加密市场以积极的面貌开启了2023年,比特币近 40% 的价格涨幅跑赢了传统风险资产。随着周三重要的美联储 (Fed) 利率决议公告临近,加密市场策略师警告道,美联储主席鲍威尔可能在新闻发布会上坚持他的鹰派言论,因此比特币可能会打破年初至今的涨势,但这种回调将是“短期且健康”的。

“”

继去年加息 425 个基点 (bps)后,美国12月份经济数据显示通胀已经降温,其中衡量工资的重要指标–就业成本指数–显示,第四季度工资增幅 1%,低于道琼斯 1.1% 的估计。市场预期美联储将在周三放慢紧缩步伐至 25 个基点,换言之,加息 25 个基点已被市场消化。投资者的焦点将集中在鲍威尔是否承认近期通胀和经济活动疲软,进而发出暂停紧缩政策的信号,这将增强市场对尽早转向宽松政策的希望。

“”

美联储的长期通胀目标是每年 2%,鲍威尔过去曾表示,在美联储考虑暂停加息之前,他需要看到通胀以有意义的方式走低。

“”

截至周二美股收盘,道琼斯工业平均指数上涨 0.63%;标准普尔 500 指数上涨 0.91%,创下 2019 年以来最好的 1 月涨幅;纳斯达克综合指数上涨 1.19%。比特币上涨 1.6%至 23,115 美元附近。以太坊上涨 1% 至 1,573 美元左右。

“”

分析师认为,美央行政策过早转向的可能性不大,因为最近股票和债券的上涨以及美元的下跌自 4 月以来首次缓解了资本市场的压力,也削弱了美联储通过收紧信贷标准来应对价格压力的努力。

“”

加密资产管理公司 Wave Financial财务负责人 Nauman Sheikh 发表评论称:“在新闻发布会上,鲍威尔很有可能会变得更加鹰派并重新收紧金融环境。因此,我们可以看到加密货币和所有风险资产的健康短期修正”。

“”

Sheikh 补充说,尽管美联储一再警告利率将“长期保持在较高水平”,但市场在定价美联储转向方面已经超前了。

“”

Twitter 用户名为 The Carter 的市场策略师也警告道,随着美联储会议临近,鲍威尔周三将以比市场目前预期更为强硬的方式表态,包括加密货币市场在内的风险资产的“大屠杀”可能成为现实,他认为,这将导致所有风险资产的大幅抛售,其中包括比特币和大多数其他数字资产。他在推文中写道:“2 月 1 日,市场会见‘血’,鲍威尔将通过正面强行降息来重新收紧金融状况”。

