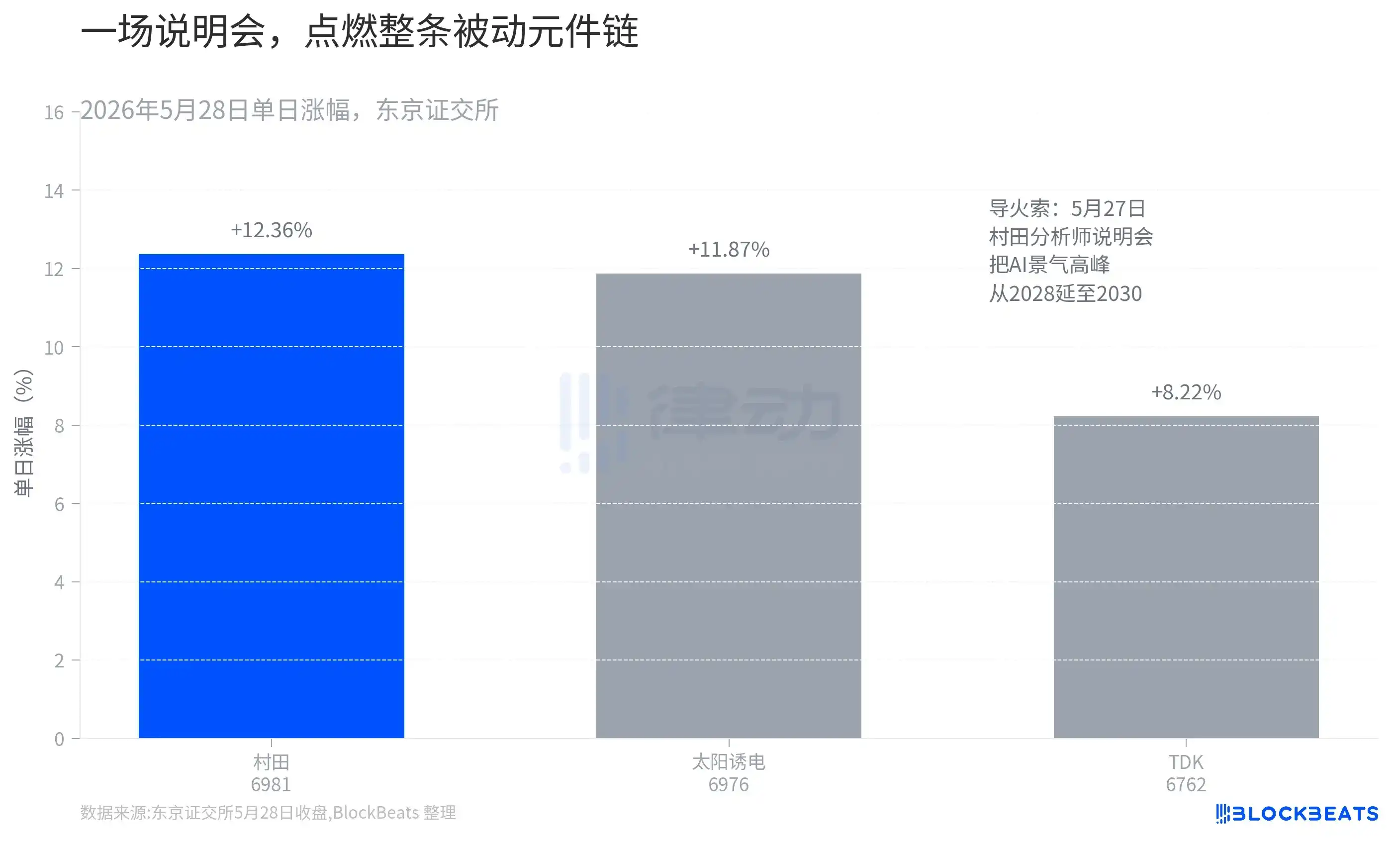

28 мая Murata Manufacturing, крупнейший в мире производитель пассивных электронных компонентов, выросла на Токийской фондовой бирже на 12.36%, в ходе торгов коснувшись верхнего лимита и закрывшись на уровне 8787 иен, обновив исторический максимум с учетом дробления. Два месяца назад мы разбирали статью о том, как Murata повысила цены на MLCC (многослойные керамические конденсаторы) для AI-серверов на 15–35%, где речь шла о том, как этот конденсатор размером менее миллиметра влияет на цепочки поставок для AI-вычислений. На этот раз разбирать стоит не конденсатор, а саму акцию Murata.

Потому что если открыть только что опубликованный финансовый отчет Murata, обнаруживается контраст: результаты на самом деле довольно скромные, а цена акции за год уже удвоилась.

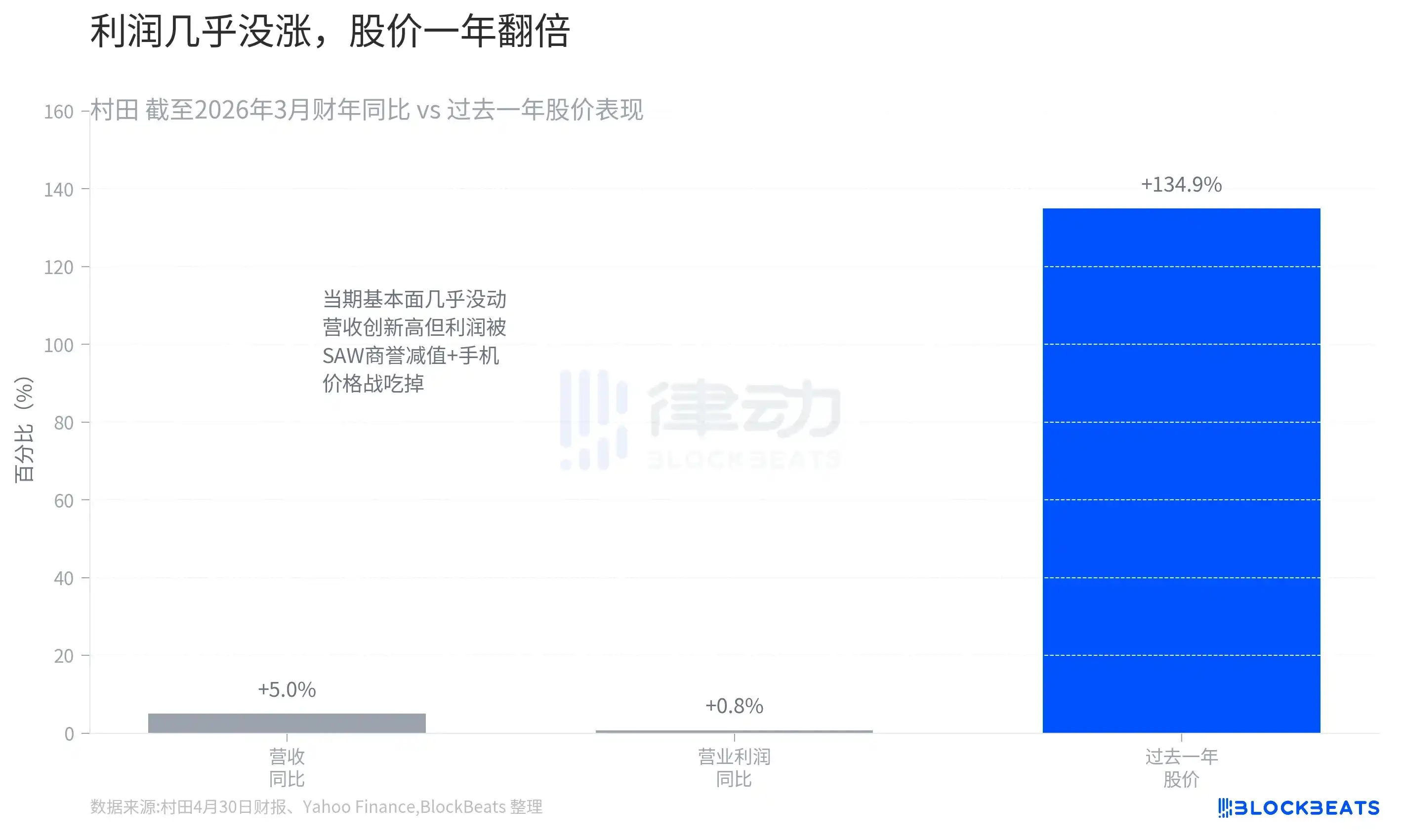

Согласно отчету Murata от 30 апреля, за финансовый год, завершившийся в марте 2026 года, выручка компании составила 1.83 трлн иен, что является рекордным показателем, но рост по сравнению с предыдущим годом составил всего 5.0%. Операционная прибыль — 281.8 млрд иен, рост всего на 0.8%, практически на месте. Прибыль сдерживали два фактора: во-первых, обесценение гудвила, связанного с бизнесом ПАВ-фильтров (SAW), а во-вторых, продолжающаяся ценовая война в зрелых сегментах, таких как смартфоны. Другими словами, как бы ярко ни выглядело направление ИИ, оно лишь компенсирует потери в зрелом бизнесе.

Но за тот же период времени цена акций Murata за последний год выросла примерно на 134.9% (по данным Yahoo Finance), последняя цена превысила 9000 иен, рыночная капитализация достигла уровня около 17 трлн иен, а коэффициент P/E поднялся примерно до 75. Компания, производящая пассивные компоненты с нулевым ростом текущей прибыли, оценивается рынком с P/E 75 — это может означать только одно: покупатели совсем не смотрят на текущую прибыль, они делают ставку на будущую историю.

Настоящим триггером стал брифинг

Запустил этот ралли не рост цен и не финансовый отчет, а небольшой брифинг (small meeting) для аналитиков, который Murata провела 27 мая.

Согласно информации от инвестиционного блогера kabuya66, основанной на содержании встречи, руководство Murata озвучило два ключевых момента. Первый — прогноз пика инвестиций в ИИ был пересмотрен с «примерно к 2028 году» до «будет продолжаться примерно до 2030 года». Для компании с фондоемким производством и планированием под заказ удлинение цикла подъема на два года означает дальнейшее накопление портфеля заказов и более уверенную окупаемость инвестиций в расширение. Второй момент был еще прямее: клиенты сейчас «гарантируют объем, а не цену», спрос примерно в два раза превышает предложение, что означает, что ниже по цепочке заказчики борются за поставки, не обращая внимания на цену, лишь бы получить объем.

Сила воздействия этих слов видна по торговой сессии на следующий день. В день, когда Murata выросла на +12.36%, акции конкурентов Taiyo Yuden выросли на 11.87%, а TDK — на 8.22% (по данным закрытия Токийской фондовой биржи). Брифинг лидера рынка привел к переоценке не одной акции, а всей цепочки пассивных компонентов. В тот же день индекс Nikkei 225 впервые превысил отметку 66000 пунктов, и сектор MLCC был одним из локомотивов роста.

Рынок покупает «завтрашнюю» колонку

Брифинг смог разжечь рост, потому что он позволил рынку увидеть потенциал прибыли Murata в следующем году.

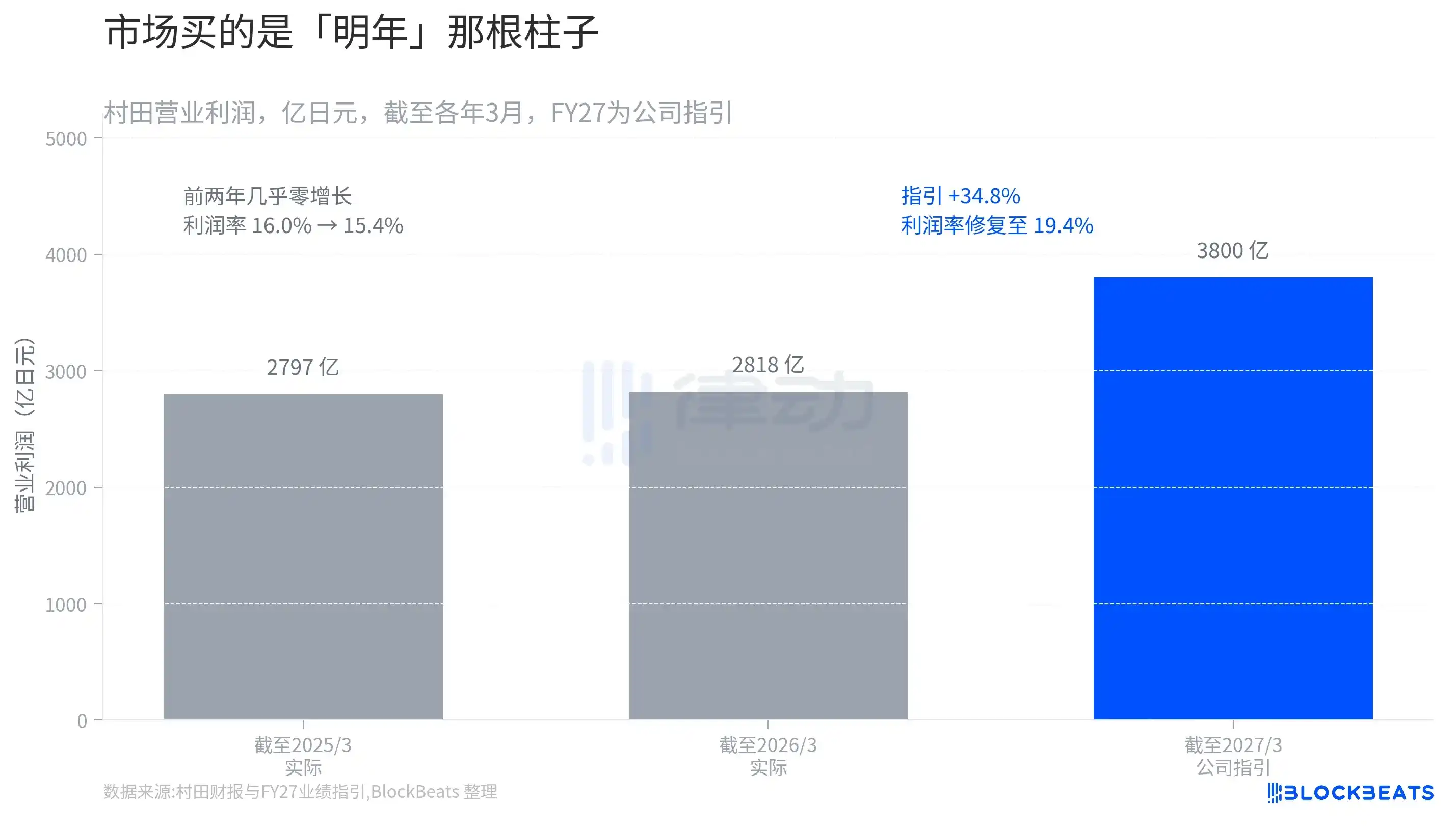

Если представить операционную прибыль Murata в виде трех столбиков, история становится наглядной. За финансовый год, закончившийся в марте 2025 года — 279.7 млрд иен, за год, закончившийся в марте 2026 года — 281.8 млрд иен, два года подряд практически нулевого роста, а рентабельность даже снизилась с 16.0% до 15.4%. Но прогноз Murata на текущий финансовый год (до марта 2027 года) — операционная прибыль в 380 млрд иен, что означает рост на 34.8% и восстановление рентабельности до 19.4%.

Весь рост заключен в самом правом столбике. Рынок сейчас покупает не два уже прошедших спокойных года, а этот еще не реализованный прогнозный столбик. Косвенным подтверждением является портфель заказов: согласно статистике Nikkei Veritas, среди публичных компаний с капитализацией выше 50 млрд иен и ожидаемой прибылью в текущем финансовом году, Murata заняла первое место по темпу роста портфеля неисполненных заказов (backlog) в прошлом финансовом году. Портфель неисполненных заказов напрямую соответствует будущей выручке — вот что дает уверенность в этом прогнозном столбике. Murata также объявила о плане обратного выкупа акций на сумму до 150 млрд иен, планируя выкупить 75 млн акций, что составляет 4.12% выпущенных акций. Руководство, используя реальные деньги, признает, что текущая цена не так уж и высока.

Поддерживает этот столбик удвоение выручки от ИИ

Откуда же берется рост прибыли на 34.8%? Ответ сосредоточен на одном направлении.

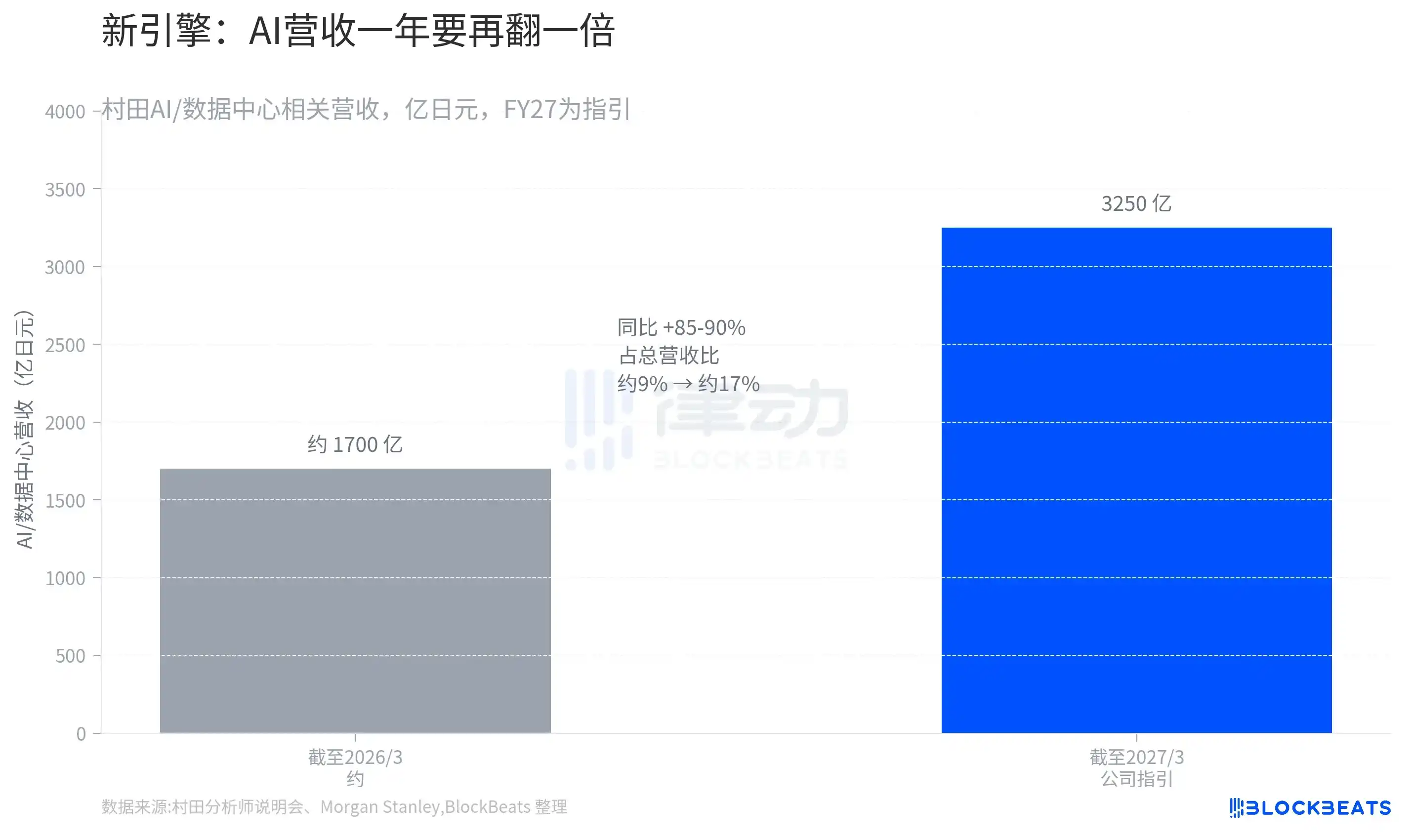

Согласно данным брифинга Murata, выручка компании, связанная с ИИ / центрами обработки данных, вырастет с примерно 170 млрд иен в прошлом финансовом году до прогнозируемых 325 млрд иен в текущем финансовом году, что означает рост на 85–90%. Доля этого направления в общей выручке увеличится примерно с 9% до примерно 17%. Другими словами, за год ИИ превратится для Murata из небольшой доли в статью, составляющую почти пятую часть выручки.

Что еще более важно — «качество» этой части роста. Согласно анализу Morgan Stanley MUFG Securities, рост выручки Murata от ИИ в этом раунде обусловлен не повышением цен на существующие продукты MLCC, а обновлением продуктового портфеля — увеличением доли передовых продуктов меньшего размера и большей емкости, что поднимает среднюю отпускную цену (ASP). Доля Murata на рынке передовых MLCC для AI-серверов превышает 70%, и у нее практически нет конкурентов, способных за ней угнаться. Это означает, что ее повышение цен — не циклическое «растут из-за дефицита», а структурное «дорого, потому что только мы можем это сделать». Рынок готов платить P/E 75 именно за эту признанную устойчивой ценовую власть.

Конечно, обратная сторона покупки ожиданий на исторических максимумах — это то, что ожидания уже ушли вперед. Президент Murata Норихиро Накадзима сам признает, что не исключает, что прогнозы спроса некоторых клиентов «могут быть завышены». Если темп инвестиций в ИИ замедлится или прогнозы на последующие кварталы окажутся ниже ожиданий, такая высокая оценка также несет в себе риск быстрого снижения. Для акций с высокой оценкой «недостаточно хорошо» — достаточная причина для продажи.

Murata по-прежнему остается производителем конденсаторов, изменилось только то, какой меркой рынок решил ее мерить: от компании-производителя компонентов с «неизбежным снижением цен» циклического характера к «поставщику лопат для ИИ» с ограниченным предложением и ценовой властью.