When a company simultaneously brings Alibaba and Tencent to the negotiation table, and then asks them to leave one after another, that in itself is a signal.

In May of this year, DeepSeek exceptionally launched its first round of external financing. The 50 billion RMB fundraising target, 350 billion RMB valuation, founder personally contributing 20 billion, and the National Big Fund leading the investment—these numbers were explosive enough, but what really caught the industry's attention was the follow-up: Alibaba withdrew, while Tencent is poised to join as a small-scale financial investor. Alibaba perhaps sought an ecosystem lock-in, Tencent only wants a financial stake without interfering with the technical direction, but both sides seem to have failed to reach an agreement.

One exits, one enters. This is not a coincidence of who bid higher or lower, but a mirror moment reflecting the strategic divergence of the two giants in the AI era. Reviewing the ins and outs of this financing, deconstructing the underlying logic of Alibaba's iron-fisted self-research and Tencent's ecosystem embedding, might be more interesting than chasing the valuation numbers themselves.

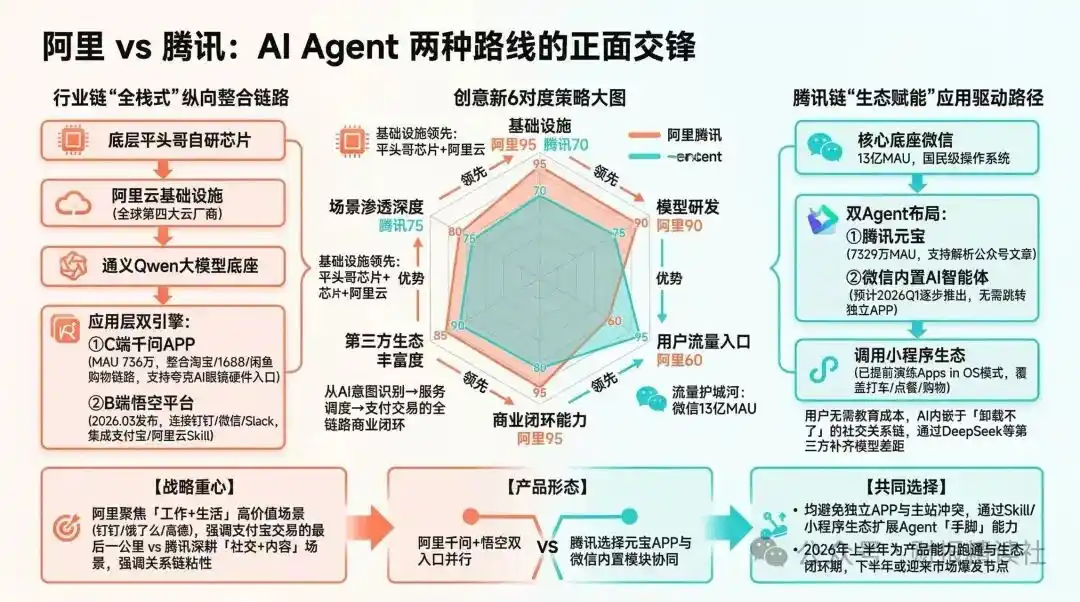

Self-Developed Closed Loop vs. Ecosystem Embedding: Three Distinct AI Approaches

For Alibaba and Tencent, these two internet giants with a combined market cap nearing a trillion dollars, hitting a wall in front of a startup isn't surprising to many in the industry. They know well that the big players' calculations when investing in AI are never simply about financial returns.

This approach has a vivid name in the industry: "Cloud Cashback Investment." The rules are roughly this: a big company claims to invest 1 billion in an AI company, but more than half of that is to "flow back" to the big company's cloud business in the form of purchasing cloud computing power.

In other words, the cash the AI company actually receives is far less, while the big company completes the book entry for external investment and boosts its own cloud revenue. More crucially, taking the money means accepting "ecosystem binding": models are deployed on the big company's servers, APIs are prioritized for integration into the big company's product system, and the technical roadmap and commercialization pace must align with the big company's strategic rhythm.

Let's further dissect the starkly different motivations of Alibaba and Tencent, who were simultaneously at the negotiating table.

Alibaba wanted "ecosystem control." This logic isn't new in the industry: investment equals procurement, equity participation equals binding. Alibaba's terms implicitly required deep integration of the DeepSeek model into its own product lines like Taobao/Tmall, Amap, Alibaba Cloud, etc.

A potential possible version was: DeepSeek's API prioritized deployment on Alibaba Cloud, inference traffic prioritized for Taobao's smart shopping guide, and the technical roadmap needed customized optimization for Alibaba's e-commerce scenarios. For Alibaba, this wasn't a financial investment, but a capital-driven attempt to "weld" external cutting-edge technology onto its own commercial foundation. This continues Alibaba's consistent strategy, similar to Alibaba Cloud's early acquisition of Changting Technology and investment in Shumeng Gongchang, all requiring deep coupling of technical teams with the Alibaba ecosystem.

However, the author believes that the consequence of this "welding" integration is likely that the investee company's technical roadmap gradually loses generality, eventually becoming a "custom model" serving only Alibaba's scenarios, its industry influence paradoxically narrowed. Yet, in the AI era, Alibaba's anxiety is concrete: if it doesn't "lock" the best model into its own fortress, competitors might use it to arm their own e-commerce and cloud businesses.

Tencent's calculations are a different story. Tencent historically built a vast ecosystem through investments but never forced investee companies to be "exclusive."

In the AI field, Tencent continues this style: financial investment is primary, no interference in technical direction, no demand for ecosystem exclusivity. Sources close to the deal revealed that Tencent's terms didn't even require DeepSeek to prioritize using Tencent Cloud, only hoping for cooperation priority in areas like WeChat smart assistants and game NPCs in the future.

This "light-touch" posture reflects Tencent's different positioning of AI. It doesn't count on an external model to restructure its own business but hopes to use external cutting-edge technology to "lubricate" its existing social and content scenarios. Tencent's confidence lies in WeChat, a super entry point. Regardless of who invests in DeepSeek, as long as users want to use the best AI capabilities within WeChat, Tencent can achieve it through cooperation, not control.

DeepSeek's temporary refusal to clearly choose a side precisely indicates it neither wants to be "locked down" nor is satisfied with being just a "plugin". It wants to become societal infrastructure, not a subsidiary of any single giant.

ByteDance's continued heavy investment makes this situation more complex. ByteDance has hardly appeared in DeepSeek financing rumors, not because it's uninterested, but because it's taken another path: self-developing Doubao, heavily investing in C-end entry points. In 2026, ByteDance pushed AI capital expenditure to 200 billion RMB, almost five to six times Tencent's AI investment. ByteDance's logic is straightforward: the ultimate battlefield for AI is user time. Whoever captures the C-end super entry point first holds the initiative. It doesn't need to invest in DeepSeek because Doubao itself is DeepSeek's competitor.

Three companies, three ways of treating external cutting-edge technology. Alibaba wants to "buy, use, and lock it in"; Tencent wants to "buy and use, but not lock"; ByteDance wants to "build it themselves, no need to buy." Behind these three choices are their distinct corporate DNA, resource endowments, and judgments about the AI endgame. DeepSeek's refusal precisely tears open this seam, allowing us a glimpse: in this AI card game, the giants hold different cards, and their play logic naturally differs. To understand where this difference comes from, we must return to the respective starting points of the three companies.

DNA, Foundation, and Strategic Logic: The Two Paths of Alibaba and Tencent

The differences didn't arise from thin air. The AI layouts of internet giants are almost written in their DNA.

Alibaba's DNA is e-commerce, cloud computing, and industrial services. The logic of Taobao is a closed loop: from product to transaction, from payment to logistics, keeping the chain within its own hands as much as possible. This DNA dictates that Alibaba is accustomed to being a controller, not a connector.

