Author: Castle Labs

Compiled by: Felix, PANews

Editor's Note: As cryptocurrencies are gradually accepted by the traditional sector, it seems to reveal a glimpse of the crypto era's development. Research institution Castle Labs writes that from the speculative era of "one-click token issuance" to the investment era of "revenue is king, institutions on-chain," 2026 may be a watershed moment for cryptocurrency development. Tokens that cannot generate real revenue will be eliminated, and a few high-quality protocols will dominate the future.

The beginning of 2026 was not smooth for cryptocurrencies. Most asset prices fell; Bitcoin hit an all-time high six months ago and has been in a sustained retracement since then. Recently, there has been a lack of positive news, continuous outflows from ETFs, declining interest in cryptocurrencies, corporate failures, and venture capital no longer actively investing. The once abundant "wellspring" of opportunities in cryptocurrency seems to be drying up.

Although these are all facts, and there are no positive factors to speak of, we are heading towards a major shift: the value of tokens that have no connection to protocol revenue will plummet, and those without revenue will not survive. The crypto space is transitioning from "speculation" to "investment."

The event that accelerated this shift was the liquidation event in October, followed by a series of macro events, such as gold outperforming Bitcoin, leading people to ask: Does cryptocurrency still have investment value? Does it still possess the upside potential that initially attracted so many investors?

This article focuses on this transition and its impact on crypto assets and the underlying investment models.

From Speculation to Investment

Cryptocurrency has gone through multiple development stages, including the initial exploration period (when it was considered geek technology with no known application scenarios); extreme speculation during the ICO boom; regulatory neglect; massive blow-ups like the Luna crash and FTX; and the current new era where institutions are beginning to get involved.

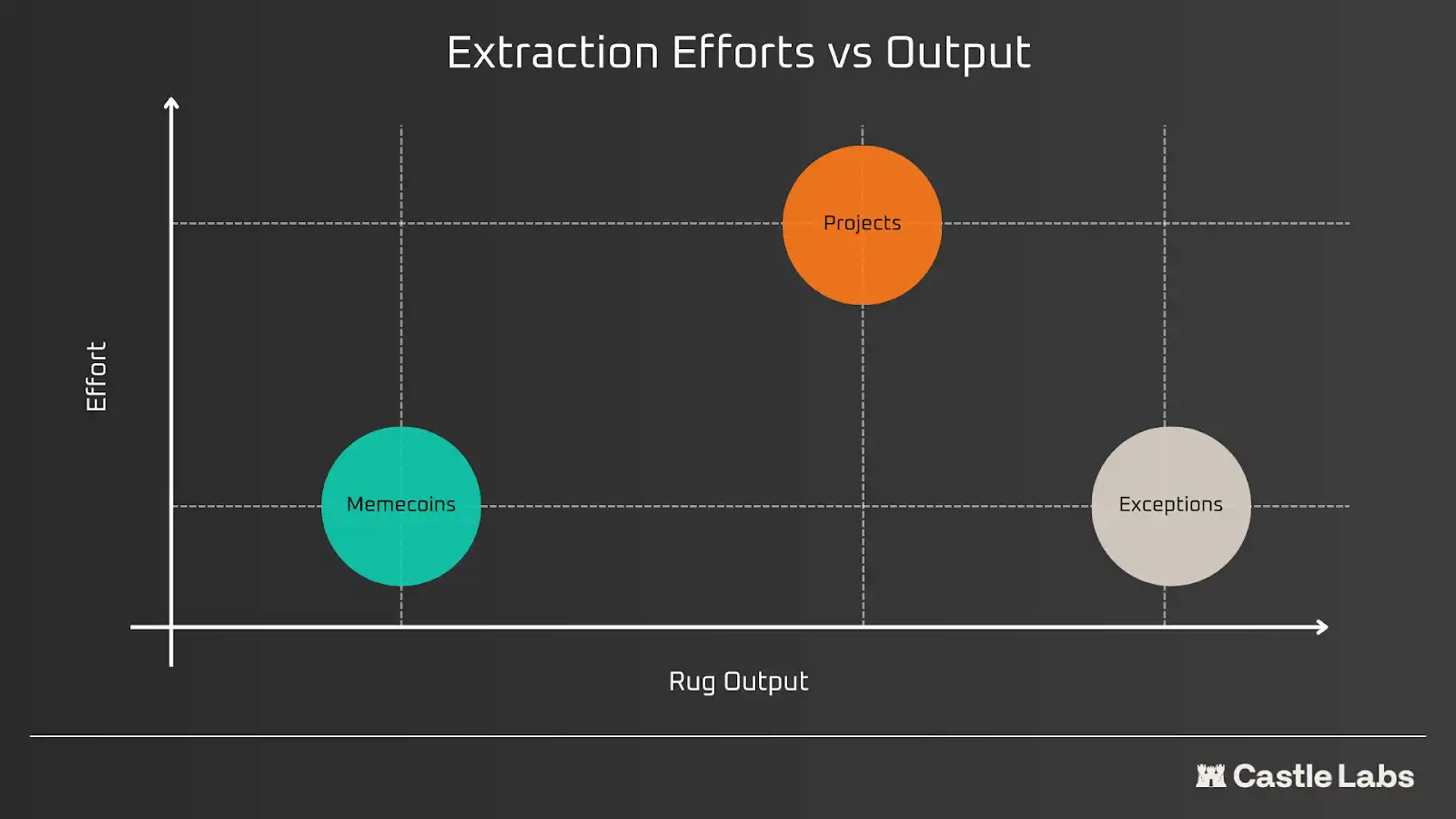

For a long time, the crypto industry has adhered to a "yield-first" model, establishing a norm of speculation rather than investment. The popularity of products like pump.fun, which allows users to launch meme coins with one click, confirms that cryptocurrency has always been a speculative bubble, with new users flooding in merely渴望暴富 (craving to get rich quick). The "yield-first" nature of cryptocurrency can be divided into three categories:

- Low input, low output (Meme coins)

- High input, high output (Scam projects and slow arbitrage projects)

- Low input, high output (Celebrity coins)

On one hand, there are some simple arbitrage methods in the market that have worked well so far and will likely continue to work, albeit potentially at a slower pace: meme coins. Meme coins are easy to issue; there's no need to explain the purpose or utility to anyone because the key to arbitrage and making money lies in one principle: exit the trade before others. Everyone trading meme coins understands this, and in some cases, they lose money by their own fault, as this is how the market operates. On the other hand, there are projects that over-promise, hype excessively, and eventually exit quietly. Of course, there are exceptions that require little input but yield high returns, such as celebrity coins.

