Автор: ethn, a16z

Компиляция: Deep Wave TechFlow

Введение от Deep Wave: a16z выпустила шестую версию рейтинга потребительских приложений с генеративным ИИ. У ChatGPT 900 миллионов еженедельных активных пользователей, но Gemini и Claude демонстрируют более быстрый рост платных подписок. Битва за «ИИ-помощника по умолчанию» официально началась.

Главное изменение в этой версии — включение в рейтинг таких старых продуктов, как CapCut, Canva, Notion, где «ИИ-функции стали основными», а также первое покрытие Agent, ИИ-браузеров и настольных инструментов.

Автор Оливия Мур — партнер потребительской команды a16z. Этот отчет — одна из самых систематических публичных данных, отслеживающих ландшафт потребительских ИИ-приложений.

Полный текст:

Три года назад мы выпустили первую версию этого рейтинга с простой целью: выяснить, какие продукты с генеративным ИИ действительно используются массовым потребителем. Тогда граница между «ИИ-нативными» компаниями и остальными была четкой. ChatGPT, Midjourney, Character.AI — это продукты, построенные с нуля вокруг базовых моделей, остальной мир программного обеспечения еще только разбирался, как использовать эту технологию.

Сейчас этой границы больше не существует. CapCut — видеоредактор с 736 миллионами месячных активных мобильных пользователей — его самые популярные функции полностью работают на ИИ: удаление фона, ИИ-эффекты, автоматические субтитры, генерация видео из текста. Двигатель роста Canva полностью построен на инструментах Magic Suite AI. Платный attach rate ИИ в Notion за год взлетел с 20% до более чем 50%, и теперь функции ИИ приносят около половины годового регулярного дохода (ARR) компании.

Начиная с этой версии, мы расширили охват, включив все потребительские продукты, где генеративный ИИ стал основным опытом, включая CapCut, Canva, Notion, Picsart, Freepik и Grammarly. Мы считаем, что это точнее отражает то, как люди на самом деле используют ИИ, хотя большинство продуктов в верхней части рейтинга по-прежнему являются ИИ-нативными.

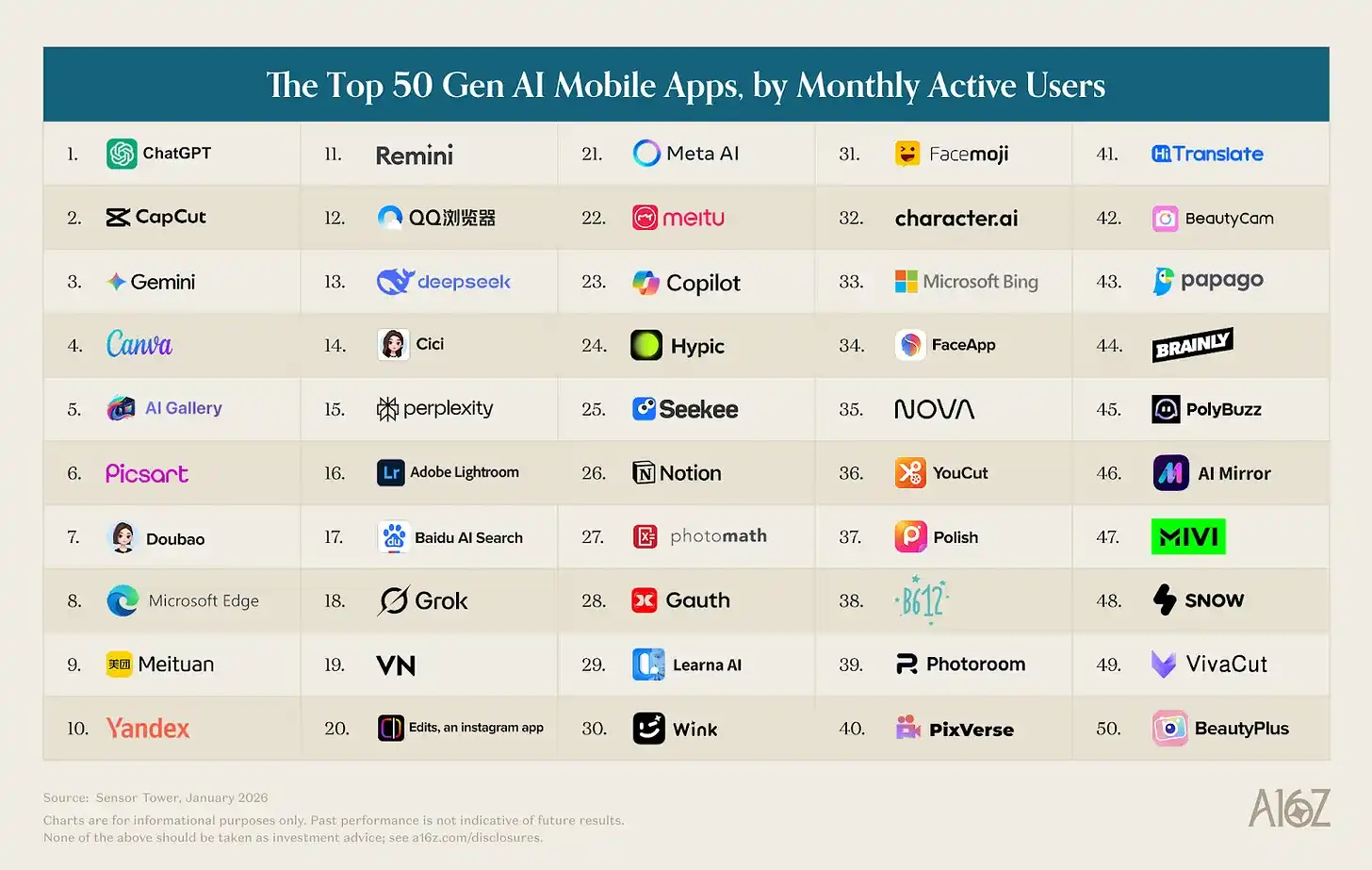

Подпись к рисунку: Полный рейтинг Top 100 потребительских приложений с генеративным ИИ, версия марта 2026 года.

Как и прежде, веб-рейтинг основан на количестве уникальных месячных посещений (данные SimilarWeb, по состоянию на январь 2026 г.), мобильный рейтинг — на количестве месячных активных пользователей (данные Sensor Tower, по состоянию на январь 2026 г.). Вот наши ключевые выводы:

1. ChatGPT лидирует, но битва за «ИИ по умолчанию» уже началась

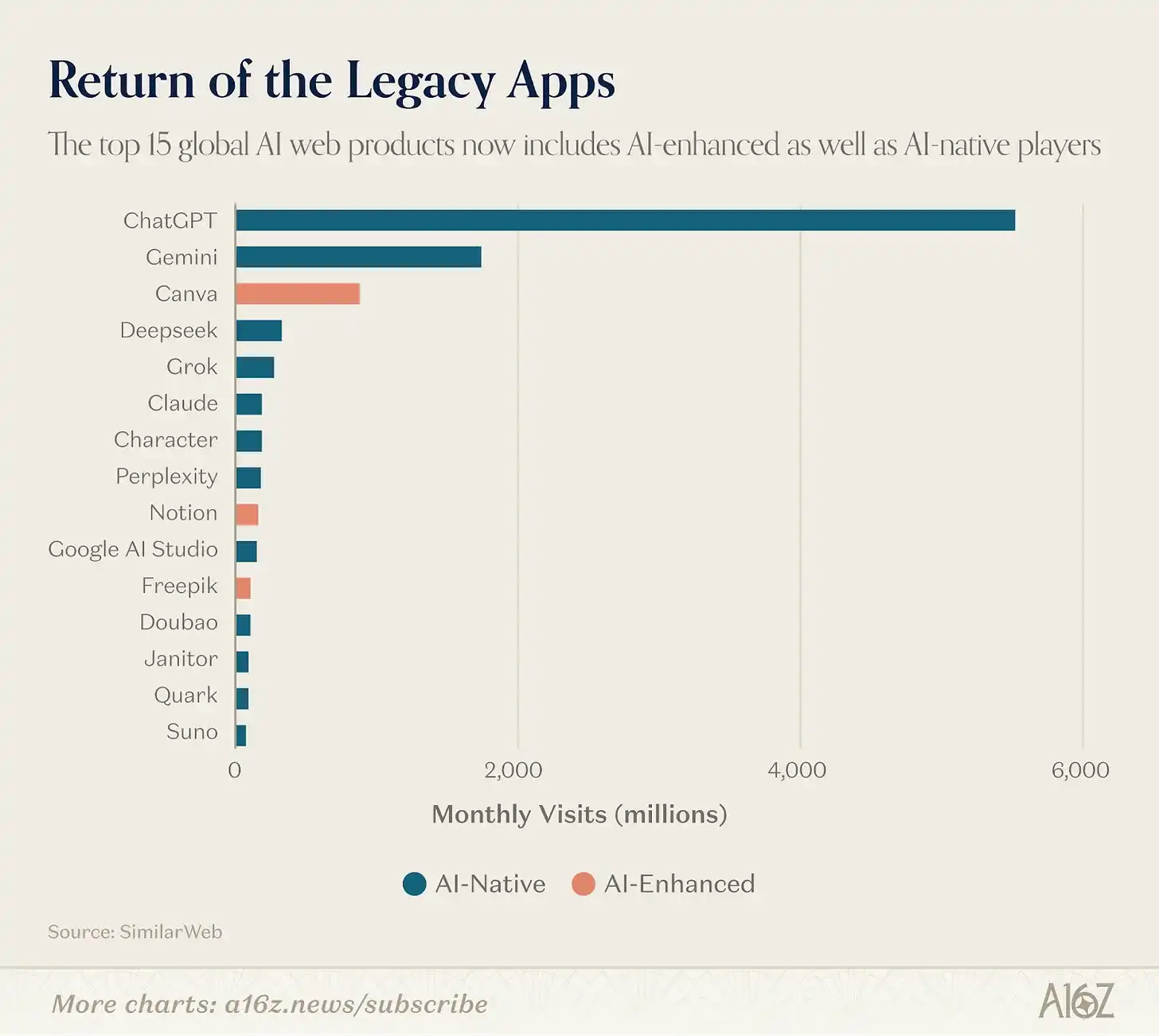

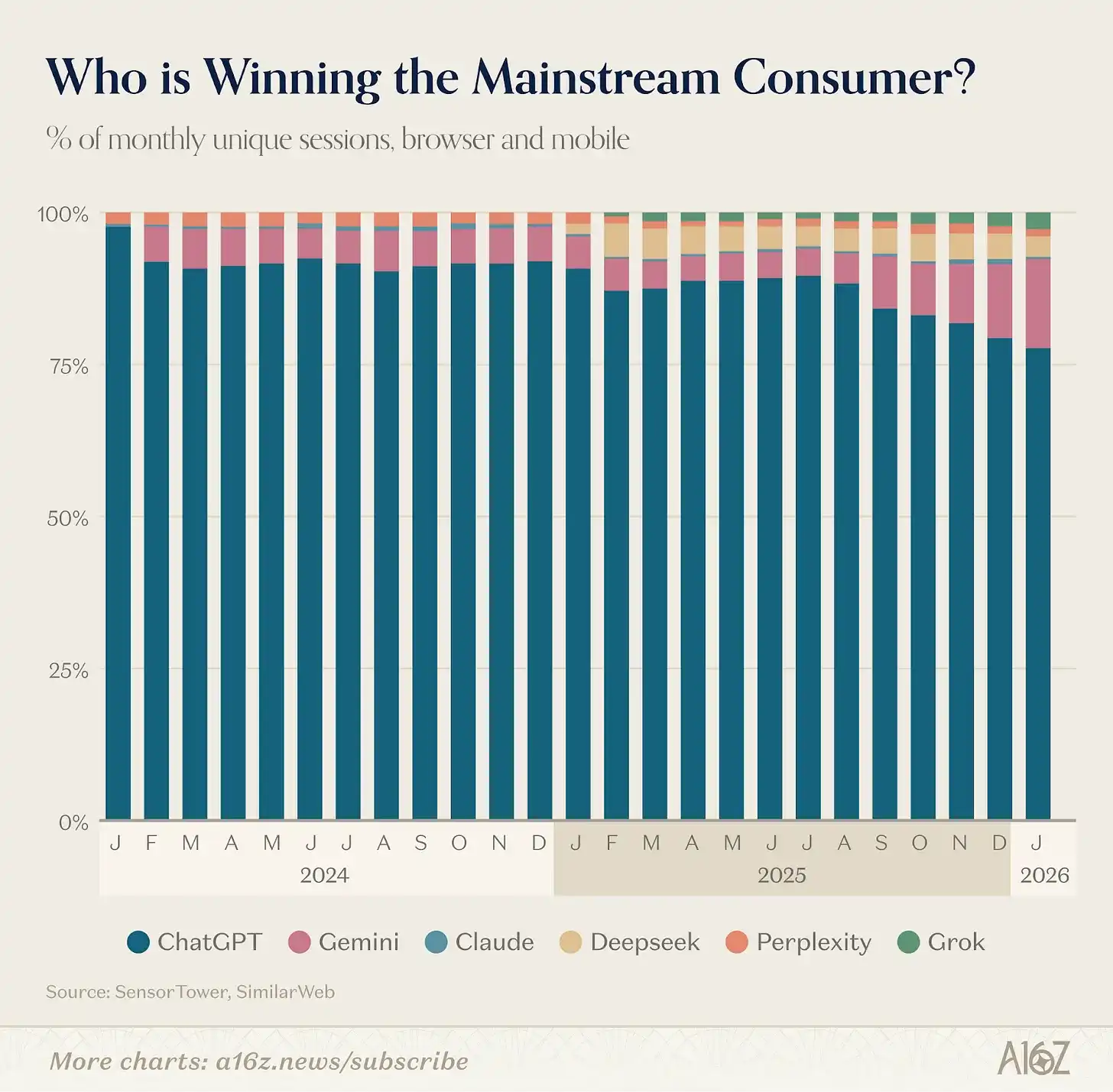

ChatGPT по-прежнему остается крупнейшим потребительским ИИ-продуктом с огромным отрывом. Веб-трафик в 2.7 раза выше, чем у второго места Gemini, мобильная месячная аудитория — в 2.5 раза больше. Еженедельная аудитория ChatGPT за последний год выросла на 500 миллионов и сейчас составляет 900 миллионов. Учитывая, что рост тем сложнее, чем больше масштаб, эта цифра поразительна — более 10% населения мира еженедельно используют ChatGPT.

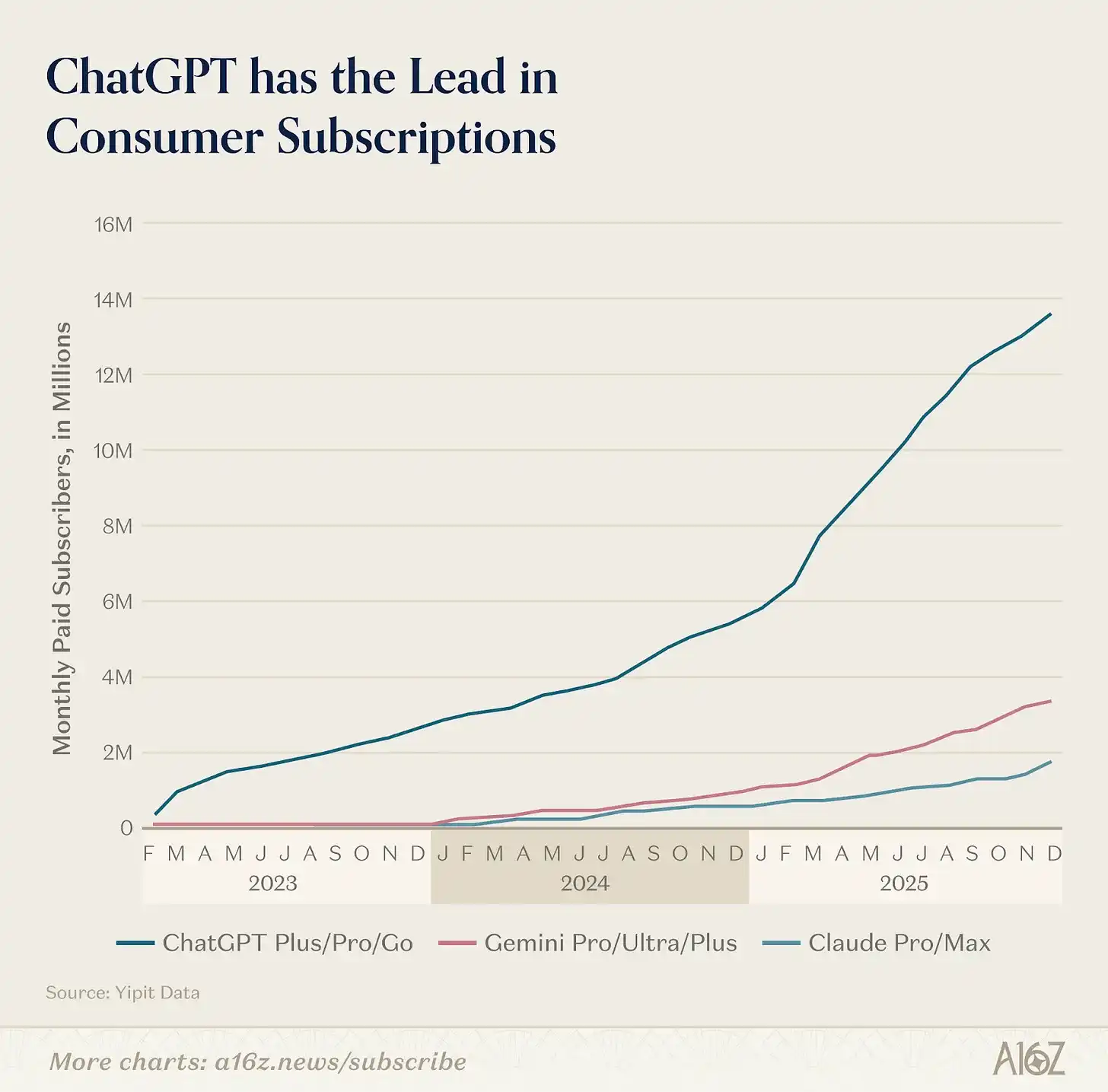

Но мы начинаем видеть, как рынок расширяется, и другие универсальные платформы набирают силу в определенных сценариях. Рост платных подписок на Gemini и Claude в США за последний год ускорился (хотя по объему они все еще сильно отстают от ChatGPT — у ChatGPT платных пользователей в 8 раз больше, чем у Claude, и в 4 раза больше, чем у Gemini). Согласно Yipit Data, по состоянию на январь 2026 года, платная аудитория Claude выросла более чем на 200% в годовом исчислении, Gemini — на 258%. При этом мы видим все больше поведения «использования нескольких платформ» — около 20% еженедельных активных веб-пользователей ChatGPT также использовали Gemini в ту же неделю.

Что происходит? Конкуренты наступают. Google одержал красивую победу в креативных моделях — Nano Banana сгенерировала 200 миллионов изображений за первую неделю и привлекла 10 миллионов новых пользователей в Gemini; Veo 3 признан прорывным моментом для ИИ-видео. Anthropic сосредоточилась на профессиональных пользователях, выпустив Cowork, Claude in Chrome, плагины для Excel и PowerPoint, и, что最关键, Claude Code.

