Автор | Odaily Planet Daily (@OdailyChina)

Автор | Azuma (@azuma_eth)

292 миллиона долларов — это общая сумма украденных средств rsETH Kelp DAO; 17,2 миллиарда долларов — это объем средств, выведенных из Aave с момента инцидента.

Aave из-за своей крайне глупой стратегии управления кризисом позволяет паническим настроениям в сообществе разгораться в течение нескольких дней, теряя свое самое большое преимущество в кредитном сегменте — многомиллиардные объемы замороженных средств и ярлык «самого безопасного DeFi» в сознании пользователей.

- Примечание Odaily: предысторию см. в статьях «DeFi снова взломали на 292 миллиона долларов, неужели даже Aave больше не безопасен?»; «Трехсторонняя игра с дырой в 290 миллионов: кто заплатит — Aave, L0 или Kelp?».

В чем ошибся Aave?

Детали инцидента с Kelp DAO уже не стоит обсуждать, бессмысленно винить Aave за слишком высокий LTV для rsETH. Здесь я хочу, с точки зрения долгосрочного пользователя AAVE, обсудить стратегию реагирования Aave после инцидента.

Во-первых, проблема масштаба плохих долгов. Aave сам подсчитывал. В зависимости от различных вариантов обращения с rsETH, возможны два сценария плохих долгов — если списать украденные средства из общего объема обращения rsETH, ожидается образование плохих долгов на сумму 123,7 миллиона долларов; если сохранить стоимость rsETH в основной сети, отнеся все потери на отображенную версию rsETH в Layer2, ожидается образование плохих долгов на сумму 230,1 миллиона долларов.

В любом случае, благодаря резервам Umbrella, казны DAO и команды, Aave имеет возможность покрыть их. Я понимаю, что Aave не хочет платить эти деньги сам, желая, чтобы основная ответственная сторона Kelp DAO и частично ответственная LayerZero также внесли свою долю. Но проблема в том, что другая сторона думает так же — «у Aave так много денег, ситуация так неловка, ты должен взять на себя больше». Таким образом, в краткосрочной перспективе этим трем сторонам будет трудно достичь консенсуса, а это означает, что временно невозможно появление решения, устраивающего всех.

Но пользователи не могут ждать так долго — уровень доходности Aave всегда был неконкурентоспособным в отрасли. Пользователи, выбирающие депозиты в Aave, идут ради репутации, безопасности и ликвидности, но сейчас ситуация такова, что Aave в самые напряженные дни после инцидента так и не дал пользователям никаких заверений, похожих на гарантии, а вместо этого一味 подчеркивал «отсутствие проблем с собственным кодом» и «невозможность контроля учета rsETH со стороны Aave», чтобы свалить вину.

Вот почему панические настроения продолжали发酵 в сообществе, пользователи пытались всеми способами вывести средства для избежания риска, те, кто мог забрать деньги, забирали напрямую, те, кто не мог, сначала занимали в других пулах, что привело к расширению воздействия.Таким образом, текущая ситуация с Aave такова: с одной стороны,持续不断的资金外流, с другой стороны,多个池子因利用率被拉满而出现流动性枯竭。

Этой неловкой ситуации можно было избежать (или, по крайней мере, она не была бы такой плохой)......既然 Aave может позволить себе заплатить, почему бы с самого начала не сделать сообществу обнадеживающее заявление, чтобы предотвратить набег? Максимум 230 миллионов плохих долгов (возможно, меньше), эти деньги ведь не придется платить только Aave, можно потом разбираться с LayerZero и Kelp DAO.

Теперь все хорошо,ради承诺救济最多 2.3 亿美元,Aave眼睁睁看着 172 亿美元的沉淀资金流失(数字可能继续增长),这还没计入 AAVE 币价这些天的跌幅......怎么算都是一笔亏麻的账。

Еще более неприятно для Aave то, что чем хуже его положение, тем спокойнее будут LayerZero, Kelp DAO и другие opposing стороны, потому что они будут считать, что Aave будет更有动力尽快解决问题, что только поставит Aave в невыгодное положение в博弈.

Дойдя до этого шага, Aave сам виноват.

За спиной Aave, Spark жадно смотрит

В то время как Aave мучается от головной боли, ситуация у конкурента Spark, наоборот, прекрасна, шумно и оживленно. Что еще более примечательно, Spark является конкурентом, «выращенным» самим Aave.

Spark изначально был кредитным протоколом, разработанным Sky (бывший MakerDAO) как форк открытого исходного кода Aave V3, обе стороны фактически используют одну и ту же базовую логику кода. В качестве компенсации между Spark и Aave было соглашение о разделе прибыли, но позже сторона Aave обвинила Spark в涉嫌毁约, и再加上расхождения в подходах,сейчас стороны находятся в чисто конкурентных отношениях.

За три месяца до кражи Kelp DAO, Spark как раз прекратил поддержку rsETH (подробнее см. «В один день, но разная судьба: Aave, принявшая rsETH, потеряла почти 200 миллионов, Spark вышел невредимым»),назовите это стратегическим консерватизмом, строгим risk-менеджментом или даже просто удачей, но результат заключается в том, что Spark не пострадал в данном инциденте — уже только по этому пункту Spark может беспрепятственно атаковать бывший ярлык Aave «самый безопасный DeFi».

