Over the past two years, the narrative logic of the AI industry's first half primarily revolved around the 'large model war' initiated by major tech giants. Model parameters progressed from hundreds of billions to trillions, training costs rose from tens of millions to hundreds of millions of US dollars, and GPU clusters expanded from thousands to tens of thousands of cards. Everyone discussed whose model was more powerful, who was closer to AGI, as if the endpoint of AI competition was determined solely by the performance metrics of the large models themselves.

By 2026, the driving logic of the AI industry has shifted. JPMorgan's latest report suggests that what will truly drive the continued expansion of AI infrastructure in the future is no longer model training, but the massive demand for AI inference. The largest consumer of computing power will no longer be just training large models, but the ubiquitous AI Agents scattered across the globe. Every call, every interaction, every task execution is essentially consuming Tokens. The AI industry is transitioning from the 'Model Era' to the 'Token Industry Era.'

Because what will truly power the future AI world is not just the models themselves, but the entire system of Token production, distribution, scheduling, and consumption that forms around them. Especially with the large-scale emergence of AI Agents, how Tokens are generated in real-time, distributed across regions, dynamically scheduled, and efficiently consumed will become the core new challenge for the entire AI industry.

As Jensen Huang recently proposed, AI is not a simple software industry but an infrastructure system akin to electricity and the internet. In his 'five-layer cake' architecture, the AI industry is divided into five structural layers: Energy, Chips, Infrastructure, Models, and Applications. As the AI industry gradually shifts from the 'Training Era' to the 'Inference Era,' GoodVision AI prefers to conceptualize the entire AI economic industrial chain as a 'seven-layer cake structure' revolving around Tokens:

First Layer: Electricity – The Energy Foundation of the AI Era

Second Layer: AIDC – The Token Factory

Third Layer: GPU – The Token Production Equipment

Fourth Layer: LLM – The Token Production Engine

Fifth Layer: Token Distribution – The 'Power Grid' of the AI Era

Sixth Layer: Token Optimization & Intelligent Scheduling – The Brain of the AI Era

Seventh Layer: AI Agent – The Token Consumption Terminal

From energy and GPUs to AIDCs, edge nodes, model inference, and intelligent scheduling, the AI industry is forming an unprecedented 'Token Industrial System.'

However, this system is still far from mature.

Some possess the most advanced GPUs but are constrained by energy supply; some have built massive AIDCs but lack efficient scheduling; some develop powerful AI Agents but face high inference costs and latency; some control edge nodes but cannot form a unified, collaborative network. Although the entire industrial chain is developing rapidly, there remains significant fragmentation, redundancy, and efficiency bottlenecks between layers.

Only when these seven layers of infrastructure are truly interconnected, coordinated, and integrated will the AI industry transition from today's 'Tool Era' to the true 'Mass Adoption Era' belonging to the intelligent world.

First Layer Cake: Electricity – The Energy of the AI Era

The Industrial Revolution competed for coal and oil, the Internet era competed for traffic and servers, and the AI era sees the most fundamental war returning to energy.

Because AI ultimately consumes electricity. The power consumption of a large AI data center is already comparable to that of a medium-sized city. Newly built AIDCs (AI Data Centers) worldwide are facing the same problem: GPUs can be purchased, land can be acquired, but power supply and grid scheduling lag behind.

This is why more and more AI companies are refocusing on energy infrastructure. At GTC 2026, Jensen Huang even defined the future data center as a 'Token Factory.' The upstream of this factory will give rise to a super energy industry.

In the Chinese market, companies like China Yangtze Power, China National Nuclear Power, CGN Power, China Three Gorges Renewables, Longyuan Power, and Huadian New Energy represent core energy directions including hydropower, nuclear power, wind power, and photovoltaics. Among these, nuclear and hydropower, with their stable supply capabilities, are becoming the most important foundational energy sources for AIDCs; while wind and solar benefit from the AI industry's demand for green power and ESG standards. With the advancement of 'East Data West Computing' and large-scale AI data center construction, the synergy between new energy bases and computing power centers is rapidly strengthening.

In the US market, traditional energy giants like NextEra Energy, Dominion Energy, Duke Energy, Southern Co., and Exelon are also benefiting from the expansion of AI data centers. Among them, NextEra is a leader in North American green power; Dominion controls core transmission resources in Northern Virginia's 'Data Center Corridor'; Exelon, with its stable nuclear power supply, is becoming a key beneficiary of the AI era's demand for 'all-weather high-stability power.' Overall, the global power industry is gradually upgrading from a traditional utility to a core resource layer in the AI infrastructure era.

