Filecoin 入门

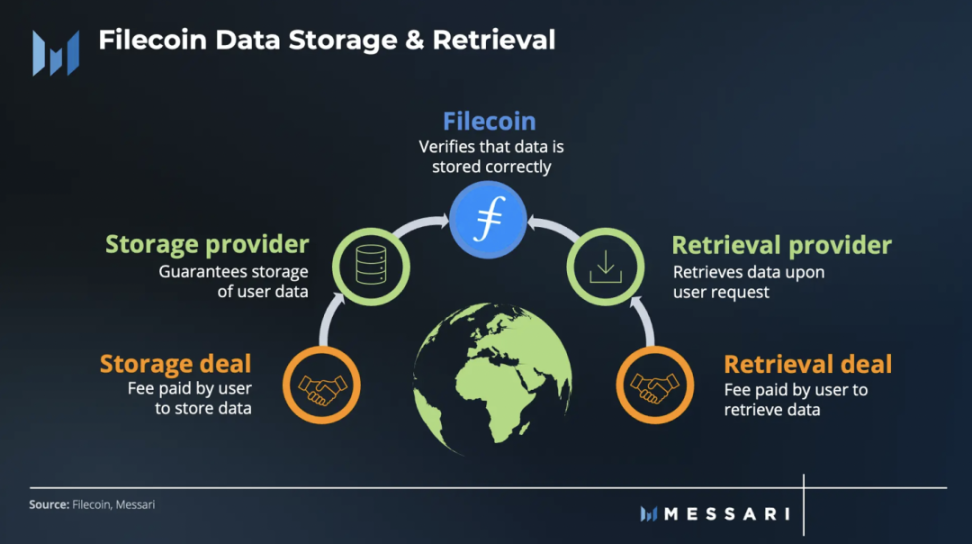

依赖集中式数据存储有一个很大的缺点:很难系统地验证存储数据的完整性。就目前而言,Filecoin 网络是 Amazon S3 的点对点版本。它建立在星际文件系统 (IPFS) 之上,IPFS 作为 Filecoin 网络的分布式数据存储和共享层。 Filecoin 定期验证数据存储,并使用基于供需动态定价的存储交易,而不是固定的定价结构。

依赖集中式数据存储有一个很大的缺点:很难系统地验证存储数据的完整性。就目前而言,Filecoin 网络是 Amazon S3 的点对点版本。它建立在星际文件系统 (IPFS) 之上,IPFS 作为 Filecoin 网络的分布式数据存储和共享层。 Filecoin 定期验证数据存储,并使用基于供需动态定价的存储交易,而不是固定的定价结构。

存储交易就像一份带有服务水平协议 (SLA) 的合同——用户向存储提供商支付费用以在指定期限内存储数据。为了保证数据安全,Filecoin 使用加密经济激励模型,定期使用零知识证明验证存储。为了激励存储提供商参与交易,Filecoin 使用网络的原生代币 FIL 奖励他们。如果数据无法检索或存储失败,存储提供商也会被罚没。

为了检索数据,Filecoin 用户向检索提供商付费以获取数据。与涉及链上交易的存储交易不同,检索交易使用支付渠道在链下结算支付,从而加快检索速度。

关键指标

性能分析

Filecoin 区块链被网络的需求方(即存储用户)和供应方(即存储提供商)使用。存储用户和存储提供商都为协议产生收入。

收入

Filecoin 的收入框架与以太坊类似,因为 gas 系统基于 EIP-1559。该 gas 系统由燃烧的网络费用组成,以补偿所使用的资源。

协议收入

根据 Messari 的收入分析,Filecoin 的协议收入代表以下总和:

