On Wall Street's monitors, the flames of the digital oracle burn ever brighter.

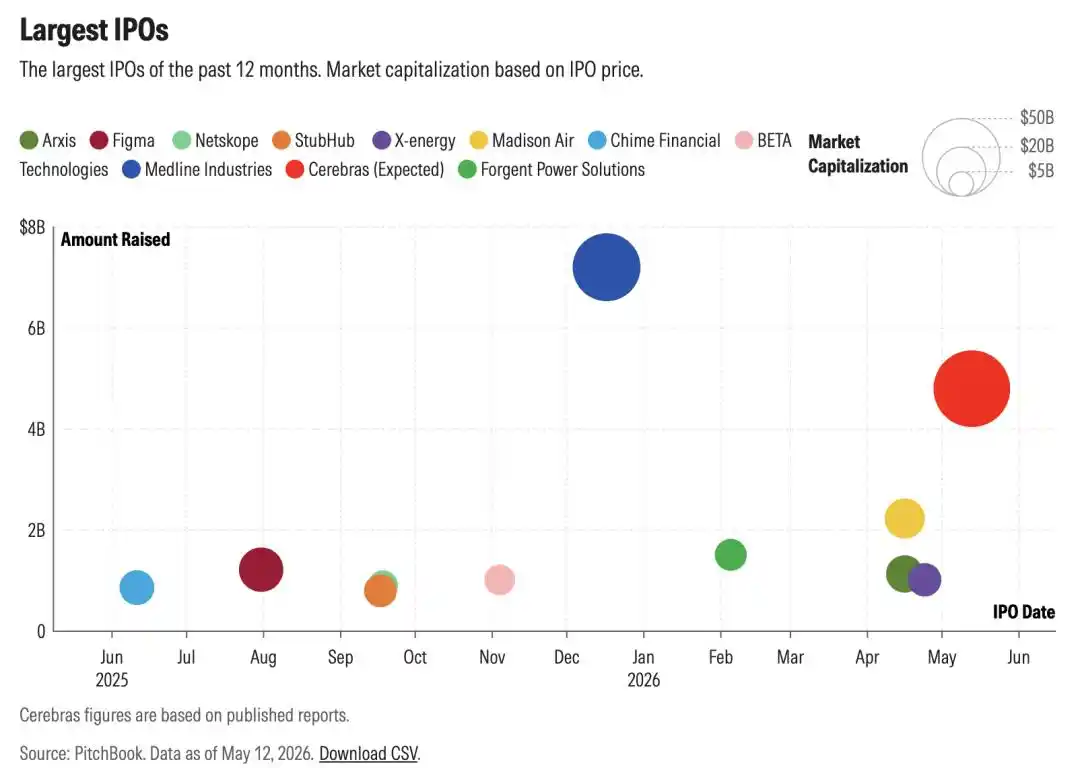

This week, the chip industry's 'maverick', Cerebras Systems, charged towards an IPO with a valuation of $48 billion—

This is the largest listing of 2026, a commercial ritual imbued with both sanctity and brutality.

To squeeze into Sam Altman's 'Hall of Gods', Cerebras personally cut away 10% of its own 'flesh and blood'—stock warrants worth approximately $5 billion.

This is no longer a simple IPO. It is a tribute from underlying hardware to model sovereignty, paid in the twilight of an era.

And standing behind all this prosperity is the man known as the 'new lord of Silicon Valley'.

