Author: momo, ChainCatcher

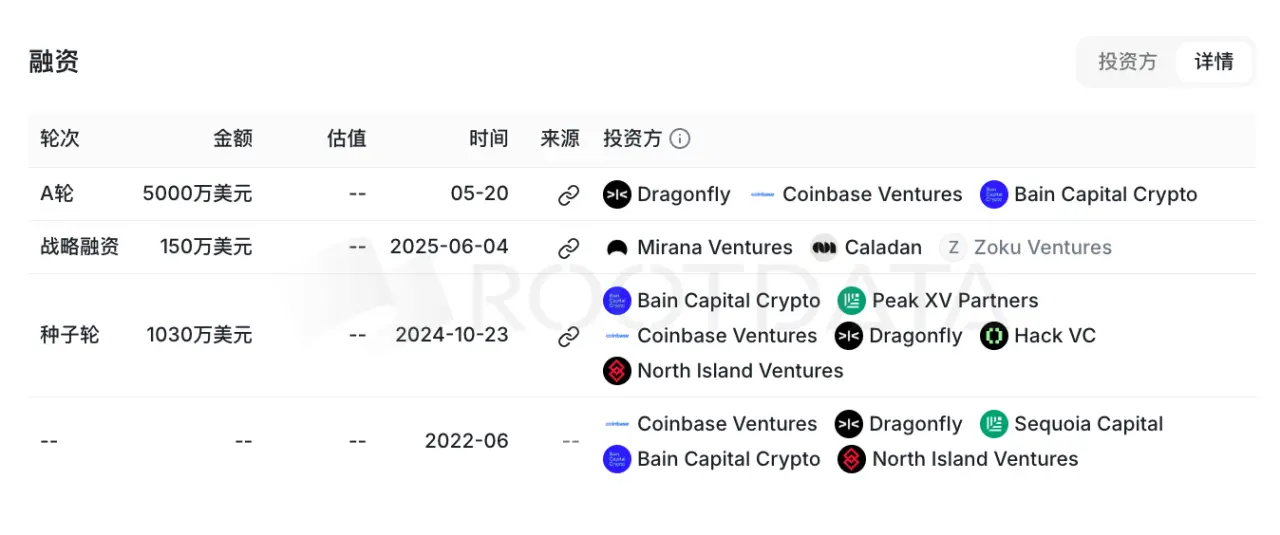

Recently, the decentralized derivatives trading platform Variational announced the completion of a $50 million Series A financing round led by Dragonfly. Combined with three previous funding rounds, Variational has raised a cumulative total of $61.8 million. Its investor lineup is quite impressive, including not only Dragonfly but also renowned institutions such as Sequoia Capital, Coinbase Ventures, Bain Capital Crypto, Hack VC, and others.

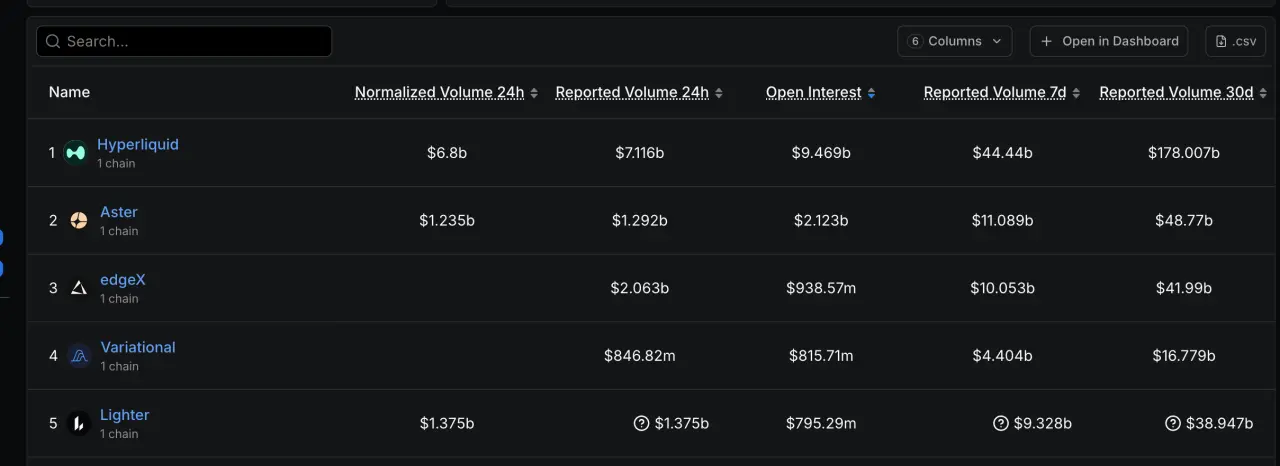

According to DeFiLlama data, the open interest (OI) on Variational has exceeded $810 million. While there remains a significant gap compared to Hyperliquid's $9.4 billion, its OI currently ranks fourth among on-chain derivatives protocols.

In the fiercely competitive decentralized derivatives sector, why has Variational continued to secure backing from top-tier institutions? What is the team's background? What are its differentiated approaches? This article provides a brief overview.

What is the team's background?

In terms of team background and entrepreneurial experience, Variational and Hyperliquid share several similarities: both teams graduated from prestigious universities, come from quantitative trading backgrounds, founded quantitative funds, and subsequently transitioned to building on-chain derivatives platforms.

However, unlike Hyperliquid's early mystique and anonymous team approach, Variational discloses its founding team's background and entrepreneurial journey in its whitepaper.

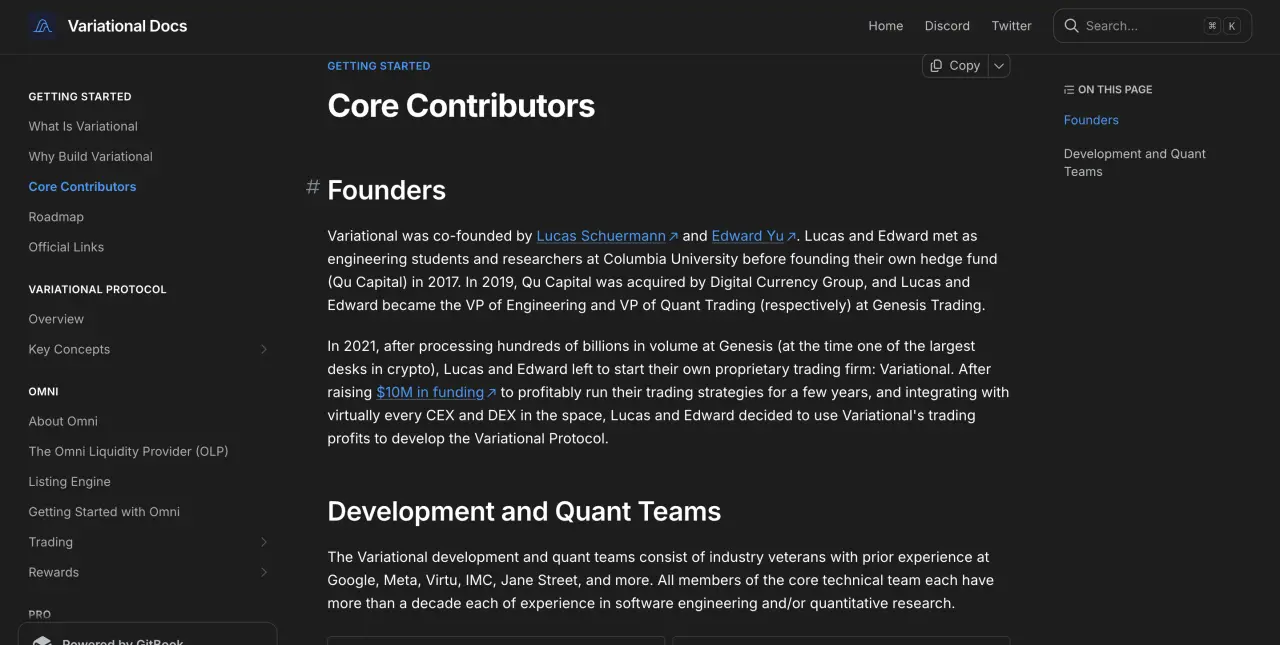

Variational was co-founded by Lucas Schuermann and Edward Yu. CEO Lucas graduated from Columbia University and was previously responsible for trading systems engineering architecture; Edward Yu has a Chinese background and was originally a quantitative analyst. The two met while studying and conducting research in the engineering department at Columbia University and co-founded the quantitative hedge fund Qu Capital in 2017.

In 2019, Qu Capital was acquired by Digital Currency Group. Subsequently, both joined Genesis Trading: Lucas served as Vice President of Engineering, and Edward Yu served as Vice President of Quantitative Trading.

According to the whitepaper, before leaving Genesis in 2021, their team had processed trading volumes in the hundreds of billions of dollars. After leaving, they founded their proprietary trading firm, Variational, and secured $10 million in funding.

In the following years, the team operated proprietary trading strategies while integrating with mainstream CEX and DEX trading interfaces. Later, based on their own trading business and system experience, they began developing and operating the Variational Protocol.

Additionally, Variational's development and quantitative team members also hail from technology and quantitative institutions such as Google, Meta, Virtu Financial, IMC Trading, and Jane Street. The whitepaper states that core technical team members generally possess over a decade of experience in software engineering or quantitative research.

What are its product features? How does it differ from Hyperliquid?