Base fees——任何存储交易或证明都需要;基本费用由消息拥塞情况决定。

Batch fees——用于增加存储容量。

Overestimation fees——优化 gas 使用所需的费用。

Penalty fees——针对存储提供商的失败收取。

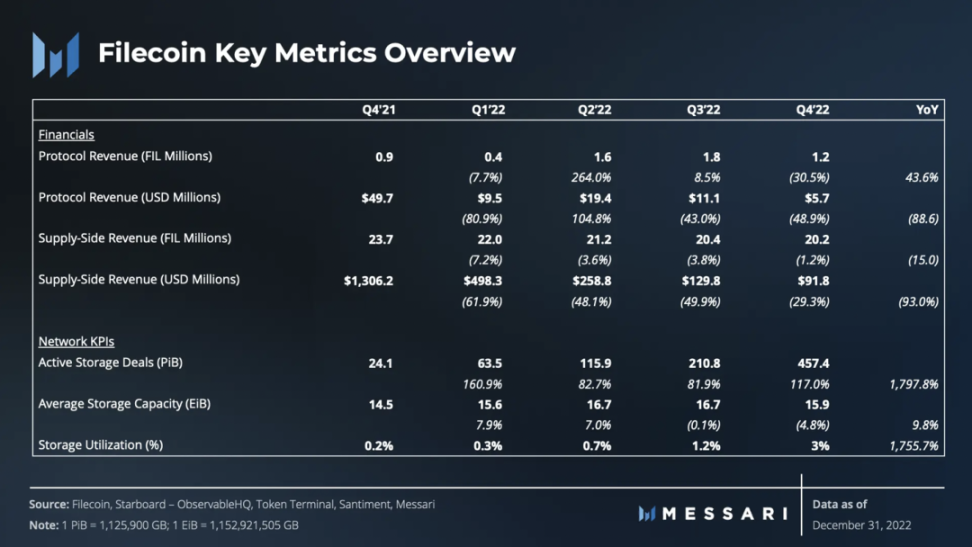

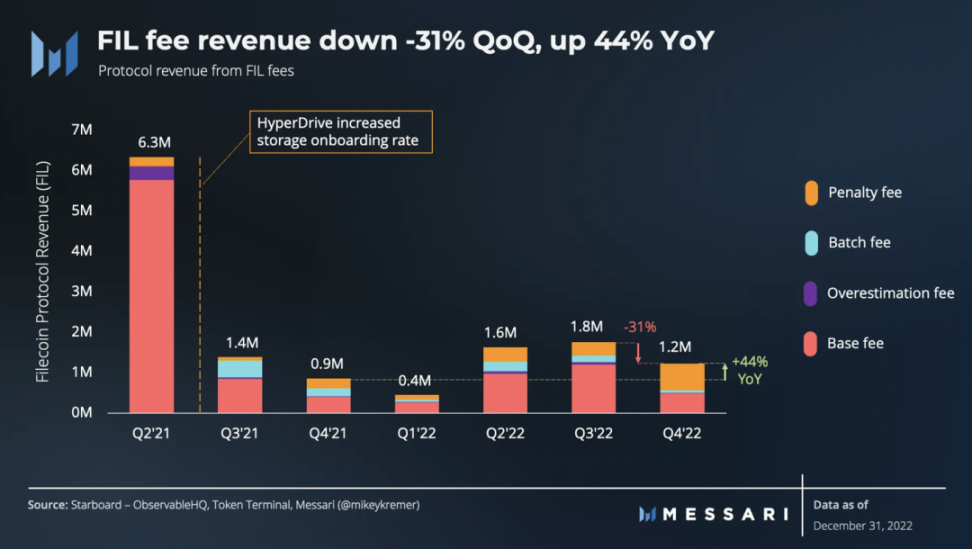

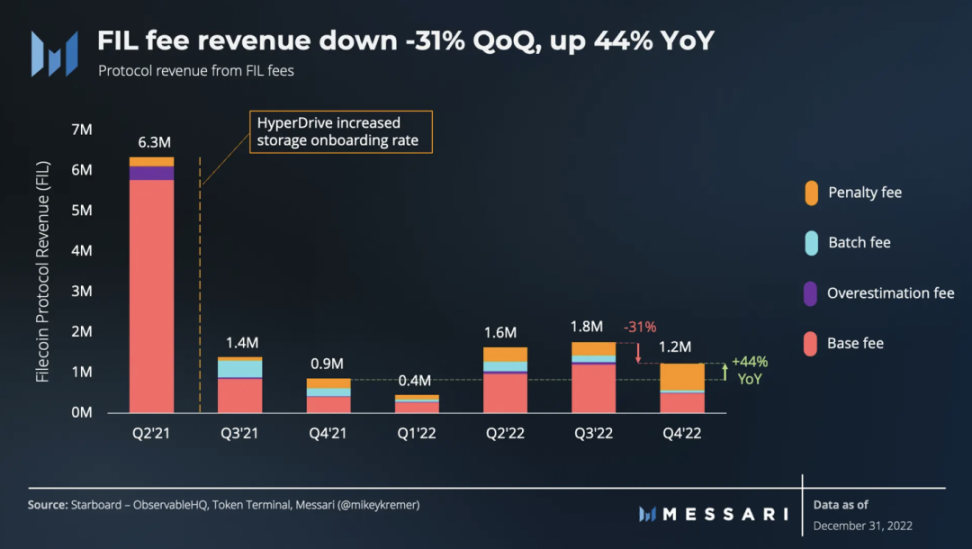

协议收入在 22 年第四季度下降 31% 至 120 万 FIL。与去年同期相比,从 21 年第四季度的近 90 万 FIL 增长了 44%。值得注意的是,Q4'22 带来了应计费用构成的两个显著变化:

尽管活跃的存储交易增长了 10%(根据 Filecoin 关键指标概览表),但基本费用下降了 60%。

由于存储提供商离线天数增加,罚款增加了 100% 并达到历史最高水平。

与 2021 年 7 月 HyperDrive 网络升级前相比,Q4'22 的 FIL 协议收入继续相对较低。通过聚合存储证明,HyperDrive 使存储上线率提高了 10-25 倍。虽然 HyperDrive 升级使网络参与者受益——通过减少拥塞和释放区块空间——但它也导致整体交易费用降低。因此,HyperDrive 升级导致过去四个季度的协议收入下降。

