The FTX incident is commensurate to the "Lehman Moment" of the traditional financial world. The spread and scope of the event has gone far beyond what was previously thought. And just Thursday night, the U.S. Bureau of Labor Statistics released data showing that the U.S. CPI rose 7.7% year-over-year in October, below the market expectation of 7.9%, and far less from the previous value of 8.2%. the CPI rose 0.4% year-over-year in October, also better than market expectation.

""

The crypto market has experienced tremendous fluctuations in an industry-wide crisis, as if on a turbo drop, and rebounded after long-craved relief from high inflation. What lessons should cryptocurrency exchanges learn and how should investors respond in such a tsunami?

""

1. Crisis for all exchanges

""

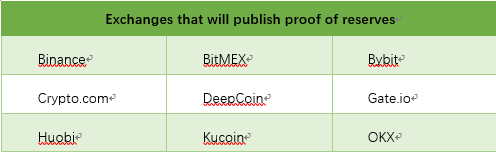

The FTX incident stemmed from appropriation of user assets, and the biggest consequence was the widespread distrust of cryptocurrency investors towards exchanges. Other exchanges were implicated and experienced runs by various degree. In response to the crisis, leading exchanges, mainly Binance and Huobi, have come forward to announce that they will guarantee safety of user assets through Proof of Reserve in the future, and establish a disclosure scheme for the sake of information transparency.

""

1.1 Asset outflows

""

The market is down severely and some funds fled. Binance is by far safe and sound, and FTX has almost nothing left.

""

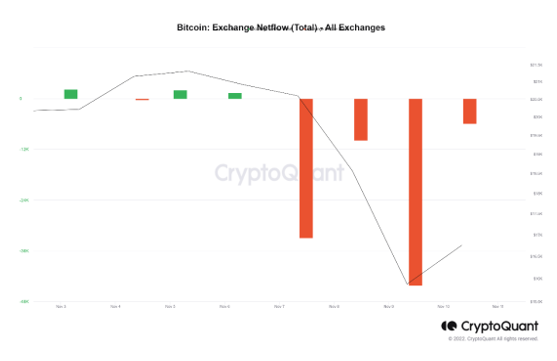

The chart below illustrates the net inflow and outflow of BTC from the mainstream exchanges in the last 7 days. From November 7, the exchanges have had a total net outflow of 92.8 K in BTC in the last 4 days, accounting for 4% of their total holdings. Similar to stablecoins, with net outflows of 3% of the total holdings over the last 4 days. This is the third flee of BTC in large amount this year, with the previous 2 occurred during May 12-17 and June 15-17 respectively. The first event was affected by the LUNA crash, and the second was on Celsius along with the Fed's first interest rate hike of 75 basis point. After the 2nd BTC outflow, price of BTC dropped 16%, while BTC has fallen about 20% since the incident, and the market is still adjusting. Evidently, this event has a greater impact on the market.

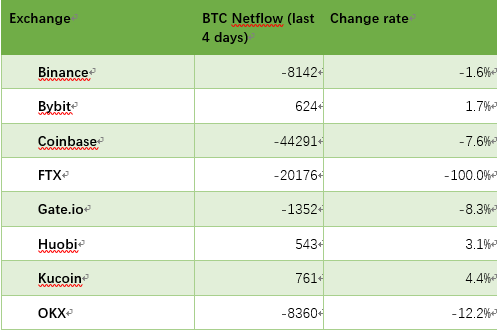

Looking at the net outflows of BTC from the mainstream exchanges, we find that most of them did not experience significant asset outflows, except for FTX, which completely collapsed. Moreover, only small amount has been withdrawn from Binance, whereas inflows were spotted for Huobi, Kucoin and Bybit. It turns out that users remain confident on their trusted exchanges. Despite rumors that Kucoin might be running low on reserves, CEO of Kucoin responded quickly to eliminate any concerns. The only exchanges with large net outflow of assets were OKX and Coinbase, which could be attributed to Star Xu's claim of support to SBF a few days ago and Coinbase's recent downtime; users are concerned about the coincidence.

