Article Author: Thejaswini M A

Article Translation: Block unicorn

Preface

There is a category of companies that actually benefit when the world situation deteriorates. Defense contractors, oil giants, gold mining companies. These are the obvious examples, companies whose business models are built on instability and factor that instability into their pricing.

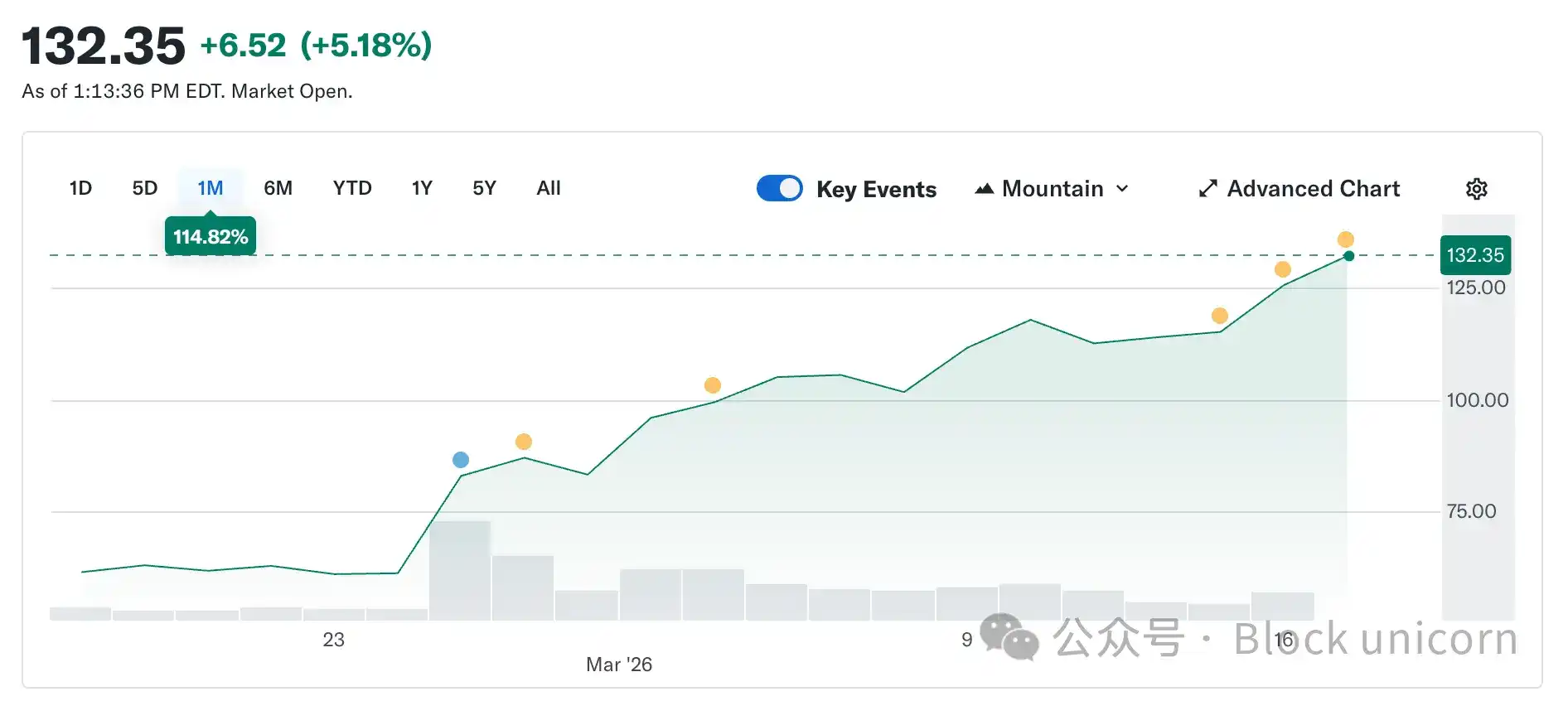

Circle was not supposed to be in this category. Its token is always worth $1, by design. Stability is the core of its product. Yet, Circle's stock price has soared from $49.90 on February 5th to around $123 today, more than doubling in just over five weeks. Meanwhile, the entire cryptocurrency market is still down 44% from its October peak.

As the world becomes increasingly turbulent, a company whose product is designed to maintain a stable price has become one of the market's hottest trades.

I want to explain how this works, why it's more interesting than it seems, and what it tells us about the difference between what Circle is and what the market is currently paying for.

