Автор: Deep Tide TechFlow

24 мая пост о Hyperliquid Strategies (NASDAQ: PURR) вызвал оживленные обсуждения в англоязычном CT:

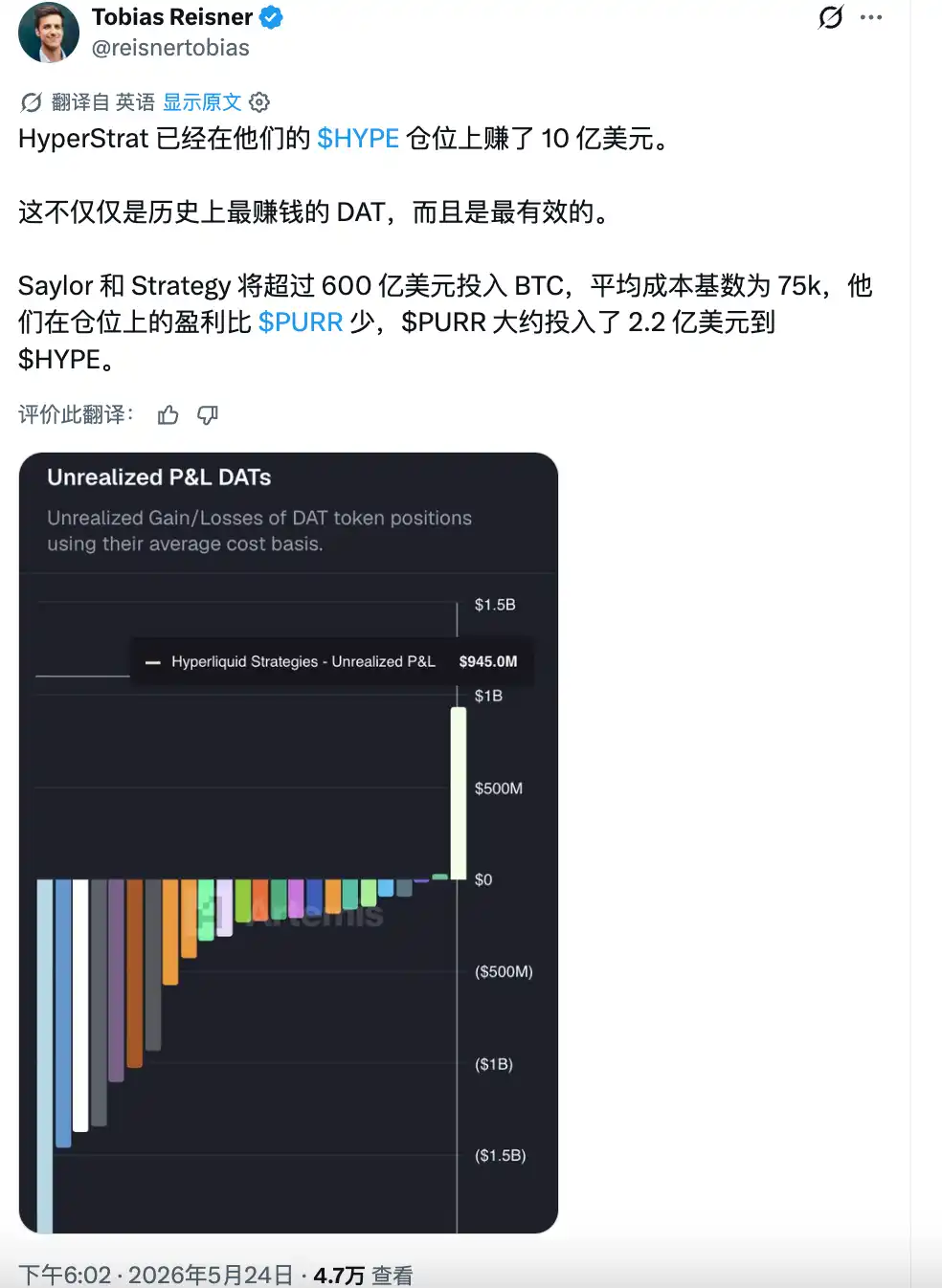

Эта компания примерно на $220 млн приобрела HYPE, и текущая нереализованная прибыль приближается к $1 млрд, что даже превышает эффективность прибыли Майкла Сайлора от BTC в компании Strategy (ранее MicroStrategy).

Сейчас эта тема постепенно распространяется и в китайскоязычном сегменте. HYPE недавно достиг исторического максимума выше $62, рост за год превысил 150%, что делает его одним из самых сильных основных криптоактивов в этом году.

PURR, будучи на данный момент единственной публичной компанией, предоставляющей доступ к HYPE, с начала года также вырос более чем на 100%, что закономерно делает ее объектом FOMO при исследованиях на рынке акций США.

Однако прежде чем следовать тренду, нужно разобраться в нескольких вопросах:

1. Что это за компания на самом деле?

2. Чем она отличается от прямого приобретения HYPE?

3. Выдерживает ли утверждение о «превосходстве капитальной эффективности над MicroStrategy» детальную проверку?

$PURR: чистая DAT

Сначала вывод: PURR — это не компания с реальным бизнесом, а, по сути, упакованный в акции продукт, основанный на $HYPE.

Ее бизнес-модель можно описать одной фразой: покупать HYPE, стейкать HYPE, держать HYPE. По открытой информации на апрель 2026 года, компания владеет примерно 20 млн HYPE, имеет около $113 млн наличных и нулевой долг.

Это означает, что вся стоимость этих акций зависит от одной вещи — цены HYPE.

Поскольку анализировать здесь нечего, остается рассматривать такие компании только по двум параметрам: сам базовый актив и то, кто управляет этой оболочкой.

Последнее определяет способность к капитальным операциям: когда проводить допэмиссию для покупки монет, когда выкупать акции для поддержки цены, как управлять соотношением премии/дисконта между ценой акции и чистой стоимостью активов... Это также определяет, готовы ли институциональные средства использовать этот инструмент.

Исторически PURR была предшественницей Sonnet BioTherapeutics, небольшой биотехнологической компании, котирующейся на NASDAQ. В июле 2025 года было объявлено о слиянии с Rorschach I, в декабре того же года сделка была завершена с общей оценкой в $888 млн, компания была переименована в Hyperliquid Strategies, а тикер изменен на PURR.

Стоит отметить, что инициатором этой сделки выступили Paradigm и Atlas Merchant Capital.

Paradigm — один из ведущих венчурных фондов в криптоиндустрии, инвестировавший в такие проекты, как Uniswap, Blur, Friend.tech, и глубоко вовлеченный в экосистему Hyperliquid, в данном случае непосредственно участвовавший в создании SPAC.

Atlas Merchant Capital — инвестиционная компания в сфере финансовых услуг из Нью-Йорка и Лондона, двое ее основателей заняли ключевые позиции в PURR: председатель совета директоров Боб Даймонд — бывший генеральный директор Barclays, генеральный директор Дэвид Шамис — бывший партнер JC Flowers.

В совет директоров также входят бывший президент Федерального резервного банка Бостона Эрик Розенгрен и бывший операционный директор Нью-Йоркской фондовой биржи Ларри Лейбовиц. Среди других участников — Galaxy, D1 и Pantera, все они являются ведущими институтами в области криптовалют и макроэкономики.

В то время как руководство большинства DAT-компаний происходит из криптосообщества, в PURR почти все — ветераны традиционных финансов.

Сильный $HYPE, взлетающий $PURR

Непосредственной причиной того, что PURR привлекла внимание китайскоязычного сегмента, стала сама сила HYPE.

HYPE вырос примерно с $25 в начале года, в мае пробил отметку в $62, установив новый исторический максимум, прирост за год превысил 150%. На фоне бокового движения BTC и слабых результатов ETH и SOL в этом году, HYPE стал самым ярким среди основных криптоактивов.

В наших предыдущих статьях мы уже разбирали базовую замкнутую экосистему Hyperliquid: около 70% доли рынка perp DEX, еженедельный доход от комиссий превышает $10 млн, 97% комиссий протокола направляется на выкуп и сжигание HYPE — эта маховик до сих пор ускоряется.

