Автор: Memento Research

Перевод: Deep Wave TechFlow

Введение от Deep Wave: Данные о крипто-финансировании за первые 4 месяца 2026 года раскрывают суровую реальность: финансирование в направлениях игр и DePIN практически иссякло, а две компании на рынках предсказаний — Kalshi и Polymarket — привлекли больше денег, чем все проекты DeFi за год вместе взятые. Ещё более тревожным сигналом является то, что количество сделок по слияниям и поглощениям (M&A) сравнялось с количеством сделок на посевной стадии, что означает смещение капитала от ставок на новые идеи к приобретению существующих лидеров рынка.

Обзор финансирования: мартовский всплеск — всего лишь иллюзия

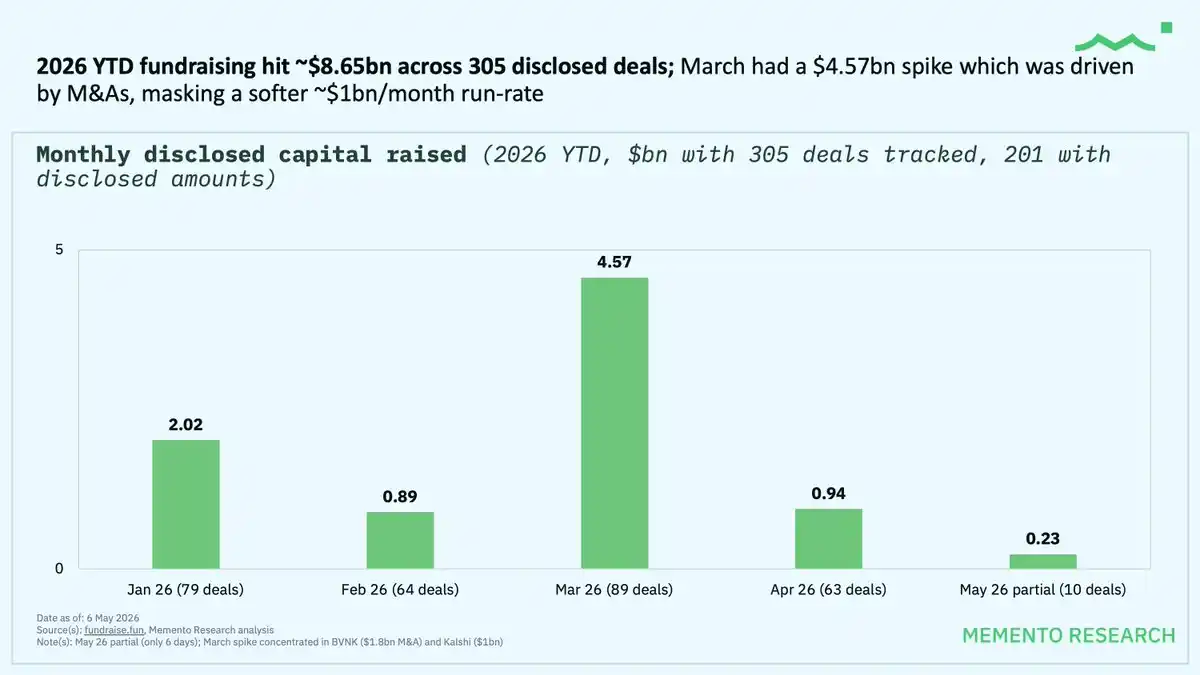

С 1 января по 6 мая 2026 года криптоиндустрия завершила 305 раундов финансирования на общую сумму 8.65 миллиардов долларов. Однако «взрывной» рост до 4.57 миллиардов долларов в марте фактически был обусловлен всего двумя сверхкрупными сделками M&A: 1.8 миллиарда долларов в BVNK и 1 миллиард долларов в Kalshi.

Если исключить эти две сделки, реальный темп привлечения средств составляет около 1 миллиарда долларов в месяц, что ещё слабее, чем в конце 2025 года.

