Pada 11 Oktober, USDe, pemimpin pasar YBS (stablecoin berbunga) mengalami kehilangan patokan di Binance, bursa crypto lepas pantai terbesar di dunia, memicu likuidasi berantai dan mencatatkan rekor likuidasi terbesar dalam sejarah pasar perdagangan cryptocurrency (perkiraan konservatif 19 miliar dolar AS). 'Crash Cryptocurrency' seketika menjadi kata kunci yang menarik perhatian media berita global.

Namun sebagai profesional, kita perlu menyingkirkan kabut kebisingan yang diciptakan media massa yang gemar menciptakan cerita yang disukai orang, dan langsung menyentuh esensi dari kehilangan patokan YBS 10·11—paparan super risiko ekor dari rekayasa keuangan yang kompleks, untuk mempelajari bagaimana model kompleks, leverage tinggi, likuiditas, risiko sistemik, dan kepercayaan diri yang berlebihan bergabung menjadi seperti apel Eden yang secara rasional menghancurkan diri manusia.

USDe: Ciptaan Estetika Rasionalisme Teknik Keuangan

Sebelum Crypto merendahkan diri menjadi infrastruktur keuangan generasi berikutnya di Amerika, legitimasi Crypto berakar pada penciptaan mata uang berbasis rasionalisme matematika murni yang bertujuan untuk menjamin kebebasan individu.

Setelah mengalami kegagalan eksperimen mata uang era Coin blockchain PoW dalam siklus inovasi teknologi pertama, dan keruntungan sistemik stablecoin algoritmik era Token kontrak pintar dalam siklus inovasi teknologi kedua, pelaku Crypto dalam siklus inovasi teknologi ketiga masih tidak dapat menahan keinginan menciptakan yang setara dengan dewa untuk menciptakan stablecoin generasi baru—synthetic stablecoin yang didukung pendapatan nyata YBS.

Berbeda dengan optimisme utopis stablecoin algoritmik (yang telah dilarang oleh undang-undang regulasi crypto global yang sekarang diterapkan) yang merupakan abstraksi matematika sederhana dan smart contract-ifikasi dari mekanisme penerbitan uang Federal Reserve, YBS sejak awal adalah sistem keuangan kompleks yang dibangun berdasarkan rasionalisme teknik keuangan, dimulai dari ide awal Nakadollar yang diusulkan Arthur Hayes dalam blognya tahun 2023 'Dust on Crust'.

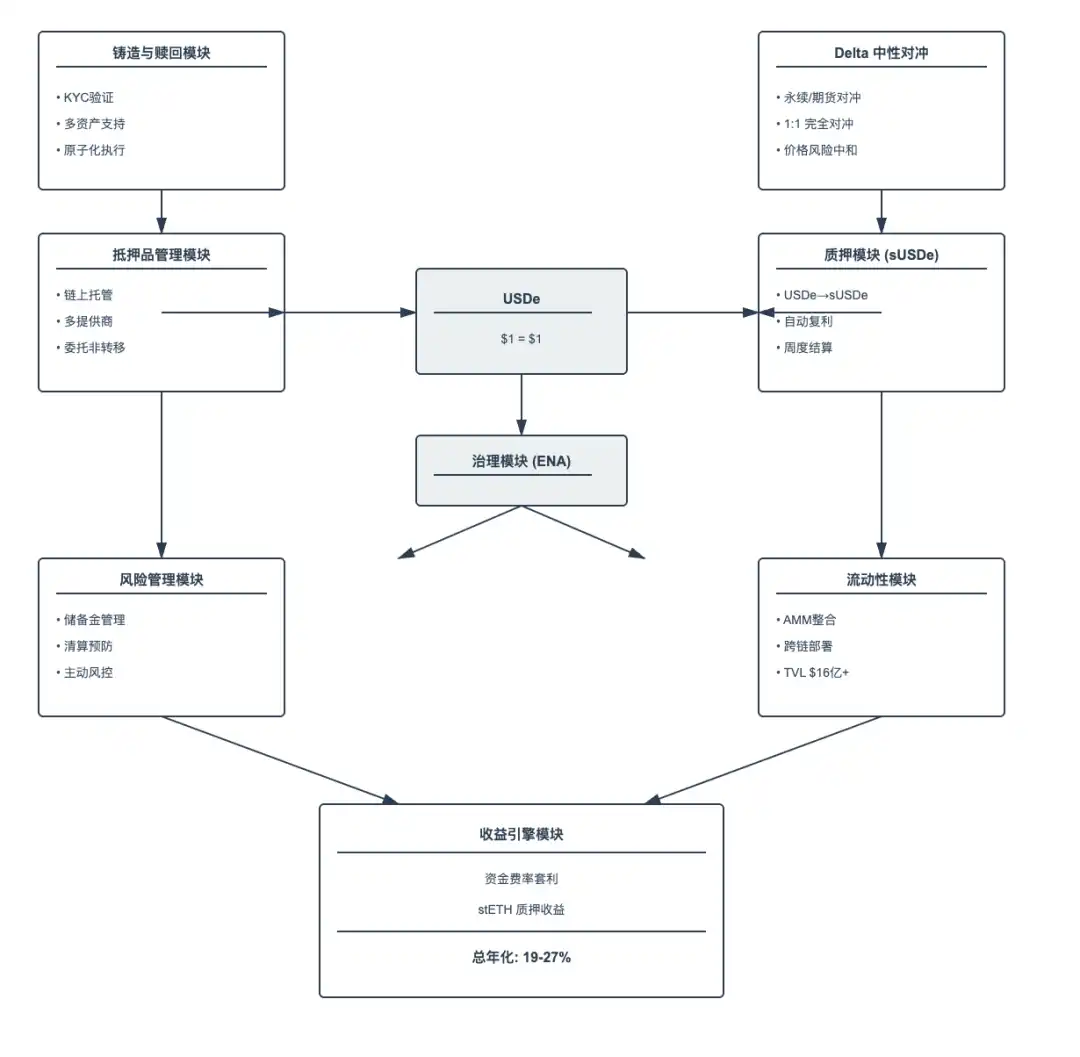

Mengambil contoh USDe dari protokol Ethena, yang terinspirasi oleh Arthur Hayes untuk menciptakan protokol YBS, ia membangun protokol dolar sintetis yang tidak bergantung pada cadangan mata uang fiat maupun kolateralisasi berlebih aset native Crypto, terdiri dari modul cetak dan tebus, modul strategi netral native Crypto, modul manajemen kolateral, modul staking (sUSDe), modul manajemen risiko, modul pool likuiditas, modul mesin hasil, serta modul governance.

Sumber: Pharos Research

Metodologi produk USDe adalah dengan menangkap pendapatan nyata melalui lindung nilai khusus dan pasar derivatif, sambil memperkenalkan kontrol risiko multi-layer (seperti tidak ada leverage berlebihan, dispersi posisi, dana cadangan) untuk menjaga stabilitas sistem, kemudian disarangkan seperti Lego dengan protokol DeFi seperti AAVE, Pendle, Morpho untuk meningkatkan APY (Tingkat Persentase Hasil Tahunan) dan mencapai pertumbuhan skala.

Ambil contoh sederhana: ketika Pengguna A menyetor 1 stETH (nilai $3,000), Ethena membuka posisi short kontrak perpetual ETH $3,000 di pasar derivatif. Jika ETH naik ke $3,300, spot untung +$300, short rugi -$300, nilai bersih = $3,000; jika ETH turun ke $2,700, spot rugi -$300, short untung +$300, nilai bersih = $3,000, Delta sistem = 0. Dan protokol Ethena, dengan paparan risiko 0 secara teoritis, dapat menangkap tiga sumber pendapatan nyata berikut:

Funding Rate - Dalam pasar bull, funding rate (biasanya 10-30% per tahun) yang dibayarkan oleh pihak long kontrak perpetual kepada short.

Pendapatan Staking - Yield yang melekat pada aset seperti stETH (~3-5%)

Pendapatan Basis - Alpha tambahan dari premium futures

Seperti ditunjukkan pada gambar di atas, APY aktual USDe dapat mencapai hingga 27%, yang lebih menarik daripada produk keuangan tradisional mana pun. Ketika pasar keuangan berjalan dalam keadaan stabil, orang menciptakan istilah khusus Inggris 'Internet Bond' untuk USDe, dan mendefinisikannya sebagai obligasi dolar global yang tidak memerlukan kepercayaan pada sistem perbankan.

Pada September 2025, kapitalisasi pasar USDe mencapai 14 miliar dolar AS yang menakjubkan, menjadi stablecoin terbesar ketiga di dunia setelah USDT dan USDC. Pada saat yang sama, Arthur Hayes di tempat umum membual bahwa USDe masih memiliki potensi pertumbuhan 51 kali lipat, rasionalisme teknik keuangan sepertinya sedang memenangkan kemenangan besar di industri Crypto.

Penumpukan Siklus Leverage Eksternal USDe

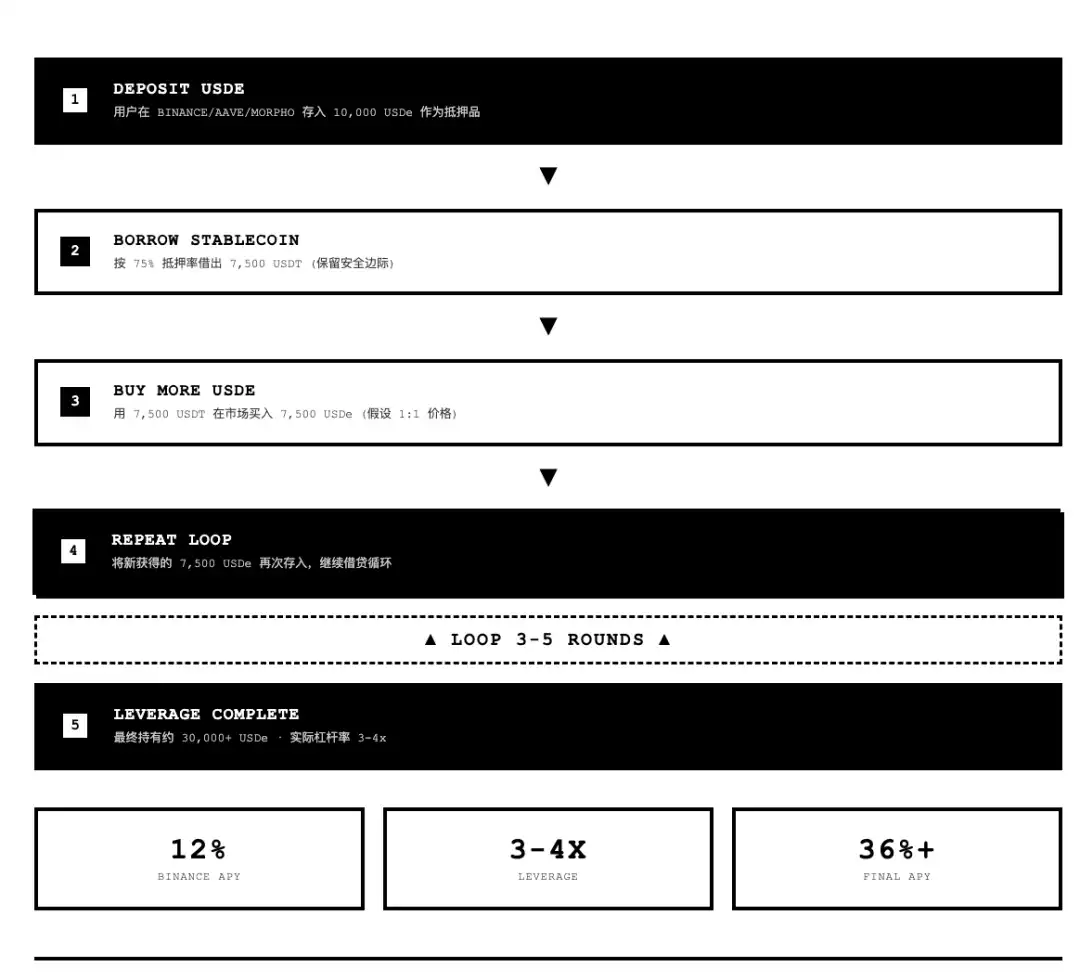

Mengingat pengalaman sejarah pahit dari collapse death spiral Lunar-UST, Ethena dalam desain arsitektur protokol sengaja memutus umpan balik penguatan siklus antara sisi aset dan liabilitas internal, berpegang pada底线底线不将代币原生 ENA 加入资产端列表, realisasi APY tinggi USDe terutama bergantung pada pinjaman siklus eksternal pengguna di protokol DeFi seperti AAVE, Pendle, Morpho dan CEX mitra.

Tetapi ketika pasar Crypto memasuki ekor siklus empat tahun pada tahun 25, dan stablecoin menjadi satu-satunya sektor yang mencapai pertumbuhan skala positif dalam setahun, 'menawarkan simpanan bunga tinggi' stablecoin menjadi alat pertumbuhan paling efektif untuk protokol DeFi dan CEX di pasar merah ini, mereka umumnya mulai mendorong dan membimbing pengguna untuk menggunakan USDe untuk pinjaman siklus eksternal dalam mekanisme produk dan propaganda pasar.

Sumber: Pharos Research

Pada 22 September 2025, 'exchange nomor satu di alam semesta' Binance meluncurkan program hadiah USDe 12% APY, mengizinkan pengguna menggunakan fungsi pinjaman internal untuk pinjaman siklus, dan dengan percaya diri menetapkan sumber harga likuidasi pinjaman USDe sebagai harga pasangan perdagangan USDe-USDT Binance titik tunggal.

Berbeda dengan kepercayaan diri dan kurangnya pengalaman Binance, protokol DeFi yang mengalami gelombang likuidasi besar era pasca DeFi Summer, umumnya meng-hardcode sumber harga likuidasi pinjaman USDe sebagai 1:1 atau menggunakan layanan oracle yang memiliki sumber data harga多方.

Peningkatan kepercayaan merek Binance, catatan patokan yang baik dari USDe, dan sentimen optimis Uptober yang menyebar di pasar, membuat banyak pengguna menghasilkan ilusi fatal bahwa USDe 12% APY adalah pendapatan bebas risiko, dan mulai menggunakan leverage siklus dengan gila dalam emosi FOMO pasar. Terarik oleh program ini, persediaan USDe di Binance melonjak dari 3 miliar dolar AS menjadi 5 miliar dolar AS.

Dari total liabilitas sistem USDe senilai 14 miliar dolar AS, sekitar 40% (≈5.6 miliar) adalah bagian lindung nilai Delta yang nyata, sisanya sekitar 60% (≈8.4 miliar) ditumpuk pada pinjaman siklus dengan leverage 2-5x.

Serangan Angsa Hitam dan Kehilangan Patokan USDe

Pada 11 Oktober 2025, pukul 5 pagi waktu Beijing, Sabtu dini hari, Trump memposting di Truth Social: "Mulai 1 November, kenakan tarif 100% pada barang-barang China."

Likuidasi besar 19 miliar dolar AS (perkiraan konservatif) yang mencetak rekor pasar Crypto就此引爆.

Gelombang pertama - Kepanikan normal (05:00-05:20): Aset berisiko global dijual secara massal, aset inti Crypto turun drastis, kontrak perpetual mulai dilikuidasi secara besar-besaran, posisi long leverage disapu.

Gelombang kedua - Ketidakseimbangan sistem (05:20-05:43): Penurunan ekstrem melampaui ambang batas, menyebabkan funding rate kontrak perpetual aset inti Crypto berubah menjadi negatif. Paus USDe mulai menjual di Binance, harga pasangan perdagangan USDe-USDT Binance meluncur dari $1.00 ke $0.9 lalu ke $0.91......

Gelombang ketiga - Jebolnya tanggul (05:43-06:16): Harga pasangan perdagangan USDe-USDT Binance jatuh di bawah $0.82, ini adalah garis paksa平仓 untuk pinjaman siklus 5x, sehingga memicu tsunami likuidasi全系统:

Tahap 1: USDe jatuh ke $0.82

→ Pinjaman siklus 5x memicu likuidasi

Tahap 2: Mesin likuidasi mulai menjual USDe untuk melunasi utang USDT

→ USDe jatuh ke $0.75

Tahap 3: Lebih banyak likuidasi terpicu

→ Pinjaman siklus 3x dan 4x mulai爆仓

Tahap 4: Likuiditas benar-benar kering

> → USDe瞬间击穿至 $0.6567Tahap 5: Likuidasi berantai失控

> → Mekanisme ADL dan akun terpadu催生 gelombang penjualan super aset jaminan USDeSeluruh proses 23 menit.

Bayangkan Anda adalah pengguna Binance, yang telah memperbesar hasil tahunan 12% menjadi 48% melalui pinjaman siklus. Teman-teman Anda menganggap Anda jenius. Anda juga berpikir begitu. Namun, dalam 90 menit pada dini hari 11 Oktober 2025, saldo akun Anda dari enam digit menjadi nol.

Ada detail yang menarik dalam badai sempurna ini: aset yang sama, pada waktu yang sama, memiliki realitas yang sangat berbeda di on-chain dan off-chain.

Selama peristiwa kehilangan patokan, fungsi cetak/tebus USDe tidak pernah terputus, protokol mempertahankan status kolateralisasi berlebih, posisi lindung nilai Delta beroperasi normal. Ini bukan collapse protokol Ethena, melainkan collapse struktur pasar spesifik Binance.

Dari badai sempurna ini, apa yang kita pelajari

Crypto menjanjikan inovasi tanpa izin, keuangan terdesentralisasi, kepercayaan yang digerakkan oleh matematika, tetapi realitas Crypto harus menerima batasan hukum keuangan dunia nyata. Dalam badai sempurna kehilangan patokan USDe ini, kita menyaksikan bagaimana faktor-faktor seperti model kompleks, leverage tinggi, likuiditas, risiko sistemik, dan kepercayaan diri yang berlebihan bekerja bersama-sama menyebabkan collapse sistem.

Meskipun protokol Ethena dalam peristiwa super ini membuktikan ketangguhan dan kemampuan anti-risiko sistem teknik keuangannya, timnya, didorong oleh keserakahan akan keuntungan dan keinginan untuk tumbuh, secara diam-diam bahkan aktif membimbing pasar untuk melihat produk DeFi Yield berisiko tinggi sebagai tabungan bebas risiko, mendorong penumpukan siklus leverage eksternal USDe, menjadi benih yang孕育 badai sempurna ini, dan akhirnya memakan kembali TVL dan kepercayaan pasar protokol.

Stablecoin bukan mata uang fiat, bukan CBDC, tidak memiliki legal tender yang memaksa, esensinya adalah Token bukti kepemilikan yang dipatok pada 1 dolar AS, mengizinkan pemegangnya untuk menebus kolateral yang sesuai. Stabilitas stablecoin, berasal dari stabilitas mekanisme (apakah protokol dapat mempertahankan patokan dalam semua kondisi pasar), stabilitas likuiditas (apakah pasar dapat memberikan kedalaman yang cukup di bawah tekanan), dan stabilitas kepercayaan (apakah pengguna mempercayai kinerjanya dalam krisis).

Satu-satunya pelajaran yang diambil manusia dari sejarah adalah bahwa manusia tidak pernah mengambil pelajaran. Manusia seperti agen pembelajaran penguatan, dengan hadiah positif yang padat cepat mempelajari strategi serakah 'leverage tinggi + lindung nilai kompleks = hasil tinggi', tetapi karena hadiah negatif terlalu jarang, ekstrem, tertunda, tidak dapat memperbarui strategi secara menyeluruh, menyebabkan pengulangan kesalahan fatal yang sama di era yang berbeda, pasar yang berbeda.

Kontributor Inti

Penulis: NingNing

Penyunting: Colin Su, Grace Gui, Owen Chen, FangHan

Desain: Alita Li