What is Circle (Of course, we'll come back to this)

Strip away the branding, the payment concepts, and the infrastructure building, and you find the essence of Circle: it holds U.S. Treasury bonds. Every dollar of USDC in circulation is backed by one dollar's worth of short-term government bonds. The interest on these bonds belongs to Circle. This accounts for about 90% of the company's revenue each quarter. Its business model is not complicated: Circle is a money market fund that issues a stablecoin.

This means Circle's revenue has only one key factor: the federal funds rate. When interest rates are high, Treasury yields are high, and Circle earns more for every USDC it issues. When rates are low, revenue decreases. Everything else is secondary.

Here is the sequence of events that led to the 150% rebound in the stock price from its February low.

Since February 28th, the Iran conflict has pushed oil prices up by about 35%. Oil above $100 means inflation worries, and inflation worries mean the Fed would be seen as reckless to cut rates. Holding rates steady on March 18th was practically a foregone conclusion. Even before the war, the CME's FedWatch showed a probability of over 90% for no change. What the war really affected was the market's outlook for the entire year. Before the conflict, the market expected two 25-basis-point cuts in 2026. After the conflict, that was reduced to one cut, and not until after September. The probability of no cuts at all in 2026 nearly doubled. With rates staying higher for longer, the yield on Circle's Treasury reserves continues to be high. Higher yields mean more revenue. More revenue means a higher stock price. War breaks out, and a stablecoin issuer benefits. This was completely unexpected.

For context, the bearish expectation that drove Circle's stock down to $49 in February was essentially a bet on rate cuts. The market expected the Fed to cut multiple times in 2026, which would directly compress Circle's reserve income. A rough estimate: at the current USDC supply of $79 billion, each 25-basis-point cut would reduce Circle's annualized revenue by $40-60 million. Two cuts would reduce its revenue by nearly $100 million by year-end. The war changed this expectation overnight. Not because Circle itself changed, but because the macroeconomic backdrop that was supposed to weaken the thesis no longer applicable.

How the Squeeze Started

While the interest rate story keeps the stock price high, the initial explosive rise came from positioning.

Before the Q4 earnings report on February 25th, about 17.8% of Circle's float was sold short. Hedge funds had built significant short positions. Their logic was that rates would eventually fall, reserve income would decrease, and the company had no minimum revenue floor independent of rates. From a fundamental perspective, this argument seemed sound. Then, Circle reported EPS of $0.43, beating the consensus estimate of $0.16. Revenue was $770 million, above the expected $749 million. On-chain USDC volume approached $12 trillion for the quarter, up 247% year-over-year. The shorts covered. The stock surged 35% in a single trading day. According to 10x Research, hedge funds lost about $500 million on their short positions in one day. Subsequently, this short squeeze intensified, extending the post-earnings gains.

The Coinbase Problem

Here is the part that doesn't make it into the rally narrative.

Circle had a net loss of $70 million in 2025, not a profit. Q4 was excellent, but the full year was not. To understand why, you need to know about the Coinbase agreement, which is the most important yet most overlooked key to Circle's business.

When USDC was first launched in 2018, Circle and Coinbase formed a joint consortium to manage it. The consortium was dissolved in 2023, and Circle took full control of USDC issuance. However, Coinbase retained a share of the revenue.