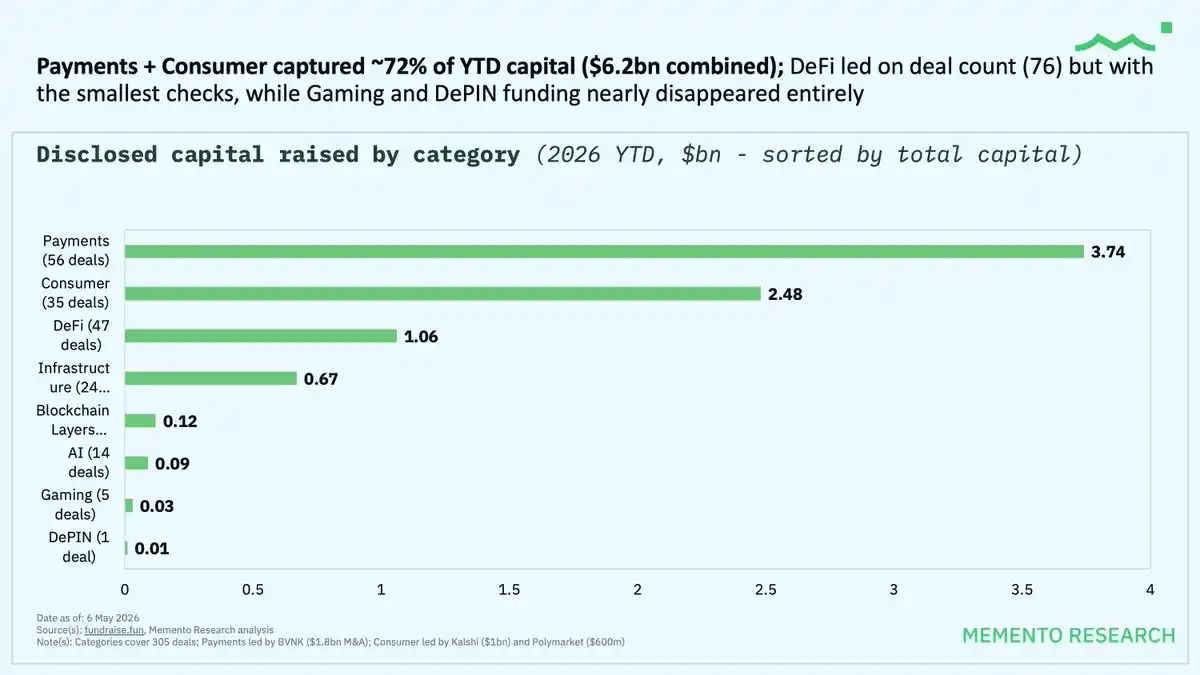

Направления потоков капитала: платежи и потребительский сегмент поглотили 72%

Разбивка по направлениям:

Платежи: 3.74 млрд долларов (56 сделок)

Потребительский сегмент: 2.48 млрд долларов (35 сделок)

DeFi: 1.06 млрд долларов (47 сделок, наибольшее количество транзакций)

Два направления — платежи и потребительский сегмент — вместе составляют 72% всех годовых средств. Финансирование игр и DePIN практически сошло на нет.