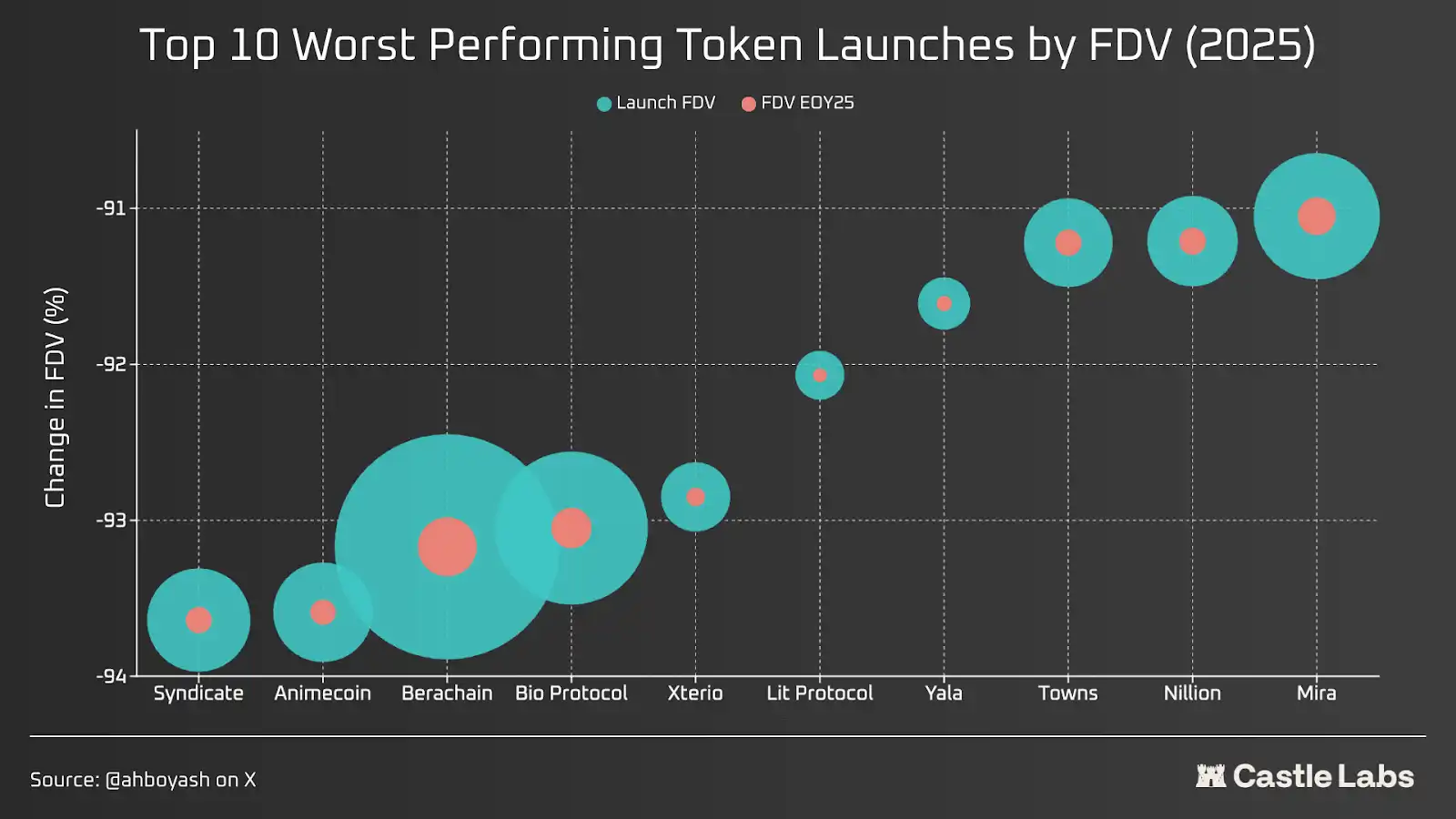

Take last year's Token Generation Events (TGEs) as an example; most could be classified as bad investments because they left token holders with significant losses by year-end. The reasons for the decline could be poor tokenomics, issuance during a valuation bubble (the main reason), market and project sentiment, etc.

For a long time, crypto projects focused on building the best technology but never committed to achieving Product-Market Fit (PMF), which is why we have technology that no one uses. But by 2026, things seem to be changing. As institutions move on-chain, the crypto "yield-first" model seems to be waning. They want to use the infrastructure the crypto industry has built over the years, but their arrival comes with a huge caveat: they don't want to have anything to do with any of the tokens we generated in the process of building the technology; they like the code and infrastructure and will use it, but this does not positively impact the vast majority of tokens.

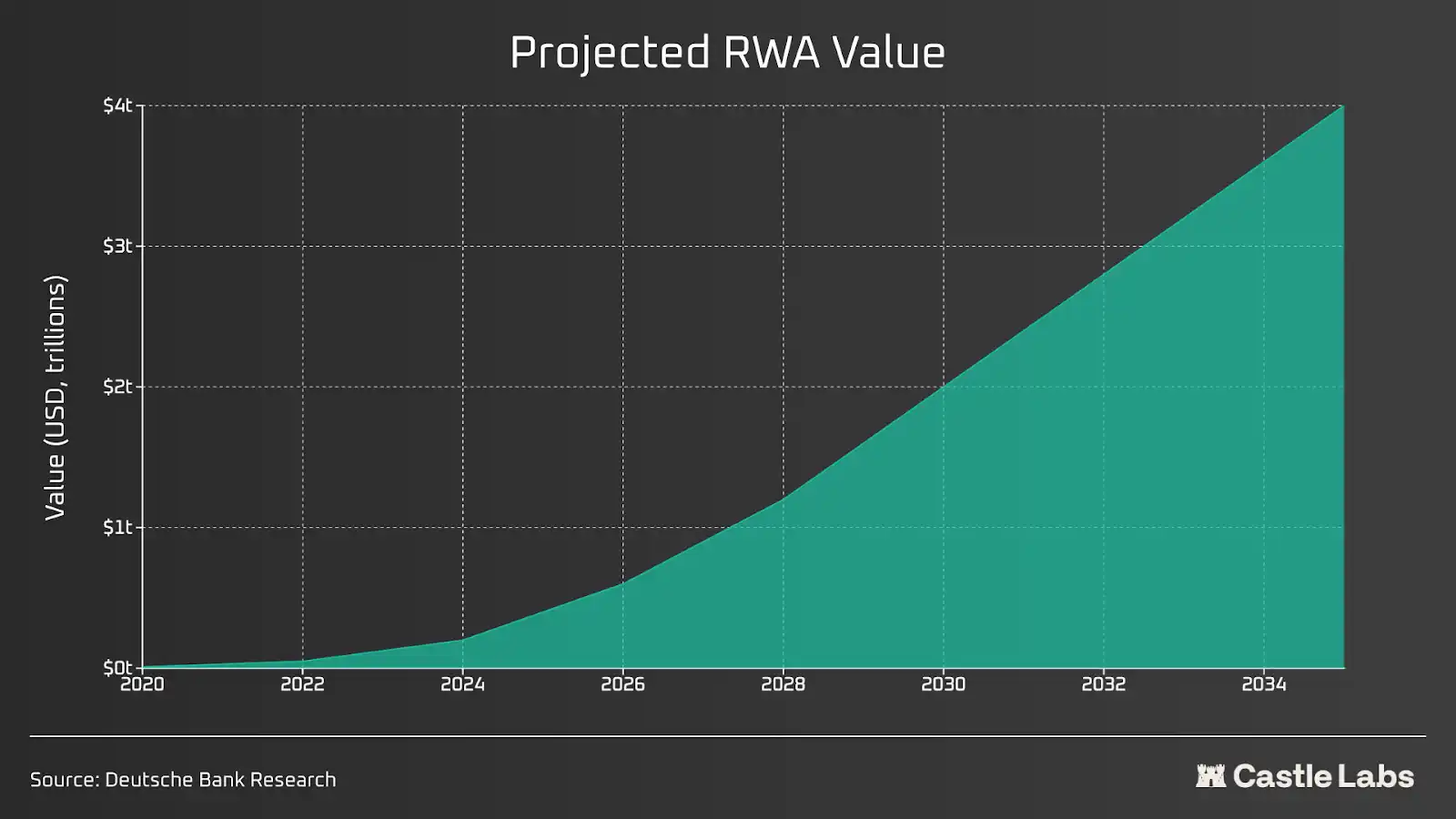

Not long ago, the New York Stock Exchange (NYSE) stated it would leverage blockchain infrastructure to support 24/7 trading. Robinhood has begun testing on an L2 built on Arbitrum Stack to tokenize stocks and ETFs, allowing users to hold "stocks" in self-custody wallets. BlackRock's BUIDL and Franklin Templeton's Benji are excellent RWA products. All of these enable instant settlement: a problem TradFi has faced for years due to trading hour limitations.

As for RWA, it is expected to reach the trillion-dollar level in the coming years. Private credit, public offerings, and short-term US tokenized debt are growing on-chain; one can trade commodities and stocks with leverage on platforms like Hyperliquid and Ostium, and these numbers are constantly climbing.

Everyone is moving on-chain because blockchain can push finance to new heights. The dream of full DeFi adoption is becoming a reality because institutions and every retail user are using the same chain, enabling transparency, faster settlement, zero latency, and greater control over funds.

In this new era, applications that have laid a solid foundation will still thrive. Incumbent leaders in the lending space like Morpho and Aave will continue to dominate because they have withstood the test of the most severe drawdowns, performed well, and continued to innovate. Furthermore, protocols like Hyperliquid are becoming some of the deepest sources of on-chain liquidity, supporting leveraged trading of public stocks and commodities. As institutions expand, they need trading venues that can accommodate their size.

Oracle networks, cross-chain interoperability stacks, L2/L1 scaling, and token standards are what truly matter. Clearly, when institutions go all-in on-chain, no asset is guaranteed to deliver the best returns, but those with a good track record will certainly not be eliminated and will be widely used by both institutional and retail investors.

Revenue is King

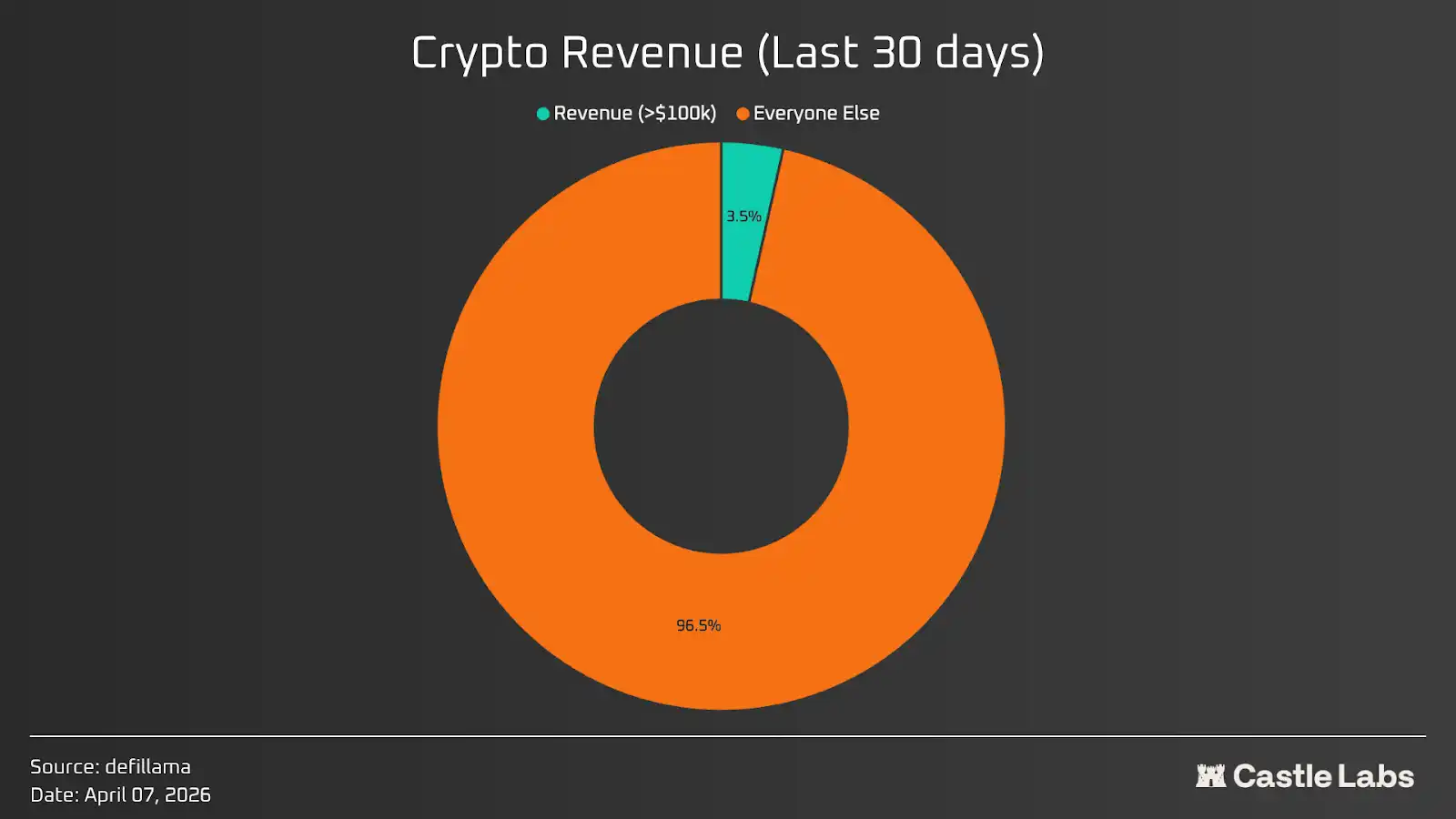

There are over 17,000 tokens listed on Coingecko.

DeFillama lists about 5,700 protocols; if we include protocols with revenue exceeding $100,000 in the past 30 days, there are only about 200 protocols or products, accounting for 3.5%. The pool of investable cryptocurrencies is smaller than anyone expected. Most tokens are not investment-grade.

If we analyze this data more practically, considering holder yield, which is the revenue returned to holders in any form. Surprisingly, only about 50 protocols had holder yields exceeding $100,000 in the past 30 days, which is less than 1% of the total protocols listed on Defillama.

Perhaps the benchmark should be raised to $1 million per month, as most tokens trade volumes in the hundreds of millions or even billions of dollars.

Delving into the issue of low token holder revenue, it stems from the long-standing issue of misaligned incentives in the crypto industry and flawed token structures. A project typically always involves two entities: the Labs and the DAO / token holders. The Labs are the "team" in the tokenomics; they are the initial developers of the project, raising funds by selling part of the company's equity and issuing tokens to investors in the early stages in exchange for capital to develop the business. Unlike equity, tokens are not a legal representation of the business and do not provide any actual rights to the company's profits. Investors holding equity shares have these rights through their holdings. But when it comes to aligning the interests of the product with the token, token holders are usually at the mercy of the project.

But over the past year, things have started to change, with people reducing their investment in speculative projects and paying more attention to the actual profitability of protocols. This shift will take cryptocurrency to heights that the "yield-first" model could not reach for years.

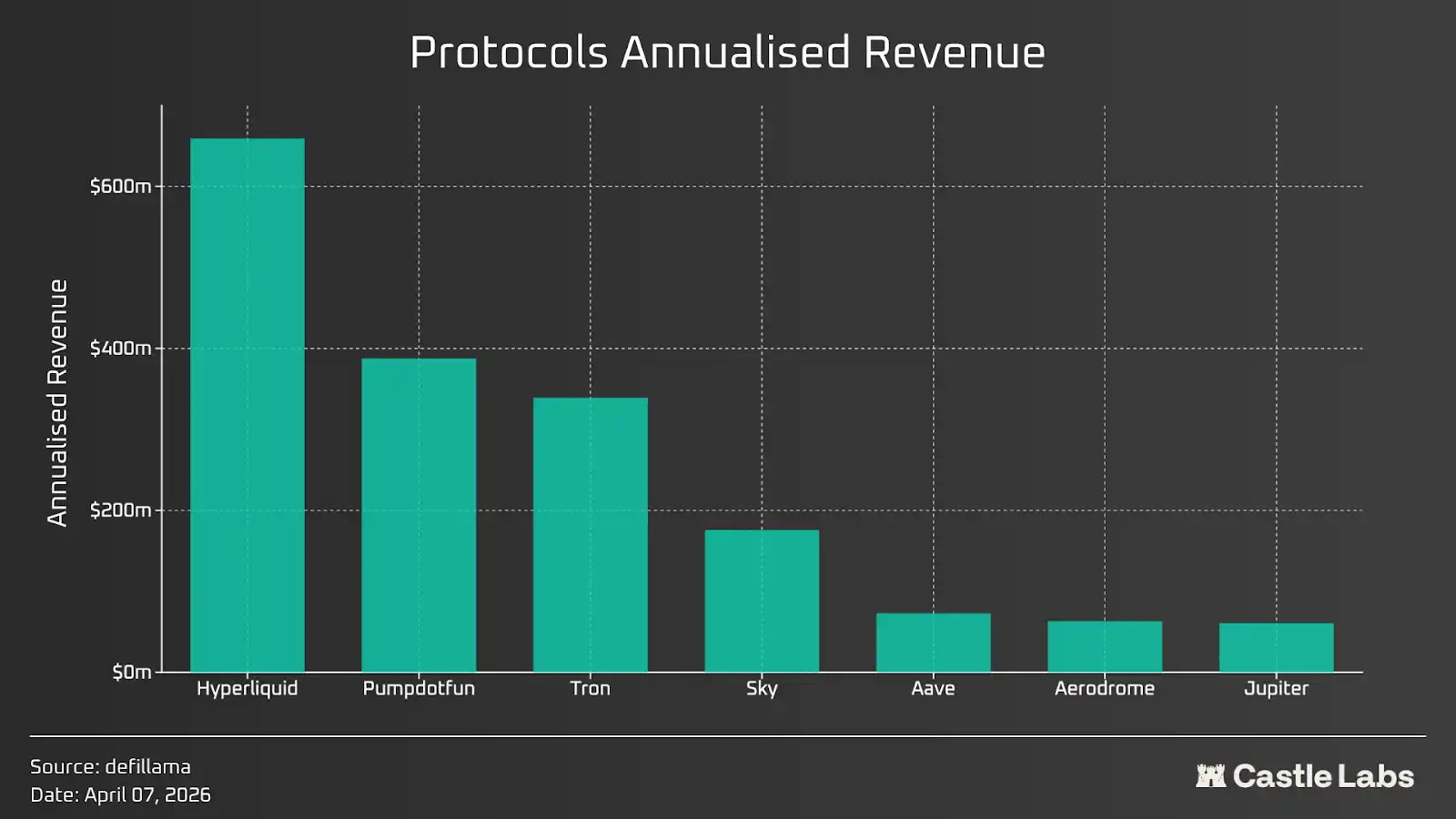

The following discusses some key metrics crypto investors should consider when analyzing tokens. This article analyzes some of the highest revenue-generating token protocols over the past 30 days, including Hyperliquid (HYPE), Pumpdotfun (PUMP), Tron (TRON), Sky (SKY), Jupiter (JUP), Aave (AAVE), and Aerodrome (AERO).

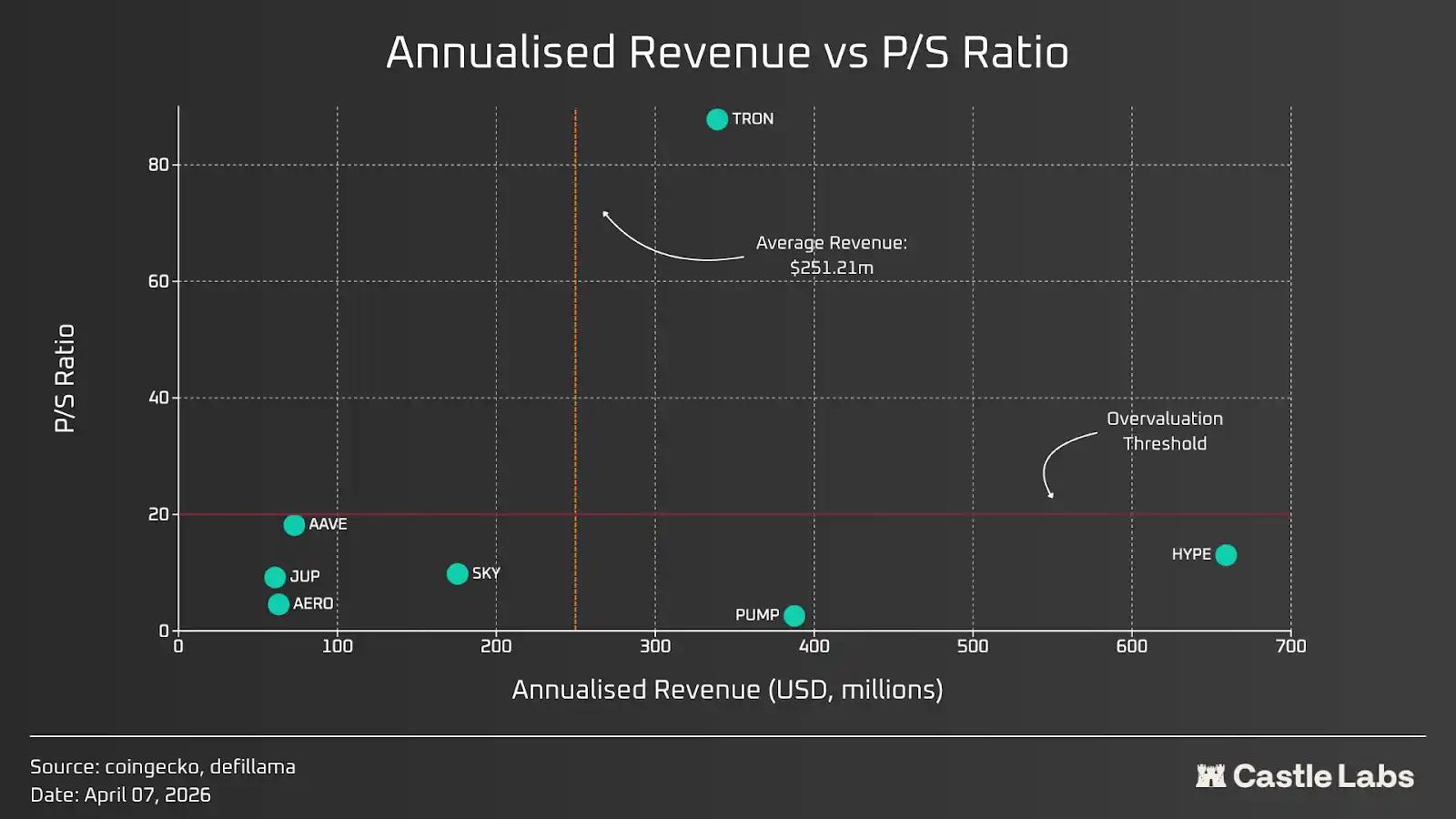

Price-to-Sales Ratio

The Price-to-Sales Ratio (P/S) is calculated by dividing the protocol's market capitalization by its annualized revenue. The P/S ratio measures how much the market is willing to pay for every dollar of revenue generated. The premium reflected by this ratio indicates how much users value the protocol's future capabilities and growth factors.

