Автор: CoinGecko

Компиляция: Deep Tide TechFlow

Введение: Ключевые данные годового отчета CoinGecko достаточно красноречивы: годовой объем торгов DEX-перпетуальными контрактами вырос на 346% по сравнению с предыдущим годом, в то время как открытый интерес на CEX за тот же период упал на 20,8%. Капитал систематически перемещается из централизованных платформ в децентрализованные.

Эта статья не просто перечисляет цифры; она четко объясняет, почему происходит эта миграция, как Hyperliquid смог обогнать Coinbase International и во что превращаются эти платформы после HIP-3.

Полный текст:

В 2025 году биржи перпетуальных контрактов, особенно децентрализованные платформы, пережили взрывной рост, достигнув общего объема торгов в 929 триллионов долларов (рост на 64,6% в годовом исчислении), что фундаментально сместило крипторынок с торговли спотом в сторону механизма ценового обнаружения, основанного на деривативах.

Ключевые моменты:

- Объем торгов DEX perps вырос на 346%, достигнув 6,7 трлн долларов; в то же время открытый интерес на CEX упал на 20,8%. Это представляет собой массовую миграцию капитала с централизованной на децентрализованную инфраструктуру, движимую такими платформами, как Hyperliquid (седьмое место в мировом рейтинге, объем торгов 2,9 трлн долларов).

- Капитальная эффективность стимулировала внедрение: Perps позволяют трейдерам получать экспозицию с кредитным плечом при меньшем объеме средств, получать прибыль в обоих направлениях (что было критически важно во время падения рынка в четвертом квартале 2025 года) и избегать трения, связанного с физической поставкой.

- HIP-3 реализовал возможность бессрочного листинга любого актива с источником цены, превращая такие платформы, как Hyperliquid, из «криптобирж» в глобальную финансовую инфраструктуру, работающую 24/7, где можно торговать всем: от товаров до акций Pre-IPO.

Почему Perps растут быстрее, чем спот-торговля

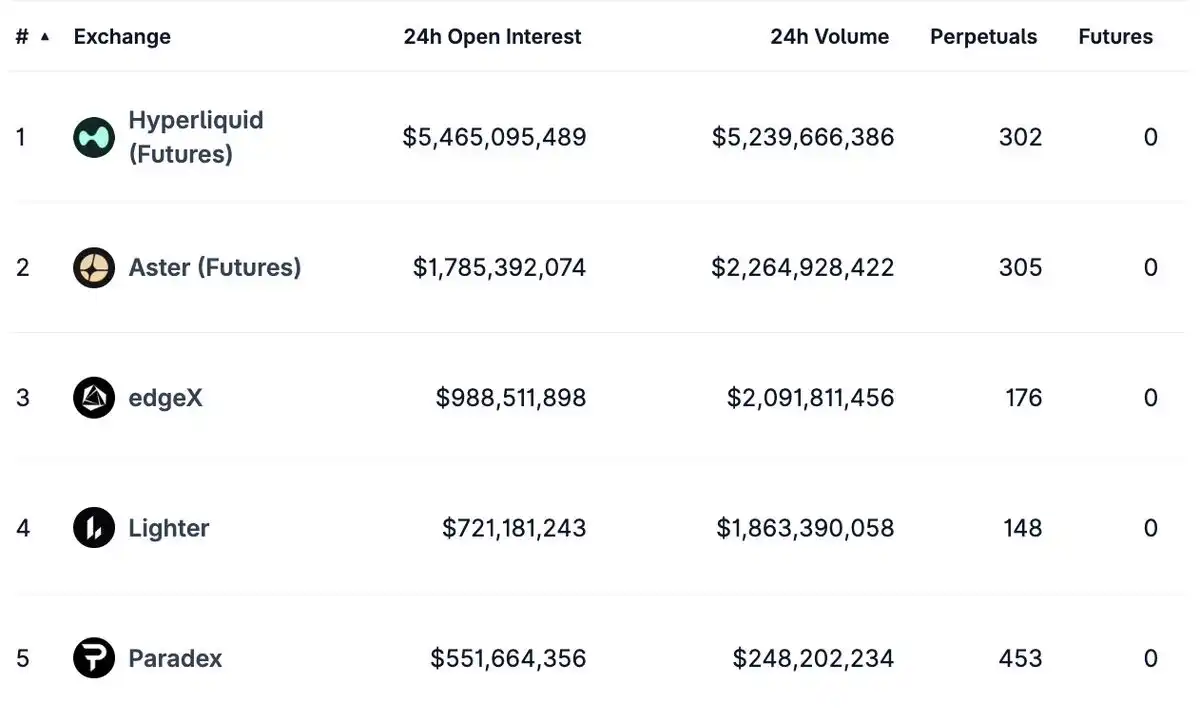

Рис.: Топ-5 децентрализованных бирж перпетуальных контрактов по 24-часовому объему торгов на CoinGecko по состоянию на 2 марта 2026 г.

Капитальная эффективность: делать больше с меньшими средствами

Фундаментальное преимущество перпетуальных контрактов заключается в капитальной эффективности. На спотовом рынке для покупки биткоина на 10 000 долларов требуется 10 000 долларов капитала, который блокируется на время удержания. На перпетуальном рынке с помощью кредитного плеча можно получить такую же экспозицию за небольшую часть средств, высвобождая ликвидность для других позиций или стратегий.

Помимо спекуляций, перпетуальные контракты также позволяют участникам рынка:

Хеджировать существующие позиции без продажи базового актива (и, следовательно, без запуска налогового события); Арбитражировать спреды между торговыми площадками; Выражать направленные взгляды без трения, связанного с физической поставкой; Одновременно развертывать капитал в нескольких возможностях.

Каждый доллар на перпетуальном рынке работает больше, чем доллар на споте. Для трейдеров, фондов и институтов, оптимизирующих отдачу на капитал, чаша весов склоняется в сторону perps.

Зрелость рынка: по стопам традиционных финансов

Взрывной рост криптодеривативов является отражением закономерности, через которую проходит каждый зрелый финансовый рынок. В традиционных финансах рынок деривативов по объему намного превосходит базовый спотовый рынок, часто в 10–50 раз. Например, рынок процентных свопов имеет номинальную стоимость более 400 трлн долларов, в то время как мировой рынок облигаций оценивается примерно в 130 трлн долларов.

Крипторынок просто догоняет. По мере созревания рынка и притока более опытных участников соотношение объемов деривативов и спота продолжает расширяться. Только десять крупнейших бирж обеспечили объем торгов перпетуальными контрактами в размере 929 трлн долларов, что намного превышает общий объем спотовой торговли на всех криптобиржах.

Фактор хеджирования: устойчивость во время падения

Возможно, самое убедительное доказательство ценности перпетуальных контрактов появилось во время падения рынка в четвертом квартале 2025 года. В то время как спотовый рынок сокращался, а настроения инвесторов ухудшались, объем торгов на десяти крупнейших биржах перпетуальных контрактов вырос на 64,6% в годовом исчислении.

Почему? Потому что перпетуальные контракты позволяют трейдерам получать прибыль в обоих направлениях. Когда цены падают, короткие позиции приносят значительную прибыль, а хеджевая активность усиливается. Способность рынка выражать медвежьи взгляды позволяет капиталу оставаться активным, объемы торгов — высокими, даже если спотовый спрос иссяк.

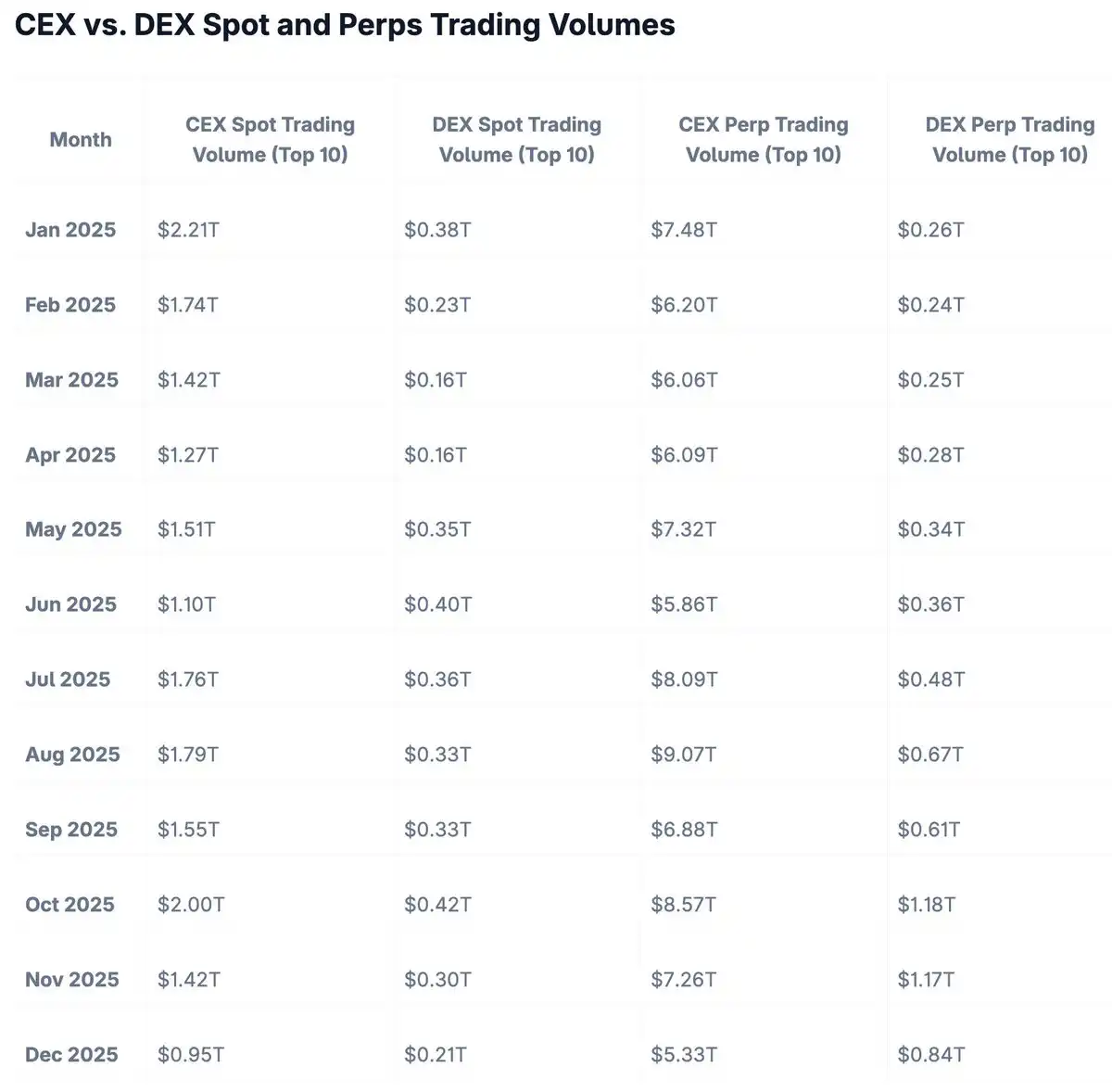

На традиционных чисто спотовых рынках падение цен означает снижение активности. Это видно по падению объема спотовых торгов на CEX с 2,21 трлн долларов в январе 2025 года до минимума в 0,95 трлн долларов в декабре.

Однако на перпетуальном рынке волатильность в любом направлении означает возможность. Данные за 2025 год доказывают, что эта динамика фундаментально изменила структуру крипторынка.

Рис.: Сравнение объемов спотовой торговли и торговли перпетуальными контрактами на CEX и DEX

Великая миграция: DEX против CEX

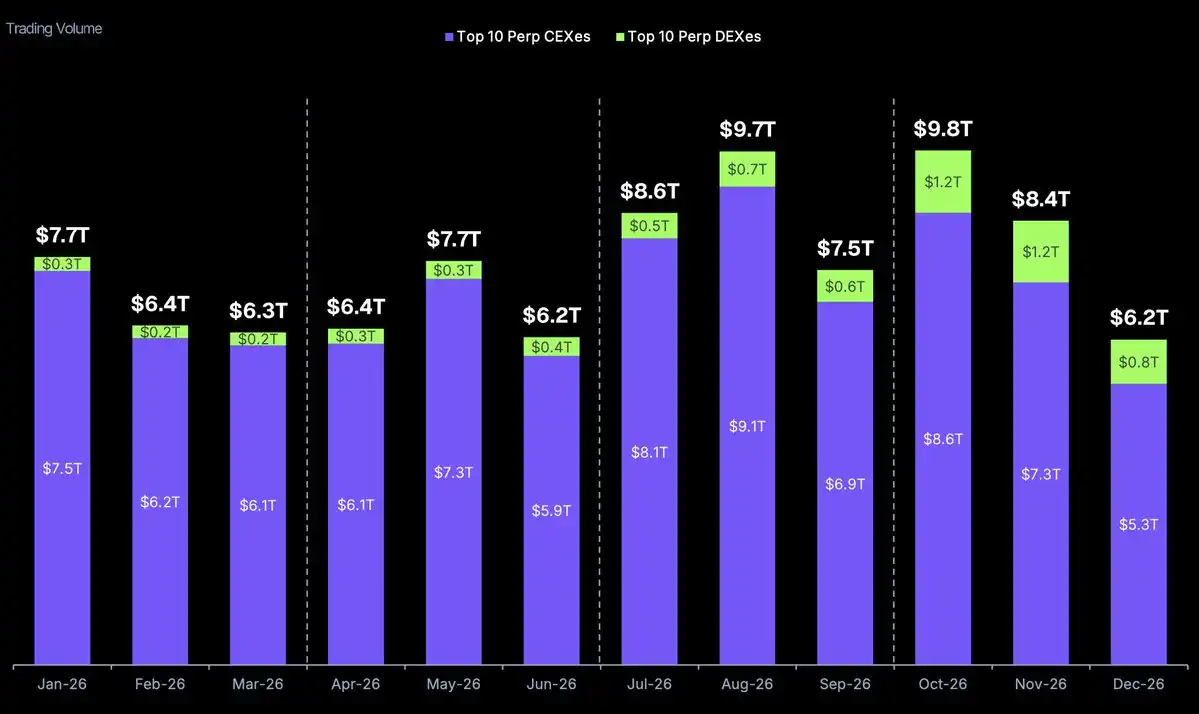

Рис.: Объемы торгов Perp CEX и Perp DEX из топ-10

Источник: CoinGecko Crypto Industry Annual Report 2025

Хотя централизованные биржи по-прежнему доминируют по абсолютным размерам, настоящей историей 2025 года стал стремительный взлет децентрализованных бирж перпетуальных контрактов. Объем торгов Perp DEX резко вырос на 346%, достигнув рекордных 6,7 трлн долларов за год.

Для наглядности этого скачка: только в пиковый месяц октября 2025 года Perp DEX обработали объем торгов в 1,18 трлн долларов, что более чем в четыре раза превышает показатель января 2025 года.

Прорыв DEX

К 2025 году Perp DEX решили фундаментальные проблемы удобства использования, которые ранее удерживали пользователей на централизованных платформах:

- Паритет пользовательского опыта: Нарратив о том, что «DEX неудобны в использовании», закончился в 2025 году. Hyperliquid и Lighter предложили интерфейсы, практически неотличимые от Binance или Coinbase. Глубина стакана заявок достаточна, исполнение почти мгновенное, и обычный трейдер уже не чувствует, что использует децентрализованную платформу.

- Конкурентная структура комиссий: Ранние DEX брали надбавку за децентрализацию. К 2025 году конкуренция и технологический прогресс снизили комиссии Perp DEX до уровня CEX или даже ниже. Такие платформы, как Hyperliquid, даже начали предлагать кэшбэк тейкерам до 90%, что сравнимо с самыми конкурентными тарифными структурами CEX.

- Масштабируемая производительность: Ранние DEX на основе блокчейна не могли обрабатывать объемы, необходимые для серьезной торговли деривативами. Появление специализированных блокчейнов Layer 1 и оптимизированных роллапов решило эту проблему. Например, собственный L1 Hyperliquid может обрабатывать тысячи транзакций в секунду с временем подтверждения менее секунды — производительность, сопоставимая с централизованной инфраструктурой.

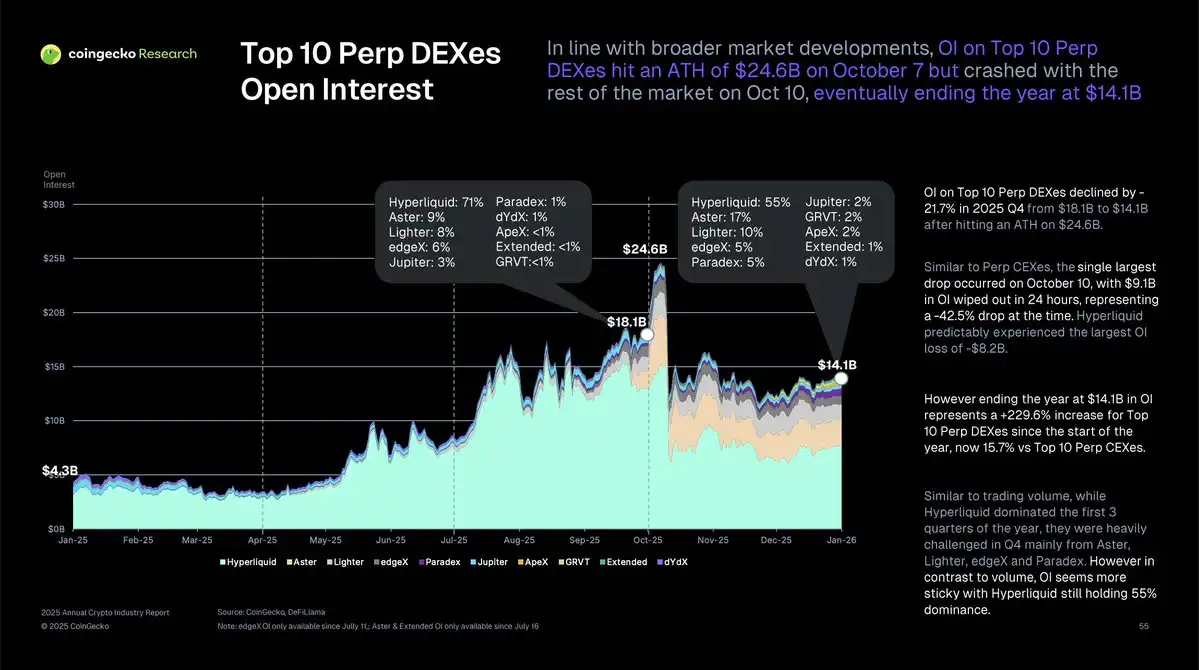

Расхождение в открытом интересе

Согласно Ежегодному отчету CoinGecko о криптоиндустрии за 2025 год, открытый интерес на CEX в 2025 году снизился на 20,8%, в то время как открытый интерес на DEX резко вырос на 229,6%.

Открытый интерес — общая стоимость непогашенных деривативных контрактов — представляет собой уже зафиксированный капитал и убеждения. Это расхождение говорит нам о том, что трейдеры не просто «пробуют» быстрые сделки на DEX; они создают значительные долгосрочные позиции в сети.

Этот сдвиг представляет собой перераспределение капитала с централизованной на децентрализованную инфраструктуру. Как только эта миграция начинается, сетевые эффекты ускоряют ее. Больше ликвидности привлекает больше трейдеров, что, в свою очередь, привлекает больше маркет-мейкеров, еще больше углубляя ликвидность.

Восход Hyperliquid и Lighter

Рейтинг бирж перпетуальных контрактов за 2025 год выявил серьезные изменения в структуре рынка. Две децентрализованные платформы уверенно вошли в топ-10, заменив старых централизованных игроков:

- @HyperliquidX: седьмое место в мире, годовой объем торгов 2,9 трлн долларов;

- @Lighter_xyz: десятое место в мире, годовой объем торгов 1,3 трлн долларов.

В 2025 году объем торгов Hyperliquid превысил показатели Coinbase International. Эта децентрализованная платформа, существующая менее двух лет, обогнала публичную, поддерживаемую институциями биржу с миллиардами долларов капитала и многолетней историей операционной деятельности.

Coinbase International в 2025 году обработала около 1,4 трлн долларов. Hyperliquid достигла 2,9 трлн — более чем в два раза больше.

Побеждает инфраструктура

Секрет успеха Hyperliquid — не умный маркетинг или токен-стимулы, а инфраструктура. Платформа построила собственный блокчейн Layer 1 (HyperCore), оптимизированный specifically для торговли перпетуальными контрактами.

Это архитектурное решение окончательно положило конец нарративу «DEX медленные». Контролируя полный технологический стек — от механизма консенсуса до движка сопоставления ордеров, Hyperliquid достигла: подтверждения сделок менее чем за секунду; нулевой комиссии за газ для маркет-мейкеров; пропускной способности более 20 000 ордеров в секунду; 100% аптайма в течение всего 2025 года.