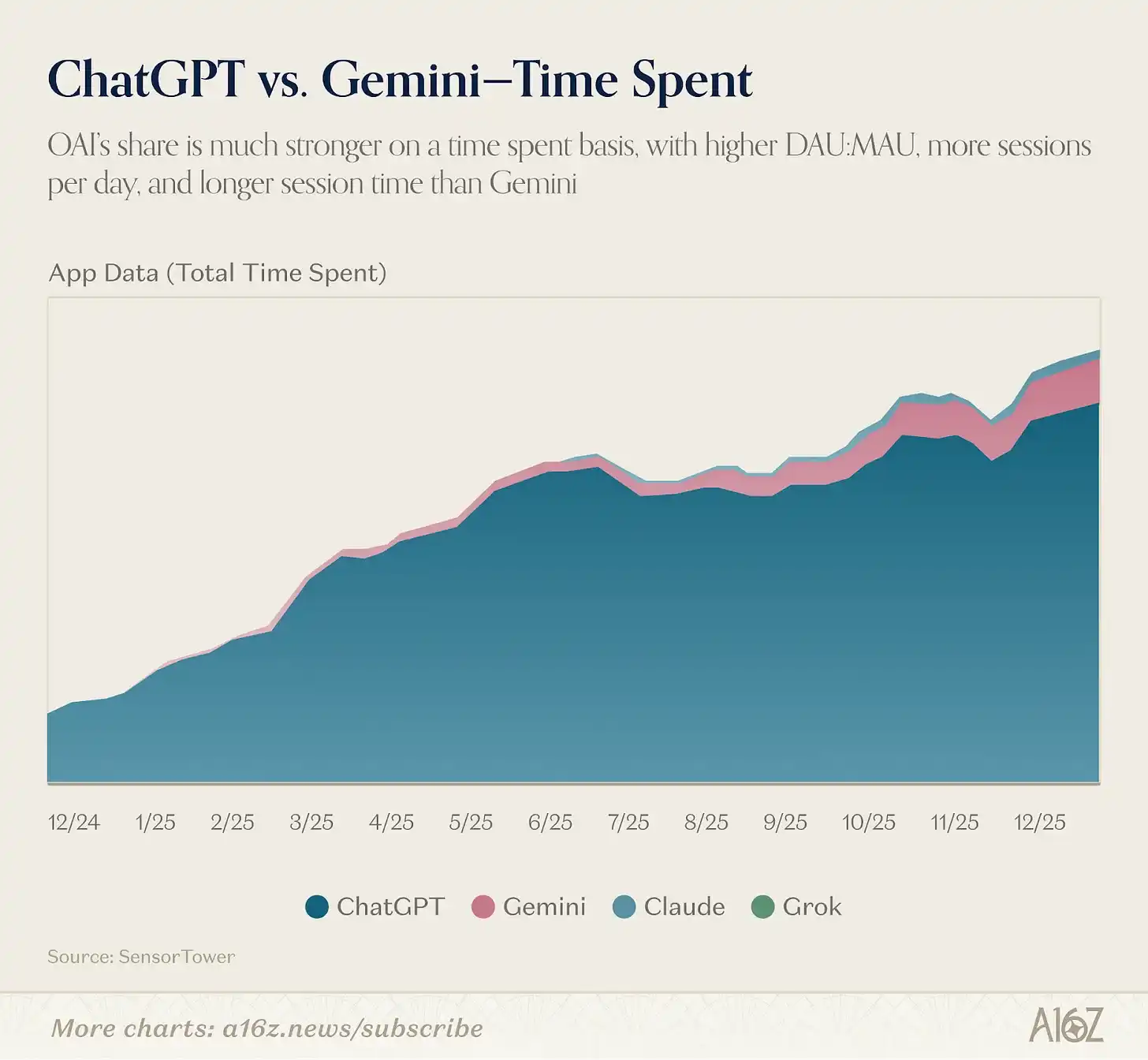

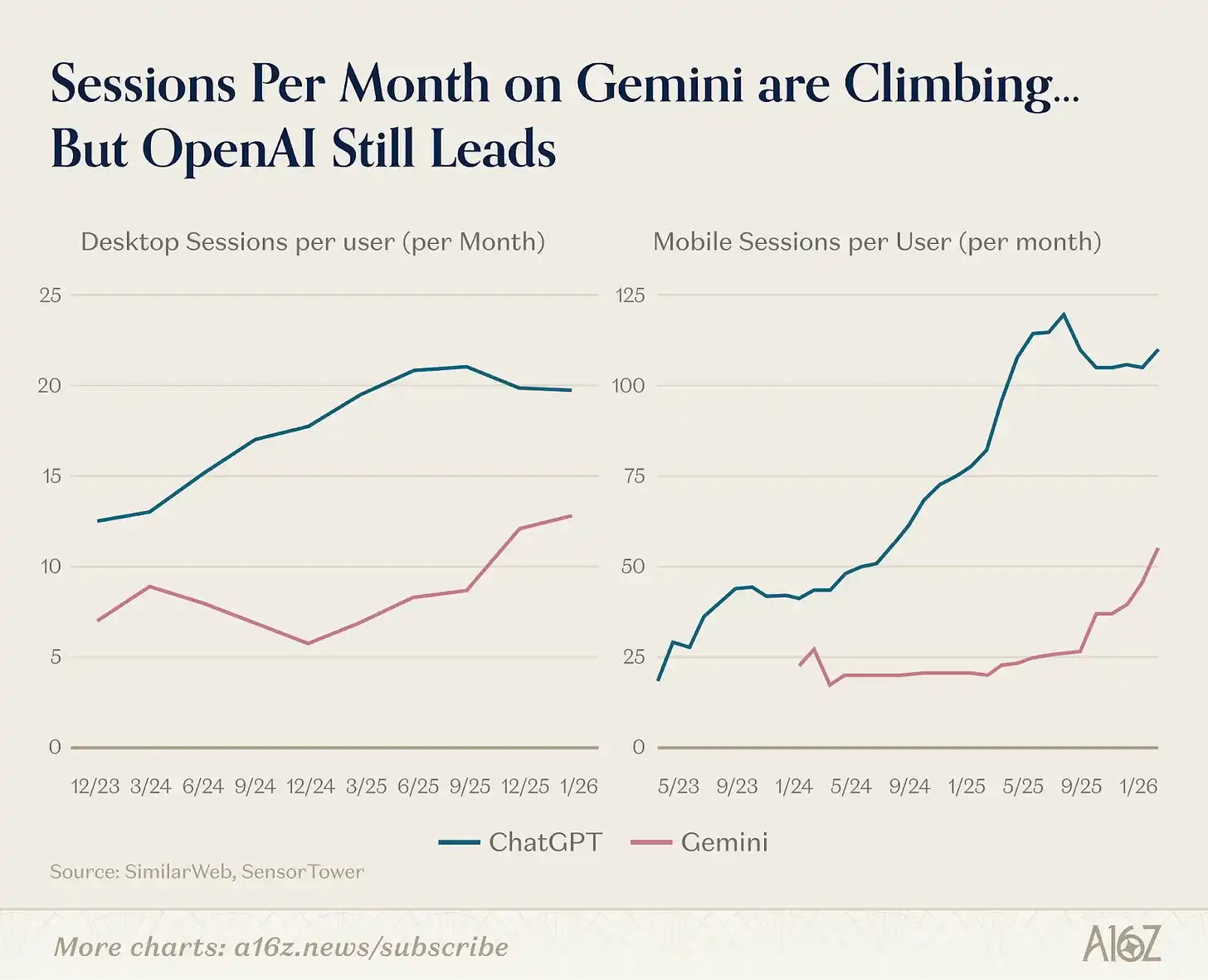

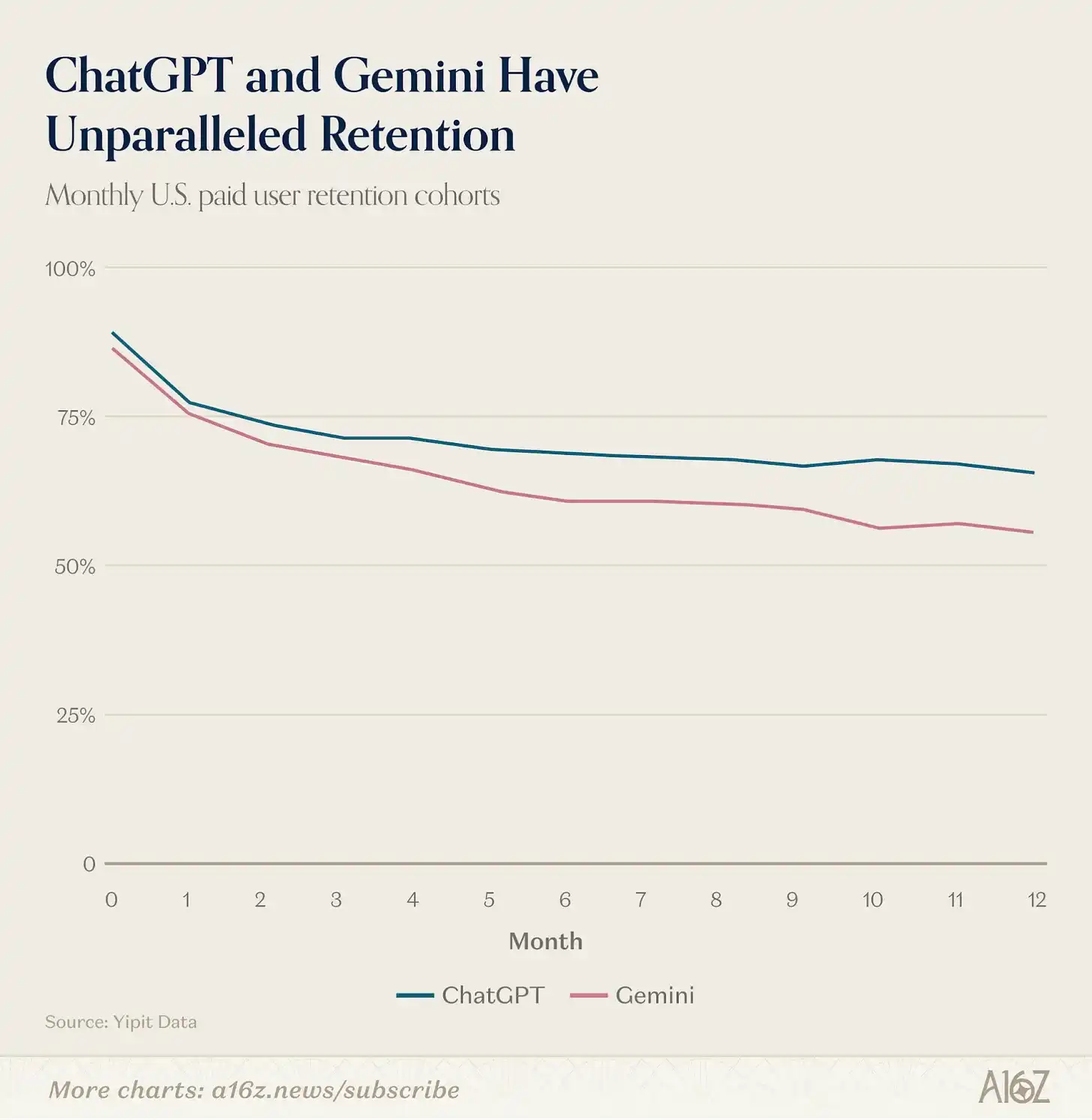

Эта конкуренция касается не только того, кто лидирует сегодня, но и того, кто сможет построить структурные барьеры. Контекст накапливается: чем больше LLM знает о вас, тем лучше результаты она дает, и тем сильнее вы от нее зависите. Ранние данные показывают, что среднее количество сессий на пользователя в месяц в веб-версии Gemini растет, хотя ChatGPT все еще опережает в 1.3 раза. В мобильной версии преимущество ChatGPT больше: среднее количество сессий на пользователя в месяц в 2.2 раза выше, чем у Gemini. Согласно Yipit Data, показатели удержания платных потребительских пользователей в США у обеих компаний являются одними из лучших в отрасли.

Следующий уровень блокировки исходит от магазинов приложений. И ChatGPT, и Claude запустили экосистемы коннекторов — у ChatGPT есть GPTs и Apps, у Claude — интеграции MCP и Connectors, позволяющие пользователям строить рабочие процессы поверх помощника. Как только пользователь настроит подключение ИИ к календарю, почте и CRM, стоимость переключения резко возрастет. Разработчики могут сосредоточить усилия на платформе с наибольшим количеством пользователей, создавая маховичный эффект, как в ранних войнах платформ.

Мы уже видим расхождение путей развития платформ. Сэм Олтман ранее заявлял, что OpenAI хочет «принести ИИ миллиардам людей, которые не могут позволить себе подписку», поэтому они начали показывать рекламу. Он также сказал, что OpenAI запустит уровень идентификации «Sign in with ChatGPT», позиционируя ИИ-помощника как интерфейс по умолчанию между потребителем и интернетом. Амбиция состоит в том, чтобы ChatGPT стал началом всего: покупок, бронирования отелей, веб-серфинга, управления здоровьем, повседневной жизни.

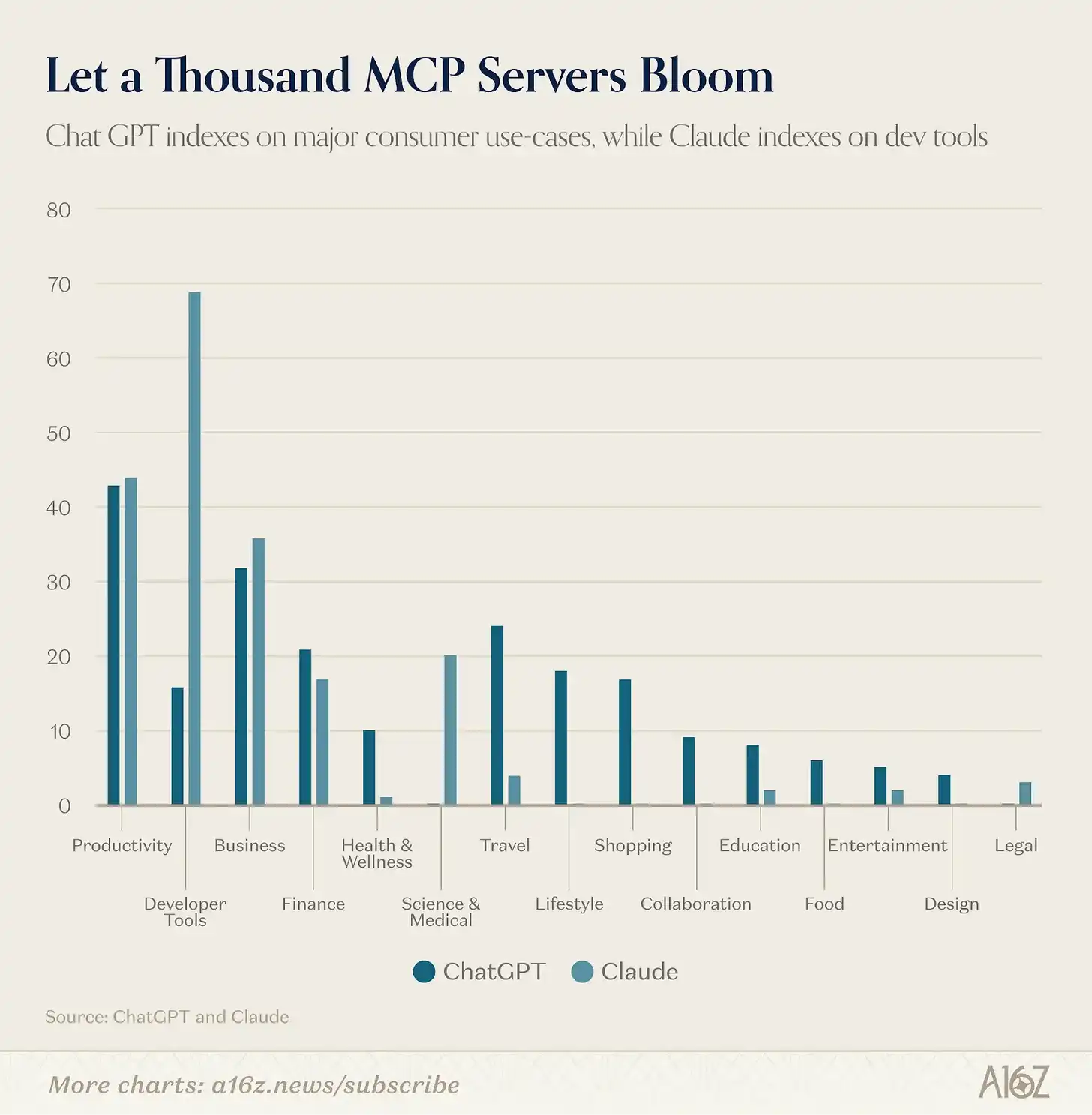

Каталоги приложений уже отражают это различие. По состоянию на конец февраля, магазин приложений ChatGPT охватывал 13 категорий и 220 приложений. У Claude около 160 отобранных коннекторов плюс около 50 сообщественных MCP-серверов. Но только 41 приложение совпадают — около 11% от объединенного каталога, и эти 41 — почти исключительно универсальные инструменты продуктивности, нужные всем: Slack, Notion, Figma, Gmail, Google Calendar, HubSpot, Stripe.

За пределами основных инструментов две платформы почти полностью идут разными путями. У ChatGPT более 85 эксклюзивных приложений в категориях путешествий, шопинга, еды, здоровья, образа жизни, развлечений, у Claude в этих категориях почти нет. Это все потребительские транзакционные сценарии: бронирование авиабилетов через Expedia, заказ продуктов через Instacart, просмотр объявлений о недвижимости на Zillow, отслеживание питания в MyFitnessPal. Это самая агрессивная стратегия суперприложения среди всех ИИ-компаний. Эксклюзивные интеграции Claude, напротив, ориентированы на профессиональный сегмент: терминалы финансовых данных (PitchBook, FactSet, Moody's, MSCI), инфраструктура для разработчиков (Sentry, Supabase, Snowflake, Databricks), научные и медицинские инструменты (PubMed, Clinical Trials, Benchling), а также сообщественный MCP с открытым исходным кодом, аналога которому у ChatGPT нет.

Anthropic, похоже, фокусируется на продвинутых пользователях ИИ (разработчиках, knowledge-работниках и т.д.). Эти пользователи более готовы и способны платить за дорогие прямые подписки. У ChatGPT тоже есть продукты для той же аудитории (например, Codex, Frontier), но они одновременно заявляют о желании стать платформой для truly массового пользователя — это может открыть больше путей монетизации по мере роста пользовательской базы. Они уже тестируют рекламу, а комиссии за транзакции — логичное направление расширения.

Если ИИ-помощник — это не просто чат-окно, а операционная системная среда, то в конечном итоге эта конкуренция может быть похожа не на войну поисковиков — где одна компания захватывает 90% рынка — а на войну мобильных ОС, где две платформы с截然 разными философиями построили экосистемы на триллионы долларов.

