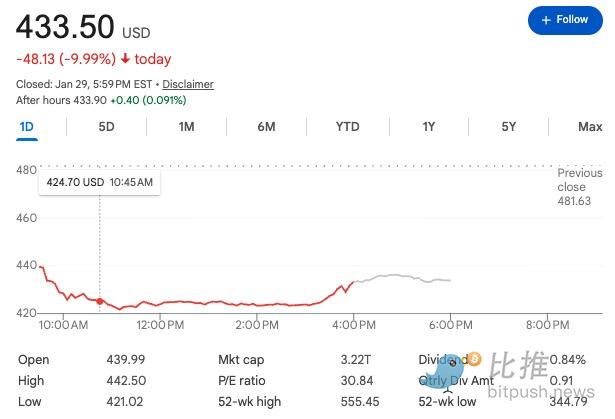

After releasing an earnings report that exceeded market expectations, Microsoft(Microsoft) encountered its most severe market sell-off of the year.

On Thursday, the software giant Microsoft plunged 7% in pre-market trading, losing $357 billion in market value in a single day—a figure equivalent to an entire Coca-Cola company vanishing from the Earth. And just on the same day, Microsoft had delivered a near-perfect report card: profits surged by nearly a quarter, and revenue hit a record high.

Profits were rising, but the stock price crashed. Behind Wall Street's vote with its feet lies an unspoken fear: the more the AI account is calculated, the more alarming it becomes. Has the growth story reached its end? When all the giants are crowding onto the same track, who can truly make money?

A Beautiful "Facade" and a Cracked "Foundation"

From the top line of the financial statements, Microsoft's performance was robust:

-

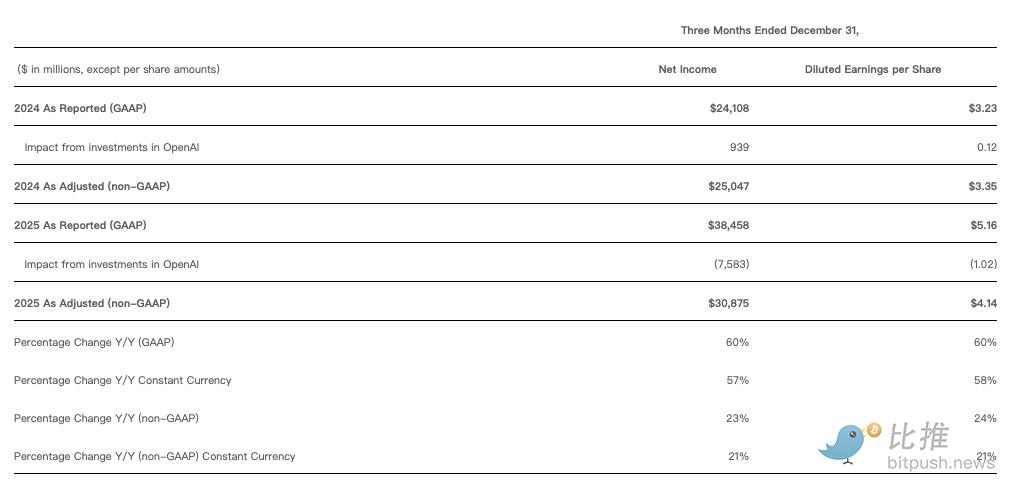

Net Profit: Adjusted net profit grew 23% to $30.9 billion, higher than the analyst expectation of $28.9 billion.

-

Revenue: Increased 17% to $81.3 billion, also exceeding the expected $80.3 billion.

-

Cloud Business: Quarterly revenue surpassed $50 billion for the first time.

However, the market's attention quickly focused on two details: the growth pace of Azure and the expansion rate of capital expenditures.

The earnings report showed that Azure's year-over-year growth rate was 38%, still strong but down one percentage point from the previous quarter's 39%.

Against the backdrop of historically high valuations, this 1% deceleration was seen as a signal of "peak growth." Barclays analysts bluntly stated: "Even though the numbers are healthy overall, buy-side investors clearly wanted to see more."

Microsoft as a "Hardware Laborer"?

In this AI gold rush, although Microsoft is a frontrunner, it resembles more of a "high-end OEM."

Behind the astronomical investments lies extremely brutal hardware premium pressure. According to the latest industry report from TrendForce as of January 2026, HBM (High Bandwidth Memory), the core配套 for NVIDIA's B200 series, is experiencing an unprecedented "capacity hijacking."

Data monitoring shows that as Micron and SK Hynix's HBM orders are generally booked until early 2027, the average selling price of HBM chips has risen against the trend by about 30% over the past two quarters. For Microsoft, this is tantamount to "structural extortion." To ensure Azure AI's computing power doesn't fall behind, Microsoft must accept a premium of thousands of dollars per chip.