Filecoin 费用中唯一没有被协议燃烧的部分是区块矿工收集的「小费」,以加速网络供应方的交易。因此,这笔「小费」算作供应方收入。 Filecoin 的供应方收入包括支付给存储提供商的代币奖励(占 Q4'22 供应方收入的 99.97% 以上),而「小费」只占一小部分。

供应方收入

供应方收入包括网络支付给供应方参与者的区块奖励。新 FIL 代币的铸造机制依赖于:

指数衰减模型(30% 的代币):区块奖励在最初最高,以刺激参与,并随着时间的推移呈指数下降。

基线模型(70% 的代币):区块奖励随着存储容量的增加而增加。

这两种模型结合的目的是避免网络早期阶段区块奖励分配后的参与度下降(见指数衰减),并通过增加存储容量不断奖励为网络创造的额外价值(见基线模型)。

供应方收入在 22 年第 4 季度下降 1.2% 至 2020 万 FIL,这是受奖励发放总体减少的影响。虽然在 22 年第 4 季度实现了基线增长目标,但由于上述指数衰减,铸币量整体减少。值得注意的是,虽然自 21 年第四季度以来(根据 Filecoin 关键指标概述表),内置存储容量的增长率环比下降,但供应方收入也是如此。

用量

存储用户和存储提供商之间的活跃交易中存储的数据量衡量了对 Filecoin 服务的需求。对 Filecoin 存储的需求来自特定于 Web2 和 Web3 的存储交易。