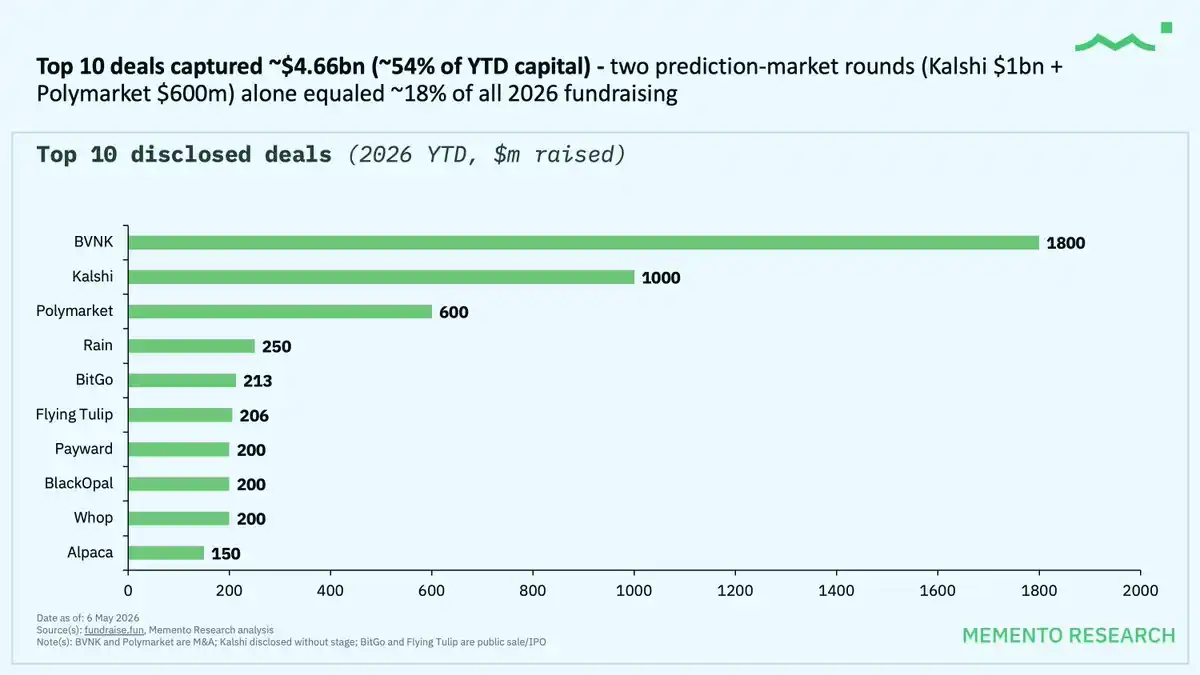

Рынки предсказаний доминируют в потребительском сегменте

Две компании на рынках предсказаний привлекли 18% всех годовых средств:

Kalshi: 1 миллиард долларов

Polymarket: 600 миллионов долларов

Сумма этих двух сделок — 1.6 миллиарда долларов — превышает общий объём всех 47 раундов финансирования в DeFi.

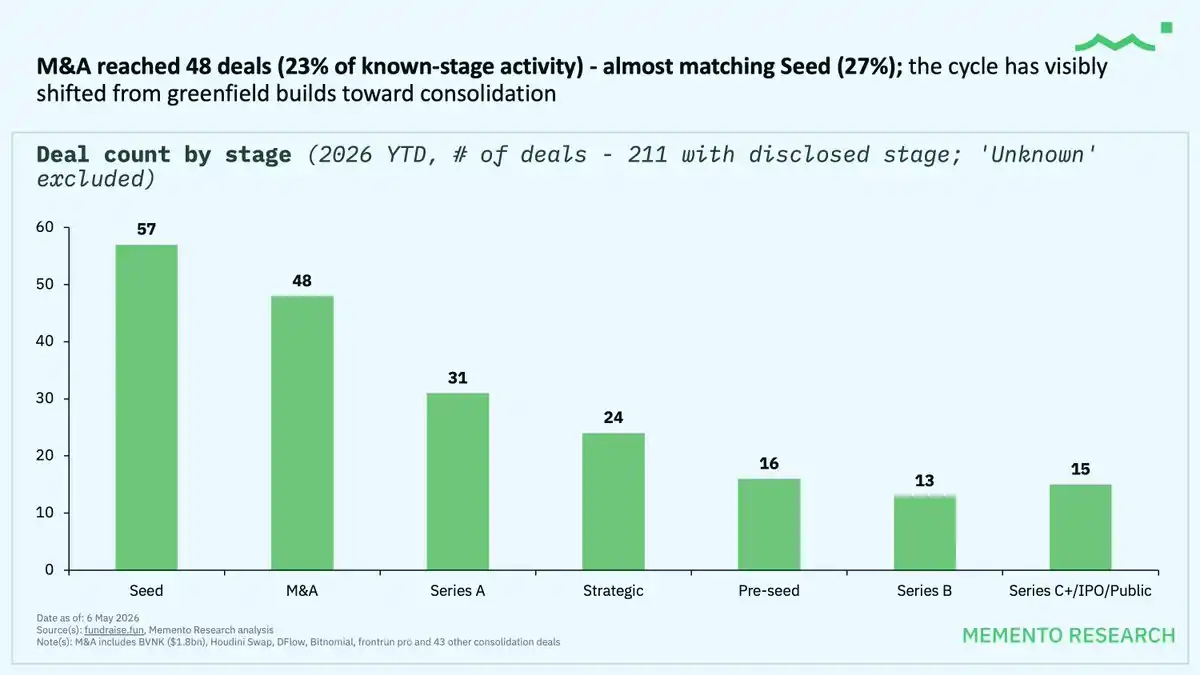

Слияния и поглощения (M&A) становятся мейнстримом

Количество сделок M&A достигло 48 (23% от сделок с известной стадией), что почти сравнимо с 57 сделками на посевной стадии (27%). Этот цикл сместился от инвестиций в ранние стадии новых идей к приобретению отраслевых лидеров.

Перетасовка в рейтинге инвестиционных институтов

Самые активные фонды в 2026 году:

Coinbase Ventures: 18 сделок (2-е место за период 2021-26 гг.)

Tether: 13 сделок (новый лидер по количеству сделок)

Animoca Brands: 11 сделок (1-е место за период 2021-26 гг.)

GSR: 11 сделок

a16z: 7 сделок (значительное снижение по сравнению с ~200 сделками за период 2021-26 гг.)