The Bitcoin-to-gold ratio, which highlights the ounces of gold required to purchase one BTC, has retraced to 20 ounces per BTC, down roughly 50% from around 40 ounces in December 2024. Rather than a collapse in Bitcoin (BTC) demand, this sharp shift reflected the unique macroeconomic regime of 2025, where gold’s asset performance dominated that of the crypto asset.

Key takeaways:

The BTC–gold ratio fell from 40 to 20 ounces per BTC between December 2024 and Q4 2025.

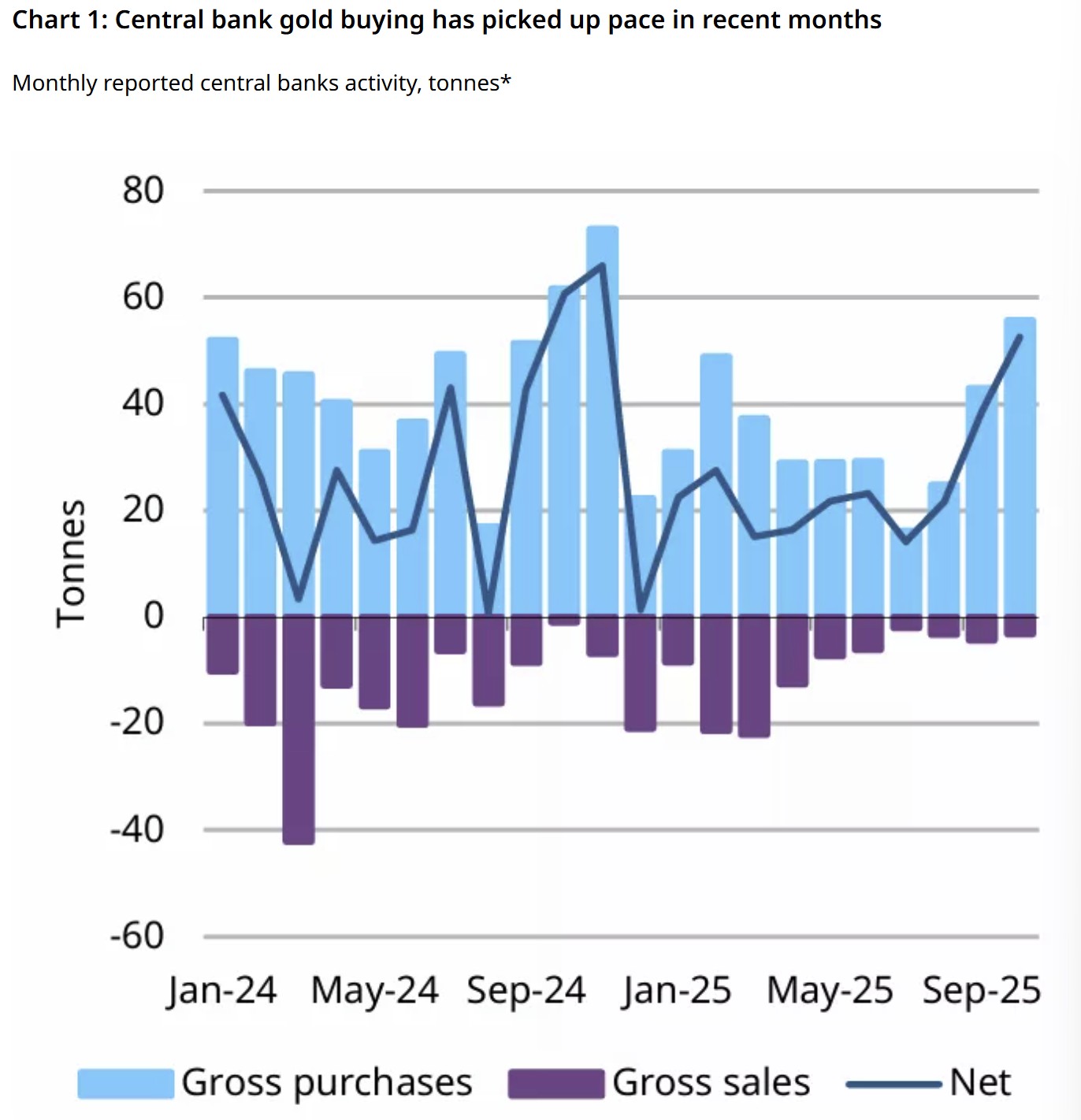

Gold absorbed sustained inflows as central banks purchased 254 tonnes through October, and global gold ETF holdings increased by 397 tonnes in H1 2025.

Bitcoin demand softened in H2 as spot ETFs’ AUM declined from $152 billion to $112 billion, while long-term holders sold over 500,000 BTC.

Why gold dominated the store-of-value bid in 2025

Gold led the global store-of-value bid in 2025, delivering a year-to-date (YTD) gain of 63% and breaking above $4,000 per ounce in Q4. What made this rally distinct was that it unfolded despite restrictive monetary conditions.

The rise took place while US interest rates remained restrictive for most of the year, with the Federal Reserve delivering its first basis-point cut only in September. Historically, such an environment would pressure non-yielding assets, yet gold advanced sharply, highlighting a structural shift in demand.