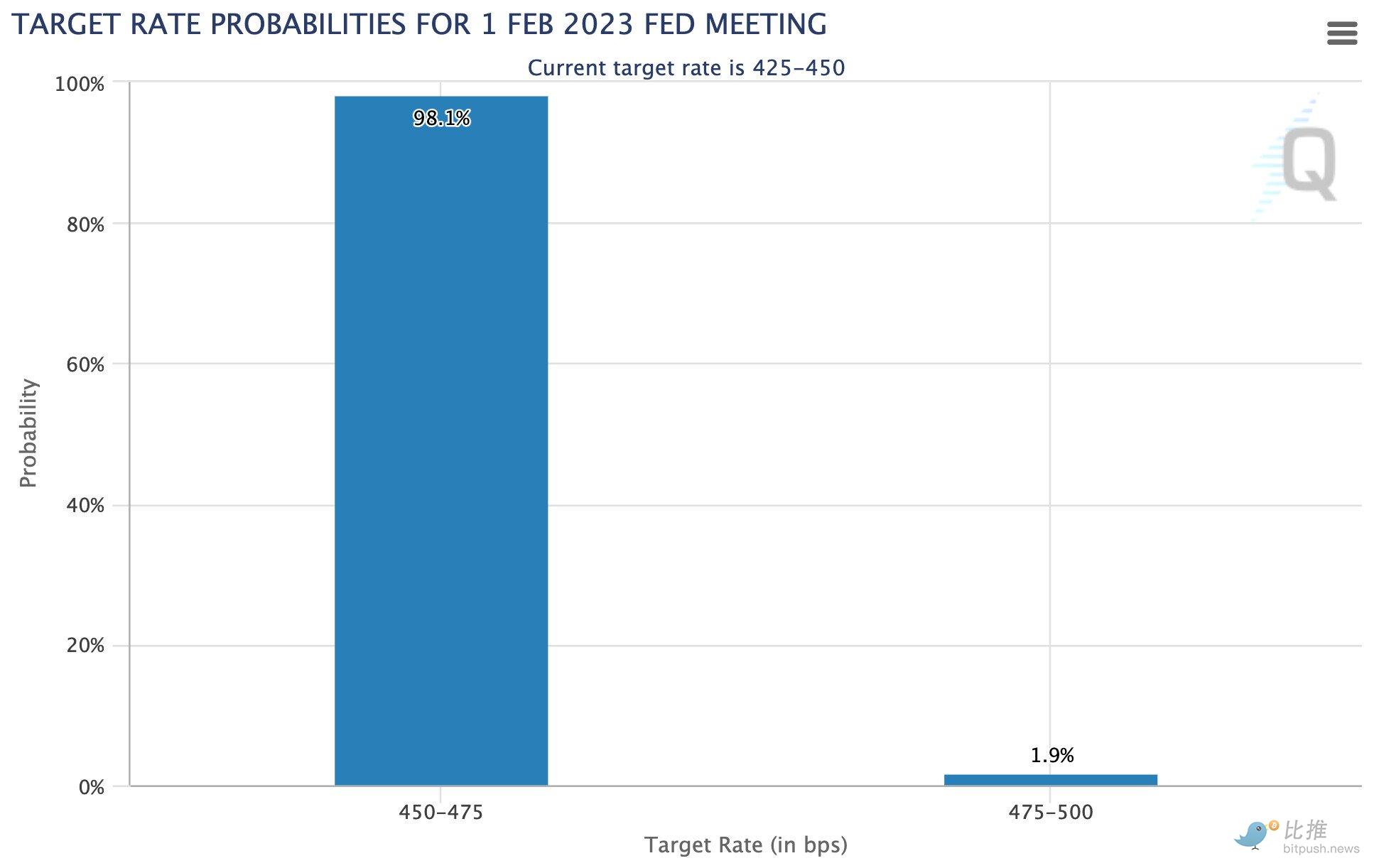

美联储定于本周三美国东部时间 2:00 PM(北京时间 6:00AM)宣布其最新的利率决定,大多数分析师预计加息 25 个基点。这也是市场目前的定价,CME 的 FedWatch 工具估计加息 25 个基点的可能性为 98.1%。

Pepperstone 研究主管 Chris Weston 在其市场周报中表示,金融状况已经恢复到鲍威尔可能会表示宽松程度“毫无根据”的程度,这将推低包括科技股和加密货币在内的风险资产。

“”

Weston 写道:“在这个时刻,美联储似乎不太可能表现得鸽派,因此风险在于美联储的鹰派——尽管这是意料之中的——而且在杠杆基金做空美元的市场(即期市场),风险小幅偏向美元上行,这意味着纳斯达克和黄金价格走低”。

“”

加密资产管理公司 Blofin 交易员 Griffin Ardern 对CNBC表示:“每周看跌期权在大宗交易者中很受欢迎,但没有远期月度看跌期权交易的记录”。这暗示着在会议之前,谨慎情绪已经渗透到市场,提振了对短期看跌期权或看跌押注的需求。

“”

牛市可能会快速复苏?

“”

鲍威尔引发的预期回踩可能是短暂的,因为市场最近对美联储的鹰派言论变得有弹性。

“”

本月初,多位美联储官员警告称可能会加息。 尽管如此,比特币本月仍然上涨了 40%,游戏代币等风险更高的加密货币出现了更大的涨势。

“”

宏观投资者 James Choi 发推文说: “我预计美联储将把基金利率提高 25 个基点(已经反映在价格中),并让鲍威尔发表鹰派言论,但这只是烟雾弹,市场具有前瞻性,它将在 3 月份开始定价‘暂停’,届时标准普尔 500 指数将达到 4500 点。”

“”

Choi 补充道:“如果市场先信了鲍威尔,标普就不会达到 4,000 点以及看到如此宽松的金融环境”。

“”

本月初,多位美联储官员警告称可能会加息。 尽管如此,比特币本月仍然上涨了 40%,游戏代币等风险更高的加密货币出现了更大的涨势。

“”

衍生品市场数据显示,持续时间较长的看涨期权斜率(衡量看涨期权相对于看跌期权的成本)仍然偏向看涨期权,Griffin Ardern 称:“市场出现这种情绪的原因是,加息 25 个基点基本已经消化,投资者更倾向于认为鲍威尔的鹰派讲话是虚张声势”。