The Return of Brutalist Aesthetics

It Forged a 'Silicon-based Leviathan'

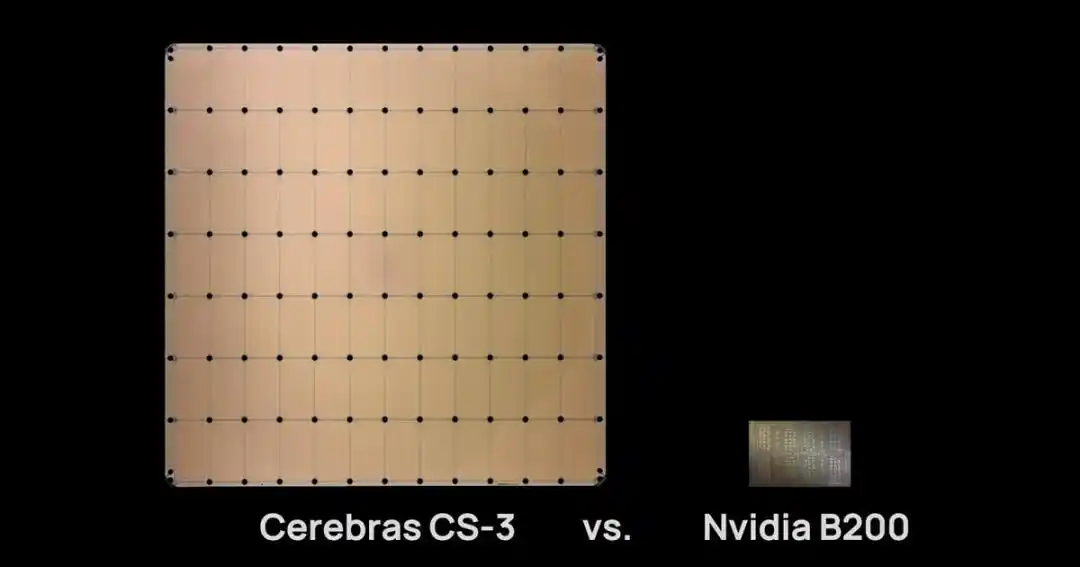

If Nvidia proudly calls its B200 chip an exquisite postage stamp, then Cerebras's flagship product, WSE-3, is a massive dinner plate.

For the past three decades, the semiconductor industry's creed has been 'miniaturization'—dancing on a pinhead, stacking transistors at the nanoscale.

But Cerebras took a counterintuitive path: Since memory bandwidth is the Achilles' heel of AI inference, why not just make the entire wafer into a single chip.

This 'silicon-based leviathan' is nearly half a square foot in size, featuring over 4 trillion transistors (19 times that of Nvidia's B200), 900,000 AI-optimized cores, and 125 petaflops of AI compute—making its total computing power 28 times that of the B200.

Its design is fundamentally about 'trading space for time': etching cores directly onto a single 12-inch wafer, flattening the 'memory wall' where data shuttles between the chip and external storage.

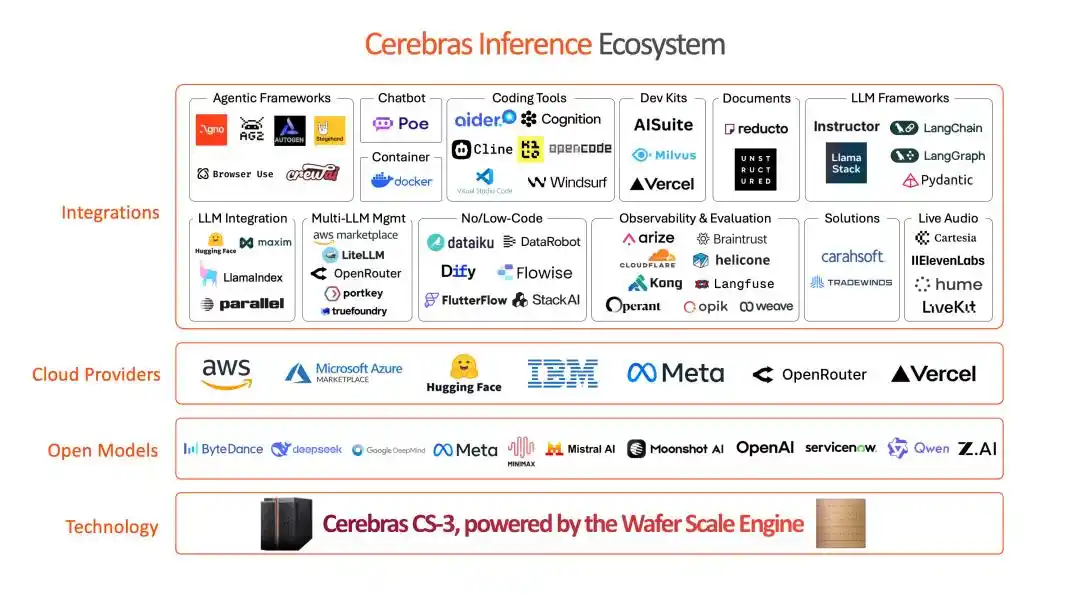

This brutalist aesthetic shows terrifying dominance in the 'Age of Inference':

When running top-tier models from OpenAI, Cognition, Meta, etc., it can achieve a throughput speed of up to 3000 tokens per second, outpacing traditional GPUs by 70 times.

However, in 2026, the hardest technology, if it can't be converted into the fastest Tokens, is just expensive sand.

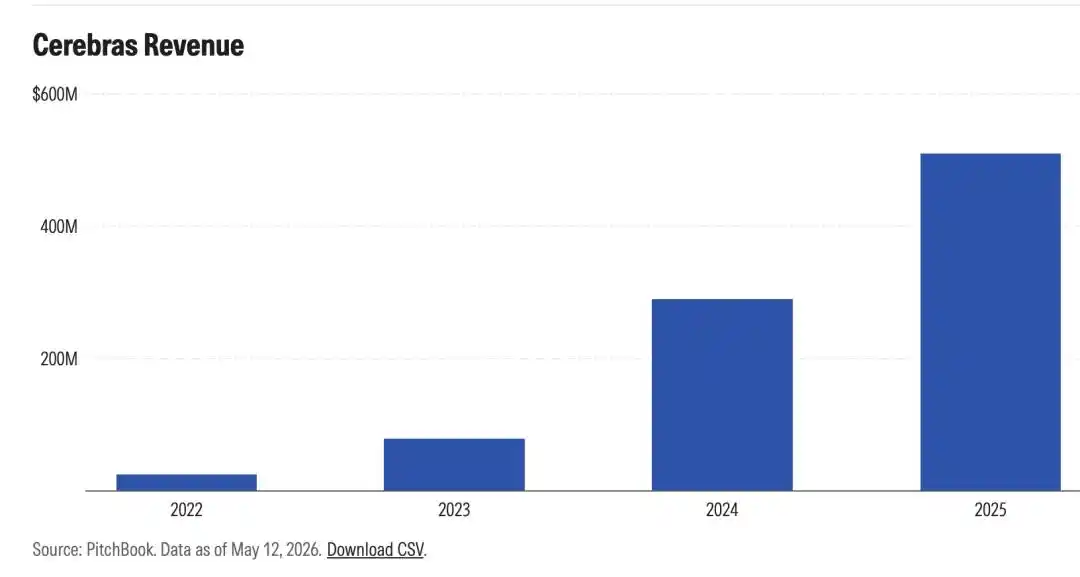

Eighteen months ago, Cerebras was a forlorn geek.

In 2025, its revenue was only $510 million, almost entirely from a single customer, the UAE's G42. It operated at a loss of $145.9 million, forcing the postponement of its IPO plans.

Despite possessing performance surpassing Nvidia's, its fate hung on the checkbook of a single client, like an orphan at constant risk of drowning.

Until it knocked on the door leading to Sam Altman's inner circle.

The $5 Billion 'Redemption Bond'

The Golden Ticket to the Future

In the world of AI, Moore's Law is giving way to the 'Law of the Circle'.

In exchange for survival and explosive growth, Cerebras signed an agreement that left outsiders dumbfounded: providing OpenAI with 750 megawatts of computing capacity over the next three years.

Calculated at current market prices (750 MW is roughly worth $9 billion annually), this deal could bring about $27 billion in revenue and $10 billion in gross profit.

