Автор: Thejaswini M A

Компиляция: Saoirse, Foresight News

Я никогда в это полностью не верил. Не потому, что я умнее других, а потому, что те, кто громче всех кричат о децентрализации, часто больше всех спешат заманить ваши деньги в свою экосистему. В любой истории такое сочетание никогда не было добрым знаком.

Но я всё равно продолжал наблюдать. И вы тоже вынуждены смотреть, потому что это поистине самое захватывающее шоу на сегодняшний день. Вся отрасль построена на радикальной идее «доверительных денег», но люди внутри нее почти все недостойны доверия. Ирония повсюду.

Сегодня, как и все очевидные вещи, которые в конечном итоге становятся общеизвестными, люди постепенно приходят к выводу — а некоторые из нас знали это всё время: децентрализация всегда была больше похожа на спектакль, чем на настоящую убеждённость. Целью был сбор «глупых денег». Те, кто постоянно твердил, что «банки — враги», теперь пожимают руку самым централизованным политическим силам на планете только потому, что это выгодно их инвестиционному портфелю.

Я даже не злюсь. Я просто наблюдаю со стороны, потому что шоу слишком хорошее.

31 октября 2008 года, в разгар последствий финансового кризиса. Сатоши Накамото опубликовал белую книгу на девяти страницах. Он предложил электронную валюту без банков, без правительства, без чьего-либо разрешения. Две стороны торгуют напрямую, без посредников и без центрального органа, решающего, имеете ли вы право на сделку.

По правде, первоначальная идея была прекрасной. Она родилась непосредственно в мире, где хедж-фонды и центральные банки чрезмерно leveraged экономику, получали прибыль от потерь простых людей, а в случае провала полагались на государственную помощь. Гнев был полностью оправдан. Если такая система, которая позволяет элите набивать карманы, а публике — расплачиваться, не может вызвать гнев, то что может?

Гениальность архитектуры, разработанной Сатоши Накамото, заключалась именно в том, что она исключала человеческий фактор. Нет единой точки контроля — нет единой точки отказа. Вместо этого — тысячи узлов, равных друг другу и взаимно проверяющих. Вы не можете подкупить всю сеть, не можете пригрозить ей по телефону. И кошелёк не заморозят из-за плохого настроения какого-то регулятора.

Бессубъектный режим в design — это прекрасная концепция.

Люди любят винить в вырождении отрасли приток венчурного капитала, хаос NFT или крах FTX. Но это всего лишь симптомы. Настоящая проблема появилась гораздо раньше — если вы были достаточно внимательны, она была видна почти с самого начала.

Проблема децентрализации в том, что она дорогая, медленная и требует координации тысяч участников, не имеющих мотивации к консенсусу. А централизация эффективна, быстра и прибыльна. Поэтому, когда на кону появились реальные деньги, экономические законы начали действовать, как всегда. Отрасль начала разделяться, но мало кто хотел говорить об этом открыто.

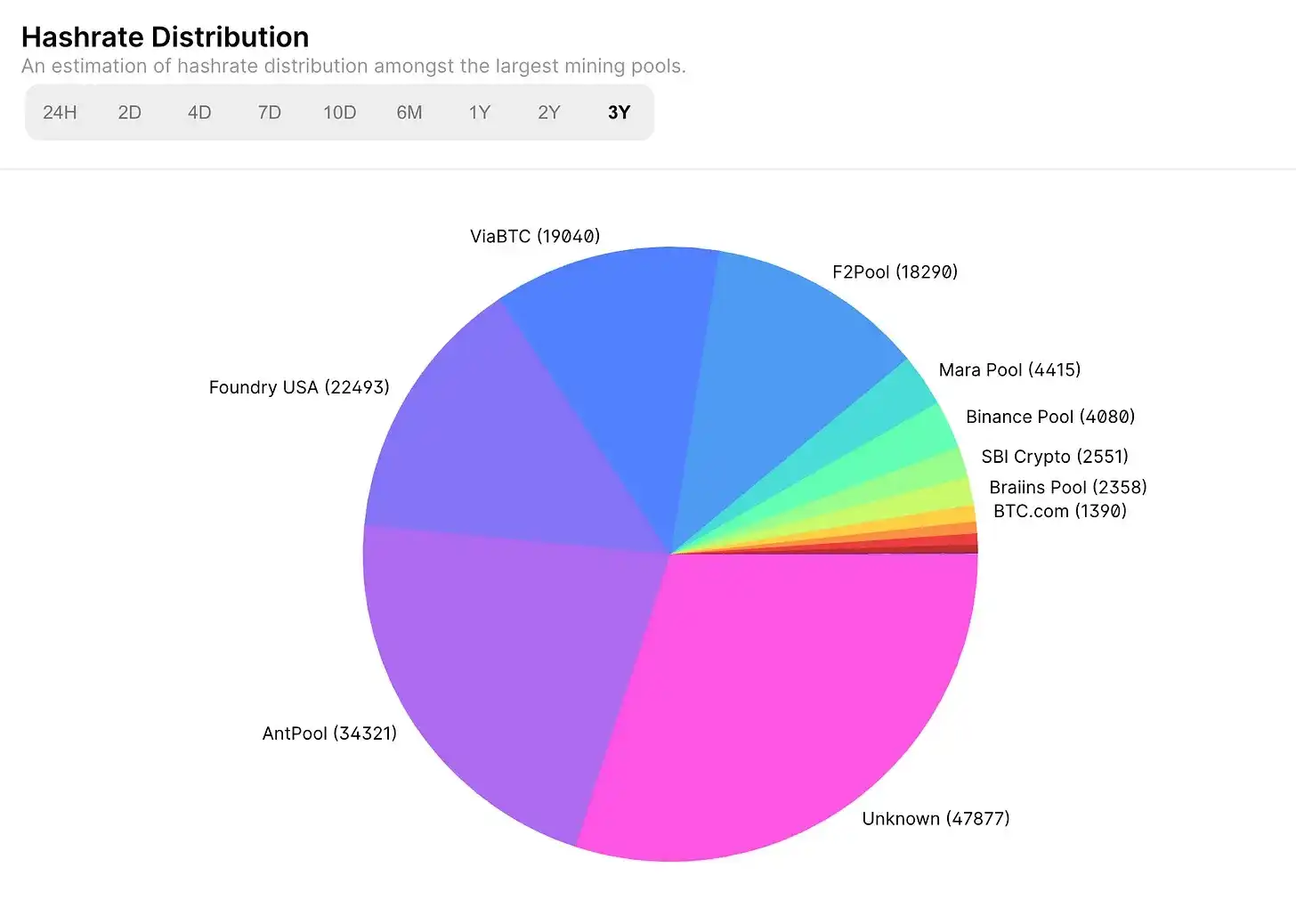

В мае 2017 года на две крупнейшие майнинговые пулы Биткойна приходилось менее 30% общей хэш-мощности, а на шесть крупнейших — менее 65%. Это был самый децентрализованный момент в истории майнинга Биткойна. Девять лет спустя пик давно пройден. К декабрю 2023 года два крупнейших пула контролировали более 55% хэшрейта, а шесть крупнейших — 90%.

Сегодня Foundry USA контролирует около 30% общей хэш-мощности сети, Antpool — около 18%, вместе они приближаются к 50%. А к марту 2026 года абстрактный риск стал реальностью: Foundry последовательно добыл шесть блоков, вызвав редкую реорганизацию цепи из двух блоков, которая перекрыла законные блоки Antpool и ViaBTC. Мелкие майнеры смотрели, как их действительная работа стирается из ledger. Биткойн никогда не подвергался атаке 51%, целостность сети сохраняется, но риск централизации, от которого изначально должна была защитить белая книга, давно перестал быть теорией и стал цифрами на графике, движущимися в опасном направлении.