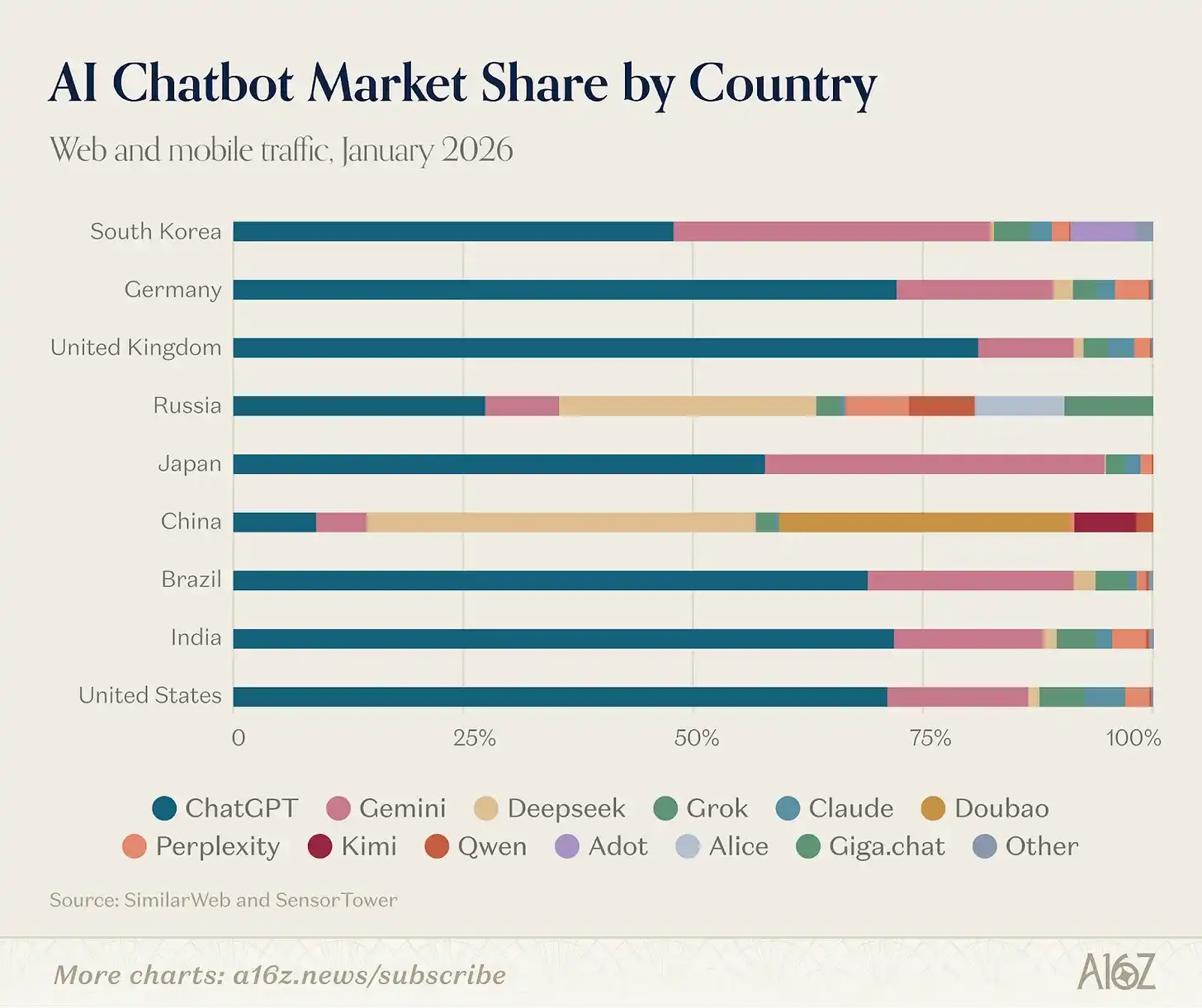

2. Глобальное использование делится по продуктам

Географически рынок ИИ раскалывается на три截然 distinct экосистемы, разрыв между которыми увеличивается.

Западные ИИ-инструменты имеют高度 схожую пользовательскую базу. Основные рынки для ChatGPT, Claude, Gemini, Perplexity происходят из одного пула: США, Индия, Бразилия, Великобритания и Индонезия, только порядок разный. Ни у одного нет значительного использования в Китае или России. Причина — политика: с 2022 года западные технологические санкции ограничили доступ России к американским ИИ-инструментам; Китай требует от провайдеров ИИ регистрации, локального хранения данных и соблюдения правил цензуры.

DeepSeek — единственный продукт, spanning multiple лагерей. Веб-трафик распределяется между Китаем (33.5%), Россией (7.1%) и США (6.6%), мобильная статистика похожа. Китайские пользователи также массово используют Doubao от ByteDance и локальный продукт Kimi.

Россия, которая в наших ранних версиях почти не представляла собой独立ный рынок, теперь стала третьим полюсом, с DeepSeek на втором месте по проникновению. Браузер Yandex с интегрированным ИИ-помощником Alice достиг 71 миллиона месячных активных пользователей, войдя в десятку ведущих мировых мобильных ИИ-продуктов. GigaChat от Сбера также впервые появился в нашем веб-рейтинге. Эта модель повторяет китайскую, только время сжато: санкции создали вакуум, и локальные продукты заполнили его за два года.

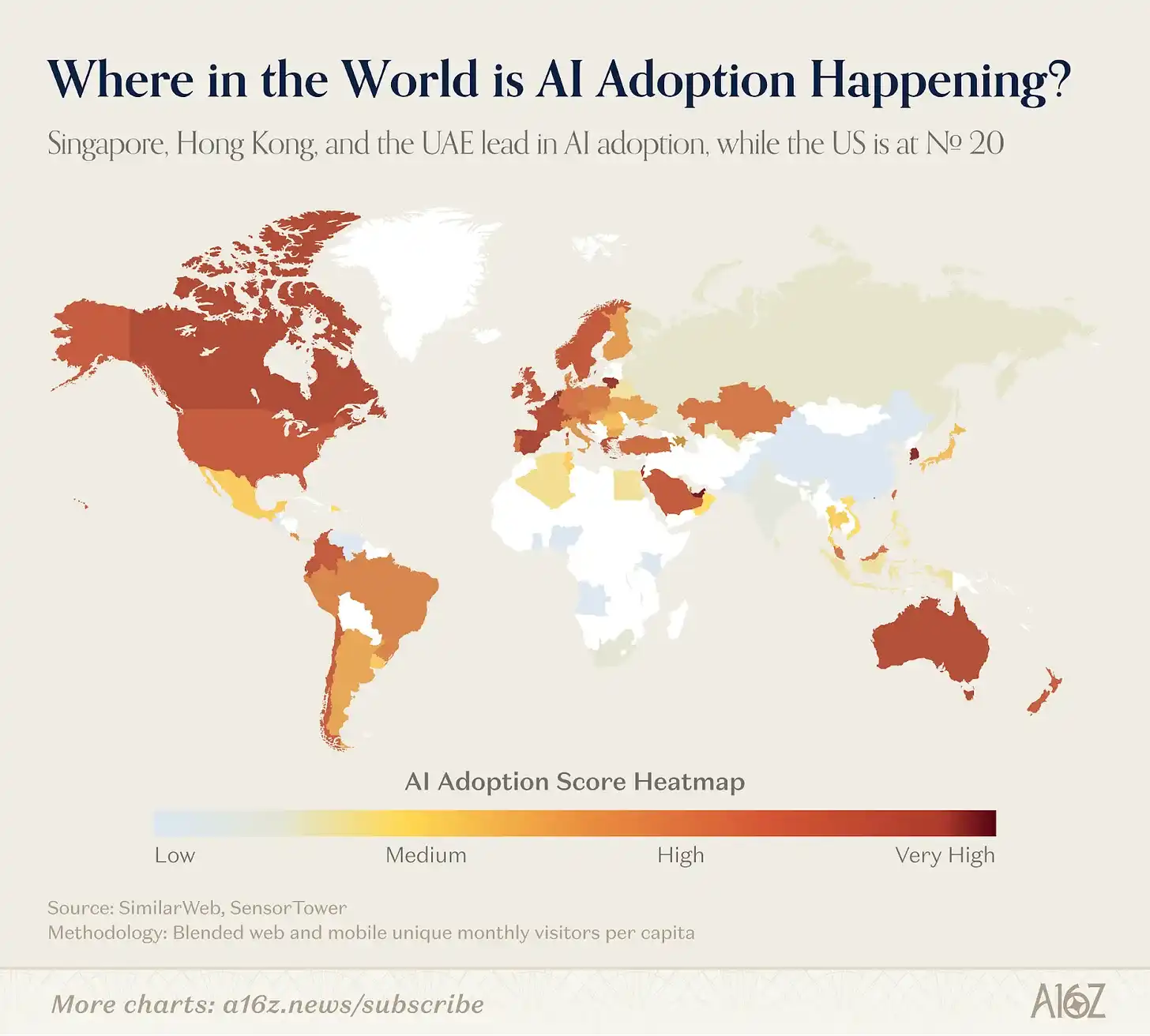

Чтобы измерить внедрение ИИ на душу населения, мы построили простой индекс, объединяющий веб-посещения на душу населения и мобильную месячную аудиторию на душу населения, с оценкой от 0 до 100. Результаты重新定义 географическую格局. Сингапур занял первое место, за ним следуют ОАЭ, Гонконг и Южная Корея. США — родина большинства ИИ-продуктов — заняли 20-е место.

Подпись: Индекс внедрения генеративного ИИ на душу населения (0-100), Сингапур лидирует, США на 20-м месте.