So is Alibaba Cloud, insisting on self-research from underlying tech to upper-layer services. Therefore, when DeepSeek emerged, Alibaba could hardly be just a financial investor. It needed a functional module that could integrate into its own AI system, not an independent kingdom.

Tencent follows another logic. Tencent's DNA is social networking, traffic, and ecosystem win-win, accustomed to building open platforms, using capital to connect rather than control.

Whether JD.com, Meituan, or Pinduoduo, Tencent's e-commerce layout relies on investment, not building its own. One core lesson Pony Ma learned from the 3Q War is that "openness is more viable than being closed," which in AI investment means Tencent won't insist on locking DeepSeek into its own drawer.

The maturity of their technological foundations also determines their bargaining power. Alibaba's self-developed AI system has already proven its full-chain capability; T-Head chips are mass-produced and delivered; Tongyi Qianwen is in the same tier as GPT-4o. For Alibaba, an external large model is icing on the cake, not a savior in a snowstorm. Withdrawing from DeepSeek financing is less "talks collapsed" and more that strategically there was no longer an absolute must-invest reason. DeepSeek wanted independent development and financial investment; Alibaba wanted technical integration and ecosystem binding—their demands were fundamentally not on the same dimension.

Tencent's Hunyuan took a different, comeback path. In early 2025, when DeepSeek went viral, Tencent once fully embraced it, and the priority of its self-developed Hunyuan was downgraded. But after heavily poaching former OpenAI scientist Yao Shunyu, Hunyuan was "scrapped and rebuilt," establishing a "co-design" methodology where model and product development advance simultaneously. The Hunyuan Hy3 preview released in April 2026 saw token usage volume exceeding the previous generation by 10 times, taking the "double first" in both usage volume and market share on the OpenRouter platform. Although still lagging behind Doubao and Tongyi Qianwen, the gap has significantly narrowed. Hunyuan's progress makes Tencent more at ease facing DeepSeek: it can acquire top-tier capabilities externally while not losing bargaining power due to lack of self-research.

ByteDance's AI foundation is the most unique among the three. It has no baggage of self-developed large models, no industrial inertia for B-end monetization. Its core goal is to seize the C-end AI entry point by any means. To this end, ByteDance even, against the backdrop of net profit plummeting over 70%, dramatically increased its AI budget to 200 billion RMB. This almost cost-blind investment puts pressure on both Alibaba and Tencent. But Alibaba's budget is scattered across chips, cloud, models, applications, etc., while ByteDance's 200 billion is almost entirely poured into C-end applications and computing power reserves. This focus allowed Doubao to rapidly approach Tongyi Qianwen's monthly active user scale in a short time.

ByteDance's "all-in" gamble is forcing the entire industry to rethink AI's commercialization pace. When a company is willing to trade short-term profits for a long-term entry point, others must either follow suit in burning money or find another path.

A thought-provoking insight is: in the rapidly changing field of AI, the window of technological leadership is getting shorter and shorter. Alibaba uses heavy-asset self-research to build long-term barriers, at the cost of reduced flexibility and narrowed space for external cooperation; Tencent uses light-asset ecosystems to maintain openness, at the cost of needing to continuously catch up in self-research capability; ByteDance uses extreme investment to buy a time window, at the cost of significant short-term profit pressure. None of the three strategies is absolutely superior or inferior.

In summary, DNA determines the path, the foundation determines bargaining power, and strategic logic determines the timing of moves. The advance and retreat at DeepSeek's financing table are all projections of these three multiple-choice questions onto the backdrop of capital.

Closed-Loop Deep Cultivation and Open Integration: Two Parallel AI Futures

Shifting focus away from the financing negotiations, the AI futures of Alibaba and Tencent are actually clear: two paths, unlikely to converge in the short term, and not necessarily one devouring the other in the long run.