For a company still in the red last year, this was a lifeline.

More tellingly, these 750 megawatts constitute just one-fortieth of the total computing power OpenAI believes it will need by 2030. This leftover order is enough to catapult Cerebras from a 'marginal player' to a market focal point.

But there is no free lunch, only expensive endorsements.

In exchange, Cerebras must gradually grant stock warrants to OpenAI. Upon exercise, OpenAI would hold 10% of Cerebras's shares—worth about $5 billion at the offering price midpoint of $155.

This means Cerebras generously offered up half the potential future profits from this mega-deal as a 'tribute' directly to OpenAI.

This is not an equal exchange. This is the AI era's 'computing power redemption bond'.

OpenAI is the 'lord' holding the power to allocate traffic and demand, while Cerebras is a heavily armored knight providing advanced tools of production—to enter the lord's domain, the knight must pay homage and share half his spoils.

Once branded as OpenAI's core blood ally, Cerebras's price-to-sales (P/S) ratio instantly skyrocketed to 15 times, a level even Nvidia must respectfully acknowledge.

'Altmanomics'

He Is Cashing Out the Hardware Giants

Cerebras is not the only computing power enterprise bowing to Sam Altman.

Last October, AMD's stock doubled after reaching a similar agreement with OpenAI; earlier, Nvidia was rumored to have deepened its ties with OpenAI through a $30 billion financing round.

A clear map of power is emerging: OpenAI is evolving from a software company into a global 'tax authority' over the AI hardware landscape.

Sam Altman's true ambition is not merely to acquire data centers for training and running its models, but to quietly expand the group of companies and investors who have a 'vested interest in OpenAI's success.'

He is weaving a vast web of an 'interest community'.

OpenAI doesn't buy chips; it only rents the future—and in the process, binds all players to the same ship.

For hardware vendors: Even with profits halved, obtaining the 'OpenAI certification' and a 15x P/S valuation is a worthwhile deal.

For Sam Altman: He not only secures the computational foundation for the next decade but also becomes a shareholder in all potential competitors.

This is the essence of 'Altmanomics': In the second half of the AI race, whoever defines the demand for models holds the 'power to tax' the underlying supply chain.

Can $48 Billion Buy a Seat at the Power Table?

This Thursday, Cerebras's IPO received 20 times oversubscription. The pricing range was raised to $150-$160 per share, implying a valuation of $48 billion, coinciding with semiconductor stocks rising 53% cumulatively from their March lows.

The capital market's frenzy is almost blind. They no longer care whether Cerebras lost $140 million last year or if its P/S ratio has already surpassed Nvidia's.

They are buying a kind of 'certainty'.

In the uncertain landscape of 2026, what identity tag is more certain than being a 'Core Partner of OpenAI'?

This is precisely the most intriguing aspect of this IPO. Cerebras's high valuation is essentially a market premium for the 'Altman endorsement'.

Conclusion: Sovereignty or Vassalage?

This 2026 listing marks the semiconductor industry's entry into a brutal era of stratification.

Future chip companies have only two paths:

Either, like Nvidia, rely on first-mover advantage to build their own ecological empire and become the rule-maker; or, like Cerebras, offer up half their soul in a high-stakes gamble for a ticket into the core circle.

If you cannot become a god, then become the most expensive offering.

This is not just a technological battle; it's a battle for sovereignty.

In every megawatt of electricity flows the 'tribute' from chipmakers to Silicon Valley's new overlord.

References:

https://x.com/FT/status/2054141078710768006

https://www.ft.com/content/3f77f8ad-16b8-4f97-ae55-0bd2e31122fa?syn-25a6b1a6=1

https://www.theinformation.com/newsletters/ai-agenda/startup-helping-openai-optimize-ai-cerebras-chips

https://www.morningstar.com/stocks/why-ai-chip-designer-cerebras-is-2026s-hottest-ipo-yet

This article is from the WeChat public account "Xin Zhi Yuan," author: Xin Zhi Yuan, editor: KingHZ