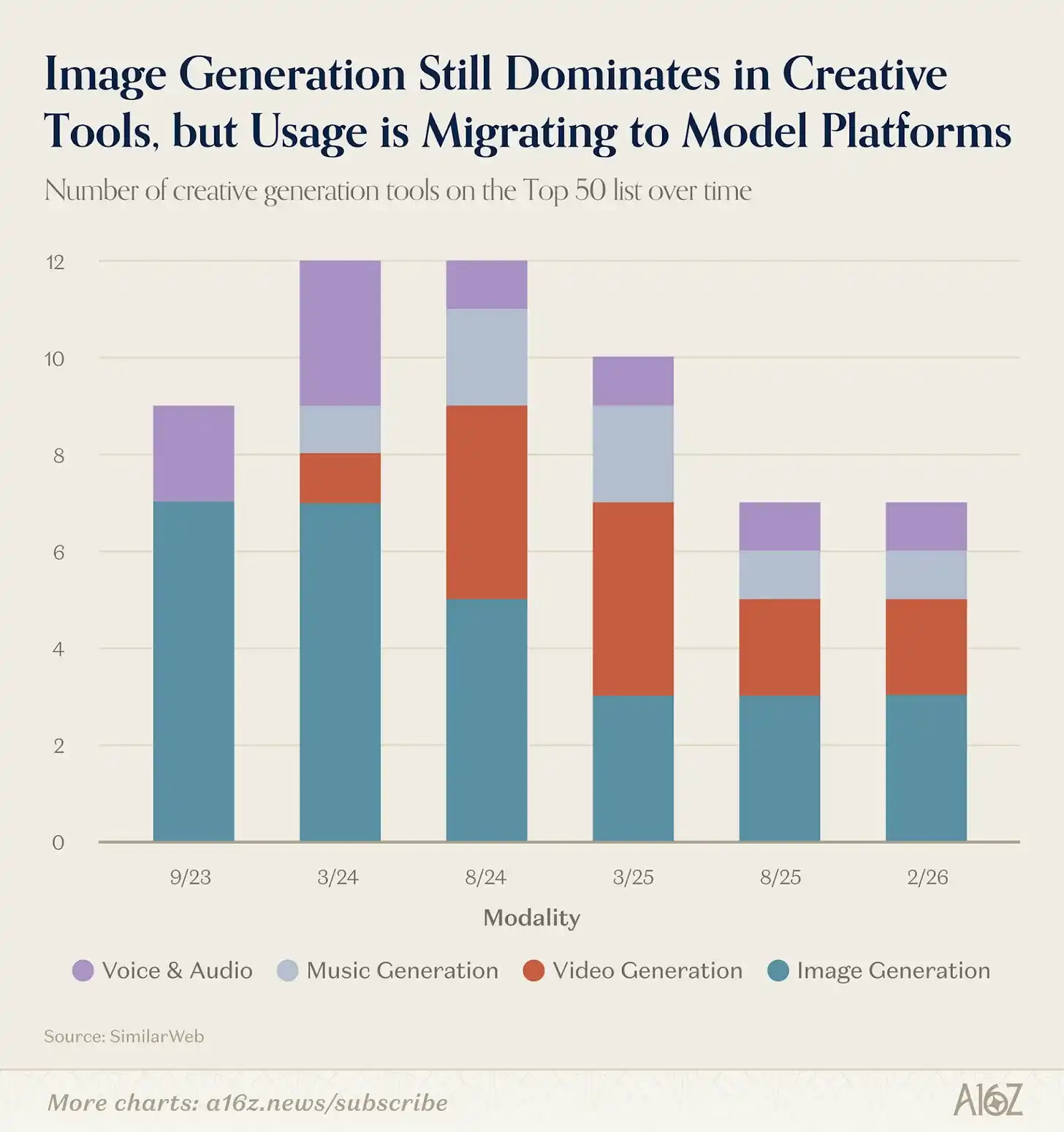

3. Большая перетряска креативных инструментов

Midjourney, DALL-E и Stable Diffusion — это продукты, которые привели в мир генеративного ИИ большинство ранних пользователей — все трое вышли до ChatGPT. Инструменты генерации изображений не только доминировали в креативной категории (генерация видео и аудио появилась позже), но и стабильно занимали верхние позиции в наших первых трех рейтингах. С этой категорией потом многое произошло.

В первой версии рейтинга за сентябрь 2023 года 9 из 9 креативных инструментов в вебе были генераторами изображений. Три года спустя в списке осталось только 3 генератора изображений, но креативных инструментов по-прежнему 7. Разница в том, что заняло освободившееся место: продукты для видео, музыки и голоса захватили позиции,腾出 генерацией изображений.

История генерации изображений — это история поглощения бундлингом. По мере того как качество встроенных моделей генерации изображений в ChatGPT (GPT Image 1.5) и Gemini (Nano Banana) росло, порог входа для独立ных продуктов резко повысился. В нашей первой версии рейтинга Midjourney входила в топ-10, сейчас она опустилась на 46-е место. Оставшиеся продукты — Leonardo, Ideogram, CivitAI — склонны обслуживать特定 креативные сообщества, дифференцируясь attitude функциями, а не конкурируя напрямую с универсальными генераторами.

Генерация видео — область с наибольшими изменениями в этой версии. Kling AI, Hailuo и Pixverse создали substantial пользовательскую базу, модели, разработанные в Китае,持续 лидируют по качеству输出. Появление приложений на основе Seedance 2.0 в следующем рейтинге нас не удивит. Veo 3 — первая американская модель, сократившая разрыв, она подстегнула трафик Google Labs (рейтинг вырос с 36-го до 25-го).

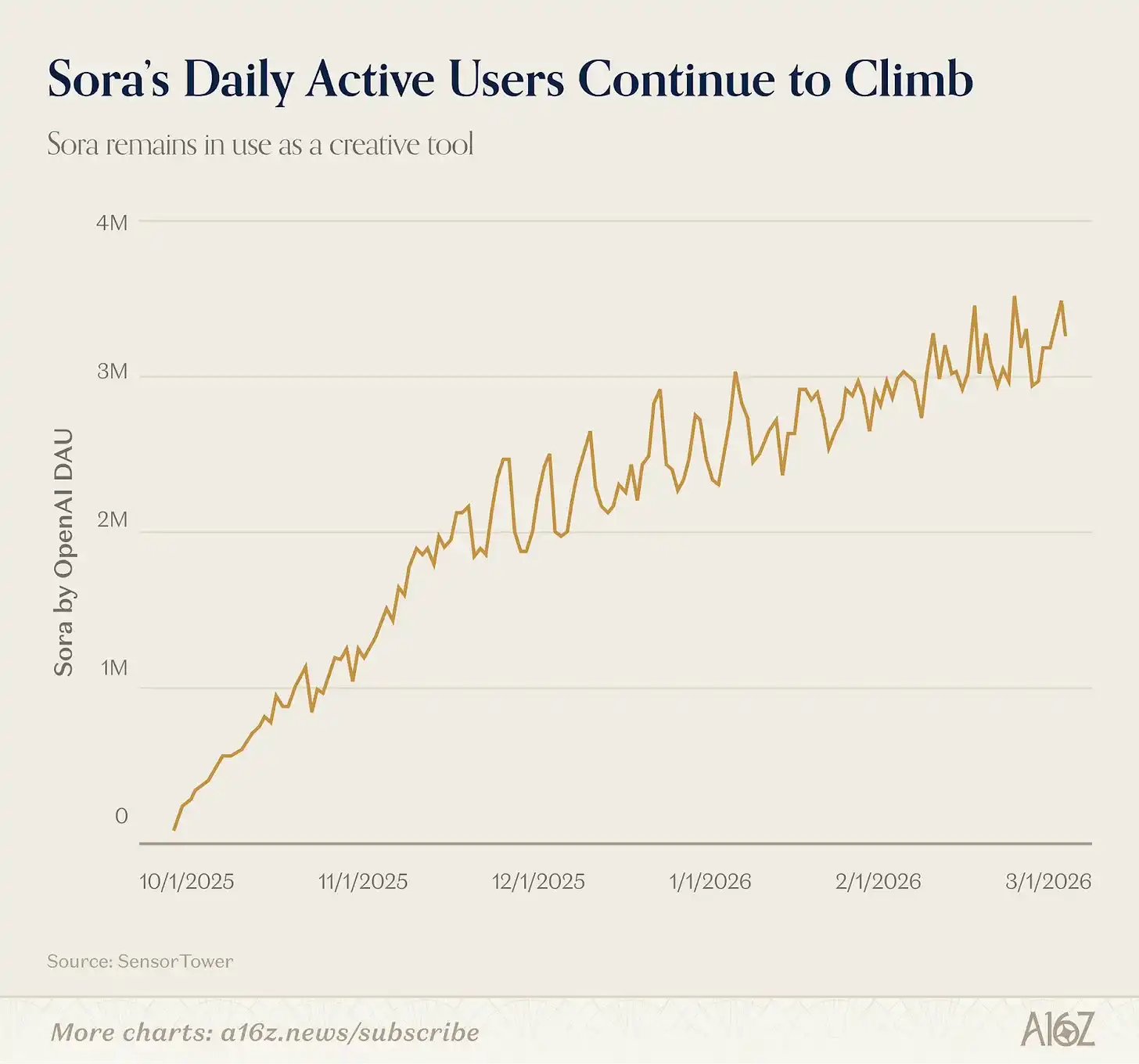

Кого не хватает? Sora. OpenAI запустила Sora 2.0 как独立ное приложение в сентябре 2025 года, пользователи могли загружать свои цифровые аватары作为 Cameo, генерировать видео с реальными людьми. Sora занимала первое место в американском App Store 20 дней подряд, достигнута отметки в 1 миллион скачиваний быстрее, чем ChatGPT. Затем скачивания снизились, потому что Sora не смогла持续 вирально расти как социальное приложение (никому еще не удалось пройти путь ИИ × социальные сети), поэтому в мобильный рейтинг эта версия не вошла. Но данные SensorTower показывают, что мобильная дневная аудитория Sora по-прежнему превышает 3 миллиона, создатели ИИ-видео продолжают использовать эту модель, даже если публикуют работы на других платформах.

Музыка и голос更具防御能力. Suno сохранила позицию с предыдущей версии (15-е место). ElevenLays входит в рейтинг с сентября 2023 года, ее核心 возможности — клонирование голоса, озвучка, production аудио — достаточно专业ны, чтобы еще не стать галочкой в продукте гигантов.

Подводя итог закономерности: в креативных направлениях, где发力 гиганты моделей и крупные игроки вроде Google и OpenAI (изображения, и все больше видео), трафик独立ных продуктов сжимается — конечно, остается пространство для продуктов, ориентированных не на мейнстрим, возможно, с attitude и более высокой ценой. В направлениях, где гиганты не发力 (музыка, голос), у独立ных продуктов больше пространства.

4. Agent пришли

Переход к агентному ИИ начался не в этой версии — он начался в предыдущей, в форме vibe coding (атмосферное программирование). Когда Lovable, Cursor и Bolt появились в нашем рейтинге в марте 2025 года, они представляли нечто новое: ИИ-продукты не просто отвечают на вопросы или генерируют медиа, а создают东西 за пользователя. Это и есть агентное поведение, просто ограниченное垂直ной областью.