Белая книга описывала систему, в которой ни один субъект не мог бы сделать этого. В этом году ей исполнилось восемнадцать. Можете сделать выводы сами.

Я хочу быть точным в формулировках, потому что ленивая критика легко уходит в сторону. Поверьте, я пробовал.

Посмотрите на все криптопродукты, которые сегодня имеют реальных пользователей, реальные объемы торгов, реальные доходы: подавляющее большинство из них не являются децентрализованными.

Но действительно ли они заявляли о своей децентрализации? Смешение этого момента сделает вашу критику острой, но направленной не туда.

Стейблкоины — это единственная безоговорочно успешная категория в криптоиндустрии. Используются для торговли,跨境汇款, в качестве платежного инструмента в странах с постоянно обесценивающейся национальной валютой. По состоянию на 2025 год, USDT и USDC вместе занимают 93% общей рыночной капитализации стейблкоинов, обрабатывая беспрецедентные объемы транзакций в триллионы долларов.

@visaonchainanalytics

И USDC, и USDT выпускаются компаниями, и обе могут замораживать кошельки. Не говоря уже о том, что их резервы хранятся в банках — институтах, которые эта отрасль должна была заменить. Децентрализованный стейблкоин DAI, который часто приводят в качестве доказательства сохранения идеалов, имеет долю рынка всего 3–4%. Никто никогда не продавал вам USDT как децентрализованный продукт, его козырем всегда была эффективность.

Межбанковские переводы долларов за несколько минут, расчеты за секунды, без банков-корреспондентов, без кодов SWIFT, без трехдневного периода клиринга. Они сохранили эмитента, но убрали все неэффективные и дорогие промежуточные звенья между эмитентом и пользователем. Настоящую «революцию» традиционные финансы проиграли централизованному доллару, заново выпущенному компанией на блокчейне. И это было его первоначальным обещанием, и он его сдержал.

Hyperliquid, с объемами торгов в миллиарды, очень быстрый, сам продукт впечатляет. Но по любому практическому смыслу им управляют 16 валидаторов. Во время инцидента с JELLY в марте 2025 года эти 16 валидаторов достигли консенсуса и за две минуты сняли с листинга определенный токен, превратив надвигающийся убыток протокола в 12 миллионов долларов в прибыль. Две минуты. Чтобы добиться какого-либо решения в управлении Ethereum за две минуты, вероятно, потребуется стихийное бедствие, и даже в этом случае кто-то в забытом часовом поясе, возможно, напишет блог с несогласным мнением.

Некоторые называли это FTX 2.0, но такая характеристика неточна. Hyperliquid принял корпоративное решение. Что действительно заслужило признание, так это то, что они решили проблему, компенсировали пользователям, внедрили механизм голосования валидаторов в сети для будущих делистингов и продолжили работу. Проблема в том, что какое-то время маркетинг Hyperliquid тратил много усилий, утверждая, что они не компания, при этом действуя точно так же, как компания.

Прогнозные рынки. Polymarket пережил первый по-настоящему мейнстримный момент выхода криптоиндустрии в свет во время президентских выборов в США в 2024 году. Журналисты цитировали его цены, им пользовались люди, никогда не державшие ETH. Никто никогда не спрашивал, достаточно ли он децентрализован, людей интересовало только, точен ли он. И он был точен. Время от времени появлялись статьи о инсайдерской торговле и позиционировании как «машины истины», некоторые из них вышли из-под моего пера. Это просто полезный продукт, использующий криптотехнологии как underlying infrastructure, а не как идеологический символ.

О DAO я мог бы написать целый абзац, но три слова «Децентрализованная Автономная Организация», пожалуй, самая комичная комбинация в языке. На этом остановимся.

Вот что действительно работает, и большинство из этого гораздо удобнее схем, описанных в белой книге.

Сегодняшний криптомир разделился на два типа.

