By | Caihua She

In the grand narrative of today's global AI race, computing chips are undoubtedly the protagonists. However, outside the spotlight, a more fundamental and critical element is quietly determining the upper limit of AI cluster scale—that element is light.

"You should stand in the light, not just stand there." This wordplay joke, which sparked a frenzy across trillions in market value, reflects a profound industrial reality: the endpoint of AI is not just computing power, but also connectivity.

And in this world of connectivity, two American giants—Marvell (MRVL.US) (hereafter referred to as Marvell) and Broadcom (AVGO.US)—are playing the role of "shovel sellers." They don't manufacture optical modules, but the majority of high-end optical modules are inseparable from them. Understanding them is key to grasping the true situation of China's optical industry.

What is an Optical Module, and Why is AI Development Inseparable from It?

An optical module looks like a small USB flash drive, connecting to server or switch interfaces, with optical fibers attached at both ends. Its core function is the mutual translation between electrical and optical signals.

Servers and GPUs transmit data internally using electrical signals, carried by copper wires or circuit board traces. However, electrical signals have fatal flaws: they become blurry over a few meters, cannot achieve high speeds, and generate significant heat.

Optical fibers transmit data using lasers, with almost no loss, high speeds, and virtually unlimited distance. However, machines cannot recognize optical signals.

This is where the optical module acts as the translator: the transmitting end converts electrical signals into laser light sent into the fiber; the receiving end converts the laser light back into electrical signals for GPU processing. Without optical modules, massive data cannot flow efficiently between numerous GPUs.

Large-scale AI training data centers often contain tens of thousands of GPUs, all requiring real-time exchange of model data, equivalent to tens of thousands of computers computing synchronously and collaboratively. If data transmission cannot keep up, even with powerful GPU computing power, idle computing cycles and data traffic jams will occur, drastically slowing down AI training.

Optical modules are the high-speed transportation network for building computing clusters, enabling:

1) Short-distance interconnection: Transmission between servers and GPUs within the same rack relies on 800G, 1.6T high-speed optical modules to support rapid large model training.

2) Data hall interconnection: Communication between switches in different racks and floors relies on medium to high-speed optical modules.

3) Long-distance transmission: Cross-city, cross-region computing power scheduling relies on long-haul coherent optical modules.

The larger the AI model parameters and cluster scale, the higher the quantity and transmission speed requirements for optical modules. 800G and 1.6T have become standard for overseas AI giants, with future upgrades to 3.2T products. Optical modules are an irreplaceable foundational hardware for AI computing power expansion.

High-speed optical modules internally contain optical devices (lasers, detectors), electrical chips, and supporting passive components. Among these, the DSP (Digital Signal Processor) electrical chip is key to determining whether high-end optical modules like 800G and 1.6T can operate stably.

During high-speed transmission, optical signals traveling long distances through fibers are prone to distortion, noise, and timing offset. DSP chips, with built-in algorithms (such as equalization, clock recovery, forward error correction), can repair signals in real-time, reduce bit error rates, and stabilize bandwidth. It can be said that high-end AI optical modules like 800G and 1.6T cannot function normally without high-performance DSPs. This is the fundamental reason for Marvell and Broadcom's dominant position.

What Kind of Companies are Marvell and Broadcom, and What Role Do They Play in the Supply Chain?

Marvell, whose stock price has risen 263.92% cumulatively this year, holds its core ace as a supplier of DSP chips specifically for optical modules (acquired through the 2021 purchase of Inphi), along with supporting TIA (Transimpedance Amplifier) chips and silicon photonics supporting chips. It provides optical module manufacturers with a complete set of supporting electrical chip solutions. Additionally, it produces Ethernet PHY chips, 5G base station communication chips, etc., covering the data center and carrier communications sectors. NVIDIA (NVDA.US) officially promotes Marvell's DSP solutions for its AI servers. Over 70% of high-end optical modules exported from China carry its chips, with Zhongji Innolight (300308.SZ) being one of its major global customers.