存储交易

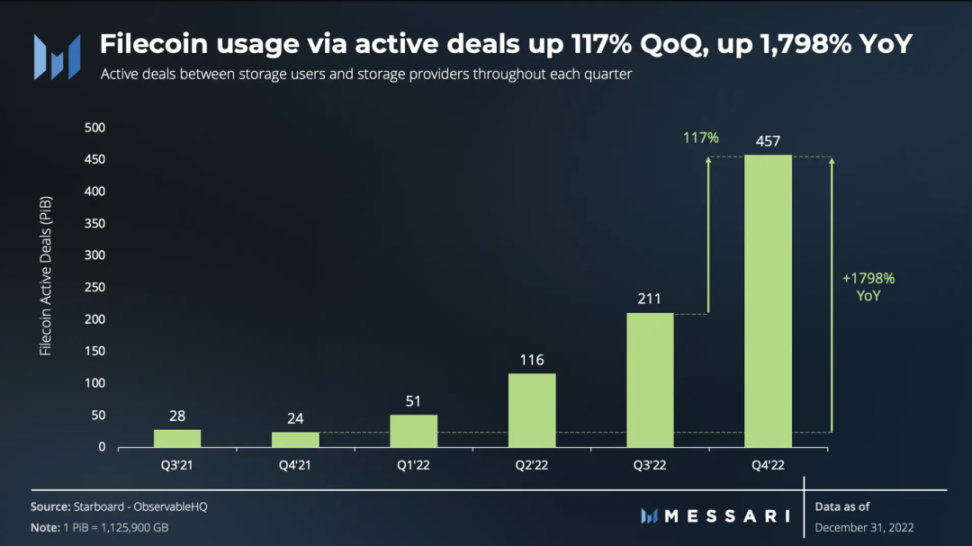

接近零的存储费用可能进一步鼓励通过交易增加数据存储。到 22 年第四季度末,超过 231 个 PiB 通过活跃的交易存储在 Filecoin 网络上——比上一季度增加了 10%。自 21 年第四季度以来,这种积极的增长趋势一直在持续,因为 Filecoin 的活跃交易同比增长了 850%。

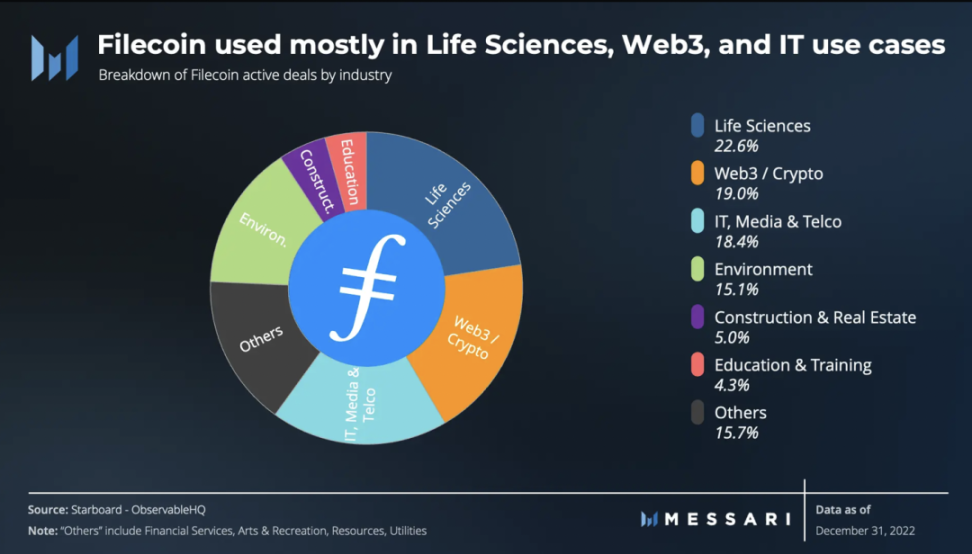

按行业用例对活跃存储交易进行细分,揭示了最多利用 Filecoin 的行业:

生命科学 (23%)

Web3 / 加密 (19%)

信息技术 (18%)

为了激励使用真实数据进行这些存储交易并防止网络奖励游戏,引入了 Filecoin Plus (Fil+) 计划。 Fil+ 通过增加存储提供商赢得区块奖励的可能性,为参与经过验证的交易提供更多奖励。这导致存储供应商削减竞争供应商的费用。因此,在 22 年第 4 季度,存储几乎没有成本。

自 2021 年第 4 季度以来,从常规交易(未经验证的数据交易)转变为以 Fil+ 交易(经验证的数据交易)为主。这种转变对应于 Fil+ 交易的持续上升趋势,占 22 年第四季度所有新交易的 99.5%。 Fil+ 交易对常规交易的翻转,加上新交易的增加,表明 Fil+ 激励机制和入职计划正在成功推动存储利用率。

客户

根据 Messari 最近的去中心化存储网络指南,Filecoin 主要面向企业和开发人员提供冷存储解决方案。其具有竞争力的价格和易于访问的特性使其成为寻求具有成本效益的替代方案来存储大量档案数据的 Web2 客户的有吸引力的选择。