We compared some of the highest revenue protocols and their tokens based on annualized revenue and P/S ratio. We took the past 30 days' revenue and multiplied it by 12 to get the annualized revenue figure. The results are shown in the chart below.

We set the overvaluation threshold at a P/S of 20, based on the P/S ratios of top US listed stocks. Most protocols have a P/S ratio near or below this threshold, with only Tron's P/S ratio significantly higher than the others. Another threshold we considered was revenue, using an average annualized revenue of about $250 million. Only three protocols exceeded this threshold: Pump.fun, Hyperliquid, and Tron, which together account for about 80% of the total revenue of the protocols mentioned above.

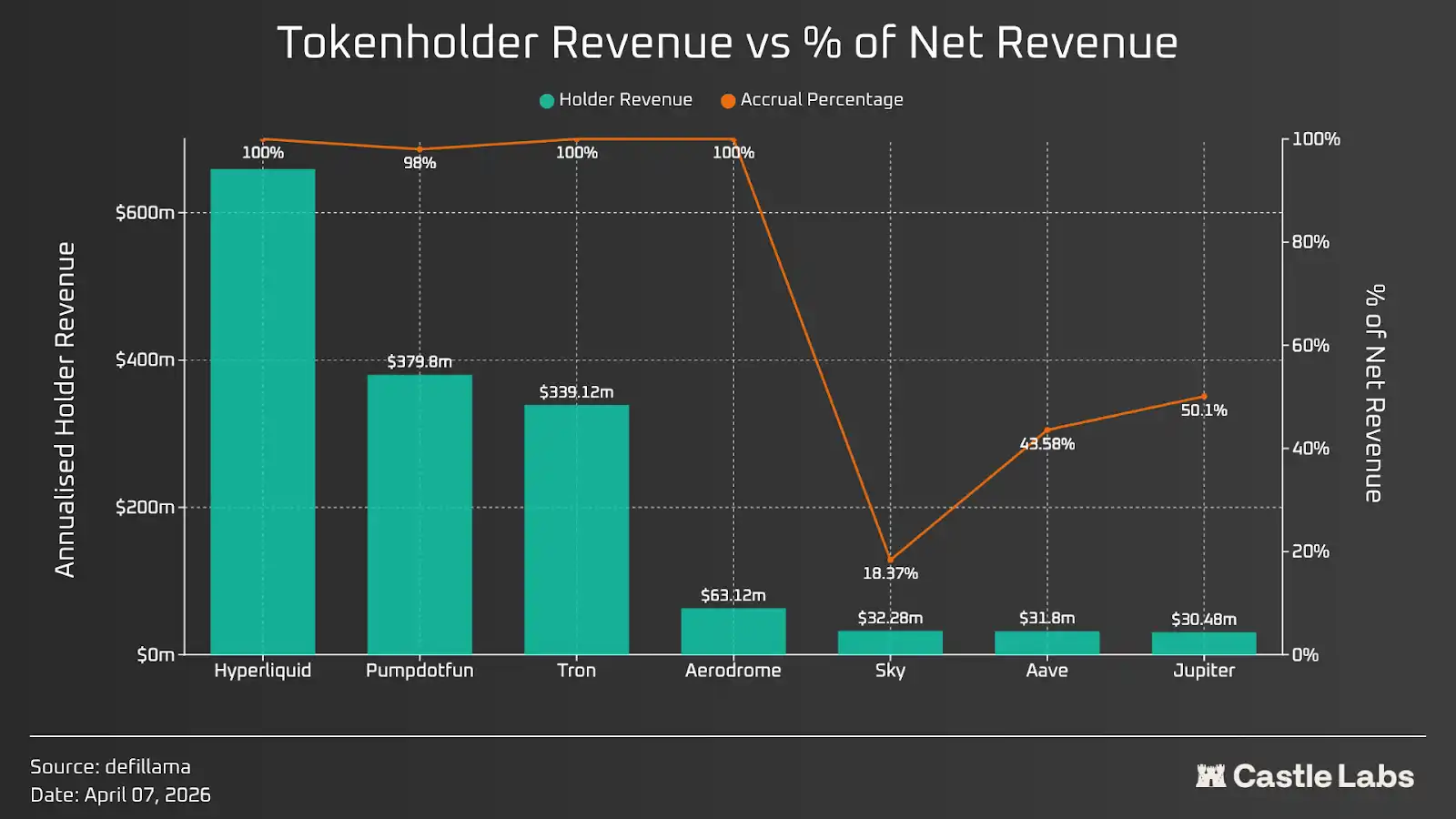

Token Holder Yield

The next important factor to discuss is token holder yield. This depends primarily on the protocol's revenue and the portion actually returned to token holders through methods like buybacks, token burns, and staking rewards. Today, token holder yield has become a hot metric, almost everyone is talking about it, and it is more important than the actual revenue because this is how value accrues to the token.

Again, we categorized the protocols based on holder yield over the past 30 days, multiplied by 12 to get an annual estimate. At first glance, most protocols treat their holders fairly and use most, if not all, of the revenue to enhance token value.