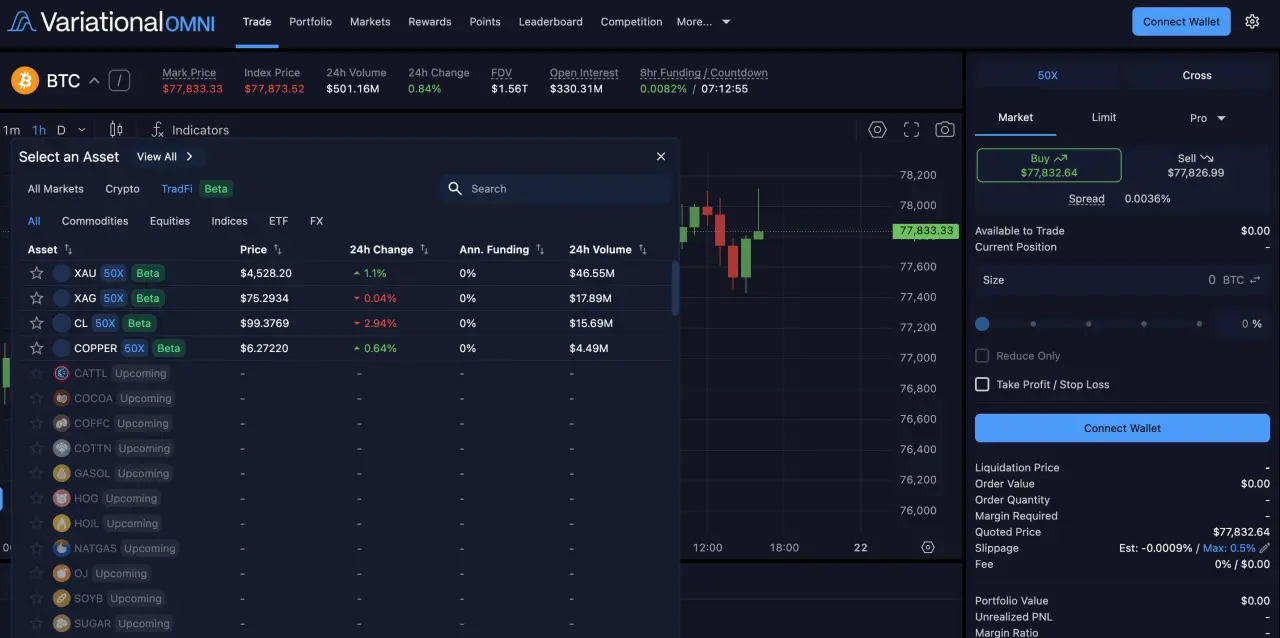

Judging from the trading interface, there isn't a significant difference between Variational and Hyperliquid. The platform currently lists approximately 450 trading pairs, mainly covering cryptocurrency and TradFi assets, offering users leverage up to 50x. The TradFi section is currently in Beta testing. According to official disclosures, the TradFi market will list over 100 trading pairs.

However, in its press release, Variational emphasizes a distinctly different positioning from Hyperliquid.

Variational describes its model as more akin to a brokerage rather than another exchange in the style of Hyperliquid. Its target users are not limited to crypto-native traders; it aims to make the on-chain derivatives trading experience closer to traditional markets through zero-fee trading and liquidity aggregation.

Currently operating on Arbitrum, Variational employs a dual-product-line model. The Omni version primarily targets retail users, positioned as a perpetual contracts trading product aggregating liquidity from multiple sources, while the Pro version caters to institutional over-the-counter derivatives trading.

The most significant difference from Hyperliquid lies in order matching and liquidity mechanisms. Hyperliquid relies on its self-built L1 chain and a public central limit order book (CLOB), with market makers or the HLP treasury within the protocol competing to provide quotes, and traders paying maker/taker fees. In contrast, Variational uses an RFQ (Request for Quote) model, with a single liquidity provider as the counterparty. It does not rely on on-chain internal market making but instead aggregates external liquidity in real-time from sources like CEXs, DEXs, OTC channels, and traditional financial market makers, managing risk through hedging.

The rationale for choosing this differentiated path, according to Variational CEO Lucas, is that on-chain liquidity still lags far behind traditional trading venues like the CME, and order book models face a "cold start" problem. Aggregating liquidity from external sources avoids the need to rebuild liquidity from scratch on-chain.

What is the current stage? What participation opportunities are available?

Variational is currently still in the Pre-TGE stage; the $VAR token has not been issued. The project initially planned a TGE in Q1 2025, which has since been postponed. No new definitive TGE date has been officially announced.

In December 2025, Variational launched the Omni Points points system. The official statement indicates that 50% of the $VAR supply will be allocated for community incentives, distributed gradually through mechanisms like Points rather than a one-time airdrop.

Regarding points, 3 million points have been retroactively distributed to early users. Subsequently, points are distributed every Friday based on the previous week's trading snapshot. The points program is scheduled to conclude by Q3 2026 at the latest.

The main current participation opportunity is to engage in perpetual contracts trading on the Omni platform. Trading volume is the core factor for earning points, with additional point bonuses available for holding positions over time and referring others.