来源:Tiger Research

作者:Ryan Yoon

原标题:Is This a Crypto Winter? Post-Regulation Market Shift

编译即整理:BitpushNew

随着市场进入下行周期,对加密市场的怀疑正在与日俱增。当下的核心问题是:我们是否已经进入了“加密熊市”?

核心观点

-

加密寒冬的演变路径: 重大事件 → 信任崩塌 → 人才流失。

-

本轮周期的特殊性: 过去的寒冬由内部问题引发;而当前的暴涨与暴跌均由外部因素驱动。目前既非“寒冬”,也非“暖春”。

-

监管后的三层市场结构: 市场已分裂为合规区、非合规区以及共享基础设施;过去的“滴漏效应(Trickle-down effect)”已经消失。

-

ETF 资金的局限性: 资金停留在比特币内部,并不会流向合规区之外。

-

下一轮牛市的前提: 需要“杀手级应用”的诞生,加上有利的宏观经济环境。

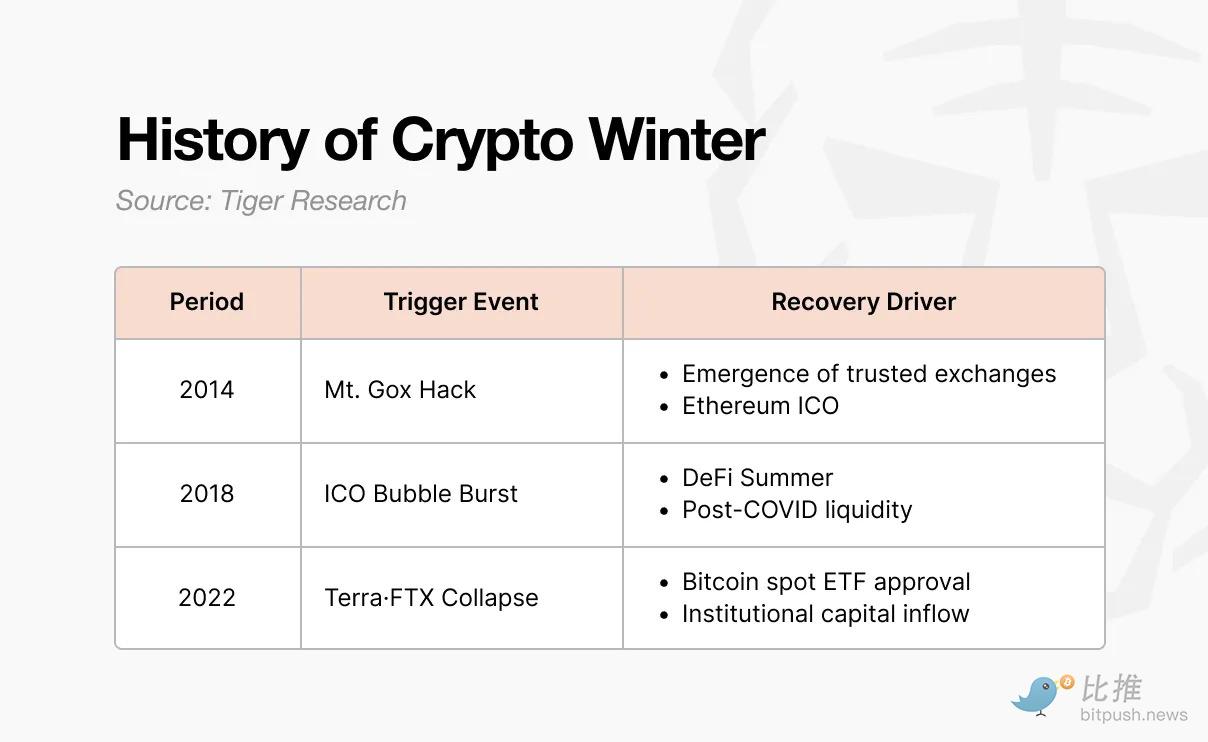

1. 历次加密寒冬是如何演变的?

第一次寒冬发生在 2014 年。 当时 Mt. Gox 交易所处理了全球 70% 的比特币交易量。由于黑客攻击,约 85 万枚 BTC 凭空消失,市场信任彻底崩塌。随后,具备内部控制和审计功能的各种新交易所开始涌现,信任才得以缓慢修复。与此同时,以太坊通过 ICO(首次代币发行)诞生,为行业展现了新的愿景和融资方式。

这一 ICO 模式成为了下一轮牛市的火种。 当任何人都能发行代币并筹集资金时,2017 年的狂热被点燃了。仅凭一份白皮书就能融资数百亿的项目层出不穷,但其中大多数毫无实质内容。

2018 年,韩国、中国和美国相继出台严厉监管措施,泡沫破裂,第二次寒冬降临。 这次寒冬一直持续到 2020 年。新冠疫情后,流动性开始涌入,Uniswap、Compound、Aave 等 DeFi 协议受到关注,资金重新回流。

第三次寒冬最为惨烈。 2022 年 Terra-Luna 崩盘,引发了 Celsius、Three Arrows Capital 和 FTX 的接连倒闭。这不仅是简单的价格下跌,而是整个行业的结构遭到了动摇。直到 2024 年 1 月,美国证监会(SEC)批准了比特币现货 ETF,随后伴随着比特币减半和特朗普的亲加密货币政策,资金才再次开始流入。

2. 加密寒冬的模式:重大事件 → 信任崩塌 → 人才流失

前三次寒冬都遵循了同样的演变逻辑:一个重大负面事件触发,导致信任体系崩溃,最终引发人才大规模流失。

-

始于重大事件: 无论是 Mt.Gox 被黑、ICO 监管打击,还是 Terra-Luna 崩盘及随后的 FTX 破产,虽然规模和形式各异,但结果如出一辙——整个市场陷入震荡和恐慌。

-

蔓延至信任崩塌: 这种冲击很快转变为信任危机。曾经讨论“下一步该建什么”的人们开始质疑加密技术是否真的具有实际价值。建设者之间的协作氛围消失,取而代之的是互相指责。

-

引发人才流失: 对前景的怀疑导致了人才撤离。那些曾在区块链领域创造动力的建设者陷入了悲观情绪。2014 年,他们流向了金融科技和大厂;2018 年,他们转向了传统机构和 AI 领域。他们离开这里,去了看起来更确定的地方。

3. 现在是加密寒冬吗?

从表面上看,过去加密寒冬的某些迹象在今天依然清晰可见:

-

重大事件:

-

特朗普迷因币(Trump memecoin): 市值曾在一天内达到 270 亿美元,随后暴跌 90%。

-

“10.10”爆仓事件: 美国宣布对华征收 100% 关税,引发币安史上最大规模的爆仓潮(190 亿美元)。

-

信任崩塌: 怀疑论在行业内蔓延,讨论重心从“建设”转向了“甩锅”。

-

人才流失压力: AI 行业飞速增长,提供了比加密货币更快、更丰厚的变现路径。

然而,很难将当前定义为典型的“加密寒冬”。 过去的寒冬爆发于行业内部——Mt. Gox 被黑、ICO 归零、FTX 暴雷,这些都是行业自毁长城。

现在的情况截然不同:

ETF 的获批开启了牛市,而关税政策和利率变动驱动了下跌。是外部因素拉升了市场,也是外部因素拖累了市场。

建设者们也并未离场:

RWA(现实世界资产)、perpDEX(永续合约交易所)、预测市场、InfoFi、隐私协议等新叙事层出不穷,且仍在持续迭代。虽然它们没有像当年的 DeFi 那样拉动全盘上涨,但它们并未消失。行业基本面没有崩溃,只是外部环境变了。

正如我们并未亲手创造这个“暖春”,所以目前也没有所谓的“寒冬”。

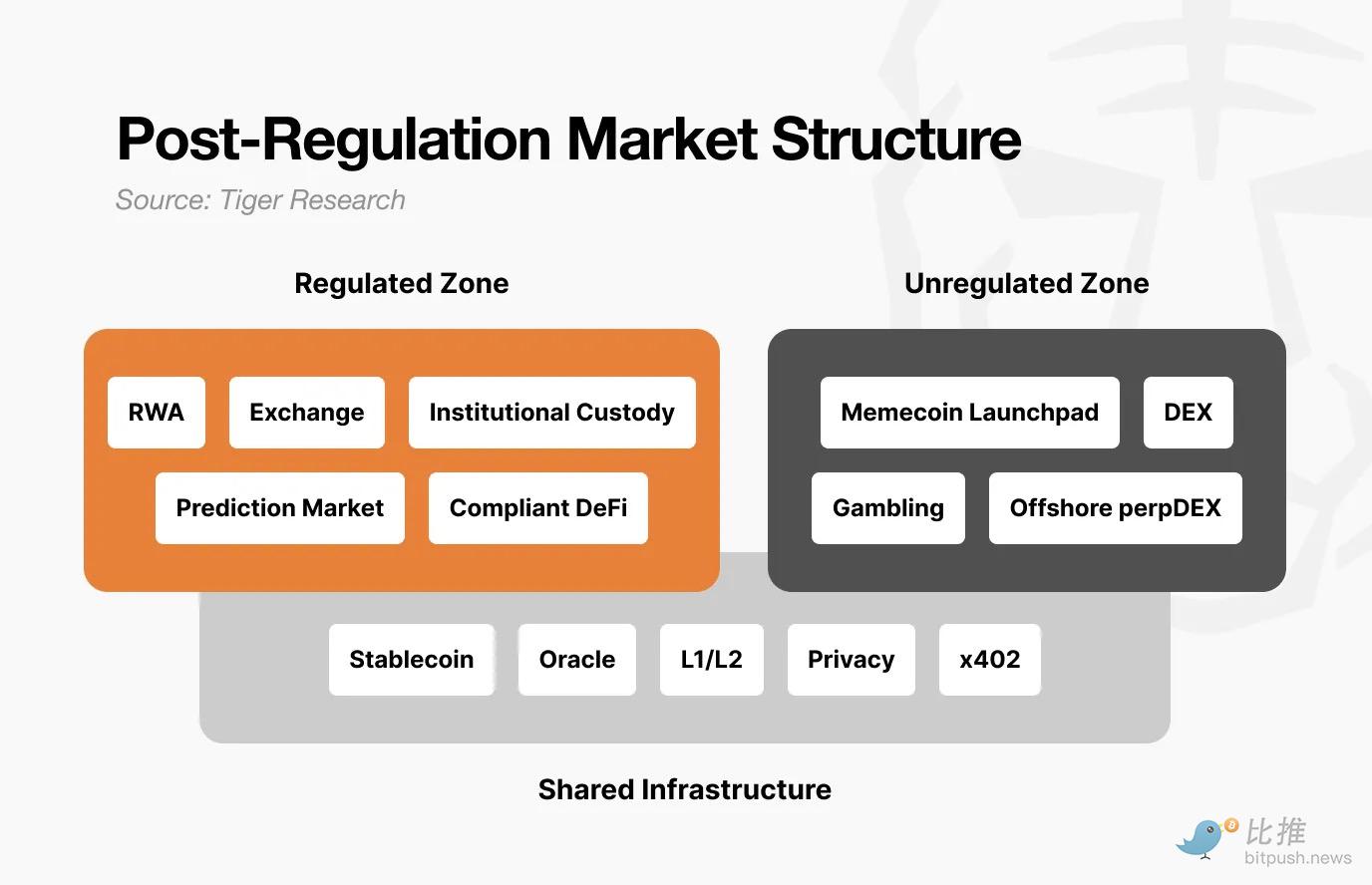

4. 监管后市场结构的根本性变化

在这种现象背后,是监管后市场结构的深刻演变。目前市场已经分化为三个层面:1) 合规区,2) 非合规区,3) 共享基础设施。

-

合规区: 包括 RWA 代币化、持牌交易所、机构级托管、合法预测市场以及合规 DeFi。这些领域接受审计、履行披露义务并受法律保护。虽然增长较慢,但资金规模巨大且稳定。

-

特点: 进入合规区后,很难再期待过去那种爆发式的百倍收益。波动性降低,上限受限,但下限也同样有了保障。

-

非合规区: 这一领域未来的投机色彩将更加浓厚。门槛低、节奏快,今天暴涨 100 倍、明天跌去 90% 将成为常态。

-

意义: 这一空间并非毫无意义。非合规区是创意的摇篮,一旦某个赛道被验证有效,它就会向合规区转移(如当年的 DeFi 和现在的预测市场)。它起到了“实验场”的作用,但其本身将与合规业务日益剥离。

-

共享基础设施: 包含稳定币和预言机。它们同时服务于两个区域。同一枚 USDC 既可以用于机构级的 RWA 支付,也可以用于 Pump.fun 的投机交易;预言机既为代币化国库提供数据验证,也为匿名 DEX 的强平提供支持。

这种分化改变了资金的流动路径。

在过去,比特币上涨会通过“滴漏效应”带动山寨币齐涨。现在不同了:通过 ETF 进场的机构资金停留在比特币内便戛然而止,合规区的资金不再流向非合规区。 流动性只停留在价值被证明的地方。甚至比特币本身,作为避险资产的属性也尚未在风险资产面前得到充分证明。

5. 下一轮牛市的条件

监管框架正在完善,建设者仍在耕耘。接下来还需要满足两个条件:

-

非合规区诞生新的“杀手级应用”: 必须出现像 2020 年“DeFi 之夏”那样能创造全新价值的事物。AI 代理、InfoFi、链上社交都是潜在候选,但目前尚未达到触动全局的规模。必须再次形成“非合规区实验 → 验证成功 → 向合规区迁移”的良性流动。

-

宏观经济环境的配合: 即便监管尘埃落定、建设者努力、基建完善,如果宏观环境不支持,上涨空间依然有限。2020 年的 DeFi 热潮爆发于疫情后的全球大放水;2024 年 ETF 后的上涨也恰逢降息预期。无论加密行业自身做得多好,它都无法控制利率和流动性。行业内所构建的价值要获得广泛认可,宏观环境必须反转。

像过去那样“普涨”的加密赛季不太可能再现。 因为市场已经彻底分裂。合规区将稳步增长,而非合规区将继续剧烈波动。

下一轮牛市终会到来,但它不会眷顾每一个人。

Twitter:https://twitter.com/BitpushNewsCN

比推 TG 交流群:https://t.me/BitPushCommunity

比推 TG 订阅: https://t.me/bitpush