But by 2026, when AI large language model companies were bleeding money on computing power and worrying themselves bald about commercial monetization, a piece of data from AppMagic surprised everyone.

In 2025, generative AI apps paid nearly $900 million in commissions to Apple just to be able to be listed on the App Store, the so-called "Apple Tax." Of this, nearly 75% of the money was paid by ChatGPT alone. Musk's Grok ranked second, contributing 5%.

This is Apple's most terrifying aspect. It may not have built the shovels for the gold rush, but it directly controls the only road to the gold mine and built a toll booth.

Whether you are Claude or OpenAI, if you want to reach billions of high-net-worth iOS users globally, you must乖乖 listen to Apple and faithfully hand over 30% (or 15%) of your revenue to Cook. In the狂热 AI bubble, Apple used a近乎流氓 force of ecosystem monopoly to forcibly transform all AI innovation试图颠覆 it into steadily growing service revenue on its own financial reports.

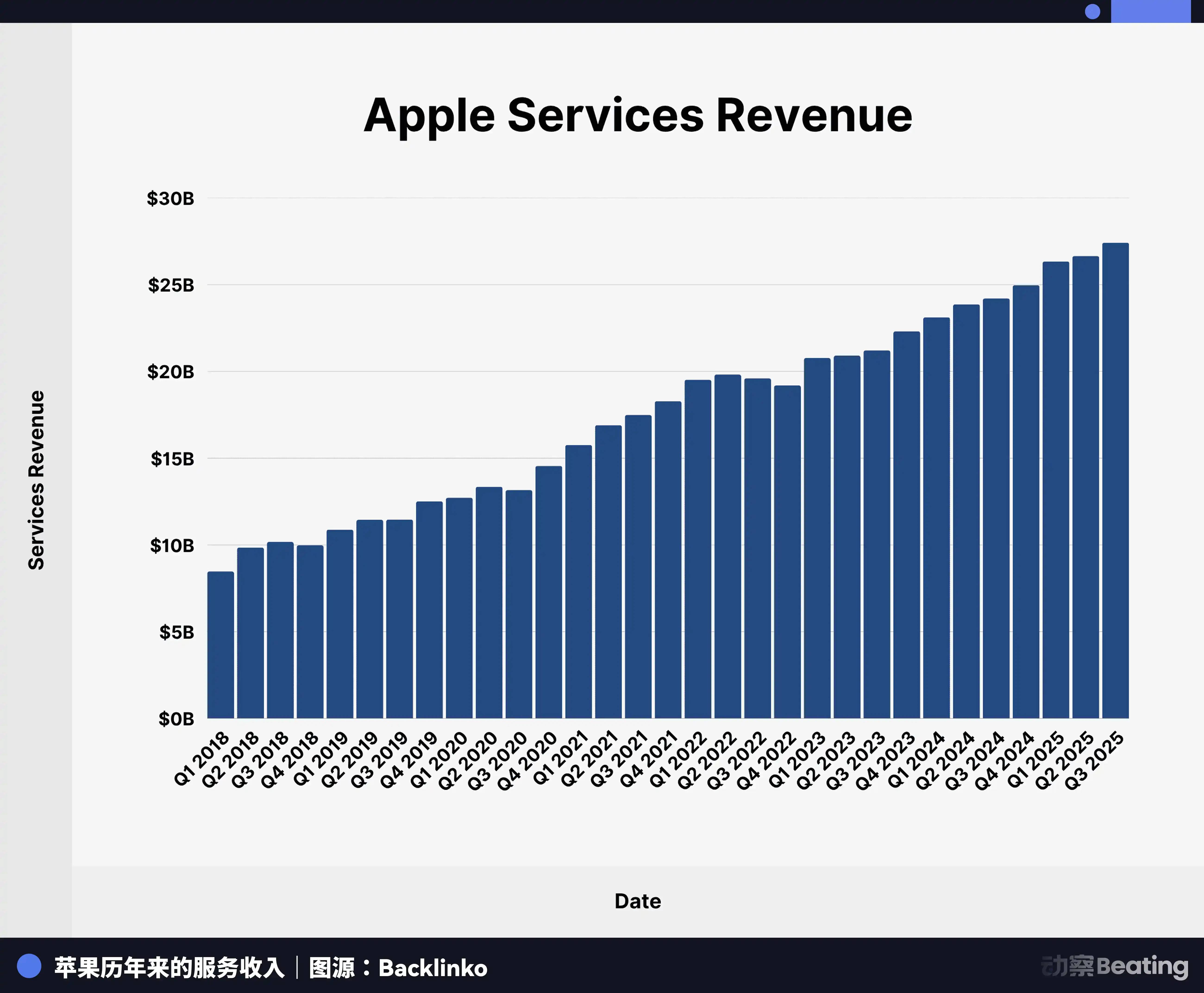

In the fourth quarter of fiscal year 2025, Apple's service revenue hit a historic high of $28.8 billion, a year-on-year increase of 15%. Among this, the AI apps seen as Apple's disruptors by the outside world contributed the most succulent piece of profit.

Of course, this kind of behavior has also attracted the hammer of antitrust. On March 15, 2026, facing huge regulatory pressure, Apple罕见 conceded in the Chinese market, reducing the standard App Store commission from 30% to 25%, and the commission for small developers from 15% to 12%. But this doesn't hurt its fundamentals at all.

From the supply chain in the physical world to the App Store in the digital world, Apple has mastered systemic control to the化境. When this machine becomes精密 to the extreme, does the person in the driver's seat still need to be a genius?

The Final Victory of the Cooks

At the 50th anniversary milestone of Apple, the biggest gossip in Silicon Valley isn't some revolutionary new product, but Cook's successor.

All clues point to one name: John Ternus.

This 50-year-old Senior Vice President of Hardware Engineering at Apple is practically a carbon copy of Tim Cook. He graduated from the University of Pennsylvania in 1997 with a degree in Mechanical Engineering, joined Apple in 2001, and has been there for 24 years. His resume is clean, devoid of Jobsian madness like going to India to find a spiritual guru, or those eccentric anecdotes.

