Author:Xu Chao

The latest analysis from research firm SemiAnalysis reveals that Anthropic is reshaping the AI commercialization landscape with profitability and growth rates far surpassing its competitors. Leveraging a high-margin, API-centric business model, Anthropic has become a frontrunner in the B2B AI market.

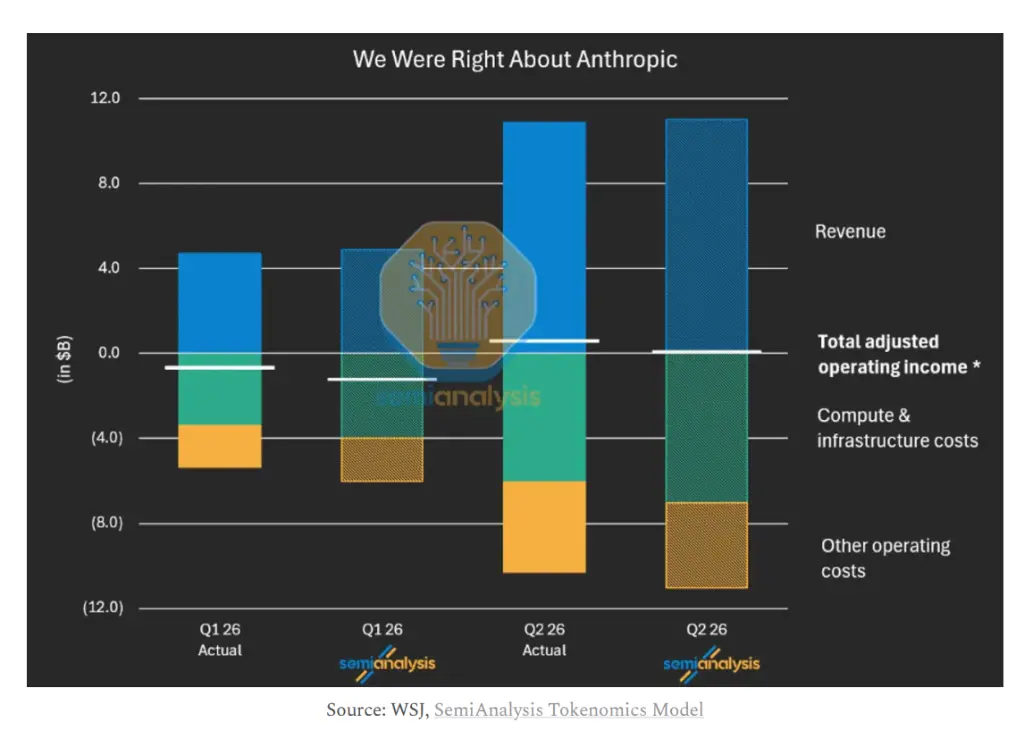

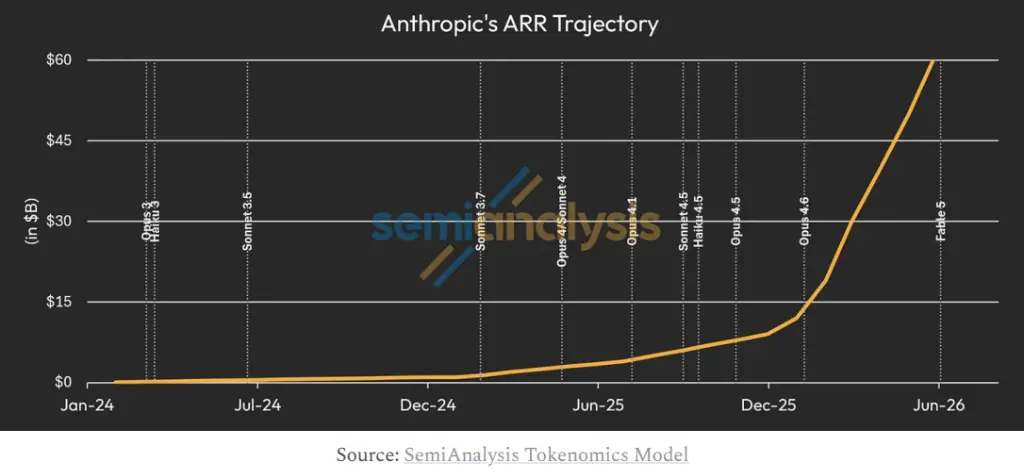

According to a deep-dive report from SemiAnalysis, Anthropic is projected to achieve GAAP EBIT of $1 billion in Q3 2026, representing a profit margin of approximately 6%. Concurrently, its Annual Recurring Revenue (ARR) has surged from $9 billion at the end of 2025 to over $60 billion currently. The agency predicts that if Anthropic maintains its Net New ARR (NNARR) pace of about $15 billion per month, its ARR by the end of 2027 could reach $300 billion, corresponding to a $6 trillion enterprise value, potentially making it the world's highest-valued company.

Anthropic confidentially filed its IPO application on June 1. SemiAnalysis believes there is strategic urgency for listing at this time — Alphabet has completed $84.75 billion in equity financing, and Meta is also rumored to have a multi-billion dollar financing plan, indicating a narrowing capital market window. The report notes that Anthropic's superior financials and business model mean it should go public before OpenAI to seize the initiative in the capital competition.

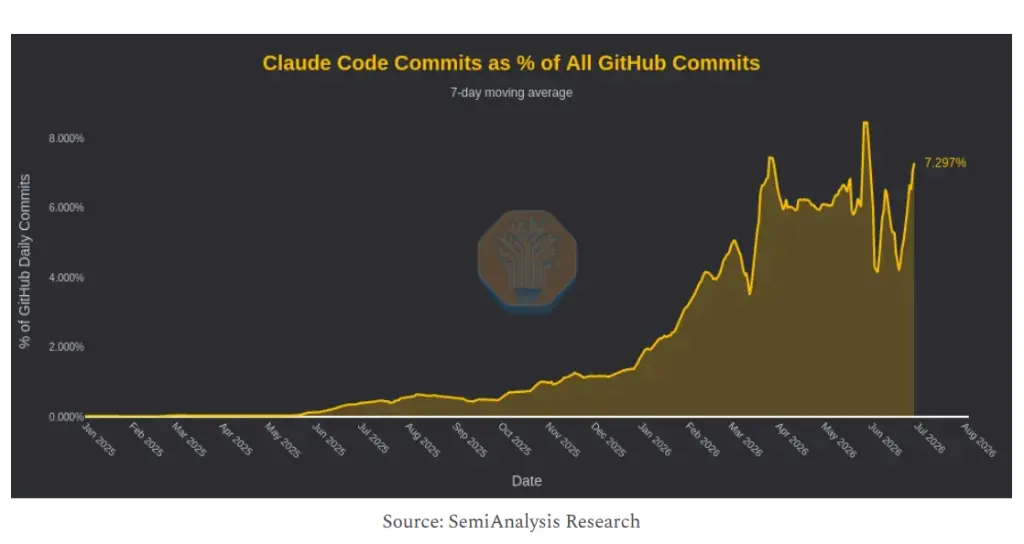

Anthropic's performance inflection point stems from the explosive adoption of Claude Code. SemiAnalysis data shows that Claude Code now accounts for over 7% of all code commits on GitHub, directly driving the company's monthly net ARR additions from $3 billion in January to $11 billion in March.

In terms of revenue structure, Anthropic and OpenAI show a significant divergence. Approximately 75% to 85% of Anthropic's ARR comes from usage-based API billing, with consumer subscriptions comprising only about 5% of total ARR. In contrast, over 65% of OpenAI's revenue in Q1 2026 still came from subscription models, with consumer ARR accounting for about 40%.

SemiAnalysis points out that the core advantage of the API model is the absence of a per-user revenue ceiling — as the same customer adopts more agentic workflows, their token consumption and corresponding revenue will continue to grow, enabling expansion without acquiring new customers. Anthropic's CFO Krishna Rao disclosed in a podcast this May that the company's net revenue retention rate (NRR) is as high as 500%, meaning that the cohort of customers who contributed $30 billion ARR in Q1 contributed only $2 billion a year ago.

The difference in business models is directly reflected in gross margins. SemiAnalysis estimates that Anthropic's current consolidated gross margin has risen to the mid-60% range, compared to negative 94% in 2024. The API business gross margin exceeds 80%.

The core driver of the dramatic gross margin improvement is gains in inference efficiency. Measured by ARR per megawatt of computing power, Anthropic's metric will reach $60 million later this year, up from just $16 million nine months ago. Since inference computing costs are largely fixed, marginal profit margins approach 100% when the number of tokens processed per unit of computing power or token pricing increases.

The report calculates that if both Anthropic and OpenAI reach $100 billion ARR, OpenAI's gross profit would be about $25 billion lower than Anthropic's due to the need to support over 900 million free users (estimated monthly service cost of approximately $0.70/person by SemiAnalysis). This gap will directly impact both parties' reinvestment capacity for next-generation model training.

SemiAnalysis introduces "Earnings Before Training, Interest, and Taxes" (EBTIT) as a core metric for measuring a lab's reinvestment capacity, with Anthropic achieving an EBTIT margin of 36% in Q2 2026. The report forecasts that by 2028, Anthropic's cumulative EBTIT will be $250 billion higher than OpenAI's.

SemiAnalysis estimates that currently over 65% of Anthropic's ARR comes from programming-related use cases, with programming tool startups like Cursor, Cognition, Loveable, and Replit collectively contributing approximately $6 billion ARR. Meta is Anthropic's largest single customer, but its share remains between 3% and 5%.

The report believes that cybersecurity will be the next explosive vertical after programming, and expects that the release of the Fable new model will further increase token pricing and expand application scenarios, driving monthly NNARR in the second half of 2026 beyond the current level of $10 billion per month. Healthcare, finance, biotechnology, and other verticals are also listed as potential major TAM expansion directions.

In terms of distribution channels, the indirect "Tokens-as-a-Service" (TaaS) model sold through hyperscale cloud platforms like AWS Bedrock and Azure Foundry is growing rapidly, now accounting for 15% to 20% of Anthropic's ARR, up from just 5% to 10% a quarter ago. SemiAnalysis believes that paying 20% to 30% of revenue share to hyperscale cloud platforms remains economically justifiable from the perspective of enterprise customer reach efficiency and compliance convenience.

The core constraint facing Anthropic's growth prospects lies in computing power supply.

SemiAnalysis predicts that by 2030, the combined unconstrained computing power demand of Anthropic and OpenAI will exceed 100 gigawatts (GW), while the net new computing power in 2025 and 2026 was only 2.5GW and 5GW respectively. Currently, the combined available computing power of the two companies is just over 6GW.

It is precisely this supply-demand gap that gives the IPO clear strategic significance. The report notes that funds raised from the listing will primarily be used to fill the growing gap between inference operations and new model training demands, and to secure computing power resources in advance at more favorable financing costs. The report also mentions that Meta is considering renting out computing power to external parties (source: market rumors on July 1, 2026) and expects Anthropic to procure incremental computing power from such trusted suppliers.

SemiAnalysis also lists key risk factors, including: rumored price-cutting plans from OpenAI; competitive pressure from Google DeepMind and Meta in programming models; potential regulatory restrictions on frontier model releases by governments; and the dilutive effect on consolidated gross margins from the rising proportion of TaaS revenue. The report clearly states that if regulatory regimes hinder model releases and narrow the capability gap between open-source and frontier proprietary models, it would fundamentally undermine Anthropic's business moat.