Author: Prathik Desai

Original Title: The CLARITY Paradox: When clearer rules cloud competition

Compiled and Edited by: BitpushNews

Historically, money has rarely been neutral; it inherently possesses an appreciative attribute. Long before the emergence of modern banking, people expected that holding or lending money should yield returns.

As early as the third millennium BCE, ancient Mesopotamia saw practices of charging interest on silver loans. From the fifth century BCE onwards, ancient Greece utilized maritime loans to finance high-risk sea trade.

In this system, lenders provided funds for a merchant's single voyage. If the ship sank, they bore the entire loss, but if it returned successfully, they demanded high interest rates (typically between 22% and 30%). In Rome, interest was deeply embedded in economic life, often triggering debt crises that made voluntary debt relief a political necessity.

Throughout these systems, one concept remained consistent: money was not merely a passive store of value. Holding money without compensation was the exception. Even with the advent of modern finance, the perception of money's nature was further reinforced. Bank deposits could yield interest for savers. It was widely accepted that money that did not appreciate would gradually lose its economic value.

It is against this backdrop that stablecoins entered the financial system. If you strip away the blockchain facade, they share little in common with any cryptocurrency or speculative asset. They present themselves as digital dollars, adapted to a blockchain world that eliminates geographical boundaries and saves costs. Stablecoins promise faster settlement, lower friction, and 24/7 availability.

However, U.S. law seeks to prohibit stablecoin issuers from paying yields (or interest) to holders.

This is why the CLARITY Act, currently under review in the U.S. Congress, has become such highly contentious legislation. Viewed in conjunction with its sister bill, the GENIUS Act, which passed in July 2025, this act prohibits stablecoin issuers from paying interest to holders but allows for "activity-based rewards."

This has prompted strong opposition from the banking industry to the current draft of the legislation. Some amendments proposed by banking lobbyists aim to completely stifle stablecoin rewards.

In today's in-depth analysis, I will explain why the CLARITY Act in its current form could impact the crypto industry and why this has left the crypto sector visibly dissatisfied with this legislative proposal.

Let's get into it...