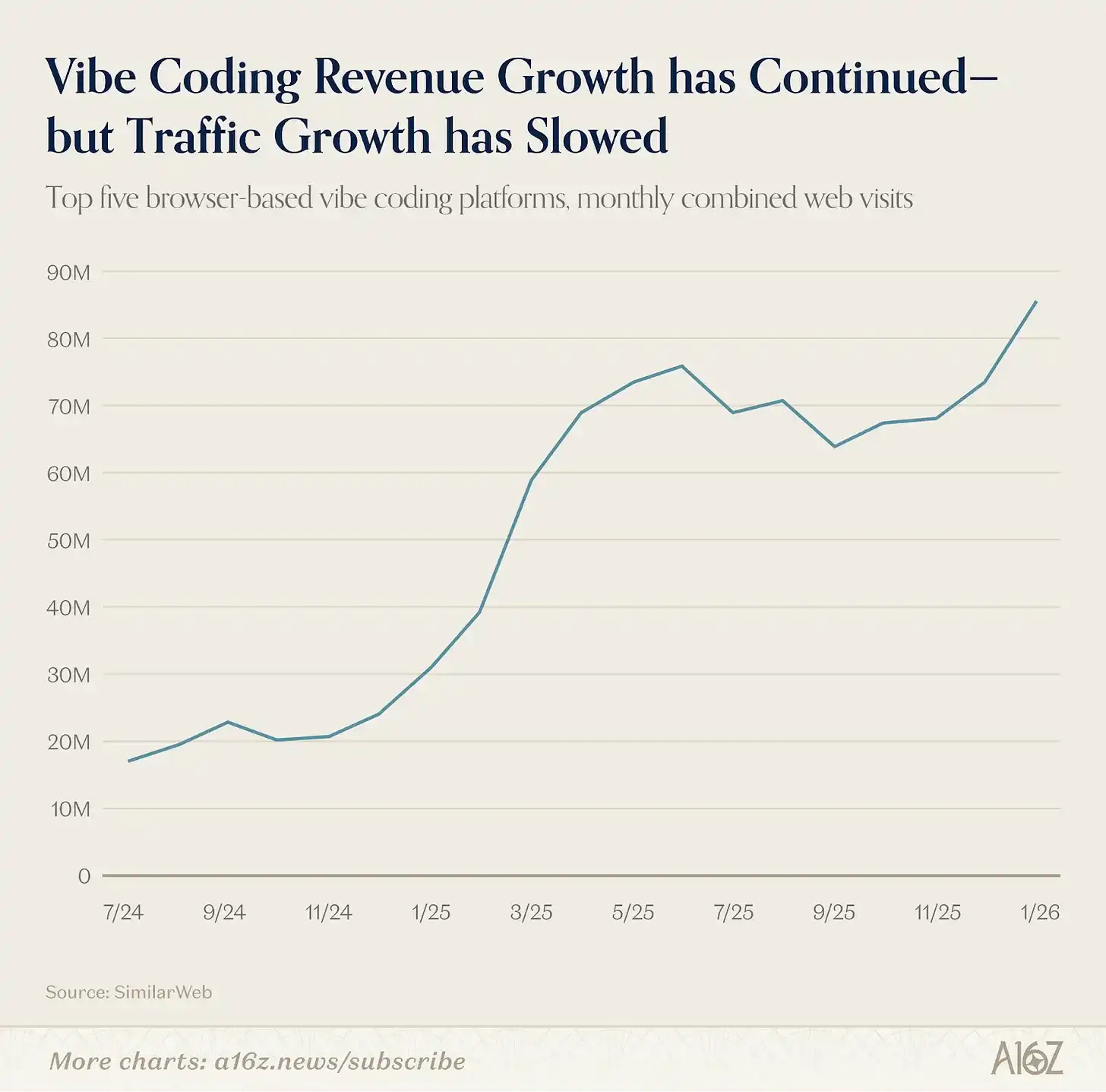

Vibe coding доказала способность удерживать технических (и полу-технических) пользователей. В этой версии и Replit, и Lovable в рейтинге, как и Claude Code (через Claude). Остается пространство для роста, потому что этот тренд еще не真正 проник на массовый рынок. Трафик пяти крупнейших платформ vibe coding все еще растет, хотя и медленнее, чем в最初的 взрывной период, но доходы многих продуктов растут, потому что разработчики и команды используют их более интенсивно.

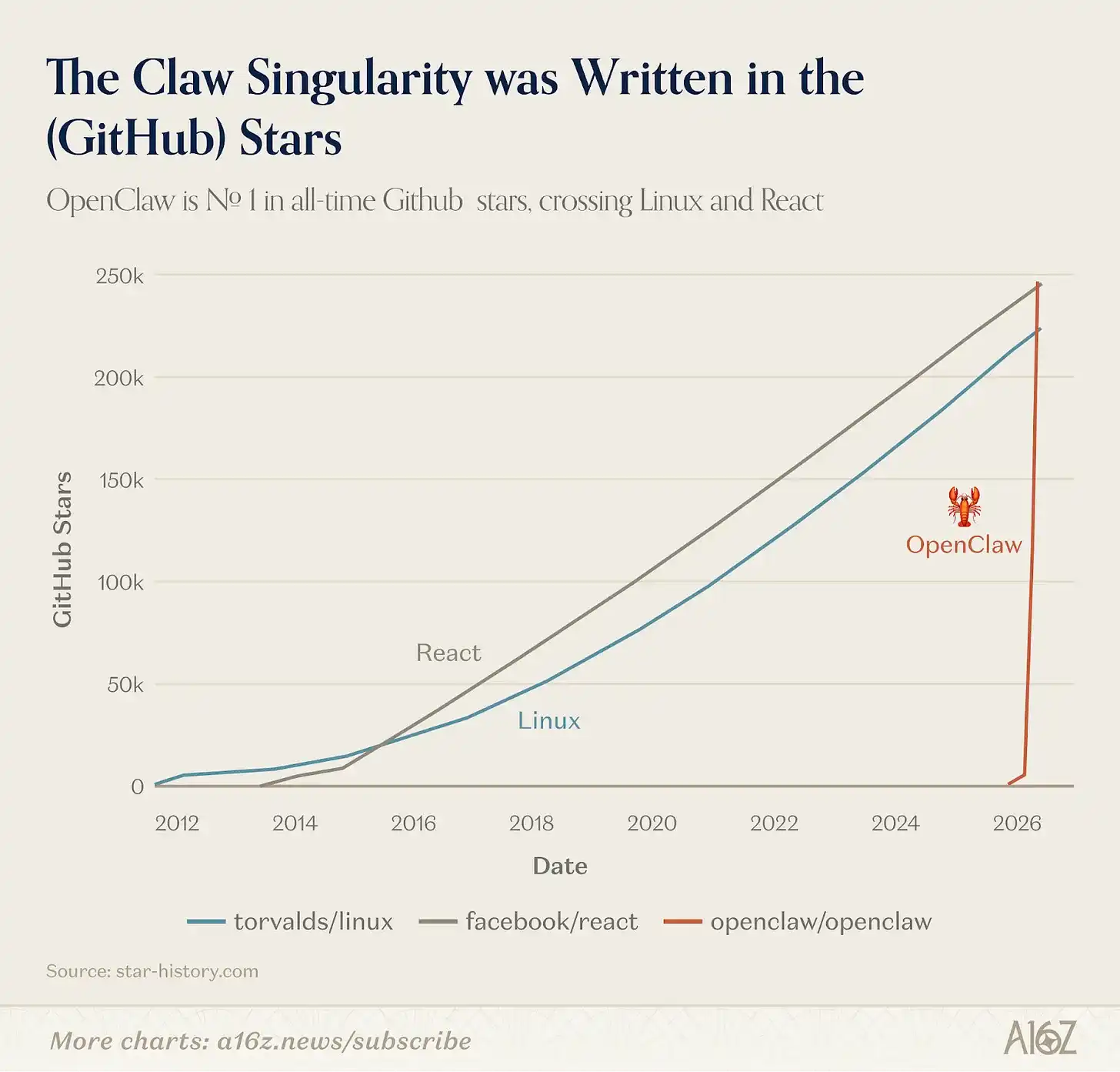

Более недавно начали появляться универсальные агенты. В январе 2026 года опенсорсный проект под названием OpenClaw из сайд-проекта独立ного разработчика превратился в 68 000 звезд на GitHub и освещение в мейнстрим-медиа всего за несколько недель. OpenClaw, созданный австрийским разработчиком Питером Штайнбергером, — это ИИ-агент, работающий локально, который может подключиться к вашим мессенджерам и выполнять за вас многошаговые задачи.

Если ChatGPT был моментом, когда потребители discovered, что ИИ может вести диалог, то OpenClaw может стать моментом, когда потребители discovered, что ИИ может действовать. Продукт взорвал сообщество разработчиков — если бы мы сдвинули窗口 анализа на февраль, а не на январь, OpenClaw вошел бы в веб-топ-30.