Для сравнения, DEX на основе Ethereum страдали от перегрузки сети и переменных затрат на газ, а другие решения L2 зависели от внешней инфраструктуры. Вертикальная интеграция Hyperliquid обеспечила пользовательский опыт, неотличимый от централизованных бирж, при сохранении полной безопасности децентрализации.

Lighter пошел по схожему пути, хотя и с другой технической реализацией. Вывод ясен: чтобы конкурировать с централизованными биржами, DEX должны сами контролировать свою инфраструктурную судьбу.

За пределами крипто: революция HIP-3 от Hyperliquid

В конце 2025 года Hyperliquid реализовала HIP-3 (Hyperliquid Improvement Proposal 3), фундаментально изменив свою рыночную структуру.

Бессписочный листинг

Ранее для открытия нового перпетуального рынка требовалось одобрение валидаторов — полуцентрализованный процесс. HIP-3 ввел механизм развертывания бессрочных рынков без разрешений.

Теперь любой разработчик может создать перпетуальный рынок для любого актива, имеющего надежный источник цены. Никаких токенов, никаких разрешений, никаких листинговых сборов.

Мгновенный эффект был взрывным. В течение нескольких недель на платформе появились перпетуальные рынки для активов, которые ранее никогда не торговались в сети.

Мост к традиционным финансам

К февралю 2026 года влияние HIP-3 стало очевидным. Такие платформы, как Hyperliquid, больше не являются просто «криптобиржами деривативов», они становятся глобальной финансовой инфраструктурой.

В настоящее время перпетуальные рынки на Hyperliquid охватывают:

- Товары: золотые и серебряные перпетуальные контракты, отслеживающие фьючерсы COMEX; сырую нефть и природный газ; сельскохозяйственную продукцию (пшеница, кукуруза, соя).

- Акции: Pre-IPO компании, такие как SpaceX и OpenAI; синтетическая экспозиция на основные акции технологических компаний; перпетуальные контракты на фондовые индексы (S&P 500, Nasdaq 100).

- Альтернативные активы: прогнозные рынки (результаты выборов, экономические показатели); производные инструменты для спортивного betting; погодные деривативы.

Такое расширение означает, что Perp DEX становятся инфраструктурой для глобального ценового обнаружения 24/7.

Рынки, которые никогда не закрываются

Традиционные финансовые рынки закрываются — NYSE закрывается в 4 вечера по восточному времени, фьючерсные рынки CME прекращают торги в воскресенье вечером. Это создает трение, информационные пробелы и альтернативные издержки.

А основанные на блокчейне перпетуальные рынки никогда не закрываются. Когда традиционные рынки offline, ончейн-рынки продолжают работать, включая новую информацию в реальном времени.

Представьте: в воскресенье вечером выходят важные новости — геополитический кризис, банкротство компании, неожиданные действия центрального банка. Традиционным рынкам придется ждать до утра понедельника, чтобы оценить эту информацию, что приведет к потенциальным гэпам и диспропорциям.

Перпетуальные контракты на таких платформах, как Hyperliquid, немедленно оценивают информацию. По мере углубления ликвидности на этих рынках они могут начать влиять на цены открытия традиционных рынков — 24/7 цены в сети становятся ориентиром, к которому традиционные рынки вынуждены подстраиваться в понедельник утром.

Заключение: Новые границы перпетуальных контрактов

Данные за 2025 год рассказывают однозначную историю: перпетуальные контракты стали доминирующей силой в криптотрейдинге, а децентрализованные платформы быстро сокращают разрыв со своими централизованными аналогами.

Цифры говорят сами за себя: объем торгов десяти крупнейших бирж перпетуальных контрактов — 929 трлн долларов; рост торговли DEX perps на 346%; открытый интерес на DEX вырос на 229,6%; ведущие DEX уже заменили крупные CEX в рейтингах.

Поскольку стало возможным создание рынков без разрешений, а блокчейн-инфраструктура по производительности сравнялась с централизованными системами, граница между «криптобиржей» и «глобальным финансовым рынком» исчезает. Эти платформы движутся к «ончейн финансовым рынкам» — где любой актив с источником цены может торговаться 24/7, полностью в режиме самохранения, с прозрачным расчетом.

Спотовая модель торговли — покупка и физическая поставка активов — сохранится. Но в ценовом обнаружении, хеджировании и капитально-эффективных спекуляциях доминировать будут перпетуальные контракты.