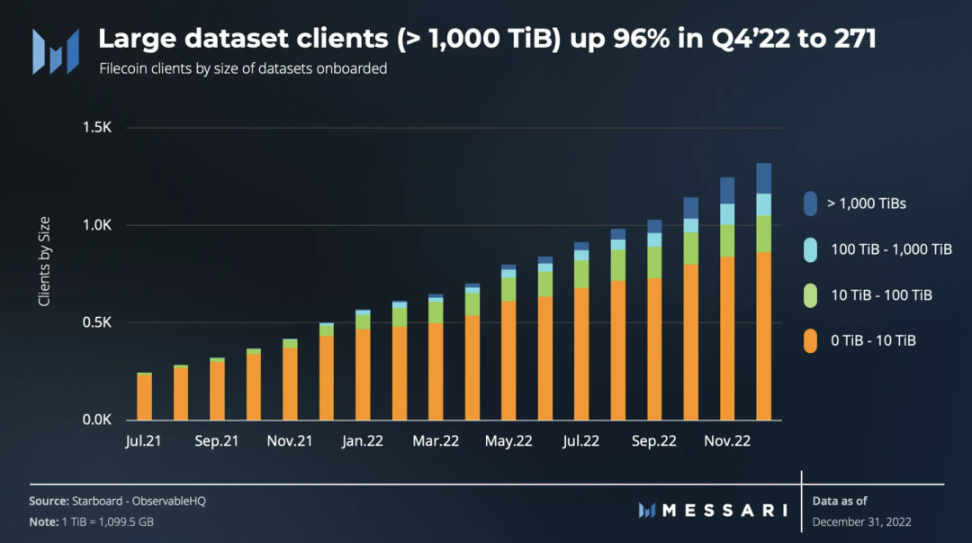

到 22 年第四季度末,共有 1,320 个客户在 Filecoin 上使用了数据集,其中 271 个客户使用了大型数据集(例如,存储大小超过 1,000 TiB 的数据集),比第三季度的 138 个客户增加了 96% 22. Filecoin 的客户范围从纽约市和 USC Shoah Foundation,到 OpenSea 等 Web3 平台。将数据载入 Filecoin 网络的其他值得注意的用例包括:

加州大学伯克利分校与 Seal Storage 合作存储物理研究

GenRAIT 利用 Estuary 在 Filecoin 上存储关键基因组数据

Starling Labs 研究中心存储敏感的人类历史数字记录

中国增长最快的数字内容主机 Eweison 使用 Filecoin 进行数据保存

利用率与容量

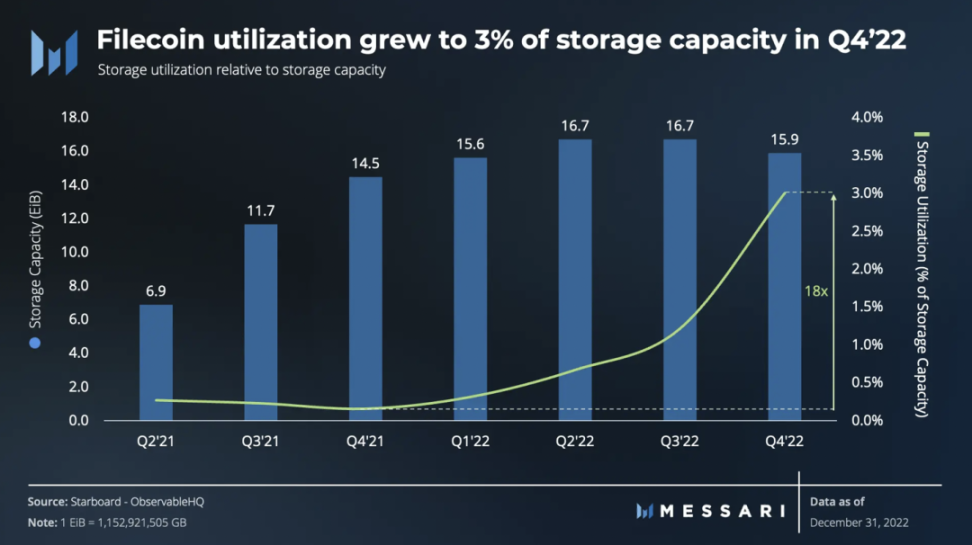

尽管整体市场低迷,但 Filecoin 的承诺存储容量在过去五个季度中增长至 16.7 EiB。这种增长部分归因于存储提供商的增加。 Filecoin 存储提供商的数量激增了约 300%,达到 3,030 家——与网络容量的峰值相对应。然而,在 Q2'22 达到历史最高点并在 Q3'22 达到稳定后,Q4'22 的存储容量出现下降。

同时,相对于总可用存储容量的存储利用率在过去几个季度稳步上升至 22 年第 4 季度的 3%,而 21 年第 4 季度仅为 0.2%。也就是说,尽管起步基数较低,但过去一年的使用量增长速度是容量的 18 倍。

由于 Fil+ 程序能够获取新用户并引入有价值的数据集,因此它可以作为未来围绕数据开发可盈利用例的基础。从本质上讲,Filecoin 的策略似乎是以接近零的成本获取数据,以便在未来通过数据检索或数据计算获利。

虽然 Fil+ 计划的推出有利于供应入职和需求生成,但人们齐心协力孵化新业务和用例以在 Filecoin 上构建。

检索

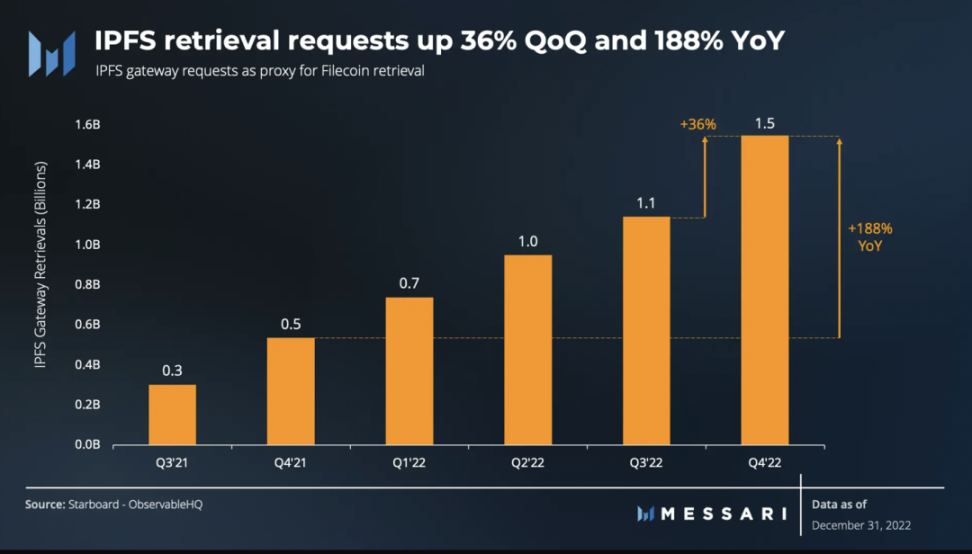

IPFS 网关请求可以作为 Filecoin 检索的代理,因为 Filecoin 的大多数开发人员存储工具都可以让整个 IPFS 网络访问数据检索。

与 Q3'22 相比,Q4'22 的检索请求数量增加了 36%。与去年同期相比,检索请求增加了 188%。这种积极趋势是捕捉依赖 IPFS 进行存储和检索的流行存储开发人员工具(例如 NFT.storage 和 Web3.storage)使用量增加的合理代表。随着检索市场的不断发展,新的指标将可用于在 IPFS 网关之外进行跟踪。

