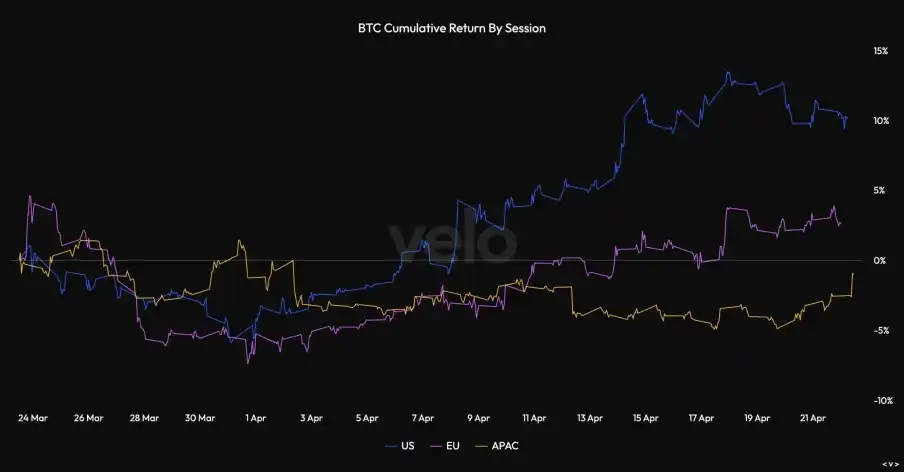

Over the past month, Bitcoin's price action seems to be sending a signal: when Strategy enters the market, BTC finds support; conversely, once Strategy temporarily steps back, the market quickly weakens.

Last week, the company spent $2.54 billion to buy 34,164 BTC, bringing its total holdings to 815,061 BTC. Strategy's TWAP strategy has injected real spot demand into the market, while the market is still watching: near the key resistance level of $80,000, can the current trend stabilize independently?

Looking back at March, after the ex-dividend week, Strategy significantly slowed its pace of buying BTC, which in turn dragged down BTC's price. The reason BTC managed to hold its price was entirely due to Strategy's support. The subsequent trend depends entirely on whether this buying persists after the ex-dividend window closes.

The March price action already exposed the risks. Strategy aggressively bought during the window, then went quiet, and BTC's price almost immediately "lost momentum and fell." Entering the post-ex-dividend period in April, the situation was exactly the same. The real question now is, once the ex-dividend window closes, will Strategy continue to buy.

If April can avoid repeating March's "post-ex-dividend weakness," the bullish logic will be much stronger. If not, it's just a repeat of last month's old script.

Core Summary (TL;DR)

- Marginal Buying: Strategy is the largest marginal buyer in the market. The recent rally during US trading hours proves that much of Bitcoin's gains over the past month were largely driven by it.

- March's Script: Strategy bought BTC aggressively before the $STRC ex-dividend window, but BTC's price plummeted in the following two weeks.

- April's Difference: As of April 22nd, BTC has not yet experienced post-ex-dividend weakness and remains firm around $77,500.

- Key Signal: The upcoming 8-K filing (due April 27th) is crucial, as it will determine whether Strategy is still buying after the ex-dividend window closed.

- Long-term Risk: Strategy's high dividend yield of 11.5% is costly. If capital markets tighten, they may eventually be forced to sell BTC or dilute shares to fund it.

Bitcoin's Largest Marginal Buyer: Strategy

Over the past month, almost all of BTC's gains occurred during US trading hours. This was partly thanks to spot ETFs, but more due to buying pressure from Strategy. The best perspective to understand this rally is not a vague "risk-on" bounce, but rather concentrated US-based buying意愿 supported by ETF flows. Farside's daily data shows net inflows of approximately $1 billion, highlighting tangible market demand.

However, this alone isn't enough to fully explain the price action. In the week ending April 19th, Strategy's massive $2.54 billion purchase exceeded the net inflows into ETFs. This supports a more reasonable interpretation: it's not that "ETFs were absent," but that both ETFs and Strategy were buying, and Strategy's buying volume is substantial enough to be one of the most important marginal buyers in the market, which also perfectly matches the chart during US hours. Since almost all gains happened during US hours, and one of the largest US buyers spent $2.54 billion, Strategy's absolute influence on BTC's price is self-evident.