(Рекомендуем прочитать: «Наблюдение за рынком: от HYPE до ZEC, уловите 4 нарративные линии, стоящие за недавним ажиотажем вокруг альткойнов»)

Растет HYPE — растет и PURR.

Как единственный на данный момент инструмент на рынке акций США, предоставляющий доступ к HYPE, PURR с начала года вырос более чем на 100%, поднявшись с уровня около $3 до недавнего максимума в $8,79.

Для инвесторов, у которых есть только аккаунты на рынке США и нет прямого доступа к крипторынку, PURR — практически единственный выбор для получения экспозиции к HYPE. Но то, что превратило PURR из «нишевого актива» в «тему в соцсетях», — это несколько институциональных сигналов, активно поступавших с мая.

Goldman Sachs в документах 13F за первый квартал раскрыл покупку примерно 650 тыс. акций PURR, сумма хоть и небольшая (около $3,3 млн), но само имя Goldman Sachs уже является знаком доверия. В то же время спотовые ETF на HYPE от 21Shares и Bitwise были листингованы на NASDAQ и NYSE, а Cantor Fitzgerald повысил целевую цену PURR с $6 до $8.

Эти события, наложенные на временной промежуток достижения HYPE новых максимумов, вывели PURR в поле зрения большего числа людей.

Затем последовал пост, упомянутый в начале статьи: PURR купила HYPE на $220 млн, а текущая нереализованная прибыль приближается к $1 млрд; если считать за короткий период, эффективность использования капитала определенно превышает показатели MicroStrategy.

На фоне сильного роста неизбежно приходит повышенное внимание. Однако, если вы планируете работать с этой акцией, стоит проявлять осторожность.

Самая высокая капитальная эффективность среди DAT. Правда ли?

Strategy (бывшая MicroStrategy) инвестировала более $60 млрд в BTC при средней цене около $75 тыс.; PURR потратила всего около $220 млн на покупку HYPE, а нереализованная прибыль близка или даже превышает прибыль первой. Вывод: «капитальная эффективность» PURR намного выше, чем у MicroStrategy?

С цифровой точки зрения здесь все верно, но логически это вводит в заблуждение.

Средняя стоимость ранних позиций PURR по HYPE составляет около $7, текущая цена — $62, рост почти в 9 раз. Средняя стоимость BTC у Strategy — около $75 тыс., а BTC сейчас находится примерно на этом же уровне, почти не изменившись.

Таким образом, более высокая нереализованная прибыль PURR связана не с тем, что компания провела более умные операции, а просто с тем, что рост базового актива находится в совершенно другой весовой категории. Любой, кто в то же время вложил бы те же деньги напрямую в спотовый HYPE, получил бы такую же доходность, не беря на себя риски разводнения акций.

Другими словами, это победа «правильного выбора монеты». Если бы время основания PURR сдвинулось на полгода вперед, и вход был бы на уровне HYPE в $40, эта история о «капитальной эффективности» полностью бы развалилась.

Для инвесторов на рынке акций США, которые только сейчас обратили внимание на PURR, более практичный вопрос: покупая PURR сегодня, вы платите цену выше или ниже стоимости HYPE, которой владеет компания?

Это затрагивает ключевой оценочный показатель DAT-компаний — mNAV (скорректированная чистая стоимость активов на акцию).

Мы взяли данные с официальной панели управления PURR и из документов SEC и сделали быстрый расчет mNAV.

В настоящее время компания владеет 20,8 млн HYPE (около $1,296 млрд по текущей цене), плюс $114 млн наличных, после вычета отсроченных налоговых обязательств и других обязательств чистая стоимость активов составляет примерно $1,34 млрд.

Если рассматривать только выпущенные 134,6 млн акций, NAV на акцию составляет около $9,98, текущая цена акции — $7,67, дисконт около 23%. Если учесть все существующие варранты (около 29,8 млн штук) и полностью разводненные примерно 155 млн акций, NAV на акцию составляет около $8,66, дисконт около 11%. Однако компания только что зарегистрировала 35,16 млн новых акций для допэмиссии; если все они будут выпущены, знаменатель увеличится примерно до 190 млн акций, NAV на акцию упадет до $7,07, а цена акции, наоборот, превратится в небольшую премию в 1,08 раза.