生态系统概览

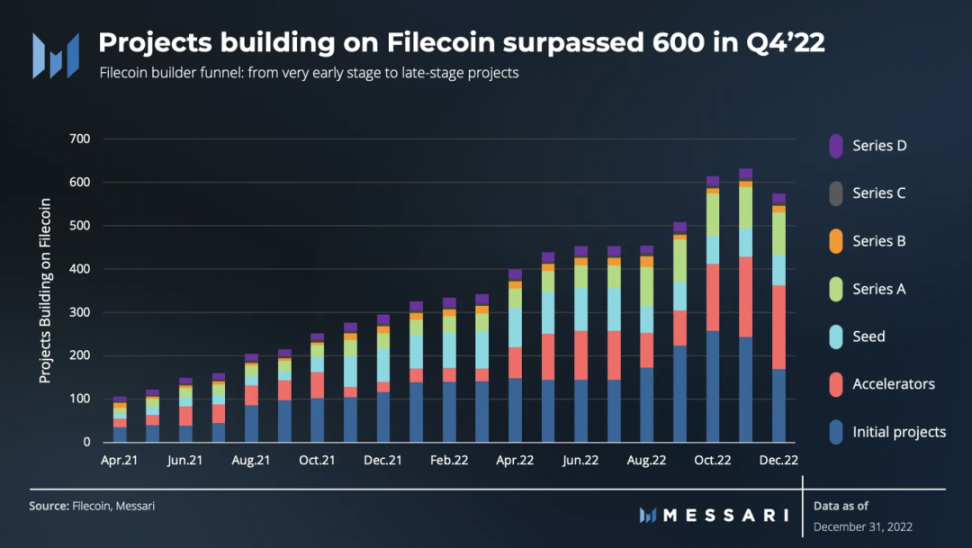

Filecoin 生态系统一直在通过黑客马拉松、加速器、赠款、指导和增长支持等活动积极开发开发人员和建设者的漏斗。该漏斗旨在帮助早期项目和团队发展到足以获得资金和投资的程度。资金由 Protocol Labs 或附属实体提供。

目前正在 Filecoin、IPFS 和 Protocol Labs 网络生态系统上开发 600 多个已知项目,比 22 年第三季度的近 500 个有所增加。这些项目利用 IPFS、Filecoin、libp2p 协议或构建在这些协议之上的服务。增长的很大一部分来自加速器,从 22 年第三季度的 82 个增加到 22 年第四季度的 194 个。此外,NFT.Storage 和 Web3.Storage 等项目使其他项目能够利用 Filecoin/IPFS。

该生态系统被用于大量不同的用例:数据基础设施、媒体流、元宇宙和游戏。大多数利用 Filecoin 的应用程序和协议都提供专注于数据服务的服务:

Ocean Protocol:数据市场的开发者工具和平台

Lighthouse:具有一次性支付定价模型的永久数据存储服务

Slate:用于处理和共享个人数据的搜索引擎

Berty:安全消息传递和社交媒体应用程序

Dether:现金进 / 出和多样化的金融交易

另一大类是媒体和娱乐;例子包括:

MoNA:元宇宙中的 3D 艺术画廊

NFTwitch:Twitch 内容的 NFT 铸币平台

Huddle01:去中心化视频会议

Curio:娱乐品牌从知识产权中获利的 NFT 市场

OPGames:从游戏中铸造 NFT

通过引入 Filecoin 虚拟机 (FVM),Filecoin 旨在允许智能合约应用程序的外部集成。在 Filecoin 网络上构建本机应用程序并与它们外部集成的能力扩大了其潜在网络活动和应用程序生态系统的范围。

定性分析

产品更新

Saturn

Saturn 是一个完全去中心化的 Filecoin 内容检索和交付网络 (CDN),旨在加速 Web 内容交付。 Saturn 还寻求通过降低运行 Filecoin 节点的成本和加快去中心化数据检索来增加 Filecoin 对 Web3 开发人员的吸引力。 Saturn 的长期目标是占据很大一部分应用程序来检索信息,从而实现令人垂涎的「Web3 杀手级应用程序」。

V17 Shark 升级

Filecoin 于 2022 年 11 月进行的 v17 Shark 升级包括改进其针对 Fil+ 交易的智能合约可编程性。此升级自 2022 年 3 月开始进行,并引入了可编程存储功能。目标是改进链上智能合约和链下数据提供者之间的集成。然而,由于链上验证的 gas 消耗增加,预计交易启动将变得更加昂贵。