The Real Test of the Rally Comes After the Ex-Dividend Date

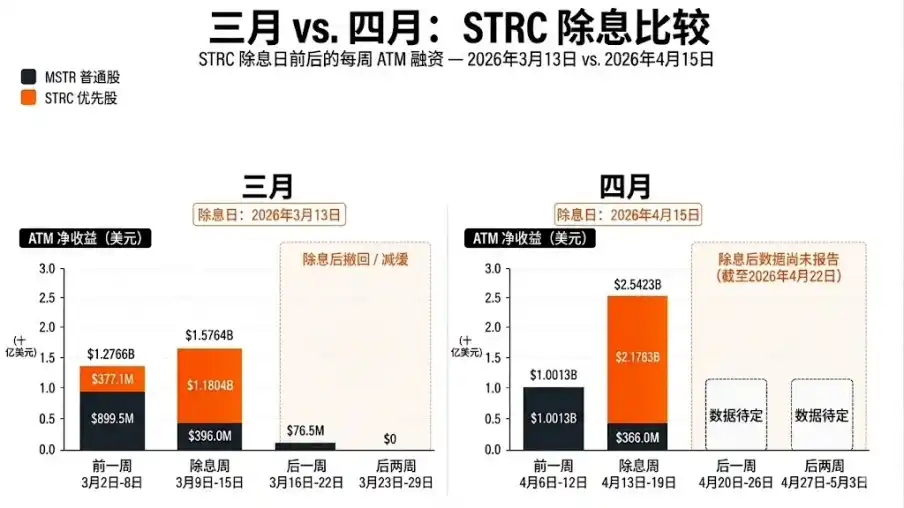

In March, Strategy bought frantically during the $STRC ex-dividend window, but BTC's price fell sharply in the subsequent two weeks. In the week ending March 22nd, demand for $STRC plummeted from $1.18 billion to a mere $76.5 million. ATM (At-The-Market) offerings for MSTR common stock also dropped to zero. By the week ending March 29th, total proceeds from ATM offerings were directly zero. This was also the first time in 13 weeks that Strategy did not buy any BTC at all.

Strategy's two-week disappearance, coupled with BTC's decline during the same period, is the clearest case proving Strategy's decisive role in BTC's price movement. BTC fell all the way to just over $70,000, touching around $70,400 on March 20th and around $70,600 on March 23rd. The price action reflected reality: when STRC issuance stopped, and MSTR common stock didn't fill the gap, buying power weakened significantly.

Therefore, the core question now is whether April will replay March's "hangover" or break the spell.

The next 8-K filing (due April 27th) will cover the week ending April 26th. If STRC issuance again falls to levels that can be considered margin of error, and MSTR common stock ATM offerings remain stalled near zero, then April is just an amplified version of March, not a true paradigm shift. However, if STRC remains active, and MSTR common stock ATM offerings reach a considerable size (over $150 million), then the script has truly changed.

April is Crucial Because BTC Has Held Firm So Far

April 15th, 2026 was the ex-dividend date for $STRC in April, with STRC's annualized dividend yield remaining at 11.50%. In the week ending April 19th, Strategy raised $2.5 billion and bought 34,164 BTC, releasing enormous demand. However, the real focus is on BTC's performance afterwards: unlike March, BTC did not immediately experience a price plunge.

One could argue that Strategy has changed market dynamics. But the upcoming filing is much more important than the last one. If the usual "post-ex-dividend weakness" appears again, then April might just be a replay of March's performance. If it doesn't, then the market must seriously consider that Strategy is not just buying during the window, but is supporting BTC over a longer time horizon.

Will the Buying Continue?

This is the part traders really care about.

Simply noting that Strategy bought a lot of BTC last week won't make money. What truly matters is whether this buying will continue once the pure ex-dividend day logic plays out.

The experience from March tells us that a strong ex-dividend week alone is not enough. Strategy bought 22,337 BTC in the reporting period ending March 15th, but was largely absent in the following two weeks, and BTC's price weakened accordingly.

April's performance suggests there might be a turnaround, as Strategy bought even more—a full 34,164 BTC—and BTC's price action has not yet repeated March's decline.

The logic here is very straightforward. If the next 8-K filing shows substantial buying continued after the ex-dividend date, the market must assume this buying is still active. If it shows issuance plummeting again, it indicates that March's performance is their fixed modus operandi, not a coincidence.

Why It's Bullish Now—But Future Concerns Linger

As of April 2026, STRC's annualized dividend yield is as high as 11.50%. As long as the market is happy to buy this structure and the BTC price cooperates by rising, this isn't a problem. But if BTC stagnates and capital markets become less generous, things could get very tricky.

Although this is a medium-term issue, not the immediate trading logic, the risk is客观存在的 (objectively exists). This flywheel only works perfectly when BTC is rising and investor appetite is strong.

Therefore, the purest understanding is: As long as Strategy is still buying, it is bullish for BTC, but this does not mean its funding structure is without risk. It's just that for now, the market only needs to focus on the first half of that sentence.

Final Conclusion

Recent BTC price action looks like a market propped up by an extraordinary super marginal buyer. March showed us what happens when that buyer disappears. When Strategy's $STRC stopped raising capital in the first two weeks after the ex-dividend date, April's price action is likely to follow suit.

So, the right way to read the current market is not to obsess over the headline number of the last purchase, but to ask a simpler question: Once the obvious window closes, is Strategy still bidding for BTC?

If the answer is yes, BTC will likely continue to find support. If the answer is no, then BTC will soon experience what it's like to "lose the support of its largest visible marginal buyer." If it can still rise then, that would be an ultimate bullish signal.