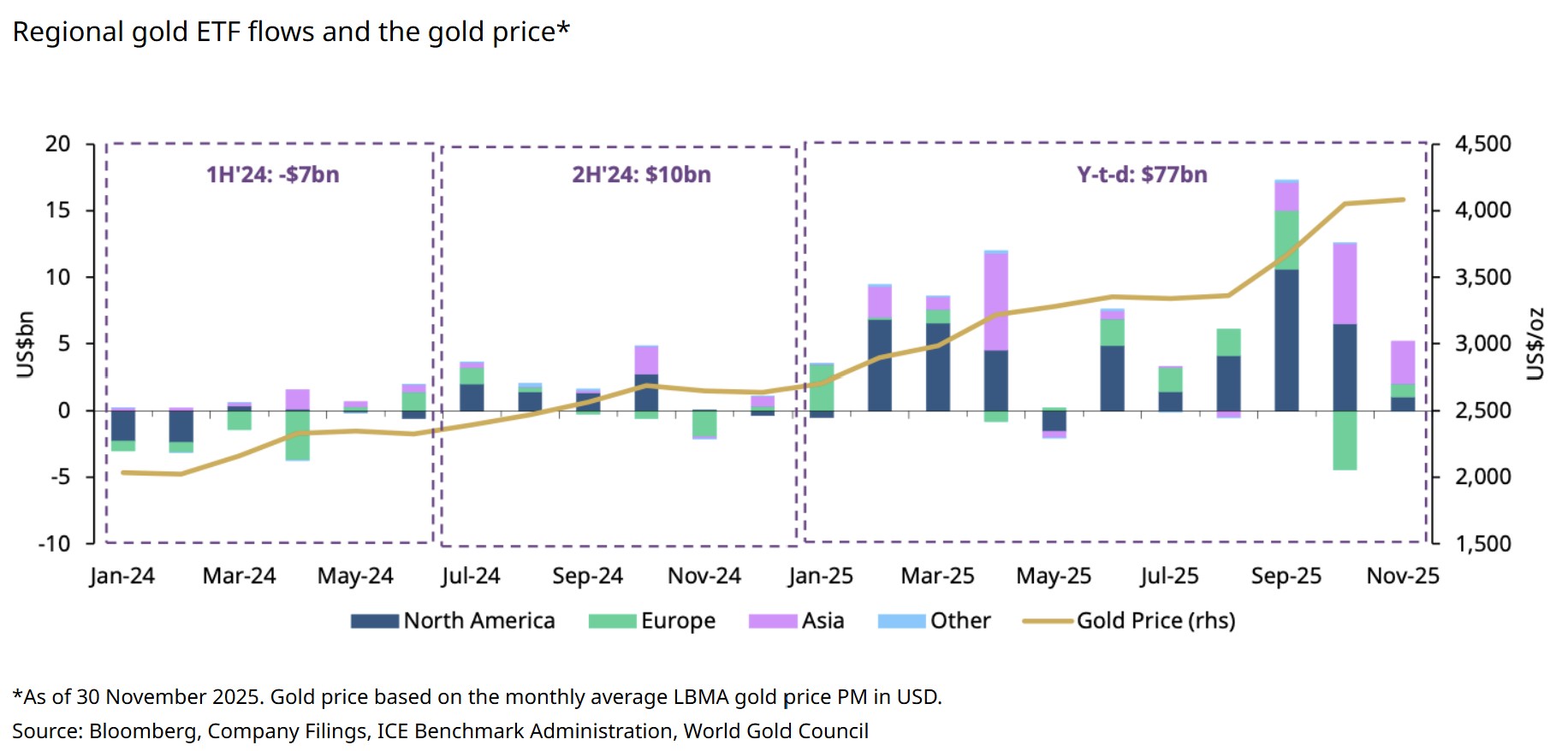

Central banks were at the core of this move. Global official sector purchases totaled 254 tonnes through October, with the National Bank of Poland leading the charge, by adding 83 tonnes. At the same time, Global gold exchange-traded funds (ETFs) holdings expanded by 397 tonnes in H1 2025, reaching a record high of 3,932 tonnes by November.

This was a significant reversal of the 2023 outflow pattern. This inflow occurred despite real yields averaging 1.8% across developed markets in Q2, during which gold still rallied 23%, signaling a clear decoupling from its traditional inverse relationship with yields.

Elevated uncertainty further reinforced gold’s appeal. The VIX (Volatility Index) averaged 18.2 in 2025, up from 14.3 in 2024, while geopolitical risk indexes climbed 34% year-over-year. Gold’s equity beta compressed to negative 0.12, its lowest since 2008, confirming demand from both risk-off hedging and long-term allocation.

Thus, defined by tight US financial conditions and delayed policy easing, gold functioned less as an inflation hedge and more as a broad portfolio insurance in 2025.

Related: Bitcoin sharks stack at the fastest pace in 13 years, with BTC down 30%

Why Bitcoin lagged gold on a relative basis

Bitcoin delivered solid returns through 2025, reaching six-figures and benefiting from demand for spot BTC ETFs. However, relative to gold, Bitcoin underperformed as demand conditions weakened during the second half of the year.

Spot Bitcoin ETFs saw strong early momentum, with total assets under management (AUM) rising from $120 billion in January to a peak of $152 billion by July 2025. Since then, AUM declined steadily to around $112 billion over the following five months, reflecting net outflows during price pullbacks and a slowdown in fresh capital formation. This contrasted with consistent inflows into gold ETFs over the same period.