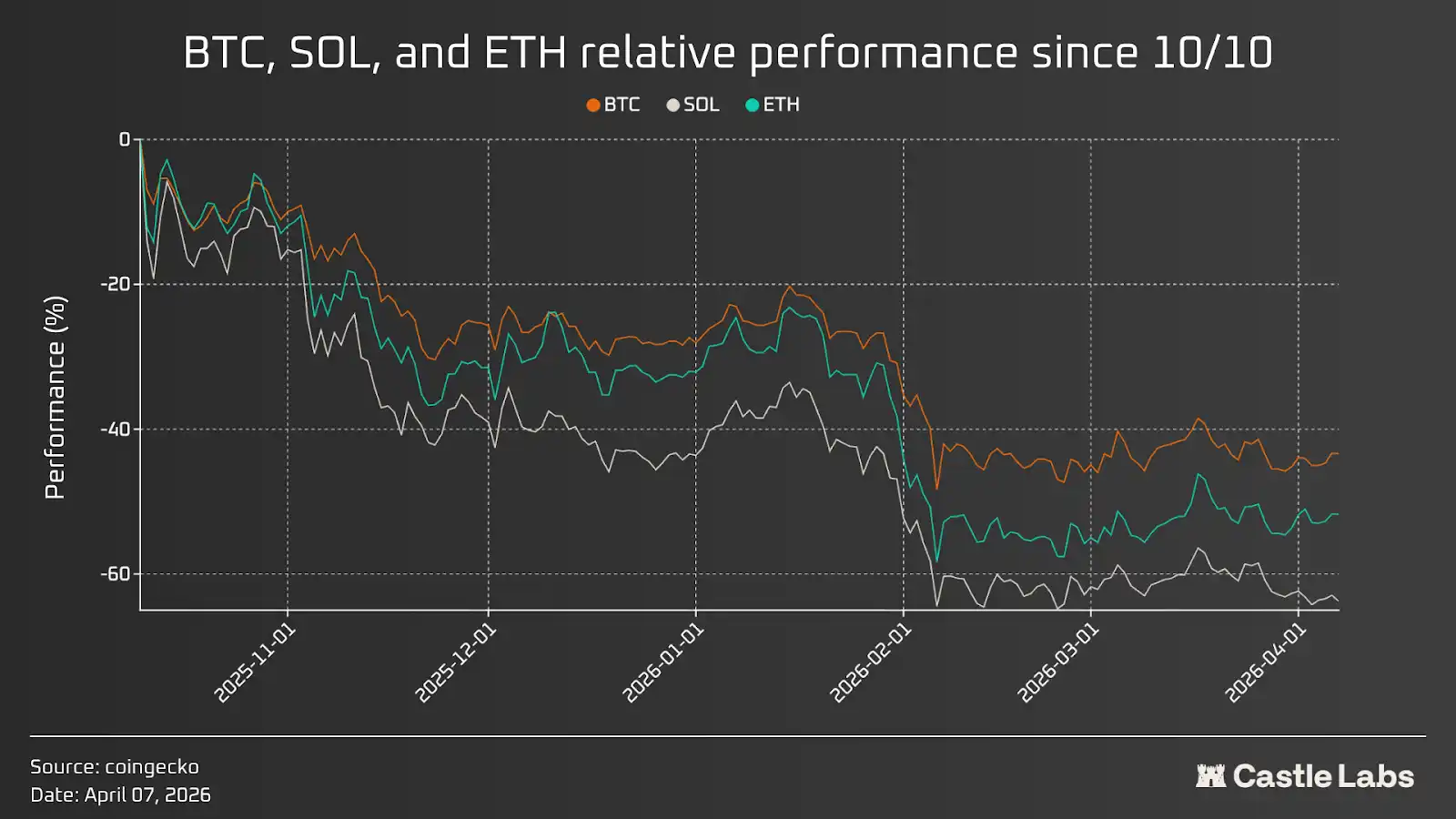

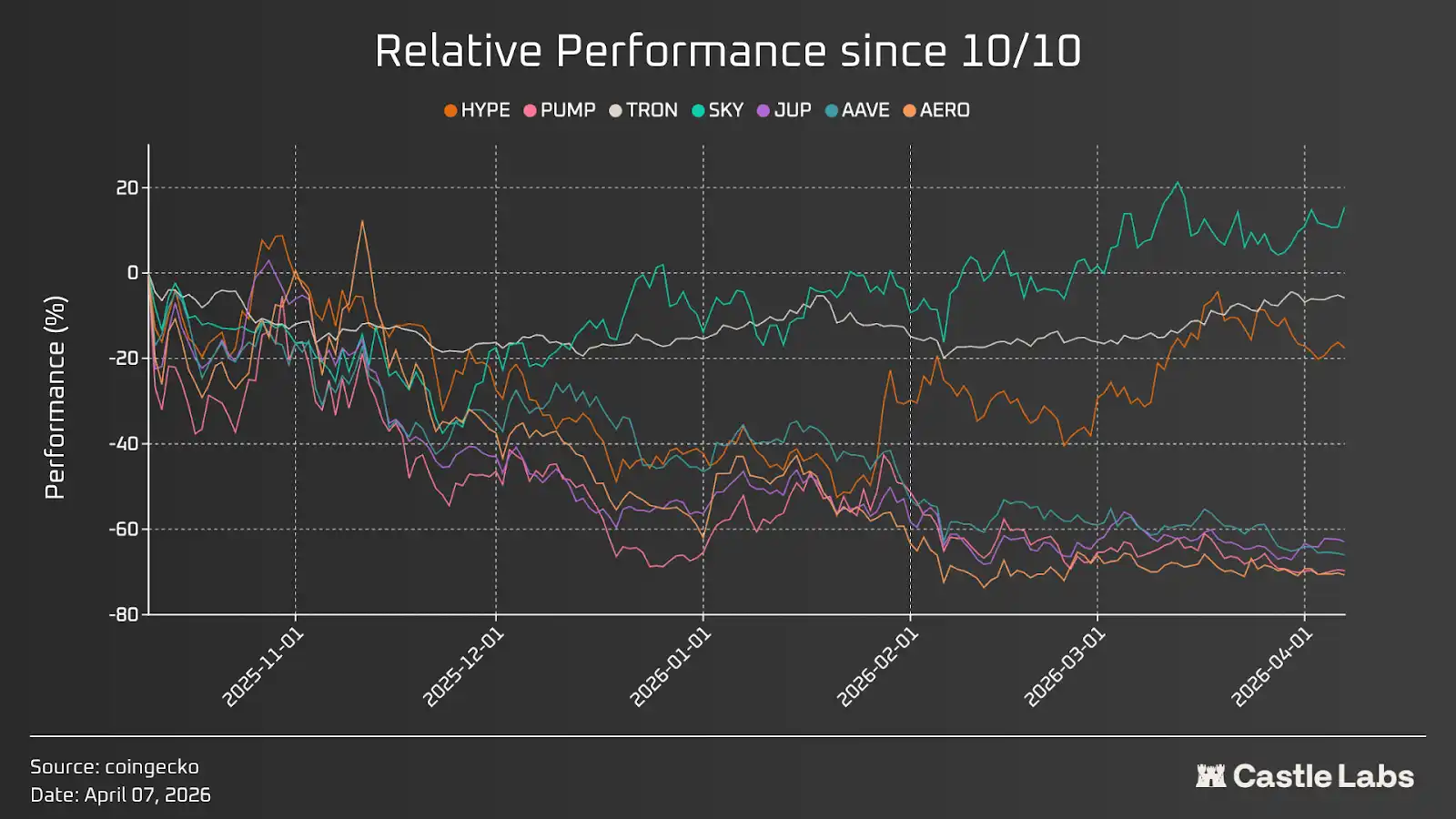

This is just one side; it reflects that token buybacks are ongoing, and if continued at a similar pace, will add millions of dollars in value to the tokens. To better understand this value accretion, we also compared these tokens' relative performance after the October liquidation event to show the impact of token value-add activities more clearly.

In the chart above, there are some outliers, such as TRON, HYPE, and especially SKY, which showed positive relative performance. Among these three tokens, TRON's price movement was relatively flat; while HYPE's price diverged from other tokens in late January.

