Author: XY

Compiled by: Tim, PANews

One Year into the Bear Market

It took me some time to convince myself: we are in a bear market, and it has been going on for about a year.

November 2024 was a period of market excitement, and the launch of $TRUMP pushed the market into extreme euphoria—it was the final frenzy that no one wanted to believe was the end.

Below, I will explain my perspective.

It all starts with that old cliché: "History doesn't repeat itself, but it often rhymes."

This foolish saying has been hugely misleading for market analysis—it's downright harmful.

It has made us overly reliant on historical patterns and, at the same time, eroded our ability to question.

Yes, this reliance on historical patterns for prediction is like viewing the world through a prism carved with old designs. It inevitably misinterprets new realities and ultimately causes us to overlook the latest driving factors in the market. This is precisely where the danger lies.

More specifically, we misread two fundamental changes.

Change One

We thought Meme mania was the spark that would ignite altseason, but in reality, Meme mania was altseason itself.

When Meme coins surged one after another, we thought it was just the beginning.

Some talked about altseason, and a few bold ones even mentioned a raging bull market.

We were all wrong.

Keep in mind that previous cycles always featured bubble叠加-bubble phenomena, typically driven by new narratives. These new narratives gave rise to new markets, which often led to differentiation.

This differentiation was important because it split liquidity into two distinct groups.

The first group is dumb money.

This type of capital prefers simple operations, market depth, and low barriers to entry, staying within highly liquid tokens.

The second group is hot money.

This capital actively pursues returns and is willing to overcome complexity to find opportunities.

The subsequent short-term rotation of hot money fueled bullish trends, which eventually evolved into what people called altseason.

This cycle never produced that trend. There was no new narrative to explore this time.

From start to finish, both groups remained in the same arena.

Dumb money could participate effortlessly, and hot money could still profit by getting in early.

Our mistake was expecting an "altseason" to occur.

But it never happened.

The only path the market had was: from Bitcoin to a new narrative, then to altseason.

That used to be the script you wanted.

But the reality is that Meme mania became the altseason people anticipated.

November 2024 marked the peak profitability for most traders, and TRUMP was the climax of the market狂欢.

Change Two

Bitcoin is no longer driven internally by the crypto market but is instead dominated by institutions and macro markets.

And the macro environment follows a different timeline and reacts differently to changes.

After the TRUMP surge, many interpreted Bitcoin's resilience as the market still being in a consolidation or bull market correction phase.

This interpretation stemmed from an anchoring bias based on past experiences: people are accustomed to the idea that Bitcoin must crash sharply to confirm a bear market, applying this to a market structure now dominated by institutions.

This cognitive framework is outdated.

Bitcoin has actually decoupled from the native cryptocurrency market cycle.

Once you recognize this, the subsequent developments make perfect sense.

The bear market began after the MEME coin TRUMP, regardless of Bitcoin's price performance.

So, stop focusing only on Bitcoin.

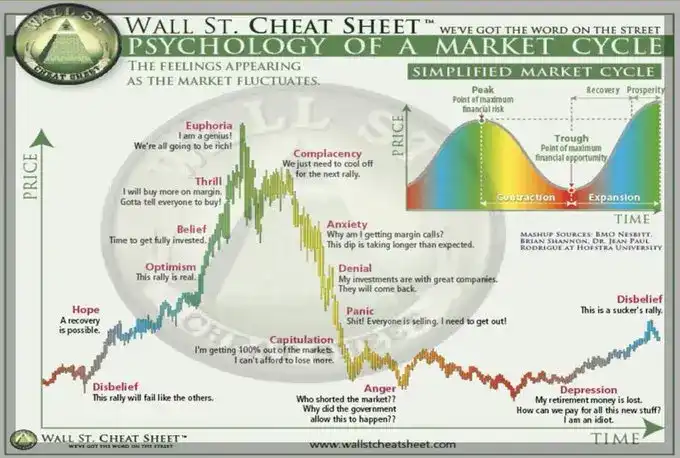

From January 2025 to the present, the market has fully gone through the three stages of anxiety, denial, and panic. If you've made profits, you can clearly see these stages in the people around you; if you've suffered losses, you've experienced these emotions firsthand.

We are now in the stage of anger and depression.

So, why am I writing this post?

Two reasons.

First, one of the reasons the crypto market has been profitable for me is the ability to buy near the bottom. If you misjudge the market phase, this advantage disappears.

If you think the bear market isn't over yet, you'll keep waiting for the bottom to arrive, unaware that you're already in it.

Second, I hope this perspective sparks fierce debate or helps people become alert and break free from the wrong cognitive framework.

I have extremely high confidence in this judgment.

That's why I will soon start acting to prove my judgment.