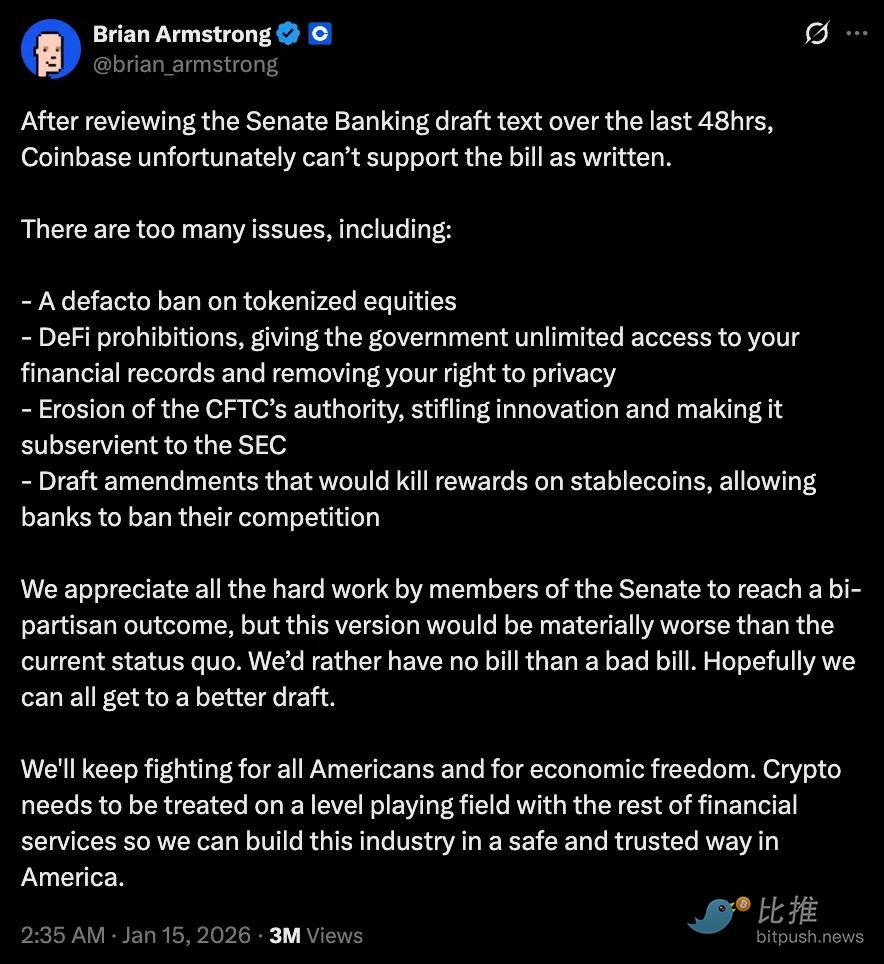

Within 48 hours of reviewing the Senate Banking Committee's draft, Coinbase publicly withdrew its support.

"We would rather have no bill than a bad bill," its CEO Brian Armstrong stated on Twitter, arguing that this proposal, which claims to provide regulatory clarity, would make the industry's situation worse than it is now.

Just hours after the largest U.S. listed crypto company withdrew its support, the Senate Banking Committee postponed its markup session—a meeting intended to discuss amendments to the bill.

The core objections to the bill cannot be ignored. The bill aims to treat stablecoins purely as payment instruments, not as any form of monetary equivalent. This is precisely the crux of the controversy, enough to unsettle anyone expecting stablecoins to revolutionize payments.

This version of the bill demotes stablecoins to mere pipelines, rather than assets that can be used to optimize capital. As I described earlier, money has never operated this way. By prohibiting interest at the base level and banning activity-based rewards for stablecoin use, the bill restricts stablecoins from achieving yield optimization, which is what they claim to excel at.

This is also where concerns about competition arise. If banks are allowed to pay interest on deposits and offer rewards for debit/credit card usage, why prohibit stablecoin issuers from doing the same? This tilts the playing field in favor of existing financial institutions and undermines many of the long-term benefits promised by stablecoins.

Brian's criticism extends beyond stablecoin yields and rewards, also touching on how the bill does more harm than good. He also pointed out the issue of the DeFi ban.

@brian_armstrong

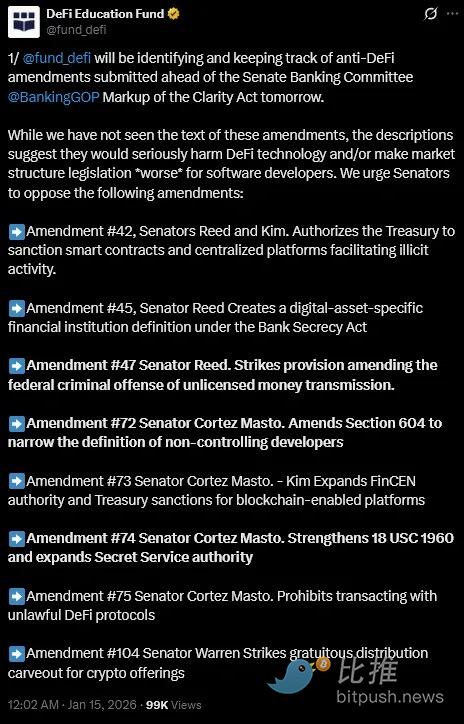

The DeFi Education Fund, a DeFi policy and advocacy organization, also urged senators to oppose legislative amendment proposals that appear "anti-DeFi."

"While we have not yet seen the text of these amendments, their description suggests they would severely harm DeFi technology and/or make market structure legislation more unfavorable for software developers," the organization posted on X.