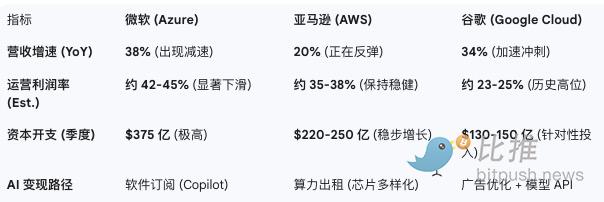

Horizontal Comparison of Cloud Giants' Core Data (2025 Q4 – 2026 Q1)

What does this mean?

The hundreds of billions of dollars Microsoft invests each quarter mostly flow to upstream hardware suppliers. This means the money Microsoft earns hasn't even warmed up on the books before being handed over to NVIDIA for GPUs and to Micron for memory. Although Microsoft is also developing its own Maia chips, it remains highly dependent on external procurement. The result is brutal: the gross margin of Microsoft's cloud business has slipped from above 70% to around 67%.

In contrast, Amazon AWS, with its early布局 of self-developed chips (Trainium series), has reduced its reliance on expensive hardware, and its operating margin remains solid at 38%. And while Meta is also investing heavily, its stock price反而 surged 10% because AI directly improved ad conversion rates, showing "receipts." Comparatively, Microsoft seems more like it's "working for hardware manufacturers."

This "bleeding" investment not only failed to satisfy the market's appetite but also triggered a unique computing power "internal consumption" for Microsoft. Due to supply constraints, Microsoft faces a brutal balance: should it lease the top-tier computing power to external cloud customers for immediate profit, or reserve it for its own Copilot to bet on the ecosystem's future? Microsoft chose the latter. This strategy of "sacrificing external for internal" stabilized the user experience but severely diluted Azure's profitability as a pure cloud platform in the short term.

Concentration Anxiety: The "Single-Point Dependency" Crisis with OpenAI

In this earnings report, Microsoft disclosed a startling figure for the first time: about 45% of its $625 billion future cloud contract book value comes from OpenAI.

This means Microsoft's cloud growth is highly tied to a single startup. Although CFO Amy Hood emphasized that another $350 billion comes from other industry customers, investors still worry: if OpenAI falters in competition or shifts to its own hardware in the future, Microsoft's massive, costly system will face serious "idle risk."

The Erosion of the Moat: Open Source and Low-Cost Disruption

Furthermore, the strong tie with OpenAI is facing a "cost-effectiveness revolution" disrupting from a lower dimension.

With the rise of low-cost or open-source models like China's DeepSeek, the "price war" in the AI market has already begun. When enterprise clients find that open-source models costing a few cents can solve 90% of their problems, Microsoft's high-premium Copilot subscription fee model is facing challenges.

This business model uncertainty makes Microsoft's high P/E ratio seem precarious. If Microsoft cannot prove that its high computing costs can translate into equally high premium revenue, the moat it built might be quietly leveled by the open-source wave.

Facing the stock decline, Nadella remains resolute. He极力推销 his "full-stack AI" vision on the analyst call: "When you think about our capital expenditure, don't just think about Azure, think about Copilot. We don't want to maximize just one business; we want to allocate capacity to build the best portfolio."

Conclusion

Despite the panic selling, the giant is stabilizing its position through a series of complex capital maneuvers.

Microsoft disclosed an $7.6 billion accounting gain this quarter, entirely thanks to its early investment in OpenAI. As OpenAI reorganized from a non-profit to a traditional for-profit entity in October, its balance sheet膨胀ed dramatically with multiple rounds of huge financing. Currently, Microsoft holds a 27% stake in this AI leader. With OpenAI seeking a new round of financing at a valuation exceeding $750 billion, Microsoft's initial investment of $14 billion has yielded惊人的 paper returns.

This左脚踩右脚的 "ecosystem flywheel" is becoming increasingly complex: competitor Anthropic just committed to buying $30 billion worth of Azure computing power in the future, and Microsoft随即 plans to inject $5 billion into it. In this potential deal, the startup's valuation has been pushed to $350 billion.

In summary, the $357 billion evaporated market value is a market correction of Microsoft's "heavy capital, slow monetization" model. Although the paper investment gains are极其丰厚, what Wall Street truly cares about is not how much valuation premium Microsoft earns as a "VC firm," but whether its core cloud business can truly recoup real money from global enterprises under the erosion of hardware costs.

The AI industry at this moment is like a high-speed train: once the infrastructure is laid, it's hard to stop. Whether it can maintain speed while gradually achieving commercial闭环 willdetermine the market pricing logic for the next phase.

Author: Bootly

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush