Author: Axis

Compiled by: WuBlockchain

TL;DR: Key Points on South Korea's Crypto Market Shake-Up and Information Asymmetry

· The Deep Impact of Bithumb's Suspension: The six-month partial business suspension of Bithumb, South Korea's second-largest exchange, has been severely underestimated by the global market. This is not a simple compliance crackdown; it is dismantling the competitive price discovery mechanism of the South Korean crypto market (where Upbit and Bithumb hold a 96% share).

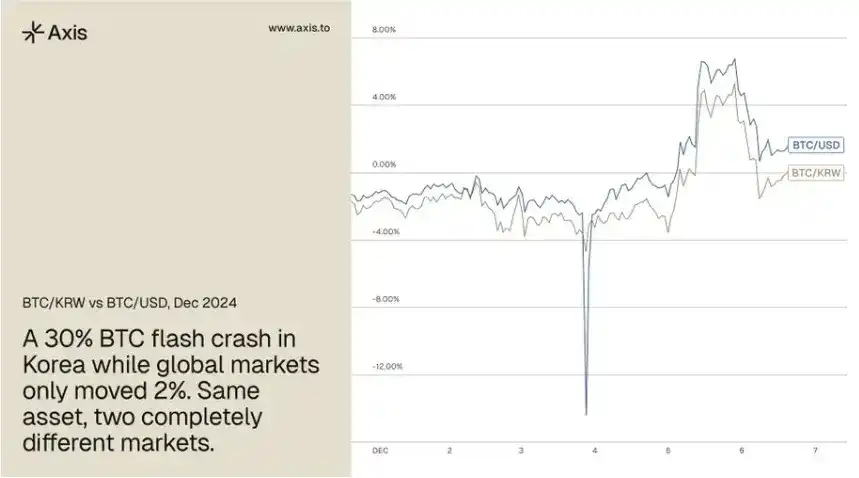

· A Critical Structural Information Gap: Due to language barriers and capital controls, political or regulatory shocks in South Korea (like the December 2024 martial law declaration that caused a 30% local BTC crash vs. a 2% global drop) often trigger massive local tremors first. The delayed reaction in the English-speaking trading community creates a brief yet highly profitable window for arbitrageurs with first-hand information.

· Re-evaluating the "Kimchi Premium": The premium is not just a sentiment indicator for retail investors; it's a "thermometer" for cross-border capital friction. Under capital controls, Bitcoin maintains a structural non-zero floor of about 1.24%. A contraction in the premium often signals a shift in underlying capital pressures, not just a return to normalcy.

·Liquidity Oligopoly Risk: Bithumb's suspension is accelerating the concentration of funds into Upbit. Excessively concentrated liquidity is prone to extreme volatility (e.g., a 17% flash crash in BTC/KRW in February 2026 due to a Bithumb operational error), making future market dislocations more hidden and destructive.

· Core Conclusion: As the contradiction between institutional capital inflows from the new government's "pro-crypto" policies and the tightening of retail infrastructure intensifies, this structural "information asymmetry" in the South Korean market will persist, continually generating fleeting excess arbitrage (Alpha) opportunities.

A Market-Shaking Event Just Occurred, But Was Largely Underestimated by Global Traders

On March 15, South Korea's financial regulator imposed a six-month partial business suspension on Bithumb, the country's second-largest crypto exchange. English-language media largely treated it as routine compliance news, involving anti-money laundering (AML) enforcement and regulatory cleanup. However, most reports missed its deeper implications.

In reality, this is a structural market event occurring within one of the deepest on-chain fiat liquidity pools, with repercussions extending far beyond South Korea. Upbit and Bithumb together account for about 96% of the trading volume in the South Korean cryptocurrency market. Bithumb's suspension is not only reshaping the domestic market landscape but also weakening the quality of price signals this market has transmitted to global traders for years.

Simply put, South Korean crypto users are extremely active, but the system they operate in is constrained by capital controls, highly concentrated exchanges, and persistent language barriers. This unique environment means critical information affecting prices often ferments locally first before spreading globally. This creates a brief time window, causing a disconnect between local and global markets.

Global Traders Are Always a Step Behind: Due to Structural Differences, Not Chance

South Korea is by no means a peripheral market in crypto; it is one of the most valuable markets for insights into the origins of global on-chain opportunities. The Korean Won (KRW) is the second-largest fiat currency in the global crypto market by trading volume, with year-to-date trading reaching approximately $663 billion, accounting for nearly 30% of global fiat-to-crypto trading volume. Furthermore, nearly one-third of South Korean adults hold digital assets, double the proportion in the United States.

The current South Korean government, which took office in June 2025, ran on what is considered one of the most explicit "pro-crypto" political manifestos in history. Since the president's inauguration, nearly half of the top 30 performing stocks in the Korea Composite Stock Price Index (KOSPI) have been related to digital assets. Traditional stock markets quickly digested this positive signal, but the broader crypto community was largely slow to react.

This market dislocation is not an isolated case. Local political and regulatory developments in South Korea typically ferment first in Korean-language media and local Crypto Twitter (CT), causing anomalies in KRW trading pairs on Upbit and Bithumb, while English-language media often follow up hours or even days later. This information gap works in reverse too: global macro developments originating in the English-speaking context also take time to be fully priced into local Korean trading pairs. Often, by the time the information is translated and disseminated, the initial market move is over.

The most stark example occurred on December 3, 2024, when South Korean President Yoon Suk-yeol declared martial law. Driven solely by this domestic political shock, the price of BTC on South Korean exchanges plummeted by approximately 30% intraday, while the global market decline was only around 2% — a staggering price difference of 28 percentage points. The total scale of this sell-off was about $33.3 billion, briefly making the South Korean market the highest volume market globally.