Overall, the competitive landscape at this layer is shifting from the traditional 'electricity price competition' among energy companies to a 'power locking right competition' between downstream AI data centers, cloud providers, and energy companies. Whoever can secure long-term, stable, low-cost energy holds the first dragon ball for Token production.

Second Layer Cake: AIDC – The Raw Token Factory

A single GPU is meaningless; what truly matters is the scaled cluster. Hence, the emergence of the AIDC.

It is like the steel mills, power plants, and assembly line factories of the industrial era, concentrating thousands of GPUs to form stable Token production capacity. But factory problems are also emerging: traditional AIDC construction cycles often last 18 to 36 months, with grid expansion taking even longer. When AI demand grows exponentially, the construction speed of the old-era IDC can no longer meet the needs of the new Token economy.

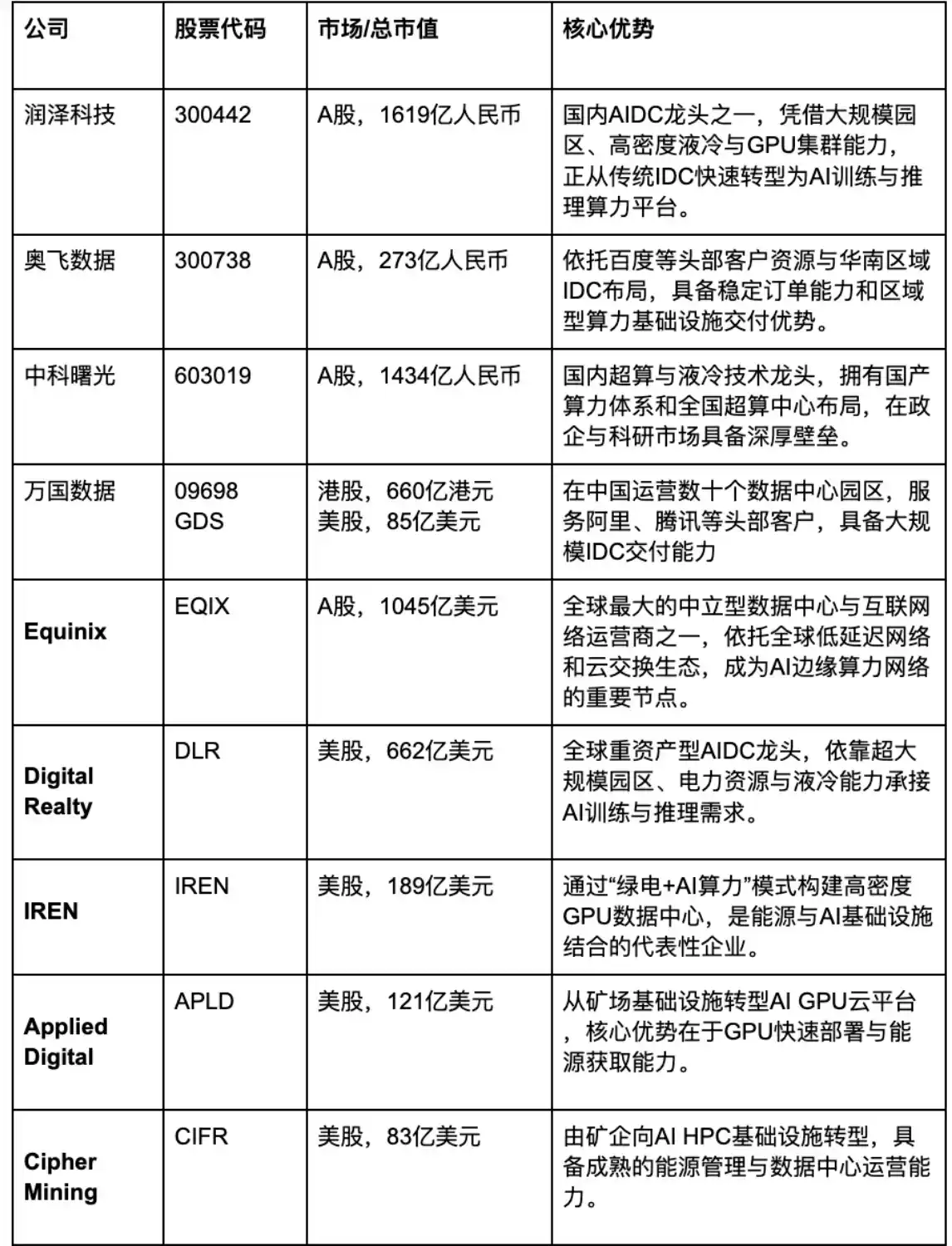

In the US stock market, Equinix is one of the world's leading data center operators, with over 240 data centers in more than 30 countries. Its core advantage is not just the number of facilities but its global interconnectivity and low-latency network resources, making it a crucial infrastructure node for AI compute deployment.