At the moment, it seems that the impact of the crisis remains on the psychological level of investors that no large scale of exodus in funds is present. The industry has had little good news in the past year, which has elevated the risk aversion for investors, resulting in panic and dumping. Most investors are still most familiar with and attached to centralized exchanges, so the outflow of funds was not severe.

""

1.2 Proof of reserves

""

The reserve is the touchstone, and a long-term mechanism is the key.

""

The most urgent schedule for exchanges today is to prove that user assets are sitting tight in their accounts rather than misappropriated. Since the FTX incident, several mainstream exchanges have issued announcements that proof of reserves will be published soon. Among them, Binance was the first to announce cold/hot wallet addresses, and Huobi is currently expediting the landing of POR. Furthermore, because Huobi has just completed a major acquisition, the assets have been under supervision of multiple credible parties and remain highly secured.

""

The announcement of POR reflects the sense of responsibility of exchanges, and it indeed is soothing to users. Exchanges that are bold enough to announce POR in the first place are most likely not misappropriating user assets. If the announcement is to be published even one second later, users may just turn to competitors immediately as the anxiety cannot wait. Ultimately, the reserve is a bona fide touchstone to accelerate the cleansing and reshuffling of the exchange segment.

The crisis has once again reminded the public that no platform can be trusted easily as long as it has a connection to finance, unless the announced public data is verifiable and credible and scrutinized by strictest regulatory. Due to the inconsistent policies across countries, plus regulations usually take all the time in the world to come out, it is unrealistic to expect that unified rules can be issued by regulators from multiple countries in the short term. A more feasible approach would be that leading exchanges in the industry could collectively agree on a code of conduct and adhere to it: misappropriation of user assets is a red line that no one can ever cross, and regularly disclosing proof of reserves to the public. Although such rules are not enforced by law, users would be more liberal to choose their own services so that violators will be kicked out of the game, the crypto market henceforth could become healthier and more mature via such a long-term mechanism.

""

For some, the skyrocketing price last night may erase the influence of the FTX incident for some time, but if the discussion ends here, no one could guarantee that they would be the lucky ones to survive from the next incident, furthermore, no one could promise that no incidents would happen in the future at all. The short rejuvenation of the market is also a touchstone for those who are willing to demonstrate good ethics in fiduciary interest of their clients in long-term.

""

2. Risks and opportunities

""

2.1 Dominoes

""

2.1.1 Risk of serial liquidations

""

Witnessed a tragical decline in recent days, could serial liquidations happen soon? For this reason, we have conducted an on-chain liquidation analysis of several mainstream coins and other altcoins closely associated with FTX.

""

BTC and ETH are safe from the mass liquidation line, and the rest of the coins are relatively safe or have little impact on the market.

""

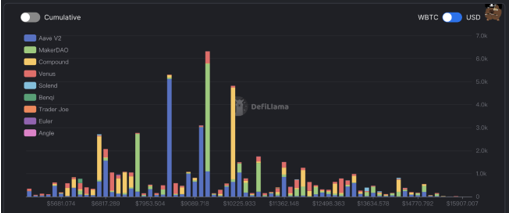

>WBTC

""

WBTC had small liquidations in $14933 and $14282 with 700-800 pieces on mainly compound maker. Large liquidation is usually between $8000-$10000 at about 5000 pieces; the price will not reach this level in average circumstances except for some major events are in the place.

>ETH

""

Strong liquidation risk for small-size (worth US$ 28M) occurs at $1050 and dominated by compound. There are two large liquidation lines, at $800-820 (worth 100M) and around $700 (worth 300M), both dominated by MakerDao. Same, something must have happened, and no risk otherwise.

>SOL

""

SOL has a large liquidation risk of $0.37 M at $10.73 with a current price of about $14; the nadir touched $12.46 in 6 hours. The trigger is likely to be pulled as SOL has tokens to be unlocked today, and panic has been dense on the market. However, from the short-term view, due to the extremely high volume of short positions in perpetual contracts, the shorting fee has been as high as 30% in a single day. In this case, it is not likely to go straight down; on the contrary, it is possible to repeat rises, pushing the short positions to be liquidated. In addition, the Solana Foundation postponed the unlock of about 28.5 million SOLs, and SOLs are less likely to fall sharply in the near future.

