Written by: Andjela Radmilac

Compiled by: Saoirse, Foresight News

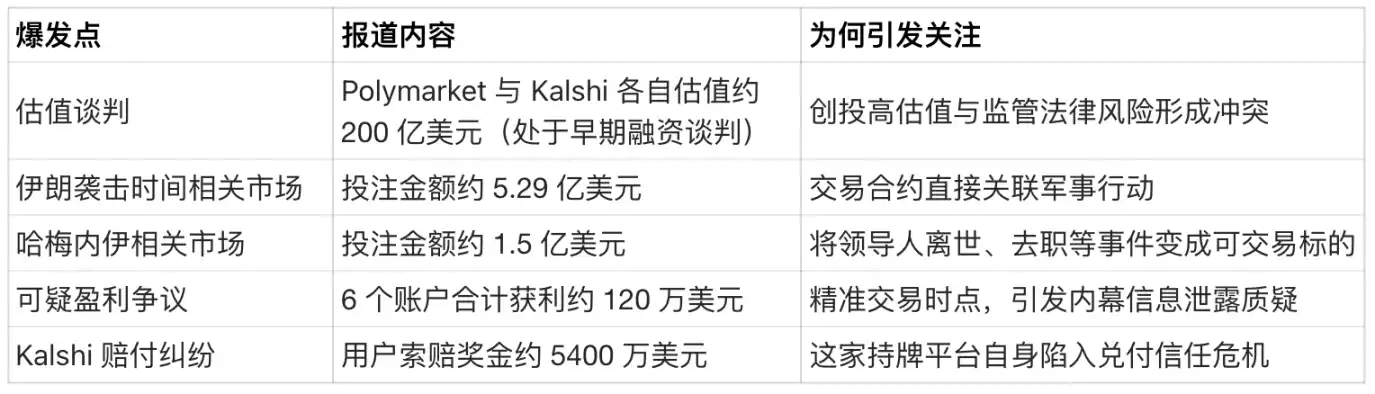

Polymarket and Kalshi are seeking funding at valuations that would place them among the top consumer fintech companies, while U.S. regulators are simultaneously accelerating the development of new rules for such products. It is reported that both companies are in early-stage funding negotiations, with valuations expected to reach approximately $20 billion each.

This funding boom coincides with a political storm.

Iran-related contracts have turned prediction markets from a niche forecasting tool into a controversial focal point involving insider information and war speculation. A Reuters investigation into the markets on Polymarket related to the timing of the attack and Khamenei's ouster found that approximately $529 million was wagered on contracts related to the timing of the attack, and about $150 million was bet on contracts related to Khamenei; meanwhile, sources indicate that six accounts, through precisely timed trades, collectively profited about $1.2 million.

Now, U.S. lawmakers are drafting relevant bills, and the U.S. Commodity Futures Trading Commission (CFTC) has also stated it will advance new regulatory rules.

Wall Street believes that event probability prediction will become part of the information system; but Washington is blocking it because it fears this system could benefit the wrong people at the worst possible time.

Why Wall Street is Bullish on Prediction Markets

Prediction markets can convert attention into trades, earn fees from those trades, and simultaneously generate real-time probability data, packaged as information products.

It is this data product that moves prediction markets out of the "gambling" category and classifies them as information tools similar to market data, polls, and financial terminals—because their output format is highly similar to market quotes.

Mainstream media have begun partnering with these platforms:

- CNBC has signed a multi-year agreement with Kalshi to integrate its probability data into television and digital content starting in 2026.

- Dow Jones has reached an exclusive deal with Polymarket to introduce prediction data into platforms like The Wall Street Journal and Barron's, treating contract prices as news infrastructure on par with earnings reports, interest rates, and election coverage.

These partnerships also amplify the impact of scandals: once probability data is embedded in mainstream media, it influences public perception of an event's likelihood and urgency. This is also why regulators believe platforms must adhere to higher standards in fairness, monitoring, and settlement.

This explains why, even as Iran-related trades spark political controversy, the valuations of both companies are rising.

Iran Incident Makes Prediction Markets a Washington Headache

The biggest advantage of prediction markets is early access to information. And the Iran-related contracts clearly show that these platforms are touching on sensitive information that the government tries to control.

On March 2, bets on the attack timing-related contracts reached $529 million, and contracts related to Khamenei's death and ouster reached about $150 million. Just hours before the attack on Iranian officials, six accounts suddenly injected funds and profited $1.2 million through these contracts.

As the conflict escalated, multiple reports pointed out that a large number of newly registered accounts made precise bets on Iran-related events. Such reports have thrust Polymarket from a crypto-niche platform directly into the sights of government regulation and law enforcement.

The core issues these platforms now face are: trust and fairness.

For prediction markets to function, users must believe the rules are stable, outcomes are determined consistently, and there is no insider advantage. Once the subject of trading is military action, the trust issue escalates into a political problem—because the motive for trading early could become a motive for leaking sensitive or even classified information.

This is also why the policy response has rapidly escalated.

Representative Mike Levin and Senator Chris Murphy are already drafting legislation aimed at restricting prediction markets. Congress will directly define which event contracts can be legally traded.

Additionally, CFTC Chairman Michael Selig stated that the agency has submitted an advance notice of proposed rulemaking to the White House Office of Management and Budget and is about to introduce a regulatory framework for prediction markets, which could affect all aspects from contract design to monitoring and enforcement.

The choice facing Washington is clear:

- Acknowledge prediction markets as legal event contracts, strengthen regulation, clarify restrictions, and allow the industry to expand orderly under rules;

- Directly prohibit contract categories related to war, assassination, and leader ousters because such trading极易 (is highly prone to) trigger insider trading and foster不良动机 (bad motives).

The data below reveals why this conflict is difficult to resolve:

Kalshi's own dispute also shows that regulation alone cannot fully solve the trust problem.

On March 5, Kalshi faced a class-action lawsuit where users accused the platform of refusing to pay approximately $54 million in winnings—users had bet that Iran's supreme leader would step down before March 1. The plaintiffs claimed the platform only activated a "death-related exception clause" after the Iranian leader was attacked, using it to refuse payment.

But Kalshi stated that its rules regarding trades on leader deaths were already clear, and it had refunded fees and compensated users for losses, meaning users did not lose money.

This is precisely the contradictory dilemma currently facing investors and policymakers.

Investors hope the industry will achieve growth, expand its reach, and justifiably integrate probability prediction data into the mainstream information system.

Users hope that when event outcomes are controversial and emotionally charged, the platform rules will be stable and credible.

Regulators希望杜绝 (hope to eliminate) these markets turning sensitive state actions into tradable products, avoiding situations where "access to confidential intelligence yields optimal trading returns." Because once these trading prices begin to influence the public information environment, the associated risks evolve into a governance challenge.