企业级合作伙伴关系

CME 将 Filecoin 纳入价格指数

CME 于 2022 年 10 月开始发布 FIL 参考利率和价格基准。虽然这一发展并未直接转化为可交易的 FIL 支持的期货合约的创建,但包含 FIL 代币可能会提高 Filecoin 在传统金融市场中的知名度。这可能会进一步为 Filecoin 带来更好的融资机会和合作伙伴关系,并增强路线图和潜在的合作。

Protocol Labs 与 Ernst & Young 和 Seagate 的合作伙伴关系

Filecoin 的创建者 Protocol Labs 与 Ernst & Young 和 Seagate 建立了合作伙伴关系,以支持企业级去中心化数据存储解决方案。如果合作成功,能够吸引机构进行去中心化数据存储,Filecoin 或将在企业级数据的存储和安全方面发挥重要作用。

关键事件

ETHBogota & ETHIndia

Filecoin 和 IPFS 于 2022 年 10 月赞助了基于以太坊的黑客马拉松 ETHBogota,并于 2022 年 12 月初赞助了 ETHIndia。Filecoin 和 IPFS 共同提供了 20,000 美元,而 ETHIndia 提供的总奖池超过 350,000 美元。 Filecoin 和 IPFS 从 ETHBogota 的 500,000 美元以上奖池中贡献了 20,000 美元。

Sustainable Blockchain Summit

Filecoin 的分支 Filecoin Green 专注于促进能源领域的数据透明度,参加了 2022 年 10 月的 Sustainable Blockchain Summit。Filecoin 的多位能源专家发表了主题演讲,包括:

再生经济的基石

解锁碳市场互操作性

FIL Lisbon

Filecoin 于 2022 年 11 月在里斯本主办了 FIL,汇集了超过 65 位演讲者,包括开发人员、存储提供商、生态系统参与者和用户。会议举办了工作组、黑客马拉松、IPFS 营地等学习机会、边会、社交活动等。会议的众多亮点之一包括强调数据安全和透明度价值的演讲,包括:

从 CIA 到 Amazon:MuckRock 如何让数据透明化

打开民主图书馆的大门

不可靠的证据:Starling 实验室记录乌克兰战争

FEVM 黑客马拉松

黑客马拉松于 2022 年 12 月举行,旨在利用 Filecoin 的基础设施来满足高度具体和独特的数据需求,例如:

Koios:无代码数据 DAO 平台

ZKsig NFTs:对市场的访问控制

DataMarket:数据购买和结帐功能

路线图

2022 年回顾

2022 年,Filecoin 推出了一系列更新以增加网络的存储容量。增加的容量使数据更容易检索,从而为其核心产品启用更多真实世界的用例。虽然尚未在主网上线,但 2022 年的更新为智能合约与 Filecoin 的数据功能进行交互奠定了基础。

展望 2023

为了弥合 2022 年到 2023 年的进展,Filecoin 继续改进其数据计算产品的最小可行产品 (MVP)。将 FVM 集成到 Q1'23 的 filecoin 中的第一步是集成 EVM 兼容性。其他改进将包括 L2 功能、分层共识和密封即服务。通过 FVM 激励的 buildernet 和 testnet,Filecoin 希望建立新的并加强现有的合作伙伴关系,以更好地促进数据基础设施社区内的产品增长。

总结

22 年第四季度标志着 Filecoin 使用量的上升,因为活跃的存储交易环比增长了 10%。虽然存储容量从历史最高水平下降了 5%,但存储利用率的增长速度比存储容量同比增长快 18 倍。虽然去中心化存储仍处于早期阶段,但 Filecoin 生态系统仍在蓬勃发展,目前有 600 多个项目正在 Filecoin 上构建。

成功推出 Filecoin 虚拟机可以实现存储以外的下一代应用程序。突出的例子包括永久存储(类似于 Arweave)、向存储提供商提供的抵押贷款不足以及去中心化计算。

如果 Filecoin 继续满足需求,它就有机会成为 Web3 和传统应用程序的去中心化存储和云服务的主要提供商。 Filecoin 必须继续证明其作为存储提供商的可靠性,并有可能成为各种数据密集型服务的推动者。