Первый — это инфраструктурный уровень: созданный для эффективности, масштаба и реального использования, жертвующий децентрализацией ради производительности, и в большинстве своем открыто об этом заявляющий.

Второй — протокольный уровень: Биткойн, Ethereum, Solana, которые структурно по-прежнему fundamentally отличаются от всех предыдущих систем, децентрализация для них — не маркетинговый ход, а design attribute, сохраненный под огромным adversarial pressure. Продукты идут на уступки пользовательскому спросу, а пользователи хотят только удобные вещи. Под давлением конкуренции за реальные деньги отрасль неизбежно движется к централизации. Это просто закономерность, а не моральный провал. Революционная риторика протокольного уровня постоянно заимствуется продуктовым уровнем, даже though они уже давно не одно и то же.

Основатель, который в 2019 году еще цитировал в речах Манифест крипто-панков, к 2023 году уже сидел на слушаниях в Сенате, заявляя, что всегда хотел конструктивно сотрудничать с регуляторами. Для большой части отрасли децентрализация была просто regulatory strategy, замаскированной под идеологию: если никто не отвечает, то и нести ответственность не нужно. Этой идеологии было достаточно, чтобы запутать юристов и регуляторов, дать время привлечь финансирование, запустить продукт и во многих известных случаях благополучно уйти. Когда регулирование стало неизбежным, эту идеологию отложили в сторону, чтобы не навлечь неприятностей.

В отрасли still есть настоящие верующие. Они пришли в криптомир, потому что видели, как правительства разрушают валюты, замораживают счета по политическим причинам, исключают целые группы из базовых финансовых услуг. Они стали моральным прикрытием для отрасли, по своей сути нацеленной на извлечение прибыли. Само по себе извлечение прибыли не предосудительно, но не нужно притворяться.

На мой взгляд, эта сделка, возможно, стоила того, и те, кто сделал выбор, понимают это, даже если не скажут в слух. Чистая форма идеи децентрализации изначально с трудом продвигалась в реальности. Никто не собирался втайне, чтобы убить децентрализацию. Дело просто в том, что когда людям приходится выбирать между «удобным продуктом» и «неработающим принципом», они каждый раз выбирают первое. Безмолвно, без объявления, без похорон.

А что мне кажется truly ироничным, так это то, как эта история разыгрывается на политической арене.