Alibaba will continue moving forward along the path of full-stack self-researched closed loops. CEO Wu Yongming has set the tone: making AI Alibaba's main growth engine. Alibaba Cloud's AI-related revenue has seen triple-digit growth for ten consecutive quarters, with a five-year goal of exceeding $100 billion in annual revenue from cloud and AI commercialization. In chips, T-Head is doubling down on domestic GPUs, gradually reducing reliance on Nvidia. Tongyi Qianwen has formed complete capabilities from inference to Agent to multimodal. The Qianwen App has 300 million monthly active users, and WuKong is accelerating penetration in the enterprise market. The three monetization methods—computing power leasing, token fees, and application subscriptions—form a sufficiently deep moat.

Tencent's approach is completely different. On the C-end, it anchors on WeChat, its largest ecosystem, moving towards a "decentralized intelligent entry point"—users don't need to specifically open an AI app but naturally use AI while chatting or browsing videos. On the B-end, WorkBuddy and CodeBuddy are already integrated into WeCom and Tencent Cloud, helping customers improve efficiency. Judging from Hunyuan Hy3's performance, Tencent cares more about whether the model can truly be used, not topping leaderboards. Tencent will continue to strategically place financial investments in quality AI companies, integrating external models into its own scenarios. If the DeepSeek investment materializes, it will be a continuation of this strategy. Tencent's path to profit is more direct: advertising efficiency improvement, game R&D cost reduction, accelerated monetization through cloud and WeChat. In 2026, Tencent Cloud completed three price adjustments, indicating it's gaining pricing power in the AI office domain.

Agents are becoming the next common focal point for both. Alibaba focuses Agent capability as a key breakthrough, with the Qianwen App integrated into ecosystems like Taobao, Alipay, and Fliggy, pioneering AI handling of complex life tasks. Tencent focuses Agent efforts on B-end productivity implementation and platform governance. In multimodal direction, both companies are pushing simultaneously: on April 16, 2026, they both released their respective world model products on the same day, moving the AI competition from language parameters to spatial intelligence. While strategic paths diverge, their judgment on technical direction is surprisingly aligned.

In this protracted war, Alibaba holds two trump cards: computing infrastructure and B-end ecosystem; Tencent occupies the nation's largest C-end traffic pool; ByteDance presses forward on the C-end with 200 billion in heavy investment and Doubao's nearly 400 million monthly active users. Each has its weakness: Alibaba's full-stack barriers are high but hard to dominate the C-end short-term; Tencent's ecosystem is flexible but its Hunyuan self-research still needs to catch up; ByteDance's investment is fierce but net profit pressure will eventually impact its decision-making.

A possible mid-term pattern is: Alibaba guards the B-end and cloud infrastructure; Tencent guards AI embedding in social scenarios; ByteDance captures the C-end independent entry point. The three form a staggered competition, not a fight to the death. For the entire industry, this multipolar pattern is more conducive to technological diversity and innovation vitality than a single monopoly.

What truly decides victory may not be whose model is stronger, but who can first turn AI from a "tool" into a "lifestyle." Alibaba bets that enterprises and developers can't do without its computing power; Tencent bets that users can't do without intelligent assistants within WeChat; ByteDance bets that Doubao becomes the next national-level entry point. All three paths are tough, but none can be easily dismissed.

Returning to the DeepSeek financing negotiation table: Alibaba leaves, Tencent approaches. This is not a disagreement over DeepSeek's pricing, but different answers from two sets of business philosophies. Alibaba builds a "castle": high walls, deep moats, self-sufficient. Tencent builds a "port": ships freely come and go, water surface prosperous. In the rapidly changing field of AI, there is no absolute superiority between "castle" and "port." The only certainty is that DeepSeek's massive financing in May is destined to become the page marking the fork in the AI road for China's internet giants.

This article is from the WeChat public account "BizWhale" (ID: bizwhale), author: Hu Duzhi