Broadcom, with a market capitalization of $1.87 trillion, is a top global networking chip giant, ranking first in switch chip market share, and also develops optical DSP chips. Its chips emphasize low power consumption advantages, favored by North American cloud vendors like Google (GOOG.US), Microsoft (MSFT.US), and Meta (META.US). It is the only DSP supplier that can compete with Marvell in the market (Credo and MaxLinear hold small shares but have smaller scale). Some overseas orders from domestic manufacturers like Eoptolink (300502.SZ) use Broadcom DSPs.

In the 800G/1.6T high-speed PAM4 DSP market for AI computing, the global market is highly concentrated. According to data from LightCounting, Cignal AI, and other research institutions, Marvell's market share is likely over 60%, Broadcom may have 20-30%, with the two combined holding over 90% of the high-end market. The remaining share is divided among Credo, MaxLinear, and others. Coherent DSPs (for long-distance transmission) are also dominated by Marvell and Broadcom, potentially holding a combined 90% of the high-end market.

In other words, for domestic factories to produce high-end optical modules for North American AI giants, currently only Marvell and Broadcom offer mature chip options. The supply is completely controlled by U.S. companies, but both Broadcom and Marvell are subject to U.S. export control regulations.

The Binding Relationship Between Marvell/Broadcom and Chinese Optical Module Companies: Could It Be a Constraint?

Zhongji Innolight and Eoptolink, already listed on the A-share market with plans for a Hong Kong listing, are the world's top two optical module assembly factories. According to LightCounting's 2025 data, among the top ten global optical module manufacturers, six are Chinese companies, as shown in the figure below. Besides Zhongji Innolight and Eoptolink, these include Accelink Technology (002281.SZ), Hisense Group's Navetek (which has filed for a Hong Kong listing), HG Genuine, and Cambridge Industries (06166.HK). China is the world's largest optical module production base.

If we compare Zhongji Innolight and Eoptolink to vehicle assembly plants, then Marvell and Broadcom are factories that only manufacture high-end engines. The assembly plants cannot produce high-end engines that meet overseas customer specifications themselves and must rely on long-term bulk purchases of DSP chips from these two American companies, combining them with domestic optical components and casings to assemble complete optical modules for sale.

Overseas cloud vendors have strict procurement standards and recognize Marvell and Broadcom chip solutions. Domestic DSPs have not yet passed the 1-2 year complete system validation by overseas customers and cannot be used in large quantities for export orders to overseas markets. Leading domestic optical module manufacturers have limited autonomy to independently switch upstream chips.

The relationship is more than simple buying and selling; it involves joint R&D for new products: Marvell provides new chips to Zhongji Innolight first for debugging and adaptation; Broadcom and Eoptolink collaborate to optimize low-power products, deeply integrated into NVIDIA's overseas computing ecosystem.