Таким образом, «дешевы» или «дороги» акции PURR, зависит от того, насколько большим вы считаете будущее разводнение.

Сама по себе допэмиссия не обязательно плоха. Если руководство выпускает акции при высокой премии и использует привлеченные средства для покупки большего количества HYPE, количество монет на акцию фактически увеличится. Но если рыночные настроения охладеют и цена акции упадет ниже NAV, а допэмиссия продолжится, это будет разводнять существующих акционеров.

Этой компании всего полгода, она еще не прошла полный нисходящий цикл, и нет исторических данных, по которым можно было бы судить, как руководство будет действовать в экстремальных условиях.

Также стоит отметить, что в приведенном выше расчете используется отсроченное налоговое обязательство в размере $60,5 млн на дату окончания отчетности за 3-й квартал (31 марта). Но с конца марта HYPE значительно вырос, поэтому налоговые обязательства, соответствующие нереализованному приросту, скорее всего, еще больше увеличились, и фактический NAV может быть несколько ниже нашего расчета.

В чем разница между покупкой PURR и прямой покупкой HYPE

Это самый практичный вопрос. Если вся стоимость PURR происходит от HYPE, зачем мне нужен промежуточный слой вместо прямого приобретения HYPE?

Ответ прост: для части инвесторов прямое приобретение невозможно. Пенсионные счета США (IRA, 401k), счета в традиционных брокерских компаниях, а также некоторые институциональные средства со строгими требованиями к соответствию не могут напрямую владеть криптоактивами.

Более того, платформа Hyperliquid прямо запрещает использование резидентами США.

Таким образом, PURR предоставляет упакованный в акции, листингованный на NASDAQ инструмент, позволяющий этим средствам получить экспозицию к HYPE через стандартные биржевые операции. Оболочка, созданная Paradigm, по сути, продает именно этот канал соответствия требованиям.

Если вы относитесь к этой категории инвесторов, PURR действительно на данный момент почти единственный вариант. Хотя спотовые ETF на HYPE от 21Shares и Bitwise уже были листингованы в середине мая, эти продукты появились совсем недавно, их ликвидность и ошибка отслеживания еще нуждаются в наблюдении.

Но если у вас есть возможность напрямую купить HYPE, то упаковка в виде акций PURR становится чистыми издержками, несущими негативный эффект; это нельзя назвать дополнением к бета-доходности HYPE.

Эти издержки проявляются на нескольких уровнях:

Во-первых, риск разводнения. При прямом владении HYPE ваша доля не может быть разводнена другими. Но при владении акциями PURR компания в любой момент может выпустить новые акции для покупки большего количества HYPE.

Во-вторых, неполная передача доходности. При прямом владении HYPE вы можете самостоятельно стейкать и получать доход от стейкинга, будущие аирдропы и стимулы экосистемы также поступают напрямую. При владении через PURR доход от стейкинга сначала поступает на счет компании и лишь после вычета операционных расходов и налогов косвенно отражается в чистой стоимости на акцию.

В-третьих, время торговли и издержки ценообразования. HYPE торгуется 24/7, PURR обращается только в часы работы рынка акций США. Если HYPE испытывает значительные колебания в выходные или после закрытия торгов, держатели PURR могут отреагировать только после открытия.

В-четвертых, риск контрагента. Как раскрывается в документах SEC, все позиции PURR по HYPE хранятся у одного кастодиана. При владении через PURR безопасность ваших активов зависит от способности этого кастодиана выполнять обязательства и непрерывности операционной деятельности компании.

По мнению автора, PURR больше похожа на «продукт-канал», а не на «инвестиционный продукт». Ее ценность заключается в создании канала от традиционных финансовых счетов к HYPE, и только. Если вам не нужен этот канал, то каждый дополнительный риск, приносимый промежуточным слоем, является излишним.

Таким образом, для китайскоязычных инвесторов в криптовалюты и акции США вывод довольно прямой:

Вам нужно решить, верите ли вы в HYPE, а не в то, верите ли вы в оболочку PURR.