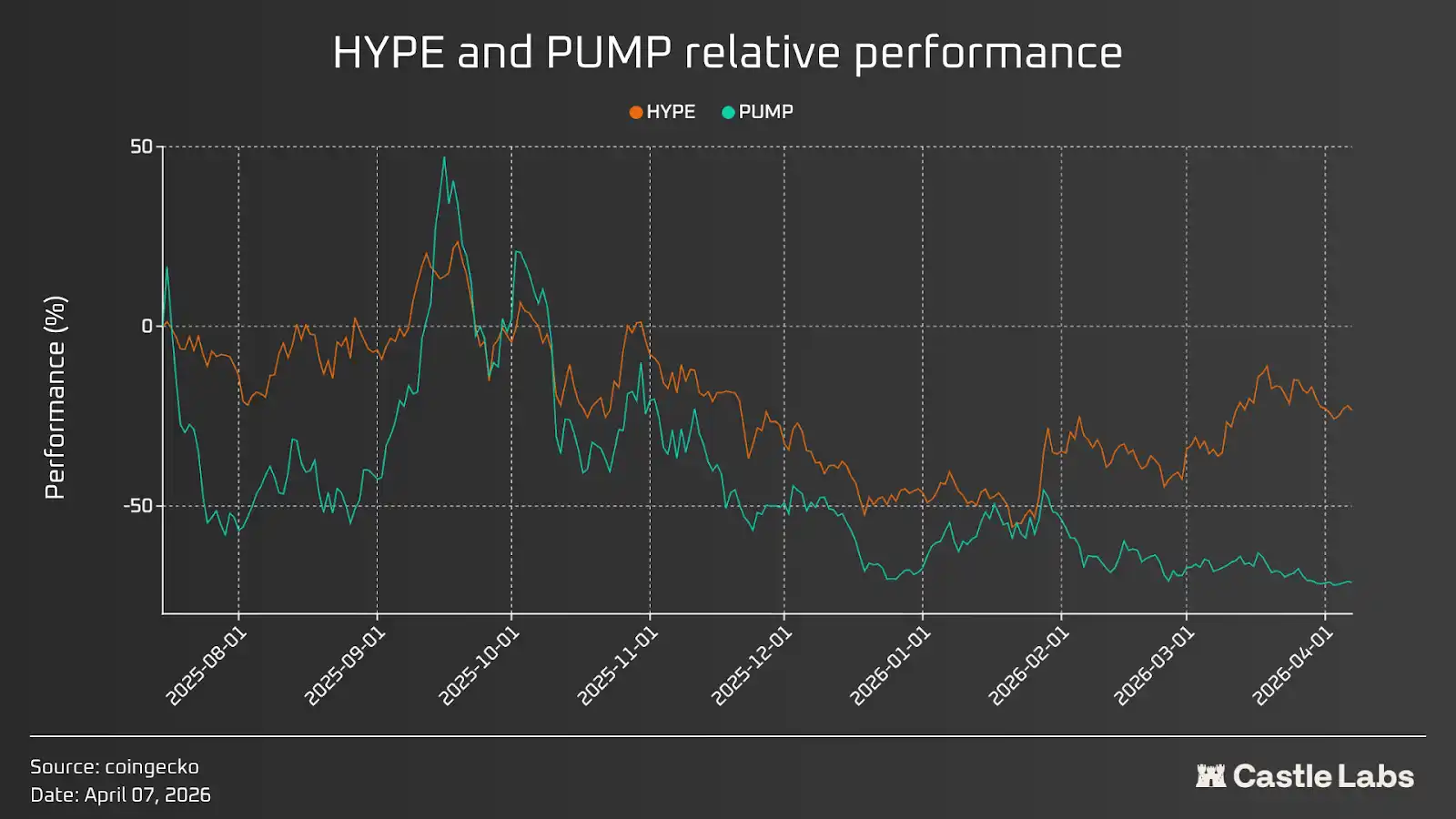

This indicates that buybacks alone are not enough to boost token value; other factors, such as broader market declines, token unlock schedules and cliff unlocks, market prospects for the sector narrative, and the overall sentiment towards the protocol, also play a role. All these factors will be discussed in subsequent sections. Before that, let's compare the two protocols with the highest yields and their token performance: Pumpd.fun and Hyperliquid. As can be seen from the chart below, when both tokens have active buyback programs, HYPE performed better (HYPE's annualized holder yield is about $660 million, PUMP's is about $380 million), because the overall market sentiment for this protocol is good, and people are pricing the token based on future supply shocks and unlocks.

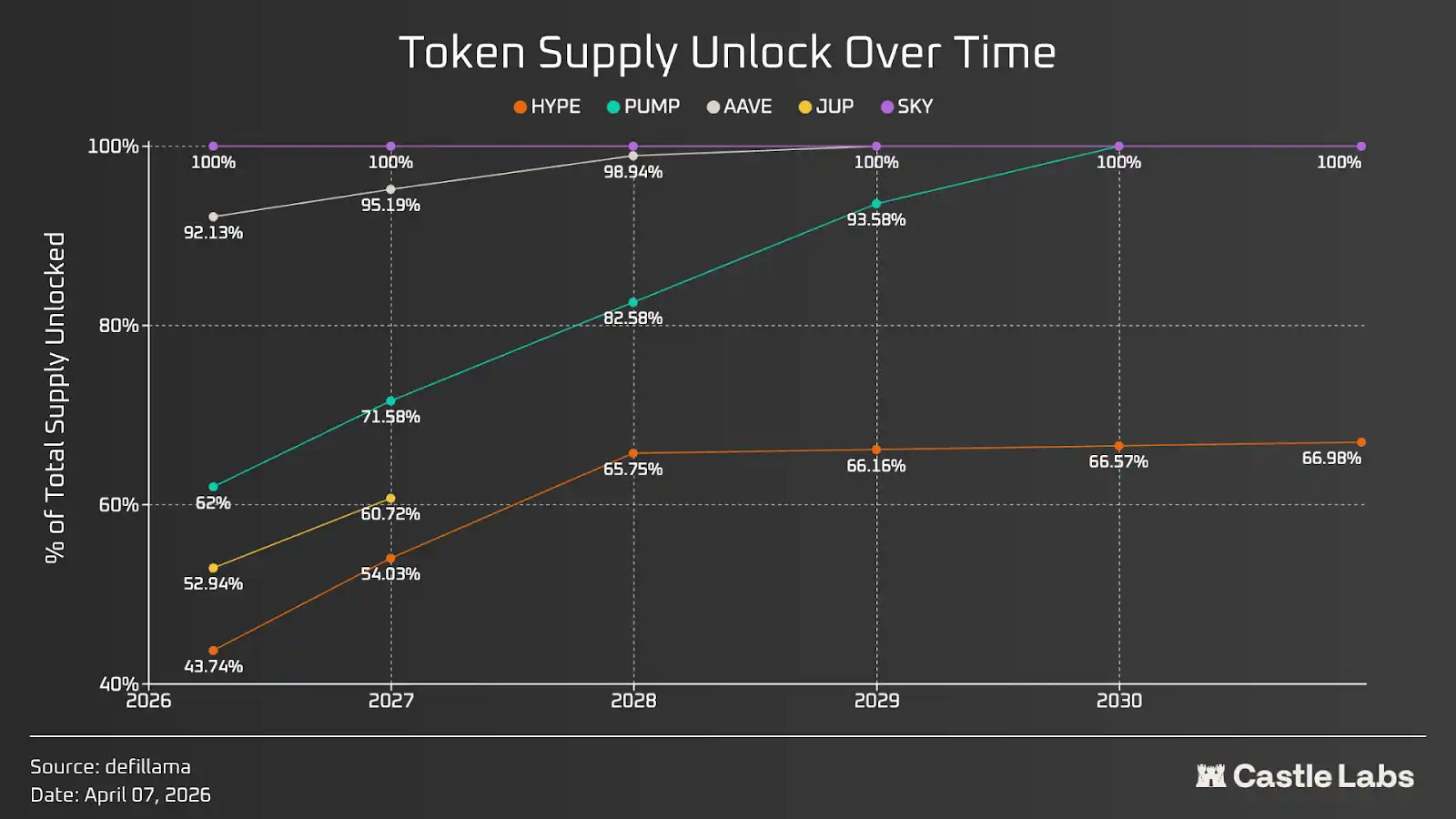

Tokenomics Design and Supply Overhang

In crypto, tokenomics aims to help projects raise funds from investors, incentivize users, sometimes conduct community fundraising, and allocate token supply to the project team. There aren't many hard rules for designing tokenomics, and different projects handle it based on their circumstances. This part is crucial because it determines not only the near-term supply pressure of the token but also how value accrues to the token, the value-destructive mechanisms used to offset selling pressure, and the alignment of the token with its holders' interests.