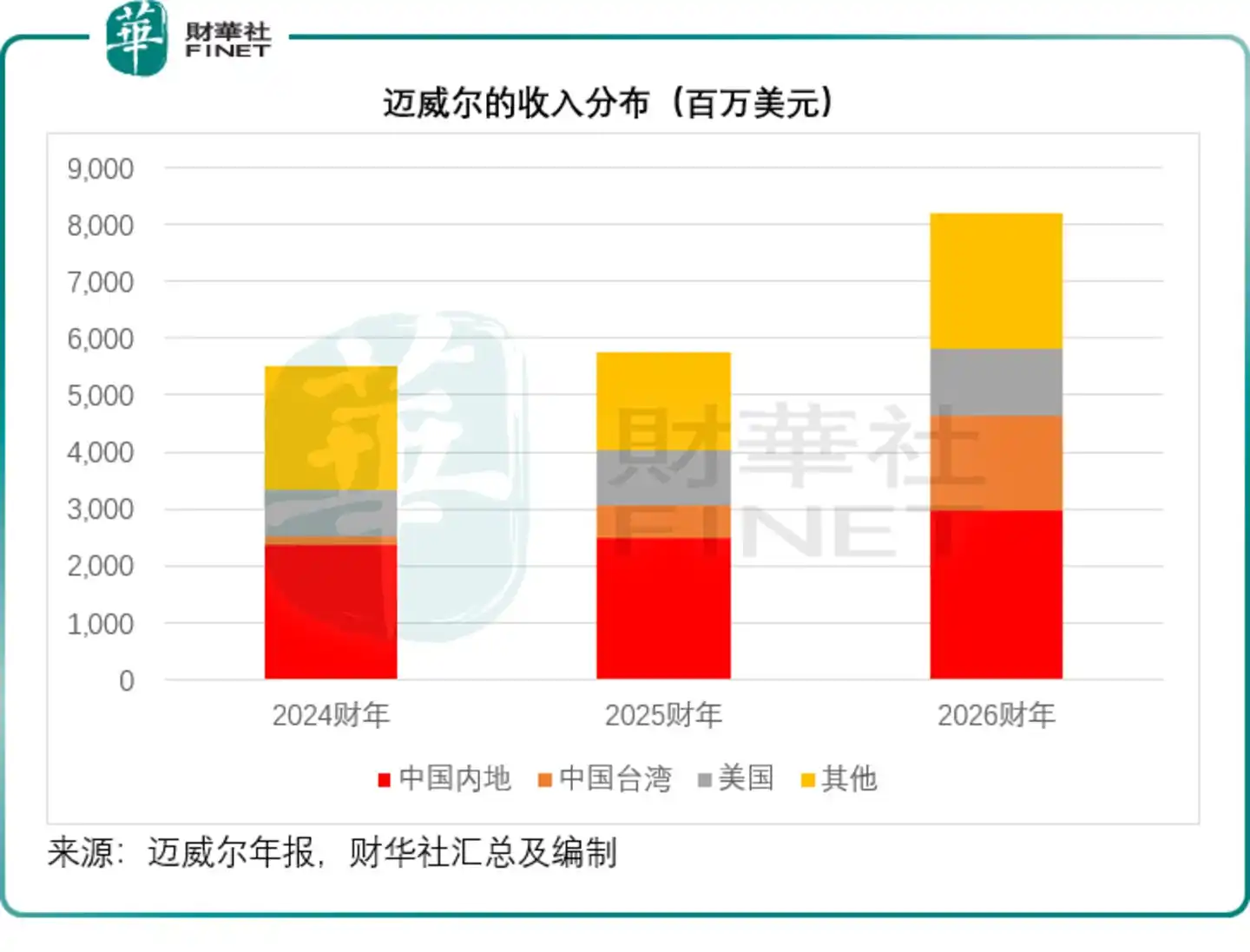

From Marvell's annual report for the fiscal year ended January 2026, we can see that the Greater China market, including Taiwan, accounts for approximately 56% of its total revenue.

Although we rely on their chips, Marvell and Broadcom cannot completely detach from the Chinese market either.

First, over half of Marvell's optical chip revenue comes from Chinese optical module manufacturers. As shown in the figure above, mainland China accounts for about 36% of Marvell's total revenue, and Greater China (including Taiwan) accounts for about 56%. China is the world's largest optical module production base. A complete cutoff would mean voluntarily abandoning the largest incremental market for AI, leading to huge losses.

Second, the packaging of Marvell's high-end DSP chips and many optical components require support from domestic companies. Companies like JCET (600584.SH) handle chip packaging and testing, while TFC Optical Communication (300394.SZ), SICC (688498.SH), etc., supply optical devices. Severing ties with the domestic supply chain would directly limit the production capacity of American chips.

Third, although Marvell and Broadcom are American companies, their products heavily rely on foundries like TSMC (which are not American), making the supply chain inherently global. This adds complexity to a complete supply cutoff.

Why is the Potential Supply Restriction Risk for Optical Chip Manufacturers Relatively Lower Than for DSPs?

Besides DSP electrical chips, another expensive component in the optical module cost structure is the high-speed EML laser chip. This is also controlled by Japanese and American companies like Lumentum (LITE.US), Coherent (COHR.US), Broadcom, Sumitomo Electric, and Mitsubishi Electric.

If DSP is the "computing brain" of the optical module, then Lumentum works on the "light-emitting heart," responsible for generating high-speed laser signals. It is another core component enabling ultra-high-speed transmission in optical modules.

In current AI 800G, 1.6T high-end optical modules, single-channel 100G, 200G high-speed EML laser chips are indispensable core devices. This high-end specification is currently highly dependent on overseas suppliers like Lumentum, with Lumentum potentially holding over 40% market share for 200G EML.

Domestic optical chip companies can currently stably mass-produce 10G and 25G medium-low-speed optical chips. Domestic production rates are approximately 60% for the former and 70% for the latter, basically meeting the needs of ordinary data centers and operator access networks. However, mass-production capability for 200G ultra-high-speed EML chips is still under development and has not yet reached scale.

Leading overseas manufacturers have long completed technological iterations and secured long-term capacity in advance. Notably, the EML chip market is generally in short supply. Lumentum's 2026 capacity is reportedly locked down by 70% for customers like NVIDIA and Google, with orders scheduled into 2027. This means that even with multiple supplier options, global high-end EML capacity remains tight in the short term, and domestic optical module manufacturers still face challenges in obtaining sufficient supply. North American AI giants like NVIDIA further exacerbate supply pressure for domestic high-end optical modules by strategically investing and signing long-term agreements to lock in Lumentum's capacity.

However, compared to Marvell and Broadcom's DSP situation, the "chokepoint" for optical chips, while severe, is more manageable. The high-end DSP market is an absolute duopoly with almost no viable second-tier options. In contrast, the high-speed optical chip sector features competition among multiple overseas vendors. Besides Lumentum, there are several mature suppliers like Sumitomo Electric and Broadcom, allowing domestic optical module manufacturers more flexibility in switching sources. Additionally, companies like Lumentum are component manufacturers; they do not control system-level certification ecosystems. Overseas cloud vendors do not individually specify their optical chip solutions. Compared to the DSP market, which is tightly locked by ecosystem bindings, there is greater autonomy in the supply chain.

More importantly, the progress of domestic substitution in this field is far ahead of that for high-end DSPs. Leading domestic companies like SICC, Everbright Photonics (688048.SH), and Accelink Technology have achieved commercial deployment of 100G EML chips at different scales. 200G high-speed optical chips have also completed sample testing and entered customer validation stages, expected to gradually achieve scale within the next one to two years, potentially quickly buffering potential supply risks from overseas vendors.

In contrast, 1.6T high-speed DSP chips may require years of certification and iteration before entering overseas high-end supply chains. The breakthrough timelines for the two likely differ significantly.

In summary, although the global industrial chain is interdependent, we must remain vigilant about the potential risk of supply cuts.

Reflection: How Can the Domestic Industry Chain Address Potential Supply Cutoff Risks?

1) Short-term Hedging: Diversify supply chains, secure long-term agreements, and protect existing overseas business.

Leading optical module manufacturers can sign long-term supply agreements with both Marvell and Broadcom to diversify single-supplier risk. Prepay to lock in chip production capacity, extend inventory cycles to cope with short-term chip supply tightening.

Simultaneously, expand into markets in Southeast Asia, the Middle East, and the domestic computing power market to reduce reliance on single North American customers and balance the business structure.

2) Domestic Market Closed Loop: Promote large-scale adoption of domestic chips to ensure domestic computing power security.

