Original | Odaily Planet Daily (@OdailyChina)

Author | Golem (@web3_golem)

On April 6, Polymarket announced a major upgrade to the platform in the next 2 to 3 weeks, including upgrading both CTF and CLOB to V2, and replacing the platform collateral from USDC.e to the native stablecoin Polymarket USD.

According to the official introduction, Polymarket USD is 1:1 backed by USDC. For most users, the transition from USDC.e to Polymarket USD is seamless, with the frontend handling it automatically—users only need to confirm once. For advanced users and API-only traders, the transition process might be a bit more complex but still not difficult; they need to wrap their USDC or USDC.e into Polymarket USD through the wrap() function of the collateral access contract.

On the surface, it seems like Polymarket is just changing the trading collateral in the backend. As the platform grows, continuing to use USDC.e is indeed a potential risk. Back in February, Circle and Polymarket had already announced plans to migrate from bridged USDC.e to native USDC, and this is just a normal progression of that cooperation.

However, Polymarket did not choose to directly introduce native USDC to replace USDC.e; instead, it added an extra layer, aiming to pool USDC into its own fund pool. This layer is called Polymarket USD. Therefore, the emergence of Polymarket USD is definitely a "One more thing"(Odaily Note: "One more thing" is a classic tradition of Apple keynotes, now symbolizing a company's finale, industry-disrupting moves, etc.).

Polymarket Gains the Right to Mint Currency

The first layer of significance is that Polymarket can pool user funds.

Previously, the money users deposited into Polymarket would be converted into USDC.e. You can think of it as Polymarket being a huge trading venue—it only handles matching, pricing, and清算; the money flows through it, but the money itself does not belong to its system. Polymarket is not a treasury.

But that's about to change. When USDC.e is replaced with Polymarket USD, Polymarket can reach out to that money which was merely "passing through." As Polymarket officially stated, the daily user experience is unaffected, but the actual on-chain settlement path behind the scenes has been altered. This transformation is no less significant than an exchange transitioning from relying on third-party清算机构 to building its own清算 center.

Polymarket USD is 1:1 backed by USDC, meaning that in the future, for every Polymarket USD in the market, there will be a corresponding USDC in Polymarket's fund pool. Currently, every Yes/No share pair on Polymarket is backed by USDC.e. When players place bets or settle, USDC.e also moves on-chain. But after switching to Polymarket USD, although it will also flow on-chain with user operations, the USDC in Polymarket's fund pool won't move accordingly. Therefore, as long as users don't come to redeem, this money is essentially Polymarket's.

Polymarket has transformed from a use case for stablecoins to an entity that holds the on-chain minting right. Polymarket USD diverts user assets from the "open sea" to Polymarket's "internal lake." Once funds begin to pool, Polymarket is no longer just a prediction trading platform, and its business model no longer relies solely on trading fees, because it can start playing the oldest "money makes money" game in the financial markets.

Increasing Polymarket's Revenue Channels

The second layer of significance is the expansion of Polymarket's business.

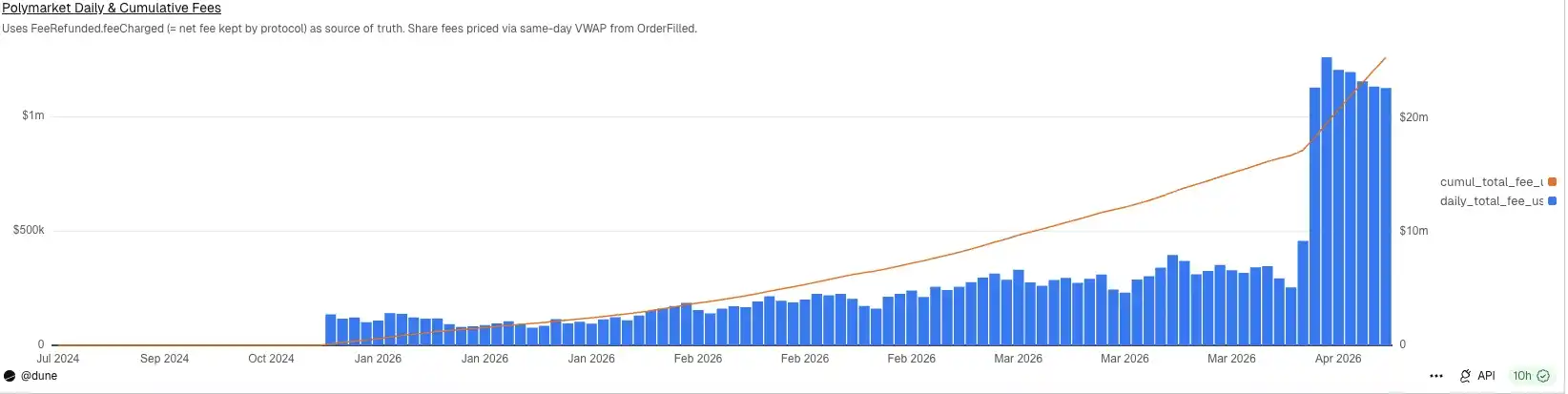

The current business model of prediction markets is simple: charging transaction fees. After Polymarket adjusted its fee mechanism on March 30(Odaily Note: Expanding the taker fee scope to include Finance, Politics, Economics, Culture, Weather, and other market categories, in addition to the original Crypto and Sports categories), its daily fee income has exceeded $1 million.