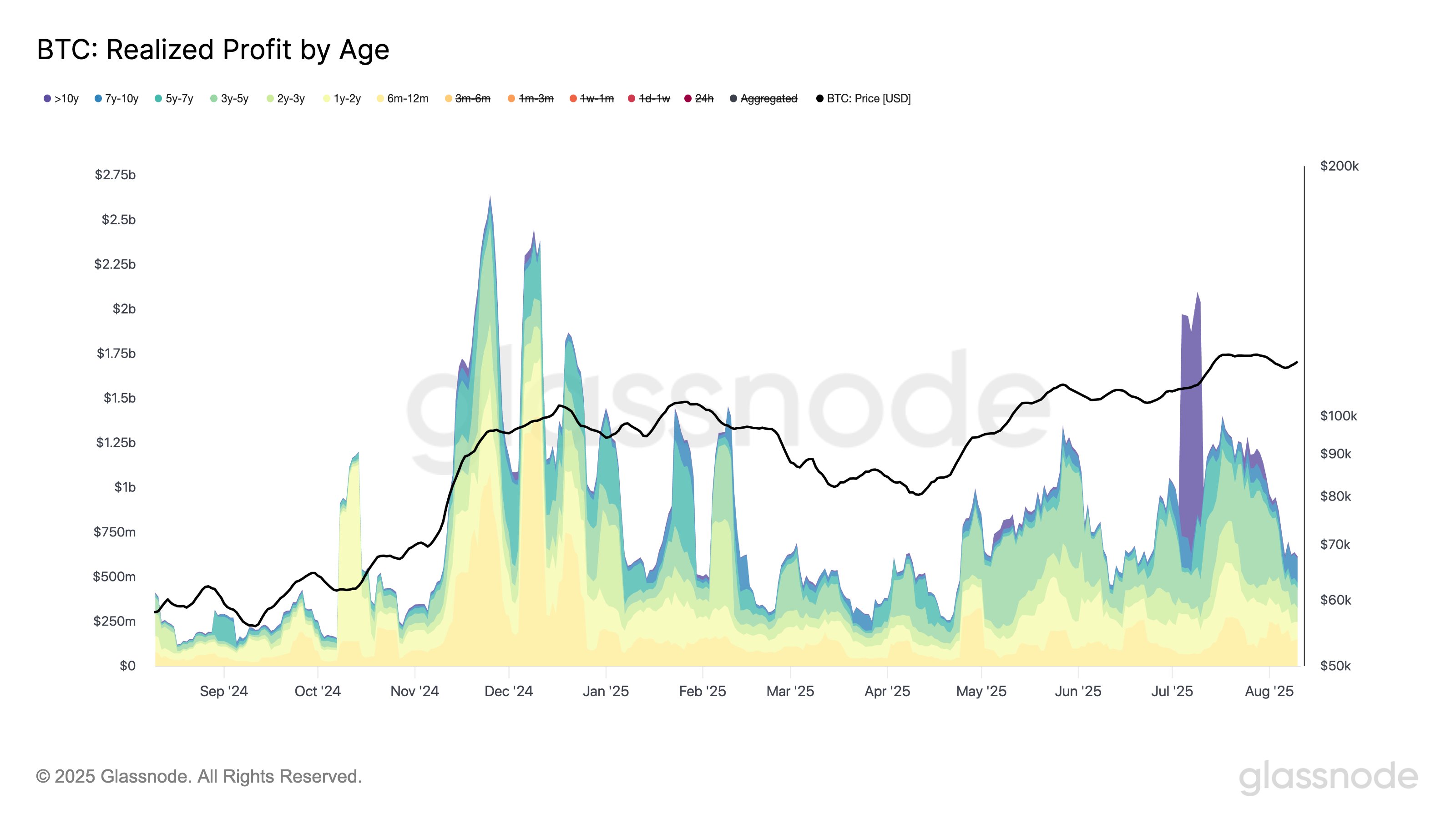

Onchain data also pointed to distribution. According to Glassnode, long-term holder (LTH) profit realization exceeded $1 billion per day on a seven-day average throughout much of July, marking one of the largest profit-taking phases on record.

While realized profits moderated in August, selling resumed later in the year. In October, long-term holders sold roughly 300,000 BTC, worth $33 billion, representing the most aggressive LTH distribution since December 2024. As a result, LTH supply declined from 14.8 million BTC on July 18 to about 14.3 million BTC at present.

Elevated real yields through most of 2025 raised the opportunity cost of holding Bitcoin, while its correlation with equities remained relatively high. Gold, by contrast, benefited from safe-haven and reserve-driven demand. This divergence in demand regimes explains the compression in the BTC–gold ratio, reflecting cyclical repricing rather than a structural breakdown in Bitcoin’s long-term thesis.

Related: Bitcoin parabola breakdown raises chance for 80% correction: Veteran trader

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.