@fund_defi

Although the CLARITY Act formally acknowledges decentralization, its definition is narrow. Protocols under "common control" or those retaining the ability to modify rules or restrict transactions risk being subjected to bank-like compliance obligations.

Regulation aims to introduce scrutiny and accountability. However, decentralization is not static. It is a dynamic spectrum, requiring evolving governance and contingency controls to provide resilience, not dominance. These rigid definitions create additional uncertainty for developers and users.

Next is the tokenization space, where there is a vast gap between promise and policy. Tokenized stocks and funds offer faster settlement, lower counterparty risk, and more continuous price discovery. Ultimately, they enable more efficient markets by compressing clearing cycles and reducing capital trapped in post-trade processes.

However, the current draft of the CLARITY Act leaves tokenized securities in a regulatory vacuum. Its wording does not explicitly prohibit them but introduces sufficient uncertainty regarding the custody of tokenized stocks.

If stablecoins are framed within the payments sphere and tokenized assets are constrained at the issuance stage, the path to more efficient capital markets will be significantly narrowed.

Some argue that stablecoins can exist as payment tools, while yields can be provided through tokenized money market funds, DeFi vaults, or traditional banks. This is not technically wrong. But there will always be market participants seeking more efficient ways to optimize capital. Innovation drives people to find workarounds. Often, these workarounds might involve moving capital overseas. Sometimes, this movement might even be opaque, in ways that regulators might later regret not foreseeing.

However, one argument stands above all others as the primary reason for opposing the bill. It's hard not to see that the bill in its current form structurally reinforces banks, weakens the prospects for innovation, and shackles an industry that could help optimize our current markets.

Worse, it might achieve this at two very high costs. The bill stifles any hope of healthy competition between the banking and crypto industries, while simultaneously allowing banks to profit more. Secondly, it leaves customers at the mercy of these banks, unable to choose to optimize their own yields within a regulated market.

These are high prices to pay, and precisely why critics are reluctant to offer support.

It is concerning that the bill is packaged as an effort to protect consumers, provide regulatory certainty, and bring crypto into the system, while its terms subtly suggest the opposite purpose.

These terms predetermine which parts of the financial system are allowed to compete for value. While banks can continue to operate within familiar boundaries, stablecoin issuers will feel compelled to exist and operate within a narrower economic landscape.

But money dislikes remaining passive. It flows towards efficiency. History shows that whenever capital is constrained in one channel, it always finds another. Ironically, this is precisely the situation the regulation aims to prevent.

Favorably for the crypto industry, the disagreement over this bill is not limited to the crypto sphere.

The bill still lacks sufficient support in Congress. Some Democrats are unwilling to vote in favor without discussion and deliberation on certain proposed amendments. Without their support, the bill cannot advance, even if it dismisses the crypto industry's opposition as noise. Even if all 53 Republicans vote for the bill, it would need at least 7 Democratic votes in the full Senate to pass with a supermajority and overcome a filibuster.

I do not expect the U.S. to produce a bill that satisfies everyone. I don't even think that is possible or desirable. The issue is that the U.S. is not merely regulating a new class of assets; it is attempting to legislate for a form of money whose inherent properties make it highly competitive. This makes it more difficult because it forces lawmakers to confront competition and draft terms that might challenge existing institutions (in this case, banks).

The impulse to tighten definitions, restrict permitted activities, and preserve existing structures is understandable. However, this risks turning regulation into a defensive tool that repels rather than attracts capital.

Therefore, it is essential to correctly understand the质疑 (questioning/doubts) surrounding the Clarity Act—this is not opposition to regulation itself. If the goal is to truly integrate crypto assets into the financial system, rather than simply fencing them off, then the U.S. needs to formulate rules that allow new forms of money to compete, experiment, and evolve within clear regulatory boundaries. This, in turn, would force traditional financial institutions to enhance their own.

In the final analysis, legislation that harms those it is supposed to protect is worse than no legislation at all.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush