Competition between chains has escalated to the level of "transaction ordering," which directly impacts market makers' bid-ask spreads and depth🧐🧐

The demand for "general-purpose chains" has been disproven. Current chain-to-chain competition focuses on two levels:

1) Building "application chains" on the foundation of existing mature businesses, allowing blockchain to supplement existing operations in areas like settlement;

2) Competition at the level of "transaction ordering."

This article focuses on the second level.

Ordering directly influences the behavior of market makers. This is the core issue.

What is Transaction Ordering?

On-chain, user transactions are not immediately written to a block; they first enter a "waiting area" (Mempool). There may be thousands of transactions simultaneously, and it must be decided by a sequencer, validator, or miner:

1) Which transactions are included in the next block?

2) In what order are these transactions arranged?

The process of "deciding the order" is transaction ordering, which directly affects the transaction costs for on-chain users, MEV conditions, transaction success rate, and fairness.

For example, during network congestion, ordering determines whether a transaction can be quickly added to the chain or waits indefinitely in the mempool.

For high-frequency traders like market makers, whether a cancellation order takes effect is more critical than a placement order succeeding. The priority given to processing cancellation orders directly impacts whether market makers dare to offer deep liquidity.

In the last cycle, everyone pursued TPS, believing that speed alone could improve on-chain transaction settlement. But it has been proven that, besides speed, the risk pricing of market makers is equally important.

On centralized exchanges, trade matching strictly follows the "price-time priority" principle. In this highly deterministic environment, market makers can provide deep order book liquidity with extremely narrow spreads.

On-chain, after transactions enter the Mempool waiting area, nodes select transactions based on Gas fees, which creates room for sniping existing orders by offering higher Gas.

Suppose TRUMP is priced at $4.5, and a market maker places a buy order at $4.4 and a sell order at $4.6 to provide depth. But the exchange price of TRUMP suddenly crashes to $4.

At this point, the on-chain market maker wants to cancel the $4.4 buy order but gets sniped by a high-frequency trader offering higher Gas—buying at $4 and selling to the market maker at $4.4.

Therefore, market makers can only widen their spreads to reduce risk.

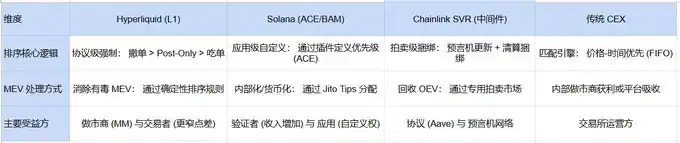

The purpose of the new generation of ordering innovations is to transition from "general ordering" to "Application-Aware Sequencing."

The ordering layer can understand transaction intent and order based on preset fairness rules, not just based on Gas fees.

1) Define the ordering method at the consensus layer

A typical case is Hyperliquid. It stipulates at the consensus layer that cancellation and Post-Only transactions take priority, breaking the Gas priority rule.

For market makers, being able to exit is paramount. During sharp price fluctuations, cancellation requests are always executed before others' takers.

Market makers fear being sniped the most. Hyperliquid precisely guarantees that cancellations are always prioritized—when the price drops, market makers cancel their orders, and the system forcibly prioritizes processing the cancellations, allowing market makers to successfully hedge risks.

On the day of the 10.11 crash, Hyperliquid market makers stayed online continuously, with spreads of 0.01–0.05%. The reason is that market makers knew they could get out.

2) Add new ordering methods at the sequencing layer

For example, Solana's Application Controlled Execution (ACE). Jito Labs developed BAM (Block Assembly Marketplace), introducing specialized BAM nodes responsible for transaction collection, filtering, and ordering.

Nodes run in a Trusted Execution Environment (TEE), ensuring the privacy of transaction data and the fairness of ordering.

Through ACE, DEXs on Solana (like Jupiter, Drift, Phoenix) can register custom ordering rules with BAM nodes. For example, market maker priority (similar to Hyperliquid), conditional liquidity, etc.

Additionally, proprietary AMM market makers like HumidiFi represent innovation at the ordering level, using Nozomi to connect directly with major validators to reduce latency and complete transactions.

During specific transactions, HumidiFi's off-chain servers monitor prices across platforms. The oracle communicates with the on-chain contract to inform it of the situation. Nozomi acts like a VIP channel, allowing effective order cancellation before execution.

3) Utilizing MEV facilities and private channels

Chainlink SVR (Smart Value Recapture) focuses on the归属 (belonging) of the value generated by ordering (MEV).

By deeply integrating with oracle data, it redefines the ordering rights and value distribution of liquidation transactions. After generating a price update, Chainlink nodes send it through two channels:

1) Public channel: Sent to the standard on-chain aggregator (serving as a backup, but in SVR mode, there is a slight delay to leave an auction window).

2) Private channel (Flashbots MEV-Share): Sent to an auction market supporting MEV-Share.

This way, the auction proceeds from liquidations triggered by oracle price changes in lending protocols (i.e., the amount searchers are willing to pay) are no longer solely captured by miners; most are captured by the SVR protocol.

Summary

If TPS is the entry ticket, then having only TPS is completely insufficient now. Custom ordering logic might not just be an innovation but a necessary path for putting transactions on-chain.

It might also be the beginning of DEXs surpassing CEXs.