Domestic smart computing centers and operator projects can prioritize the large-scale adoption of domestic optical chips and DSPs, giving preference to purchasing self-developed chips from domestic manufacturers, including vendors like Chengke Micro, Huawei HiSilicon, ZTE Microelectronics, Accelink Technology, and Yutai Micro.

The domestic market is gradually forming an independent and complete industrial chain closed loop. Even if overseas high-end chips face temporary supply cuts, domestic demand for most large model training, government computing power, and communication broadband services could still be met using domestic DSPs. However, it must be acknowledged that in extreme performance and power-sensitive high-end AI training scenarios, a certain performance gap remains between domestic DSPs and overseas solutions.

3) Mid-to-Long Term Core Breakthrough: Accelerate complete domestic substitution for high-speed DSPs.

This is the fundamental solution to the chokepoint problem, requiring simultaneous efforts across multiple technological paths:

Market-driven chip companies (e.g., Chengke Micro): Continuously iterate 800G, 1.6T PAM4 DSPs, accelerate joint debugging with domestic optical module factories, first fully cover the domestic market, then gradually progress to certification with small and medium overseas customers.

Equipment manufacturer self-developed chips (Huawei HiSilicon, ZTE Microelectronics): Develop high-speed DSPs internally to support their own optical modules and servers, forming a self-sufficient ecosystem.

Government-enterprise joint support: Increase subsidies for domestic chip tape-outs, testing, and R&D through industrial funds and computing power procurement policies to shorten product validation cycles (this may require sustained capital and policy support).

Synchronized breakthroughs in supporting industries: Simultaneously tackle 200G high-speed light-emitting chips and advanced chip packaging/testing processes to fill upstream gaps.

4) Frontier Technologies to Reduce Dependence: Develop silicon photonics and CPO new technologies to reduce reliance on single, high-value DSP chips.

Traditional discrete optical modules heavily rely on standalone DSP chips. New technologies like Co-Packaged Optics (CPO) and silicon photonic integration can combine optical and electrical circuits, reducing the need for high-end standalone DSPs.

Domestic companies like Huagong Tech, Zhongji Innolight, and SICC are all investing in silicon photonics and CPO R&D. By pursuing new technology paths, they aim to change the current chip dependency landscape and reduce external chip constraints from the ground up. However, it should be noted that CPO and silicon photonics technologies are still in the early stages of industrialization, far from large-scale commercial use. They represent a mid-to-long-term direction and are unlikely to change the dependence on high-end DSPs in the short term.

5) Countermeasure Potential from the Application Side.

China is one of the world's largest optical module markets and the largest builder of AI computing power. If upstream high-end chips are restricted, the focus could shift to the domestic market, prioritizing support for domestic substitute products. Simultaneously, countermeasures against related products could be implemented. This serves both as a tactical countermeasure tool and strategically buys development time and market space for the domestic optical chip industry.

Conclusion

Looking at the entire industry chain, Marvell and Broadcom indeed hold the core lifeline for domestic optical module exports to overseas AI markets and possess the capability to restrict our overseas high-end business in phases.

Our greatest safety buffer may lie in our complete and autonomous mid-stream manufacturing capabilities (optical modules, optical fibers, and cables) and our sizable domestic computing power and communications market.

The long-term solution to mitigate supply cutoff risks lies not in passive gamesmanship with American companies, but in continuously advancing the domestic R&D and large-scale production of high-speed DSPs and high-end optical chips. In the short term, rely on dual suppliers and diversified markets to hedge risks. In the mid-to-long term, rely on domestic chips and cutting-edge new technologies to achieve industrial breakthroughs, truly mastering the initiative in the development of the optical industry chain.

It is important to note that each step for domestic DSPs—from small batches to mass production, from domestic certification to overseas adoption—faces multiple hurdles: technological, capital, time, and ecosystem barriers. It is by no means an overnight task. The industry and policymakers must maintain strategic patience and continue investment. Only then can we gradually narrow the gap with overseas giants over the next three to five years.