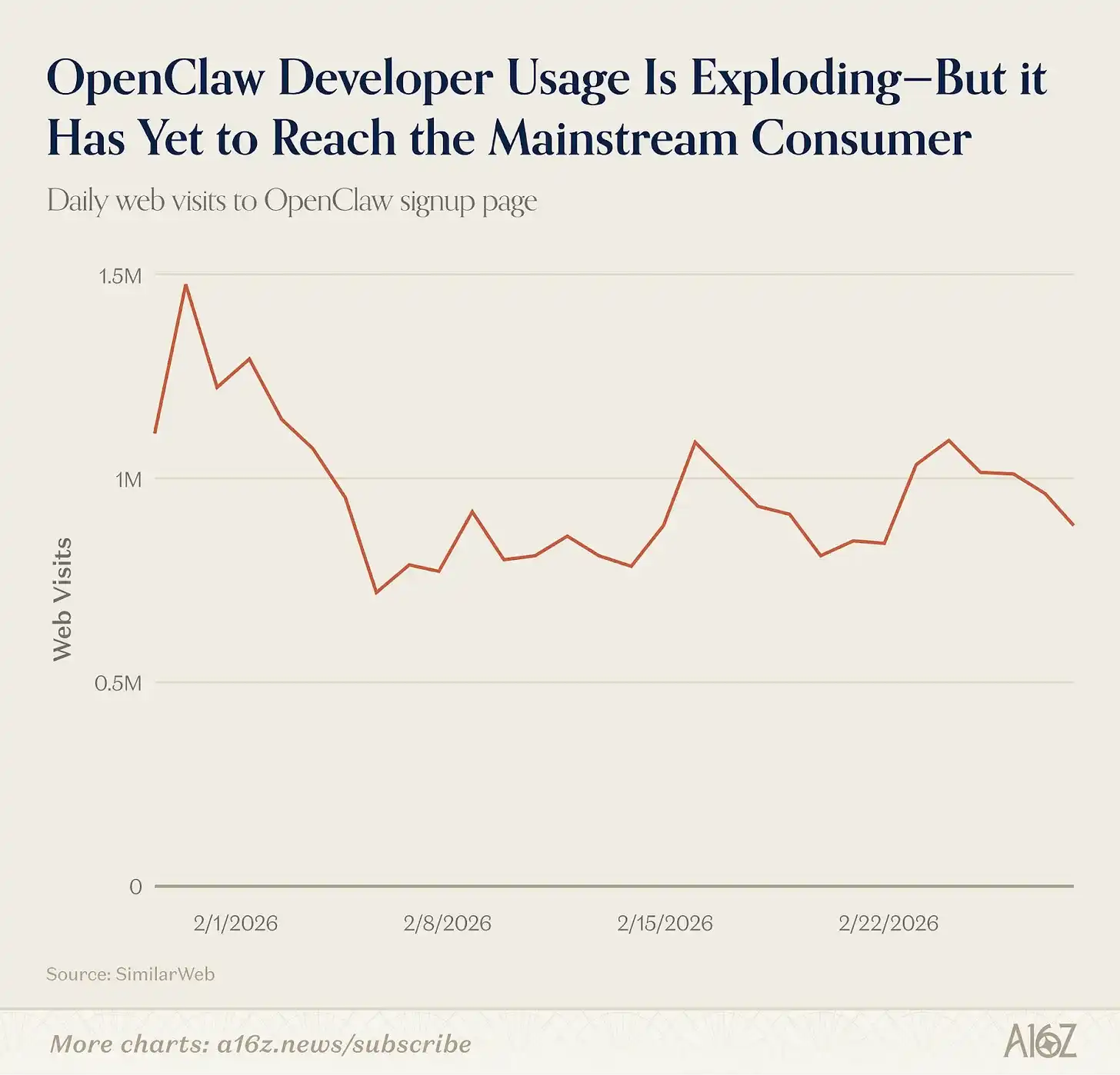

Но OpenClaw еще не потребительский продукт — установка и обслуживание требуют умения пользоваться терминалом. OpenClaw持续 набирает обороты среди технических пользователей, в начале марта став проектом с наибольшим количеством звезд на GitHub, обогнав React и Linux. Но продукт еще не «выпустился» к真正 массовому пользователю — по крайней мере, судя по данным о новых посетителях страницы установки OpenClaw, рост довольно плоский. Проект был приобретен OpenAI в феврале 2026 года, что, возможно, означает скорый выход более удобной версии OpenClaw.

OpenClaw — не единственный универсальный агент в рейтинге. Manus и Genspark также вошли в список — обе платформы позволяют потребителям поручать ИИ открытые задачи (исследования, анализ таблиц, создание презентаций), и ИИ выполняет整个 рабочий процесс от начала до конца. Manus вошел в рейтинг во второй раз, после上一次 включения он был приобретен Meta примерно за 2 миллиарда долларов в декабре 2025 года. Genspark — новичок этой версии — компания завершила раунд B финансирования на 300 миллионов долларов в начале этого года и объявила о достижении 100 миллионов долларов annualized дохода.

В мобильной сфере потребители обычно взаимодействуют с агентом через текст, а не через мобильное приложение. При установке пользователь подключает OpenClaw к таким платформам, как WhatsApp, Telegram и Signal, и отправляет ему指令, как другу, а он выполняет задачи в фоне. Другие продукты, like Poke, также предлагают类似的 агентный опыт через SMS.

Эти продукты будут напрямую конкурировать с агентными возможностями универсальных LLM-помощников, которые потребители используют ежедневно, — ChatGPT, Claude и Gemini. По мере того как эти гиганты строят свои собственные экосистемы коннекторов и приложений, выберут ли потребители одного из них в качестве основного агента? Ответ мы получим в ближайшие шесть месяцев.

5. ИИ выходит за пределы браузера и приложений

Каждая предыдущая версия этого рейтинга использовала два показателя для ранжирования ИИ-продуктов: веб-трафик и мобильная месячная аудитория. Но появляется новый класс ИИ-продуктов, которые невозможно уловить этими двумя показателями. За последний год некоторый最重要的 рост ИИ на потребительском конце произошел в продуктах,完全 невидимых в этих двух измерениях.

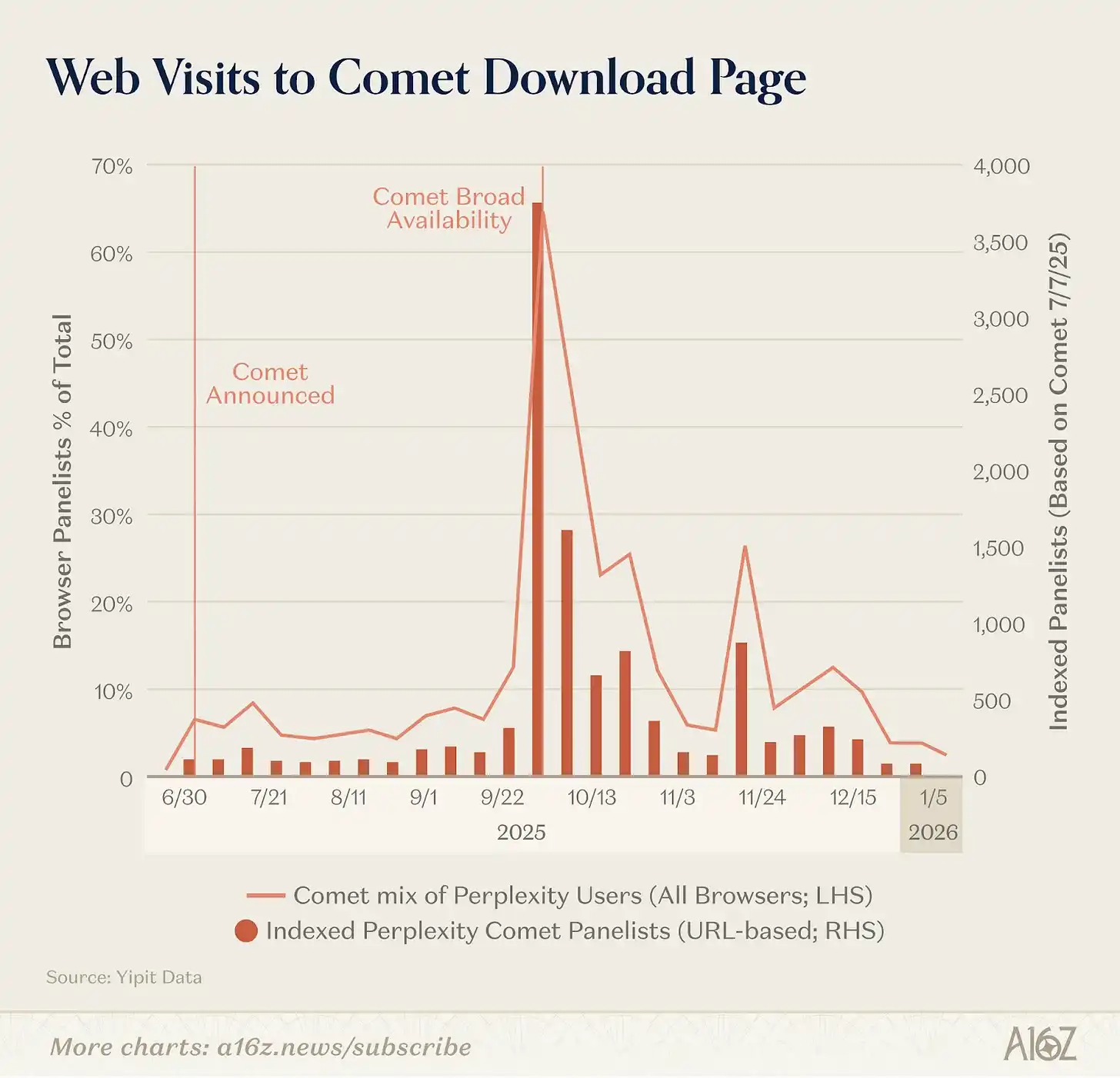

Самое очевидное изменение — сам браузер становится ИИ-продуктом. За последние девять месяцев OpenAI выпустила Atlas (браузер со встроенным ChatGPT на каждой странице), Perplexity выпустила Comet, Browser Company (позже приобретенная Atlassian) выпустила Dia. Данные Yipit показывают, что Comet от Perplexity оказал наибольшее влияние на рынок (по衡量 трафику страницы загрузки), но ни один ИИ-браузер не достиг ускоренного роста.

Другие ИИ-гиганты выбрали путь добавления ИИ в существующие браузеры, а не запуска отдельного ИИ-браузера. Google интегрировала Gemini в Chrome и выпустила бета-версию Disco, которая может динамически генерировать веб-приложения на основе вкладок пользователя. Anthropic выпустила Claude in Chrome, который может подключиться к сессии пользователя в Claude или Claude Code и驱动 действия на веб-странице.

Рост нативных десктопных ИИ-инструментов еще более стремителен, особенно среди инструментов для разработчиков. Claude Code — командный агент для разработчиков — всего за шесть месяцев достиг annualized дохода в 1 миллиард долларов. OpenAI выпустила独立ное приложение Codex для Mac, компания заявила, что у Codex в начале марта было 2 миллиона еженедельных активных пользователей с weekly ростом 25%. Cursor сохранила позицию в веб-топ-50.

Для чистых потребителей самые распространенные独立ные десктопные ИИ-приложения связаны с голосом. Инструменты для заметок, такие как Fireflies, Fathom, Otter, TL;DV и Granola, достигают пользователей через модель PLG, постепенно проникая в предприятия — совокупный трафик пяти крупнейших игроков превышает 20 миллионов посетителей. Рабочие пространства, такие как Notion (впервые в рейтинге в этой версии), также все чаще интегрируют ИИ через note-taking, research агентов и даже автоматизацию задач.

Наконец, ИИ все глубже внедряется в инструменты, которые люди уже используют. Anthropic выпустила Claude in Excel и Claude in PowerPoint. OpenAI выпустила ChatGPT for Excel. Google углубила интеграцию Gemini во всю линейку Workspace — Docs, Sheets, Gmail, Meet получили нативные ИИ-функции. Google также в январе 2026 года выпустила Personal Intelligence, подключив Gemini к Gmail, Google Photos, YouTube и Search, позволяя помощнику ссылаться на ваши бронирования отелей, покупки, фотоальбомы и историю просмотров без вашего主动 уведомления.

Вывод для этого рейтинга: наш рейтинг все больше недооценивает ИИ-продукты, которые люди используют больше всего на самом деле. Разработчик, который проводит восемь часов в день в Claude Code, или knowledge-работник, который диктует каждое письмо через Wispr, —都是 активные пользователи ИИ, но почти невидимы в данных веб-трафика. Когда ИИ превращается из направления в функцию,我们的 методология也必须 меняться.