A deep dive by The New York Times wrote that when Ternus was promoted, the company arranged a private office with a door for him, but he refused. He chose to continue sitting in the open-plan workspace, mixing with his engineering team. He is pragmatic, low-key,极其注重 team collaboration, and even in key decisions like pushing for iPadOS and the LiDAR radar in the iPhone Pro, he has shown a商人's calculation of "finding absolute balance between product definition and commercial interest."

If Ternus successfully takes over, this will be the final physical severance of Apple from "personal heroism."

The market always迷恋 dreammakers like Jobs, who descend like gods,劈开 chaos with dazzling light, telling you what the future looks like. But what truly supports the seamless operation of a four-trillion-dollar empire are the Tim Cooks拿着算盘,抠到极致 every penny and every screw.

When Cook took over Apple, the company's market cap was $349 billion. Fifteen years later, amidst骂声 of "no innovation," he pushed Apple's market cap to a peak of nearly $4 trillion, an increase of more than tenfold. He didn't rely on flashes of inspiration, but on毫厘之间的 squeezing of the supply chain, the极致 use of financial buyback tools, and the近乎霸道 rent collection of the App Store ecosystem.

Ternus's ascension means Apple has completely given up the search for the next dreammaker. This company has fully embraced Cook's philosophy: in the mature stage of the tech industry,平庸 operational genius is more critical than brilliant product genius.

We miss Jobs because we miss the era when technology could still make hearts race; we can't do without Cook because we have become accustomed to technology being as stable, boring, but indispensable as tap water.

Apple's 50 years began with an ordinary man, Wayne, who was afraid to take risks, and ended with a超级 system that is极其精密,庞大, and厌恶一切 uncertainty. It used $700 billion in buybacks to eliminate capital risk, a global supply chain migration to eliminate manufacturing risk, App Store tolls to eliminate technological obsolescence risk, and finally, it used Ternus to replace Cook, eliminating the risk of "people."

Fifty-year-old Apple has finally become the冷酷,精密, and most profitable Big Brother in the screen it itself smashed with a hammer in 1984.

The genius exits, the machine lives forever.