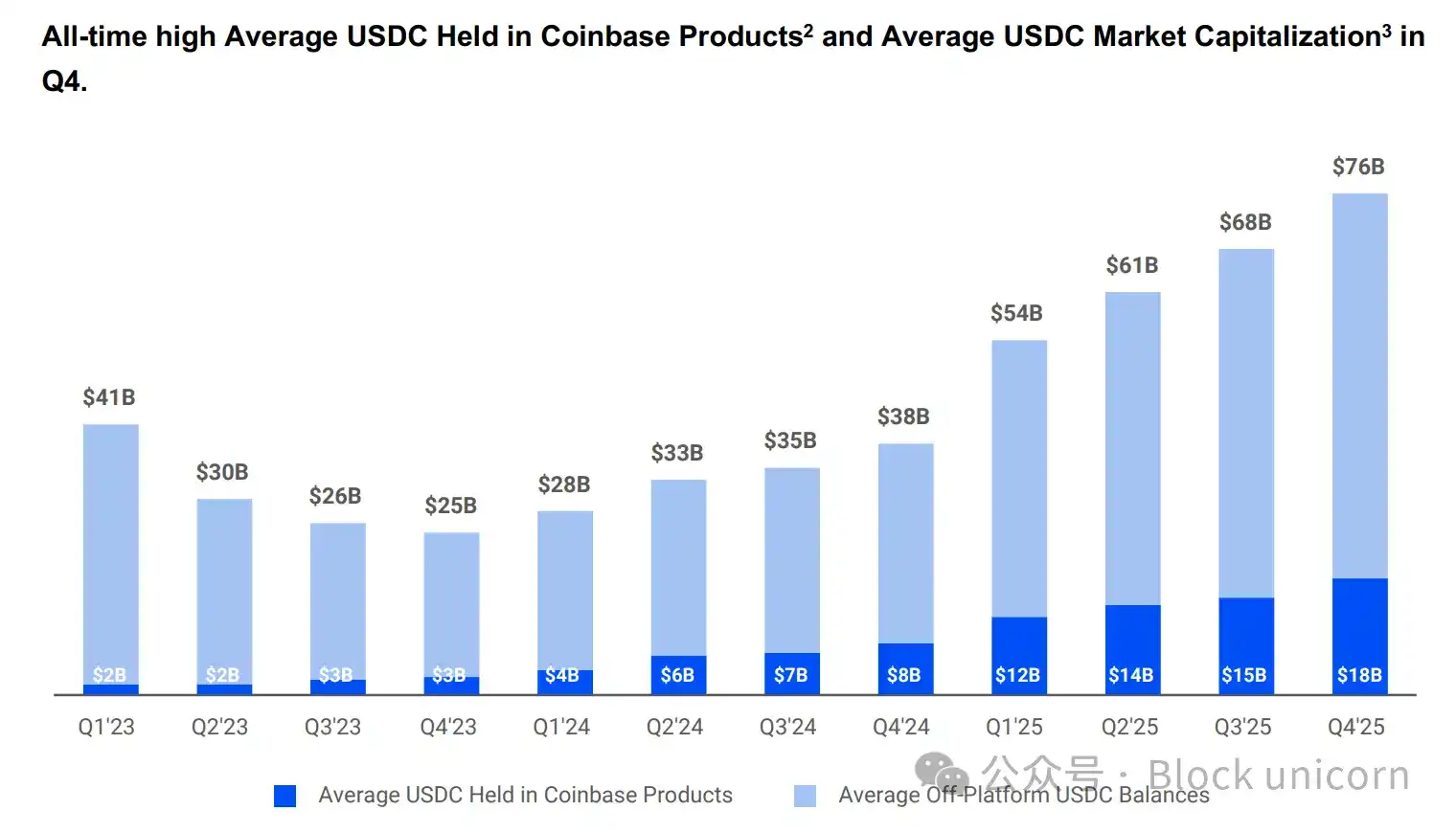

Coinbase takes 100% of the reserve income from USDC held on its platform and splits everything else 50/50 with Circle. In 2024, this arrangement sent $908 million of Circle's total distribution cost of $1.01 billion directly to Coinbase. Roughly 54 cents of every dollar Circle earns flows to a company that doesn't issue the token or handle the reserves. By early 2025, Coinbase held 22% of the total USDC supply, up from 5% in 2022. The more USDC grows on Coinbase's platform, the more revenue flows to Coinbase.

The agreement automatically renews every three years, and Circle cannot unilaterally exit it. The outcome of the next renegotiation will directly impact Circle's margins. In Q4 2025, distribution costs alone were $461 million, up 52% year-over-year. The full-year net loss of $70 million was partly due to a one-time post-IPO stock-based compensation expense of $424 million, which made the book loss look worse than the actual business condition. But Circle's core business still faces a structural cost problem that no interest rate environment can completely solve.

The market is pricing Circle as infrastructure. The income statement shows it's an interest rate trade with high distribution costs. Both views can be true, but they are priced differently. Right now, the market is paying for the best version of both views simultaneously.

What Makes This More Than Just a Macro Trade?

The recent USDC supply reached a new all-time high of $79 billion, while the entire crypto market is down 44% from its October peak. This divergence is worth noting. Speculative assets typically fall when the market falls. The reason USDC continues to grow is that people use it to move money, not hold it as a speculative asset. During the Iran conflict, demand for USDC surged in the Middle East precisely because the traditional banking system became unreliable. When normal payment channels break down, people use USDC for remittances and cross-border transfers. This is how payment infrastructure behaves under stress: usage increases, not decreases.

Transaction data confirms this. In February alone, adjusted USDC volume was about $1.26 trillion, compared to USDT volume of $514 billion over the same period. Even though Tether's market cap remains much larger at $184 billion versus USDC's $79 billion. The total supply gap is vast. But USDC's transaction volume now exceeds that of USDT.

Dormant supply and active settlement are two different concepts. The former refers to where people park their money, the latter refers to what people use when they need to move value.