This event is a classic缩影 (snapshot) of South Korean market dislocation. Buy-side liquidity evaporated instantly, sell-side pressure surged dramatically, and the selling was almost entirely concentrated on Korean Won (KRW) trading pairs. Even stablecoins experienced severe de-pegging, with USDT dropping to $0.75 on Korean exchanges, while BTC and altcoins showed deep discounts of over 50% compared to global market prices.

Local Korean users, mistakenly believing they were scrambling for the last liquidity exit, frantically sold at market prices even though global markets were barely moving. On-chain data shows arbitrageurs sprang into action, moving millions of USDT in single transactions to arbitrage away the price difference. The huge流量 (traffic) caused front-end systems of major exchanges to crash, preventing retail users from logging in to buy the dip. During this brief window, only API traders could execute orders successfully. By any measure, this was an extremely tradeable "seismic" event, but the arbitrage window closed within just a few hours.

Bithumb's current suspension is replaying the same script. The news has been circulating in Korean-language information circles for weeks, while most traders in the English-speaking context are only hearing about it now.

The "Kimchi Premium" Is Closely Watched But Often Misinterpreted

For traders lacking access to Korean information channels, the "Kimchi Premium" has long been the most direct observable metric for gauging South Korean market dynamics. This premium measures the price difference between crypto assets priced in Korean Won (KRW) and those priced in US dollars globally. Consequently, experienced traders have long closely monitored KRW market volume. South Korea's spot altcoin market volume ranks among the highest globally and has historically been a reliable leading indicator for broader market trends.

The crux is that most traders misinterpret this signal. The market generally views the premium simply as a sentiment indicator for Korean retail investors. While retail sentiment is a factor, in a market where cross-border capital flows face regulatory friction, the premium more deeply reflects the intensity of structural capital pressures. When this regulatory friction intensifies, price dislocations tend to magnify.

Historical data makes this concrete. Looking back to 2017, when the USD/KRW exchange rate was around 1060, the "Kimchi Premium" soared to a peak of 40%, meaning the implied USDT/KRW exchange rate was effectively around 1480. By December 2024, the actual USD/KRW exchange rate did indeed break through 1480. In other words, the premium pre-priced this foreign exchange move years in advance. These signals were hidden in plain sight within publicly available data, but accurate interpretation required access to local Korean information channels.

One constant feature is that this premium does not naturally revert to zero. Research suggests that as long as capital controls exist, Bitcoin's premium will maintain a structural non-zero floor of approximately 1.24%. This means that when the premium contracts towards this level, it typically reflects a shift in underlying capital pressures, not just a simple statistical reversion to the mean.

Looking back at 2025, whenever the premium approached zero, Bitcoin recorded positive returns in the subsequent week and month: its 7-day average return was 1.7%, and its 30-day average return was 6.2%. For traders, the crucial signal is not the absolute value of the "Kimchi Premium" but its dynamic evolution over time.

Bithumb's Suspension Makes Korean Market Dislocation Harder to Predict, Intensifying Information Asymmetry

The effectiveness of the premium as a reference signal depends on how price discovery occurs *between* South Korea's major exchanges. When multiple platforms compete to price similar capital flows, the resulting spreads often contain richer information. However, as liquidity becomes increasingly concentrated among寡头 (oligopolies), the clarity of this signal begins to衰减 (decay). Thus, Bithumb's suspension is dismantling the competitive price discovery mechanism upon which this premium relies.

Following the penalty announcement, funds began rapidly migrating to Upbit, further increasing market concentration. In February 2026, a major operational error at Bithumb, where 620,000 BTC were mistakenly credited to user accounts, caused a 17% flash crash in the BTC/KRW pair before prices recovered. This episode vividly illustrates the extreme conditions that can arise when price discovery hinges heavily on a single platform operating under high pressure.

The diminishing reference value of the premium indicator does not mean market dislocations in South Korea are over. Instead, it means such dislocations become harder to predict before they erupt, further widening the information gap between participants directly tracking the Korean market and traders relying solely on English-language information.

The underlying environment fostering these dislocations is also becoming more acute. In 2025, under harsh trading rules, approximately $110 billion in crypto assets flowed out of South Korea. Under the new government, capital that was structurally squeezed out is being reintroduced through new institutional channels;但同时 (simultaneously), the exchange infrastructure relied upon by retail funds is continually tightening. Historically, such severe policy divergence has been a perfect breeding ground for the most violent and fleeting price dislocations in this market.

South Korea's Market Structure Creates Replicable Information Asymmetry for Global Traders

The "Kimchi Premium" is by no means a unique phenomenon exclusive to South Korea. This mechanism operates to varying degrees in every jurisdiction where cryptocurrency develops as a parallel financial channel alongside capital controls, with the South Korean market being merely the most widely observed example.

Both the December 2024 martial law event and the current Bithumb suspension confirm the same evolutionary logic. Market dislocations here always erupt unexpectedly, rewarding only participants with first-hand information channels, and are quickly arbitraged away before the broader market reacts. The traders who acted decisively on December 3rd weren't inherently faster or smarter. They simply watched the right signals and understood, before the market caught on, how domestic political events in South Korea translated into exchange price mechanisms.

As stablecoin infrastructure deepens globally, more markets will emit signals of capital pressure similar to those generated by South Korea over the past decade. The real challenge lies not in discovering the existence of these signals, but in building the infrastructure and trading discipline to consistently capture these opportunities.