Polymarket's Daily Fee Income

Although impressive, it's not enough to satisfy Polymarket's ambitions. Prediction markets are currently the most sought-after赛道, but the business model ceiling isn't very high, the project's moat is relatively单一 (regulatory approval), and user stickiness isn't exceptionally strong. In the current landscape where everyone is doing prediction markets, how can Polymarket ensure it won't be surpassed by competitors in the future?

The answer it gives now is: I don't just match trades; I can also put players' money to work.

From a business essence perspective, the most attractive aspect of stablecoins over the years has never been fast payments and transfers, but the低调 yet highly profitable money-printing machine behind them—reserve asset yield. In 2025, the vast majority of Circle's income still came from reserve income. Polymarket understood this model, hence it launched Polymarket USD.

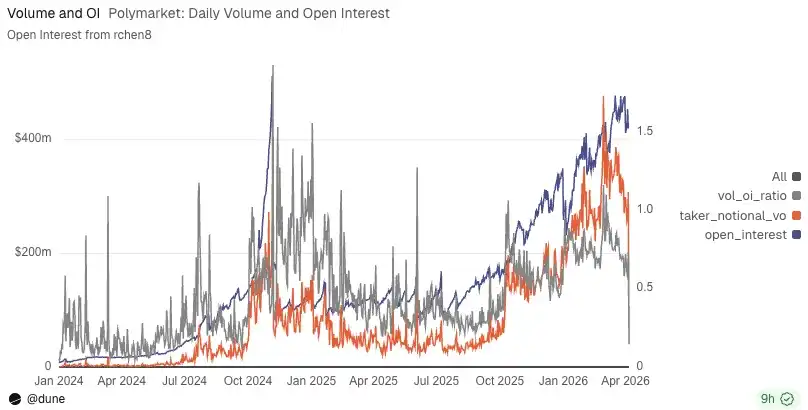

According to Dune data, the value of open interest on the Polymarket platform has exceeded $400 million. If all this money is converted into Polymarket USD, Polymarket simply needs to deposit the underlying collateral USDC into Circle's institutional account or place it in a U.S. Treasury protocol. At a risk-free rate of 4%-5%, it could earn tens of millions of dollars in "interest tax" annually just by sitting back.

Defillama founder 0xngmi even directly stated that Polymarket user wallets hold approximately $1.25 billion. If they keep this interest income, at current rates, they would gain an additional $54 million in annual revenue. Polymarket could even participate in DeFi wealth management with higher APYs, turning the idle funds on the prediction platform into active leverage and returning the到期收益 to users, effectively providing a hedge for users.

Polymarket's Daily OI and Trading Volume Curve

Prediction markets naturally have two characteristics: fund滞留 and high-frequency reallocation driven by events. Users' money doesn't truly enter and exit instantly like in a casino; it's either already in positions or sitting in accounts waiting for the next event, the next odds change. This type of money is most suitable for financial reprocessing, and for users, there's also a beautiful excuse: improving capital efficiency.

Of course, Polymarket hasn't publicly stated yet that it will definitely engage in yield extraction or on-chain wealth management after launching the stablecoin. But this path is almost a natural next step. As long as the scale of Polymarket USD grows larger in the future, it naturally gains the space to manage yields, expand collateral, and create financial combinations within the platform.

Some time ago, the《CLARITY Act》faced resistance for potentially prohibiting crypto companies from offering interest on stablecoins to users. If the outcome of the dispute remains a prohibition, all the above演绎 of Polymarket USD's potential would come to naught. But on April 6, according to U.S. media reports, the core disagreement between the U.S. crypto industry and banking over stablecoin yield mechanisms may be nearing resolution. Although details have not been disclosed, overall expectations are optimistic, and the《CLARITY Act》may enter the deliberation stage in committee in late April.

So, don't think Polymarket is far from this.

Polymarket Gains USDC Distribution Rights

The launch of the stablecoin by Polymarket has a third layer of significance: gaining USDC distribution rights.

As of today, Polymarket is still a major distribution scenario within the USDC ecosystem. Circle provides native USDC, Polymarket distributes USDC, and both sides are harmonious. Polymarket is currently experiencing strong growth momentum. Undoubtedly, the amount of USDC reserves沉淀 within its platform will grow larger in the future, potentially even becoming a distribution channel as important as Coinbase. When that time truly comes, the relationship between Polymarket and Circle might also change.

A reality in the stablecoin world is that distribution rights are as important as issuance rights, which is why Coinbase can take away over half of Circle's reserve income. Therefore, in the future, when Polymarket becomes a significant distributor of USDC, it will inevitably also gain bargaining power and be entitled to a large share of the reserve income. Furthermore, when Polymarket USD matures sufficiently, it could even explore multi-collateral backed stablecoins, not just relying solely on USDC.

This is also why I believe Polymarket USD is not an ordinary upgrade for Polymarket, but an identity update. Polymarket will evolve from "a platform collecting fees based on event volatility" to one that also兼具 "a platform organizing and清算 around the dollar".

The former is casino logic, while the latter is bank logic.

Polymarket's moat has thus gained another layer. It still maintains the beautiful narrative of information as the market and pricing facts early. But in terms of its business model, it is quietly moving itself to a more important position—no longer satisfied with being surface-level market traffic, no longer satisfied with仅仅 attracting users with odds, and no longer satisfied with continuing to cede the fattest part of the industry chain (asset reserve income) to others.