Druckenmiller made an enlightening point this week. In a Morgan Stanley interview recorded on January 30th and released earlier, he said he expects the global payment system to be based on stablecoins in the next 10 to 15 years and called crypto "a solution looking for a problem." One of the most authoritative macro investors of our time perfectly split the crypto space in two: stablecoins as inevitable infrastructure, and everything else still looking for a reason to exist. This is the bullish thesis for crypto.

The Infrastructure Bet

Tokenized assets have grown from about $1.5 billion in early 2023 to about $26.5 billion today. Many of these products, including BlackRock's tokenized treasury fund BUIDL (now holding over $2 billion in assets), rely on USDC for subscription, redemptions, and settlement processing. Prediction markets processed over $22 billion in volume in 2025, mostly settled in USDC. Polymarket alone. Visa now supports over 130 stablecoin-linked cards across 50 countries, with an annualized settlement volume of about $4.6 billion.

Tokenized assets have grown from about $1.5 billion in early 2023 to about $26.5 billion today. Many of these products, including BlackRock's tokenized treasury fund BUIDL (now holding over $2 billion in assets), rely on USDC for subscription, redemptions, and settlement processing. Prediction markets processed over $22 billion in volume in 2025, mostly settled in USDC. Polymarket alone. Visa now supports over 130 stablecoin-linked cards across 50 countries, with an annualized settlement volume of about $4.6 billion.

Circle is also building the infrastructure underneath all of this. The Circle Payment Network connects 55 financial institutions with $5.7 billion in annual volume, enabling banks and payment providers to move USDC cross-border and convert it directly into local currency. Circle's own Layer-1 blockchain, Arc, is designed for full institutional support. Its settlement infrastructure does not rely on Ethereum or Solana. While Ethereum and Solana are not yet large enough to impact revenue, they are both forward-looking strategic investments for a future where rates might be lower.

The AI layer, while small in amount, is significant. Data released by Circle's Global Head of Marketing in March showed that over the past nine months, AI agents completed 140 million payments totaling $43 million. 98.6% of these transactions were settled in USDC, with an average transaction size of $0.31. Over 400,000 AI agents now have purchasing power. While the amounts are still small, the direction is clear. If AI agents need to pay each other for compute, data access, and API calls with extremely high frequency and极光very small amounts (under $0.25), they need a payment method that settles instantly and costs nothing. Circle built Nanopayments for this. Nanopayments offer gas-free USDC transfers as low as $0.000001, with transactions batched off-chain and settled in batches. The testnet currently supports 12 blockchains including Arbitrum, Base, and Ethereum.

This is what the market is currently paying $123 per share for Circle. A company at the center of tokenized finance, AI agent commerce, cross-border payments, and prediction markets, benefiting from the regulatory tailwinds of the GENIUS Act and the potential passage of the CLARITY Act before summer. Bernstein has a $190 price target, Clear Street has a $136 target, and Seaport Global, the most bullish on Wall Street for Circle, has a $280 target.

The Lingering Tension

Here, I want to be candid about what the bullish narrative often glosses over.

Circle's profitability relies on a high-interest-rate environment. But this is not sustainable. The Fed will eventually cut rates. When that happens, the yield on the Treasuries backing USDC will fall, and Circle's interest income will decrease accordingly.

Circle knows this. It has been expanding into transaction fees, corporate services, payment networks, and Arc. These businesses operate independently of the interest rate environment. But currently, this revenue is minimal. Reserve income remains the key.

So you have these two situations sitting on the same stock price, but they are not the same investment.

The infrastructure thesis argues that USDC is becoming a genuine payment pipeline. It is regulated, transparent, and increasingly integrated into the traditional financial system, and its utility is not affected by interest rate fluctuations. This thesis is supported by data such as transaction volume, institutional integration, Druckenmiller's comments, and Macquarie calling stablecoins the foundational layer of global financial infrastructure. If this thesis is correct, then Circle is undervalued regardless of the interest rate environment, because its potential market covers the entire global payment system.

The interest rate trade thesis argues that Circle is a bet on rates staying high for a long time, and the stock price already reflects the expectation that the Fed will not cut significantly. If this thesis is the driver of the stock price, then every percentage point the Fed eventually cuts will be a headwind, and the stock is already priced above what fundamentals would support under normal rates.

Both views are priced in. The war makes it difficult for the market to decide which one it favors.

Perhaps the most important thing to understand about CRCL right now is not whether it can reach $190, but whether you are investing in infrastructure or a better-marketed Treasury yield proxy. The former is a long-term hold, the latter expires the moment Jerome Powell changes his mind.

For now, the war is keeping both alive. Oil prices played a key role, and the company's true value lies somewhere in the blank space between these two scenarios: it has figured out how to create internet money denominated in dollars, but now it has to figure out how to survive when dollar yields are no longer 5%.