Digital Realty, through its PlatformDIGITAL, enters the AI infrastructure market, serving large cloud service providers and financial institutions.

In the Chinese market, Runtze Technology is one of the most typical AIDC operators listed on the A-share market. Its core business has gradually upgraded from traditional IDC to AI computing centers, with core competencies lying in large-scale facilities, power resources, and AIDC operational capabilities. Companies like OFFLINE Data and Beijing Sinnet Technology Group are expanding in areas such as regional data centers, cloud infrastructure, and AI compute hosting. Sugon leans more towards government, enterprise, and research collaborations in its AIDC business.

Another category of players comes from 'mining farm transformations.' Companies like CoreWeave, IREN, Applied Digital, and Cipher Mining were originally related to cryptocurrency mining. However, with the explosive demand for AI GPUs, they have rapidly pivoted to AI compute infrastructure. IREN promotes a 'Green Power + AI Compute' model, building high-density GPU data centers using renewable energy. Applied Digital and Cipher Mining are also transitioning from traditional mining farms to high-performance AI computing infrastructure.

Furthermore, decentralized, smaller-scale, modular AI Factories are becoming a new trend. Just as the internet era moved from mainframes to cloud computing, AI compute needs to diffuse from super-large central nodes to regional edge nodes.

Therefore, GoodVision AI has chosen a different path: building more lightweight, modular, and rapidly replicable AI Factories. Compared to traditional large-scale AIDCs, GoodVision AI emphasizes regional deployment capability, high-density GPU cluster efficiency, and integrated synergy between energy and compute power.

Its core logic is not to build a single mega data center, but to rapidly deploy AI Factory nodes in high-density population areas globally, typically small-scale inference compute facilities of 2-4MW. This model not only allows for quicker access to local energy resources but is also more suitable for the trend of future AI inference demand spreading to the edge.

If traditional AIDCs resemble the large steel mills of the industrial era, then what GoodVision AI is building is more akin to the 'regionalized Token factories' of the AI era – lighter, more flexible, closer to users, and better suited for the development direction of a future globally distributed inference network.

Third Layer Cake: GPU – The Token Production Equipment

If electricity is the energy, then the GPU is the production equipment. In the initial years of the AI boom, GPUs primarily served training; but in the future, the larger demand will come from inference. Because training belongs to only a few leading companies, while inference will permeate every application, every device, every terminal. Robots need inference, autonomous driving needs inference, AI glasses need inference, and even future collaboration between every AI Agent consumes Tokens in real-time.

NVIDIA remains the absolute core of the global AI chip industry. Its H100, B200, Blackwell, and other GPU products almost define the current global standards for AI training and inference. More importantly, NVIDIA doesn't just sell chips; it has built a complete ecosystem through software and hardware systems like CUDA, TensorRT, DGX, and HGX. Therefore, its competitors must challenge not only GPU performance but the entire AI software ecosystem.

AMD is currently the primary GPU challenger, with core products including the MI300X and other AI GPUs. Compared to NVIDIA, AMD emphasizes an open ecosystem and the ROCm software platform, hoping to attract AI developers and enterprise customers through a more open approach.

Broadcom and Marvell represent another route – ASIC and high-speed interconnects. As AI inference scenarios become increasingly complex, more companies are experimenting with custom ASIC chips to achieve higher energy efficiency and lower costs.

Intel is entering the AI market through server CPUs and Gaudi AI accelerators, hoping to leverage its CPU ecosystem to re-engage in AI infrastructure competition.

In the Chinese market, Cambricon is one of the most representative domestic AI chip companies, primarily promoting its Siyuan series AI chips and building its self-developed AI framework, Neuware. Hygon Information has AMD Zen architecture licensing, focusing on DCU and the AI inference market.