""

>SUSHI

""

Although Alameda's xSUSHI holdings are high, the on-chain staking landscape are relatively healthy because SUSHI is generally in staking on xsushi without leverage, so there is less risk of force liquidation on-chain and less pressure to follow.

""

>SRM

""

There are $140,000 worth of SRM in staking of the Solend pool, and almost none in other platforms. The LTV of SRM is only 65%, and very little impact it would exert to the market even if all are liquidated.

""

2.1.2 Risk of joint and several liabilities for institutions and projects

""

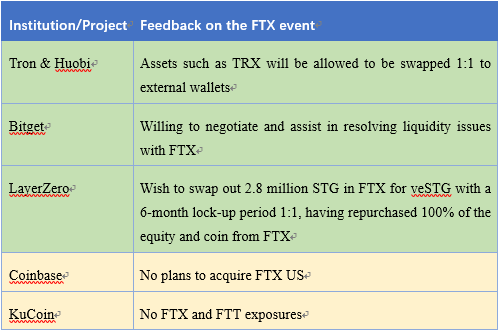

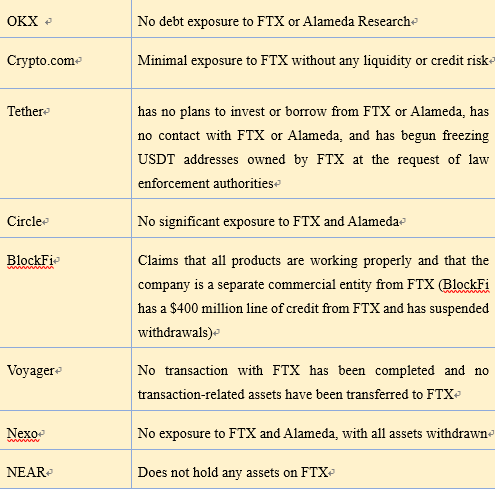

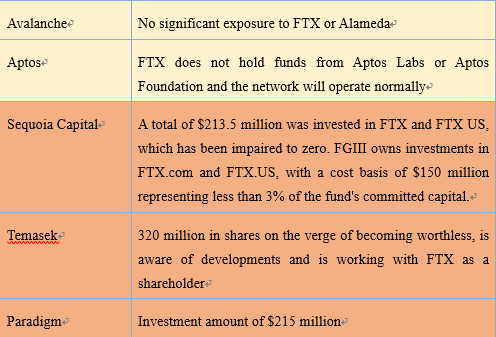

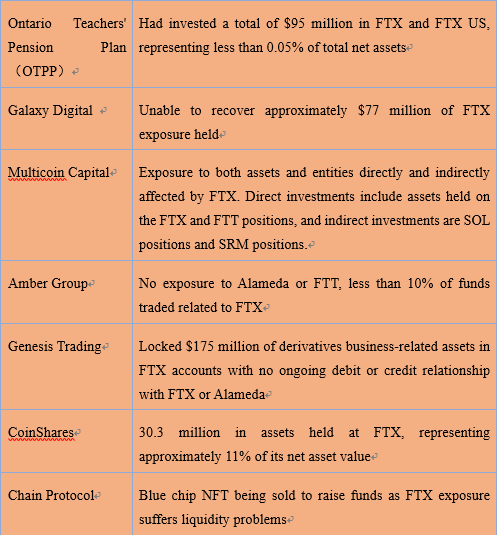

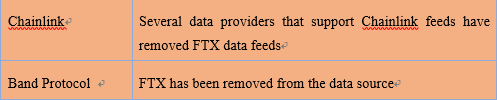

After the FTX outbreak, feedbacks were received from institutions/projects associated with FTX and Alameda, including funding investors, exchanges, crypto lenders, market makers, L1 chains, on-chain projects, etc., as specified in the table below. Institutions such as Huobi, Tron and Bitget (shaded in green) are actively negotiating with FTX to resolve liquidity issues and acting on behalf of the best interests of users. A large number of institutions (shaded in yellow) have indicated that they have associated risk exposure and the operation is not affected. BlockFi, which was acquired by FTX, has, in fact, suspended withdrawals. Having been issued a $400 million credit line by FTX, it is doubtful if the daily operations of BlockFi could sustain when FTX goes bankrupt. Those more affected by this (shaded in brown) are mainly FTX's funding investors and institutions that have significant amount of assets or trading tangled with FTX. Sequoia Capital, Temasek and Paradigm will likely be the three institutional victims with most losses: each of them has $200 million or more in investments to FTX that are likely to vanish. Numerous institutions are involved so far, most of them are capable of withstanding the shock according to publicly available information. That is to say, the odd of serial collapse is rather low.

