1、 BTC reduction horizontal plate

In the daily K-line chart of BTC, there were horizontal adjustments for several consecutive trading days, and finally there was a contraction signal in the daily level trading volume. The trading volume is lower than the equivalence line, which means that the trading characteristics with high activity in recent years have continued to change significantly. At the point, BTC was trading sideways around $19000, similar to the recent low closing price. This shows that long and short will compete around $19000, and the market is still in the expectation of volume reduction and correction.

2. The number of BTC coin holding addresses increased against the trend

The data shows that although the BTC price has continued to retreat significantly, falling below $20000 from $40000 in April, the number of currency holding addresses is not stagnant. The latest number of coin holding addresses on July 3 has reached 42.96 million, an increase of more than 9.6 million or 2.2% compared with 42million in April. Since 2022, the number of BTC coin holding addresses has increased from 40.2 million to 42.96 million, an increase of 2.76 million or 6.8%. On the whole, during the BTC price retreat, more investors hold BTC after the chips change hands. At present, the growth trend of the number of BTC coin holding addresses is similar to that in the second half of 2021, and the growth rate is weaker than that in the first half of 2021. According to this judgment, the bulls are in the stage of chip accumulation, and the price reversal of BTC needs time to test.

3. BTC price is close to the cost price of investors

During the low-level and high-volume operation of BTC price, its cost price is rapidly approaching the cost price of investors. From the perspective of holding time, the cost price of investors holding money for 18 to 24 months has risen to $17643, that is to say, this point has been higher than the recent BTC lowest price of $17622. In other words, if BTC is close to US $17643 in the short term, the possibility of further breaking and falling has been significantly reduced. The cost price of investors holding money for 18 to 24 months is the main price for holding money for a long time. Its currency holding cycle starts from the middle of 2020. If the main cost price is lower than this cost price, the cost may be an important buying signal.

4. Eth main force lures more and pulls up

In the 30 minute K-line chart, the main investors' short-term rise in BTC prices lasted for a short time, but the trading volume continued to rise significantly. The corresponding eth price rise continued on July 1. Although the main short-term trading rhythm accelerates, this trading heat does not last long, so the impact on the market is not significant. Near the key $1000, the ETH price trend still shows a contraction sideways, indicating that there is a greater possibility of further breaking. From the perspective of fluctuation space, the current US $1050 is very close to the integer price of US $1000. Therefore, ETH will also test the support effect of $1000 in the short term, so as to confirm whether it can rebound again.

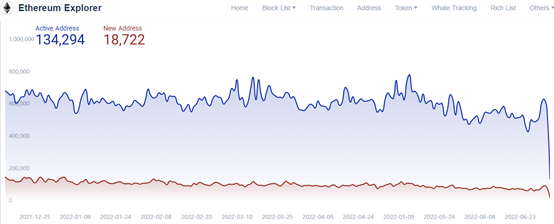

5. The number of eth active addresses rebounded

Recently, the number of active addresses of eth has continued to rebound significantly, increasing from 430000 on June 26 to 629000 on July 2, with an increase of 46%. During this period of time, the price of eth has continued to fall significantly, falling from $1242 to $1059, which shows that investors bought eth at a low price in the price decline stage. Judging from this, the early decline of eth has boosted investors' trading enthusiasm. During the same period, the number of new addresses also showed a similar increase.

At the point, ETH is closer to the integer level of $1000. Considering that there are many eth investors in short-term trading, more investors in new trading will continue to suffer losses after falling below $1000. Therefore, at present, the support of eth of $1000 is very important.