Domestic GPU companies like Moore Threads, Enflame Technology, MetaX, and Biren Technology represent the direction of 'domestic substitution' for Chinese AI chips. They generally emphasize compatibility with the CUDA ecosystem while attempting to build domestic GPU clusters.

From the CUDA ecosystem to HBM memory to Tensor Cores, the core of the entire AI industry is actually continuously improving 'the efficiency of Token generation per unit time.' Simultaneously, GPUs and their underlying infrastructure—servers, optical modules, liquid cooling, switches, etc.—are also closely related to Token production efficiency.

These elements are not as dazzling as companies like NVIDIA, OpenAI, or AI application developers, but they determine whether the entire AI world can truly function. Just as the Industrial Revolution needed not only steam engines but also railways, power grids, and ports. The AI Revolution will not be just a software revolution. It is a global industrial chain upgrade covering energy, chips, networks, cloud computing, and infrastructure.

Vertiv is a global leader in data center UPS and power management, providing data center power supply, cabinet power distribution, and precision air conditioning systems.

Envicool is the A-share market leader in liquid cooling and temperature control systems, with clients including BAT and other large internet companies. As GPU power consumption increases, liquid cooling is becoming a crucial standard feature for AIDCs.

Companies like Hangzhou Zhongheng Electric, Kehua Data, and KSTAR have important positions in UPS, power supply systems, and IDC power provision.

In the network and optical module sector, companies like Zhongji Innolight, Eoptolink Technology, and TFC Optical Communication benefit from the surging demand for high-speed communication within AI clusters.In the server OEM direction, companies like Dell, HPE, Supermicro, Lenovo, and Inspur Information are responsible for the large-scale assembly and delivery of AI servers.

This layer, though not directly facing end-users, determines whether AI infrastructure can truly operate stably. Liquid cooling, UPS, optical modules, switches, energy storage, and server OEMs are becoming the true 'pickaxe sellers' of the AI world, just like the railways, power grids, and ports of the industrial era.

Fourth Layer Cake: LLM – The Token Production Engine

LLMs (Large Language Models) determine how Tokens are understood, generated, and organized. Over the past two years, companies like OpenAI, Anthropic, Google, Meta, xAI, and DeepSeek have ignited a global 'large model competition.' Parameters have scaled from hundreds of billions to trillions, and model capabilities have expanded from text generation to multimodal, reasoning, coding, Agent collaboration, and long-term memory.

However, as the industry develops, the market is beginning to realize: what will truly matter in the future is no longer just 'who has the largest model,' but who can run models continuously at lower costs and higher efficiency. Because the model itself does not directly create value; the real value is created through the inference process of the model being called repeatedly.

This also means that LLMs are evolving from their past role of 'showcasing model capabilities' to becoming the 'Token production engines' in the AI world.

Closed-source and open-source models like OpenAI's, Anthropic's, Google Gemini, and Meta Llama are vying for the future AI ecosystem entry point; while emerging players like DeepSeek are reshaping the competitive landscape through lower costs and higher inference efficiency. Competition in the LLM layer is also gradually shifting away from a pure pursuit of parameter count, with evaluation criteria increasingly turning to comparisons across multiple dimensions:

Token Cost

Inference Efficiency

Context Capability

Multi-Agent Collaboration

Long-Term Memory

Model & Infrastructure Synergy Capability

Because what truly matters in the AI era is not just how 'smart' a large model is, but whether the model can be operated continuously, at scale, and at low cost globally. GoodVision AI also has its optimization approach at this layer: by collaborating with large model vendors, deploying large models within its AI Factory facilities, transitioning from traditional compute rental business to directly providing Token services; this not only improves business gross margin but also offers a more user-friendly experience.

Fifth Layer Cake: Token Distribution – The 'Power Grid' of the AI Era

After AIDCs are built, the next question arises: How is this compute power used by the world?

Thus, compute rental platforms have emerged. They function like the 'power grid system' of the AI era, splitting up and distributing originally centralized GPU resources, then renting them on-demand to developers, enterprises, and AI applications.

AWS, Azure, Google Cloud, Alibaba Cloud, and Tencent Cloud remain the most powerful players in this layer. They possess the world's largest cloud computing infrastructure and are gradually integrating AI GPU resources into their IaaS systems.

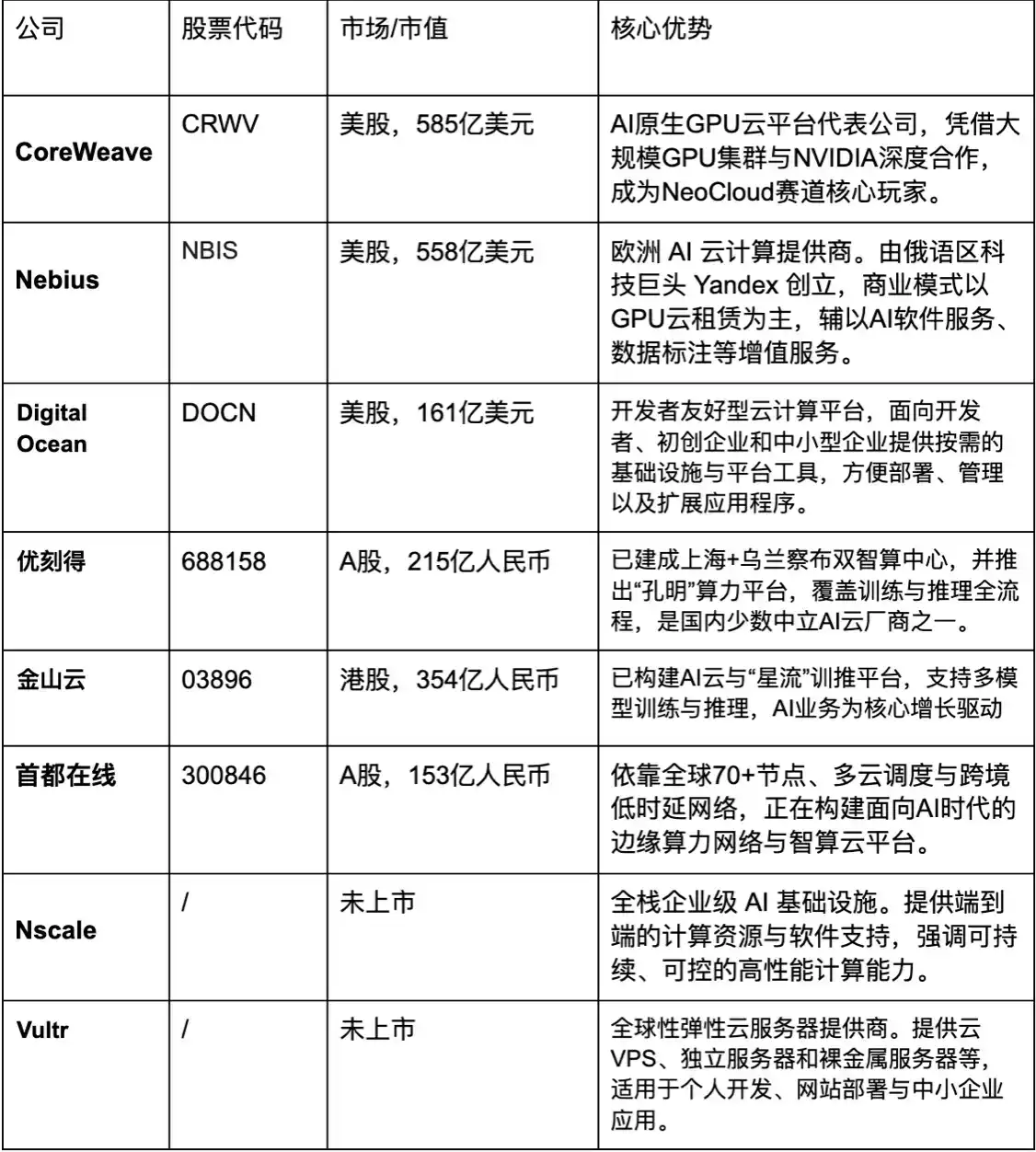

However, simultaneously, a batch of 'AI-native clouds' are rapidly rising. Companies like CoreWeave, Nebius, and Nscale build GPU cloud platforms specifically around AI training and inference needs. Compared to traditional cloud providers, they are more flexible, more focused on AI tasks, and more skilled at GPU cluster optimization.

CoreWeave is one of the most representative companies in the current NeoCloud scene. It initially focused on Ethereum mining, then pivoted entirely to AI GPU cloud services, and is now a key AI infrastructure company supported by NVIDIA.

Lightweight cloud platforms like DigitalOcean and Vultr target small-to-medium developers and startups, emphasizing rapid deployment and low-cost GPU services.

In the Chinese market, apart from the giants, companies like UCloud, Kingsoft Cloud, and Beijing Sinnet Technology Group are major suppliers in the GPU cloud and AI compute rental market. The competitive landscape in this layer is very similar to the early power grid era: how to efficiently distribute decentralized compute power.

Sixth Layer Cake: Token Optimization & Intelligent Scheduling – The Brain of the AI Era

This is perhaps the most underestimated yet most critical 'cake' layer. With the explosion in AI Agent usage, it became apparent that not all tasks warrant calling the most expensive large model. Many simple tasks can be handled by local models; many real-time tasks are better suited for edge inference; many privacy-sensitive tasks cannot even be uploaded to the cloud. After the question of 'Is there compute power?' comes another: 'How to use compute power more intelligently?'

As Token demand grows exponentially, 'Having the right model, on the right compute, handle the right task.' is key to ensuring Tokens are used rationally and efficiently. This is precisely one of the directions GoodVision AI is pursuing besides building AI Token factories.

It's like today's power system: some demand comes from the large grid; some comes from rooftop solar. What's truly important is the intermediate 'intelligent scheduling system.'

The future of AI will follow a similar structure: simple tasks handled by local small models, complex tasks calling cloud-based large models, high-privacy tasks processed at the edge, and high-concurrency tasks dynamically scheduled through hybrid clouds.

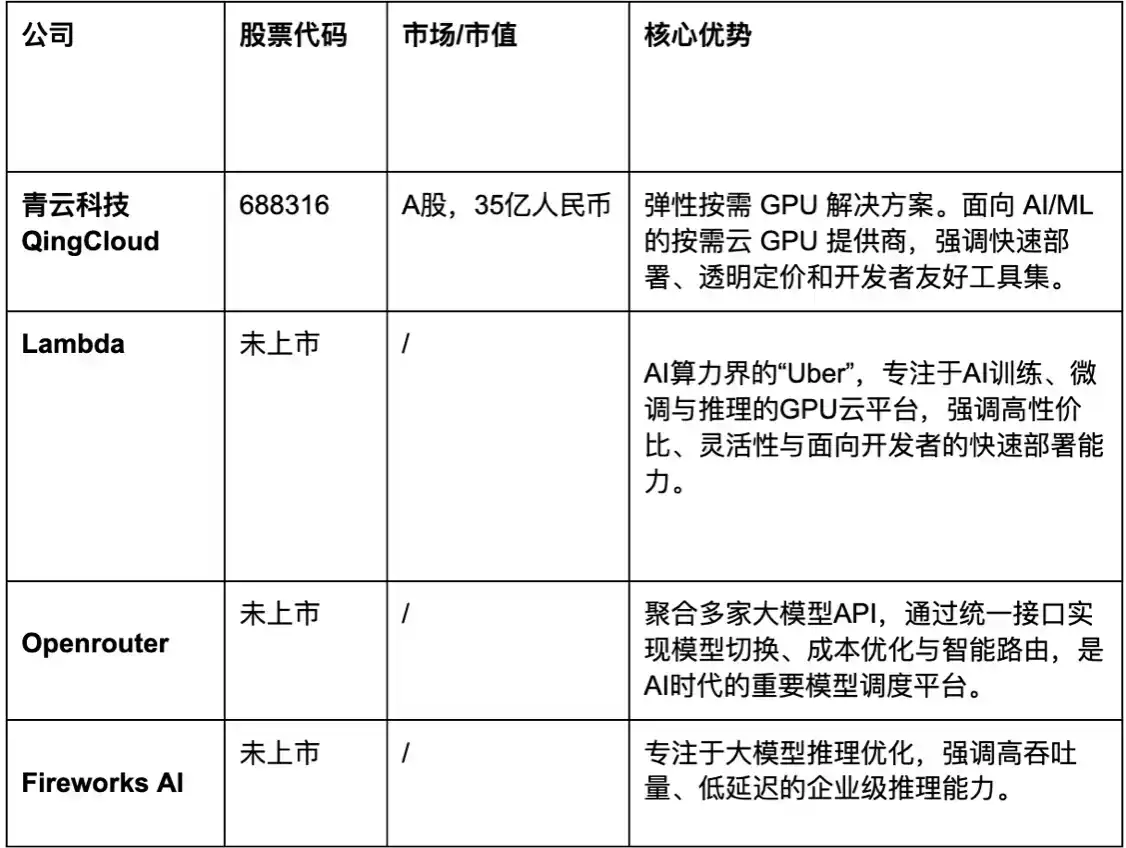

Besides GoodVision AI, companies like QingCloud Technology, Lambda, OpenRouter, and Fireworks AI are also leaders in Token optimization and intelligent scheduling.