2.2 Market forecast and optimal investment strategy

""

The market rallied strongly immediately after the release of the U.S. CPI data for October. As U.S. inflation shows signs of slowing down, marginal improvement is expected by the market in the Federal monetary policy, and the federal funds rate is likely to reach the ceiling in the first quarter of next year; the market will see a turning point in terms of liquidity. From a macroeconomic perspective, the bear market won't be too long.

""

Let's combine a few more criteria to see if the bottom of the market has been reached in this round of bear market, and some investment strategies will be given as conclusions.

""

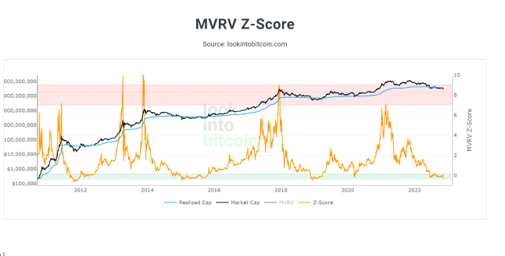

>BTC MVRV Z-Score

""

The MVRV metric is the ratio of Bitcoin's Market Value to its Realized Value, which rarely declines and generally considered to be strongly supportive. The greater the MVRV, Bitcoin is more perceived as overvalued, and the possibility of price fall is high, and vice versa. The MVRV Z-Score is smoother and more reflective of long-term trends than the MVRV.

""

As demonstrated in the chart below, the Z-Score is a handy indicator that is capable of seeking for the crest and the nadir. Whenever it reaches a negative value, which is the green zone, it signifies the periodical bottom. The current bear market is different from the previous ones, as MV and RV have been tangled since June, and the Z-Score has been swinging horizontally. It was only recently that the FTX incident triggered a downward trend. In other words, it might be deemed as the lowest point in the bottom has appeared, or on the way.

>Fear & Greed Index (FGI)

""

The investment market is a game with people, greed and fear are instincts that can never be stripped off a human being. The graph illustrates the relationship between FGI and BTC price in the past 2 years. Two conclusions can be drawn from the graph. First, periodical bottom is often accompanied by a sharp drop in FGI to around 10. Second, the bottom of FGI tends to precede or sync with the bottom of price rather than lagging behind.

""

Even with the market panic triggered by the FTX event, recent FGI has been above 20, indicating relatively stable market sentiment. Again, due to the anticipation rises on the relief or high inflation in the U.S., the market morale is unlikely to fall significantly in the near term. If there are no more series of institutional incidents afterwards, it could be said that the bottom may be right there.

The forecast is based on rational analysis on the market, and forecast is just forecast. In particular, the FTX incident is not something we see every day, the possibility of future institutional breakout and associated market downturn cannot be ruled out. It is crucial for one to find his/her own best suitable strategy.

""

Aggressive strategy: If an automatic investment plan was in effect previously, it should be continued. If the decline increases, the installment also increases. If the position is still low, a position could be set up at this time, longing on mainstream cryptocurrencies with risk adjustments according to market conditions.

""

Mild strategy: Positions are to be set up when the following two conditions are met at the same time: first, the Z-Score begins to be seen upward in the green zone; second, the BTC price does not fall to a historical new low for 7 or 15 consecutive days. At least 20% of cash cand be reserved in case of unexpected declines. Futures are off the table for now.

""

In addition, most exchange platform coins have been seen declines greater than 10% in this crisis. However, based on the direction of asset flows mentioned above along with the claimed action on publishing proof of reserves, platform tokens may be underestimated by false judgements, and those overly underestimated could be ideal target if an aggressive strategy is adopted.

""

All the above strategies do not constitute investment advice, please invest rationally and enjoy profits and losses at your own risk.