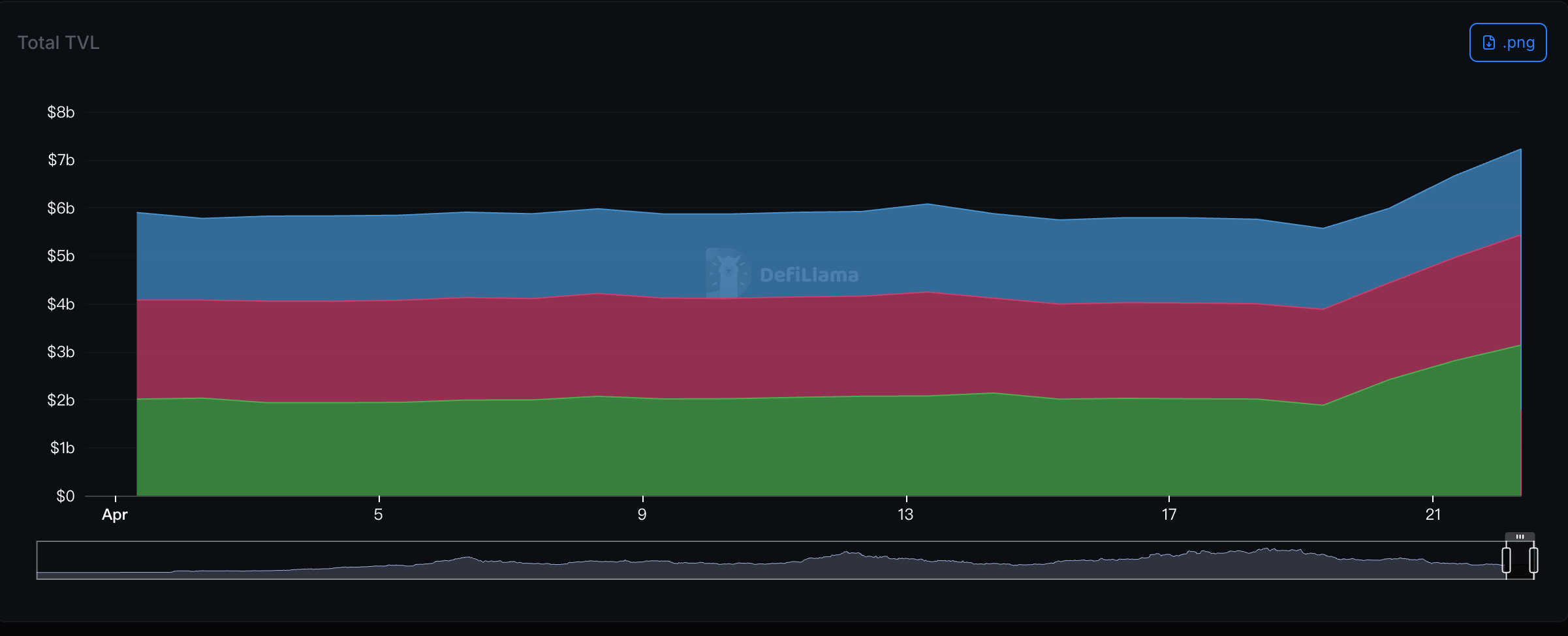

Таким образом, Spark стал одним из убежищ для бегства средств из Aave.С момента инцидента TVL Spark вырос почти на 2 миллиарда долларов (зеленая часть на графике ниже), в день инцидента Джексон Хи (Sun Yuchen) вывел из Aave 53665 ETH (стоимостью 124 миллиона долларов) и随后存入 Spark, а после дальнейшего накопления за последние дни общая сумма депозитов достигла 1.3 миллиарда долларов — в мире DeFi真的要学操作ению孙哥。

23 апреля Upbit официально объявил о запуске рынка торговли Spark (SPK) за корейскую вону, SPK под стимулом этой利好单日 вырос более чем на 80%, значительно сократив разрыв в рыночной капитализации с AAVE.

Даже основатель F2Pool Ван Чунь написал в X: «За последний год я получил из Spark 83.7 миллиона наград SPK и продал их на CoWSwap, получив 663 ETH и 1.4 миллиона долларов.Теперь немного жалею.»

Spark, очевидно, осознает, что это прекрасная возможность отобрать долю рынка у Aave.С момента инцидента руководитель стратегии Spark MonetSupply стал, пожалуй, самым активным KOL, высказывающимся по этому поводу, публикуя десятки постов в день. Хотя его высказывания в определенной степени помогают общественности понять происходящее, объективно они также усиливают панические настроения вокруг Aave.

Но это самая чистая бизнес-конкуренция, MonetSupply просто сделал最正确的选择.

Aave теряет трон кредитования в DeFi

24 апреля ранним утром, возможно, осознав серьезность ситуации,основатель Aave Стани (Stani) в X объявил о запуске плана помощи под названием DeFi United, в котором участвуют LayerZero, Ethena, ether.fi, Ink Foundation, Golem Foundation, Trydo и другие, а также лично пожертвует 5000 ETH для решения текущей проблемы.

Но средства уже ушли, доверие пользователей уже подорвано. Только этим запоздалым заявлением Aave будет трудно в краткосрочной перспективе вернуть замороженные средства и доверие пользователей.

Кредитный сегмент DeFi долгое время демонстрировал структуру «один лидер и несколько сильных», у Aave всегда было看似 очень прочное лидирующее преимущество.Но сейчас Aave уступает трон. За его спиной претенденты наступают,除了набирающий обороты Spark, другие конкуренты, такие как Morpho, Jupiter Lend, также希望отхватить кусок у Aave。

В прошлом году Стани купил за около 30 миллионов долларов пятиэтажный особняк в Лондоне, это была одна из самых дорогих сделок на低迷的 рынке роскошной недвижимости Великобритании за год. Я не знаю, существует ли что-то вроде «сглаза», но по примерам Су Чжу (Su Zhu) и других, кажется, что大佬, которые тратят деньги с размахом в圈内, всегда сталкиваются с неприятностями.

Не могу представить, о чем сейчас думает Стани в своем пятиэтажном особняке.