This 'cake' layer overlaps significantly with the previous two layers—AIDC and Compute Rental. As GPU resources, regional nodes, and inference task scales continue to expand, merely 'owning compute' is no longer sufficient to build long-term barriers. More and more AIDC operators and GPU cloud platforms are realizing that what will truly determine efficiency and profit margins in the future is not just the number of GPUs, but how to dynamically schedule models, compute power, and Token traffic.

Therefore, many platforms originally focused on AIDC and GPU cloud are also extending into the 'intelligent scheduling layer.' For example, in the Chinese market, companies like UCloud, Beijing Sinnet Technology Group, and Sugon are attempting to integrate their own GPU cloud facilities, multi-cloud resources, and inference scheduling capabilities, gradually shifting from 'selling compute' to 'optimizing compute.'

Seventh Layer Cake: Models & Agents – The Token Consumers

This layer is closest to users and最容易获得流量(easiest to gain traffic), but the competition is also the fiercest. At GTC 2026, Jensen Huang proposed this view: In the future, every company will become a 'Token producer and Token consumer.'

An AI Agent might simultaneously call multiple models, multiple tools, multiple APIs, and continuously perform reasoning, planning, and execution. This means the volume of Tokens consumed by future AI will far exceed the scale of human-AI conversations today. Some current heavy AI users, building systems with multi-agent concurrency and inter-calls, can easily consume 1 billion Tokens per day.

The future is not 1 billion people using AI, but 10 billion, or even 100 billion AI Agents working simultaneously, calling each other. And the real bottleneck will shift from 'model capability' to 'Token scheduling efficiency.'

The tech giants naturally go without saying. Microsoft, Google, Meta, Amazon, etc., are gradually embedding AI capabilities into all their products through office systems, search, social networks, and cloud services.

Enterprise software companies like Adobe, Salesforce, ServiceNow, and Palantir are rapidly advancing in enterprise-grade AI Agents and automated workflow directions. Meanwhile, Hugging Face is becoming the 'GitHub' of the AI era. It's not just a model community but a crucial piece of infrastructure for the global AI development ecosystem.

In the Chinese market, companies like iFLYTEK, Kunlun Tech, 360 Security, Kingsoft Office, and SenseTime are making layouts around AI assistants, AI office tools, and AI Agents.

When the 'Seven-Layer Cake' Truly Takes Shape, the AI World Will Truly Begin

Today's AI industry actually still operates within an infrastructure system that is not yet fully mature.

Some possess the most advanced GPUs but are constrained by energy; some have built massive AIDCs but lack efficient scheduling; some develop powerful models and Agents but face high inference costs and latency; some control edge nodes but cannot form a unified, collaborative network.

From electricity, AIDC, GPU to LLM, Token distribution, intelligent scheduling, and AI Agent, although the entire AI industrial chain is developing rapidly, significant fragmentation, redundancy, and efficiency bottlenecks still exist between layers.

Only when this 'seven-layer cake' is fully constructed and begins to operate efficiently and synergistically will the AI industry transition from today's 'Tool Era' to the true 'Mass Adoption Era' belonging to the intelligent world.

The future AI world will no longer be just about a few tech giants training large models, but about tens of billions of AI Agents being continuously online, collaborating, and calling compute and Tokens. Every conversation, every inference, every tool call, every automated task execution corresponds to the coordinated operation of energy, GPUs, networks, scheduling systems, and inference nodes.

This also means the AI industry is evolving from its past 'software logic' into a super industrial system covering energy, chips, cloud computing, edge networks, and intelligent scheduling.

Just as the Industrial Revolution needed not only steam engines but also railways, power grids, and ports; just as the Internet Revolution needed not only PCs but also fiber optics, data centers, and cloud computing. The true hallmark of the AI Revolution's maturity will not be just one killer application, but the formation, on a global scale, of an 'intelligent infrastructure network' capable of continuously producing, distributing, scheduling, and consuming Tokens.

And when these seven layers of infrastructure are finally truly connected, the competitive logic of the AI industry will be completely restructured. The most important companies of the future might no longer be those with the largest models, but those capable of connecting energy, compute, networks, models, and Token flow.