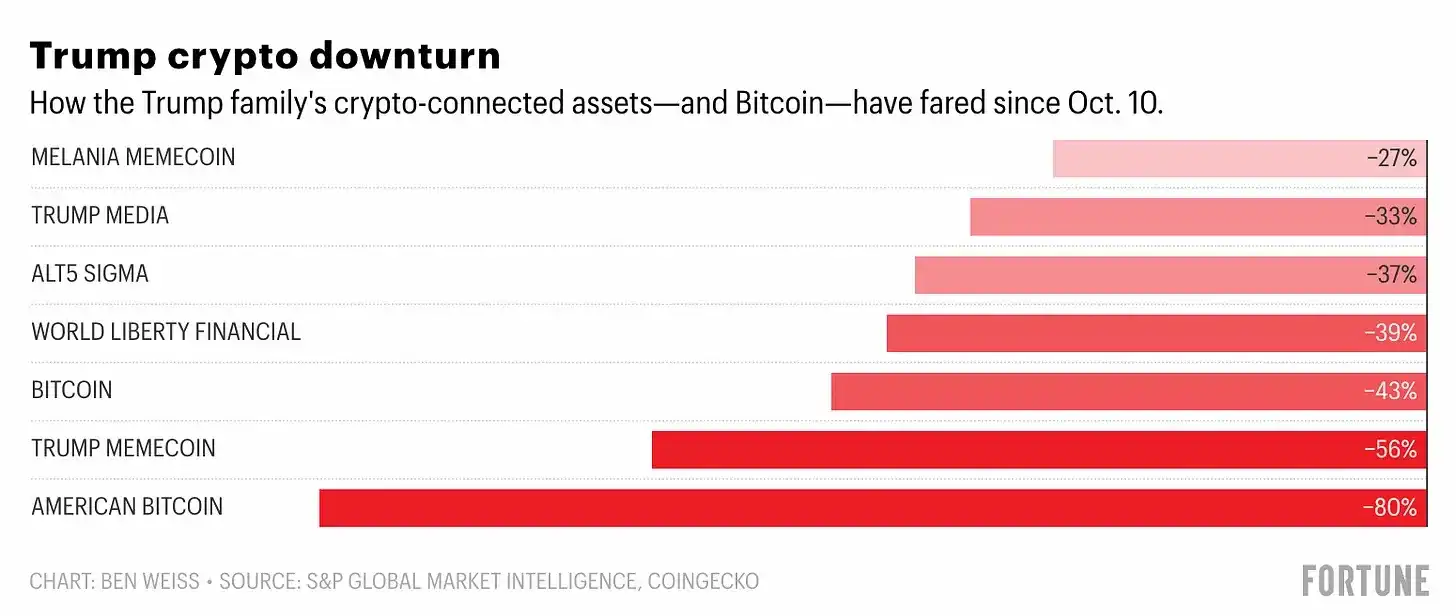

До подписания любого закона, связанного с крипто, назначения любого прокипто-регулятора, выручка Trump Organization в первом полугодии 2025 года взлетела в 17 раз, до 864 миллионов долларов, причем более 90% поступило от крипто-связанных проектов. Согласно анализу The Wall Street Journal, к началу 2026 года семья Трампа только от World Liberty Financial вывела как минимум 1,2 миллиарда долларов. Его 19-летний сын Бэррон был указан на сайте проекта как «DeFi визионер». Честно говоря, стоит почтить пятью минутами молчания того, кто написал этот текст.

@fortune.com

Этот человек в 2021 году еще называл Биткойн аферой, а к 2024 году уже вышел на трибуну Биткойн-конференции. Та группа людей, которая годами утверждала, что «правительство не имеет права контролировать ваши деньги», наблюдала, как действующий президент напрямую извлекает прибыль из отрасли, которую он регулирует, и основная реакция заключалась в предсказаниях цены монет и возгласах «бычий рынок».

В экономике есть концепция выявленных предпочтений: то, что вы actually делаете, говорит о вас больше, чем то, в что вы声称 верите. Предпочтение, выявленное децентрализованным движением при проверке реальной политической средой, таково: мы заботимся о децентрализации, пока не приходится платить за это; после этого нас волнует только цена.

Я не хочу слишком много судить. Я просто фиксирую, как есть, потому что кто-то должен это делать.

Та одержимость 2017 и 2021 годов с лозунгом «мы изменим мир» в основном рассеялась. Толпа NFT разошлась, в метавселенной люди нашли другие темы, на которые можно с уверенностью нести чушь. Оставшиеся стали тише, с меньшим мессианским комплексом и гораздо честнее в том, что они на самом деле делают. Протокольный уровень работает как designed, прикладной уровень создал потрясающие продукты. Эта революция всё же породила практическую финансовую инфраструктуру, изменила способ глобального перемещения стоимости и сделала огромное количество людей extremely богатыми.

Я хочу сказать только одно: будьте честны в том, что вы делаете.

Если вы делаете централизованную биржу с лучшим пользовательским опытом и крипто-каналом, так и говорите. Если ваш стейблкоин выпускается компанией, может замораживать кошельки, а резервы хранятся в банках, так и говорите. Если вашим DAO фактически управляют три кошелька, и все присутствующие это понимают, вы тоже можете так сказать. Пользователи выдержат честность. Что они не выдержат в долгосрочной перспективе, так это разрыв между нарративом и реальностью. И в конечном итоге они выражают свое недовольство уходом.

Сатоши Накамото молчит уже пятнадцать лет. Возможно, он предвидел всё это и chose наблюдать за этим спектаклем из-за кулис. Или же он просто знал, когда стоит уйти.