The chart below shows the unlock speed for a selection of fixed-supply tokens. While most tokens will eventually be fully unlocked, the unlock speed varies significantly: PUMP unlocks the fastest, while HYPE unlocks the slowest. Generally, a slower unlock speed is preferable because it reduces the possibility of sudden supply shocks and the resulting selling pressure that the market may struggle to absorb. For tokens like AAVE and SKY, most of the supply is already unlocked; for JUP, the long-term unlock schedule is discretionary rather than deterministic, managed by the DAO.

It is important to emphasize that unlocked tokens can be further categorized into investor unlocks, team unlocks, and community unlocks. Community unlocks can be used for staking rewards, incentives, and airdrops. This requires analysis on a token-by-token basis and plays an important role in understanding the seller dynamics of the token.

The Lindy Effect

"The longer something has existed, the longer it is likely to continue to exist."

This is the essence of the Lindy Effect, which applies to almost all businesses, including on-chain businesses, where innovation is a key factor because those that do not innovate cannot survive long-term.

Last year, the cumulative revenue of crypto protocols was about $16 billion, with revenue highly concentrated in a few top protocols. The top ten protocols accounted for 80% of net revenue, with the top three accounting for 64%, and Tether alone accounting for 44%.

Furthermore, not all protocols have issued tokens; for example, Circle is the second highest revenue protocol after Tether, and its stock is listed on the New York Stock Exchange under the symbol CRCL. Meanwhile, Tether has not issued a token. Even among the top ten protocols, only three have issued tokens, indicating that issuing a token is not always the best strategy, depending on the protocol's design.

Returning to the Lindy Effect, in most cryptocurrency categories, the top two protocols capture the largest market share and dominate. This is even more common in the stablecoin category, for example Tether (USDT) and Circle (USDC) account for 84% of the entire market, followed by other players like Sky (USDS) and Ethena (USDe). In some other areas, this pattern may seem less obvious, but it can still be pointed out, for example in the lending space, the top two protocols by TVL (Aave and Morpho) capture 64% of the market share. The same pattern is evident in multiple categories, such as prediction markets, yield, liquid staking, restaking, etc.

The Lindy Effect is also important due to the frequent hacks suffered at the protocol level in the crypto industry. This year alone, over $130 million has been lost from smart contracts, and the amount lost over time amounts to tens of billions of dollars. Therefore, entrusting funds to any new protocol becomes increasingly difficult because you cannot predict when it might be hacked. Thus, the runtime of the contract and the existence of the protocol are crucial, as the system has stood the test of time and never failed. Even in cases where the system did not perform as expected, such as the recent Aave CAPO oracle reporting error, users were reimbursed because the protocol's treasury could cover the cost. Furthermore, the longer a system exists, the more it proves its importance during market downturns. Top protocols performed as expected during market downturns, strongly suggesting that anyone should use these time-tested systems.

On the other hand, innovation is equally important, as market leaders are constantly innovating and improving their products. For example, Morpho is bringing numerous institutions into on-chain finance through its vault architecture, allowing them to personalize vaults to maximize their own needs. Aave will also introduce this capability through its upcoming v4 upgrade with its Spokes feature. Additionally, Aave is enabling institutions to borrow against tokenized RWA as collateral through its Horizon instances.

The next wave of cryptocurrency is composed of institutions and "agentic finance"; the protocols best positioned for these two directions will see the greatest growth.

Crypto Doomerism

In Citrini's article "The Global Intelligence Crisis of 2028," they wrote:

The best way to consistently save users money (especially when agents start trading among themselves) is to eliminate fees. In machine-to-machine transactions, the 2%-3% credit card transaction fee clearly becomes a target.

Agents began looking for payment methods faster and cheaper than credit cards. Most agents ended up using stablecoins via Solana or Ethereum L2s, where settlement is almost instant and transaction costs are as low as a few cents.

This opens our next chapter, which goes beyond institutional adoption of cryptocurrency and focuses on agentic finance and the broader application of blockchain technology by agents. This process has already begun, with many protocols integrating AI agents to streamline user processes and eliminate the UX bottlenecks that have long plagued crypto products. All these efforts can be categorized under the label that surfaced in late 2024: the combination of Decentralized Finance and AI (DeFAI). It worked, but like everything else in crypto, it turned itself into a "yield-first" narrative, but it did highlight how integrating more AI could greatly improve the crypto experience.

Fast forward to June 2028, most crypto transactions are performed by agents, with no human involvement. Agents seek the best yield for their users based on their risk preferences. For non-crypto-native agents, blockchain is considered the best place to execute most transactions due to its low cost, high efficiency, and verifiability. Over time, block space became cheaper, and transaction costs dropped significantly. Cryptocurrency is no longer complex. You can give an AI agent a prompt and some money, and it will help you earn the best yield. Cryptocurrency and blockchain have become mainstream and are widely used. To improve overall capital efficiency, agents move funds from protocols generating low yields or liquidity pools not being used optimally to a few concentrated places where the best yield can be found. Most public chains and protocols are practically淘汰 (eliminated) due to lack of use. The value of the tokens you invested in falls to the lowest point since your investment; you start to think you should have exited in 2026. Only a few tokens have risen, including those that truly generate revenue and continuously accumulate value through it. Capital withdrawn from all other tokens flows into the few tokens with actual performance and utility. Compared to March 2026, the total market capitalization of the crypto market has increased, but most tokens have not benefited from the growth in institutional adoption and agentic finance. The dream of crypto technology is finally realized; it is widely used by the masses, but the token part has developed very differently than many expected.

It is now March 2026; whether you believe the above scenario will come true or not, protocols with positive cash flow will sustain long-term development, and their tokens will thrive.

Conclusion

For years, crypto protocols have focused on technical issues and never really focused on product PMF, which is the biggest risk investors never priced in, but the market has finally realized it. For years, the prices of most tokens have continued to fall, with all-time highs long gone, making it clearer than ever that change is coming. The rise of certain tokens in 2026 reflects the importance of revenue data and token-first strategies, as investors begin to shift from speculation to investment.

The bad actors in crypto have always profited from the "yield-first" narrative, while most participants in this space leave with losing investment portfolios, becoming exits for liquidity, which is very unhealthy. With the influx of institutions, this perception has deepened, as they do not want to have much to do with our assets, but are more interested in the infrastructure we have helped build over the years and that has been battle-tested.

As we further develop with institutions and AI-powered crypto infrastructure, we may see this trend become stronger, as more and more investors will look for "hard metrics" that convince them to buy tokens or stocks.

Related reading: Conversation with an Airdrop Hunter: From Getting Rich to Just Running Along, Do Ordinary Players Still Have Gold Rush Opportunities?