加密货币市场持续面临抛售压力,市场情绪日益被谨慎甚至部分领域的彻底恐慌所主导。在2025年末达到顶峰的强劲反弹之后,主要数字资产的价格走势已转入防御阶段。例如,比特币目前交易价格接近68,800美元,较2025年10月创下的125,000美元历史高点显著下跌。此次回调恰逢山寨币普遍走弱,其波动性和流动性状况依然脆弱。

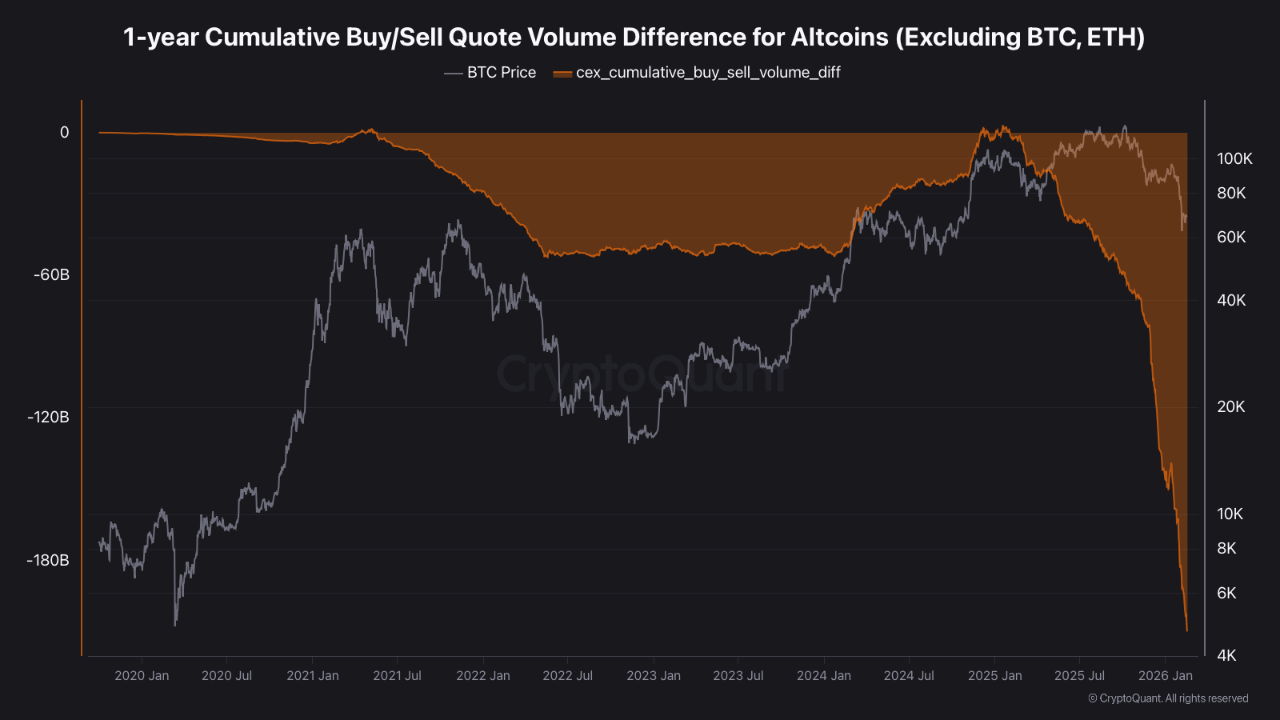

CryptoQuant的最新链上分析凸显了这一转变的规模。报告显示,排除比特币和以太坊后,山寨币的抛售压力已达到五年来的极端水平,累计买卖差额约为-2090亿美元。值得注意的是,就在2025年1月,该指标还接近中性,表明供需平衡。但自此之后,资金流动持续单向流出,指向持续性派发而非偶发性抛售。

这种长期失衡通常预示着结构性仓位调整,而非单纯的短期波动。虽然这不能自动确认长期熊市,但表明市场仍在消化过剩供应。因此,投资者持续关注流动性趋势、宏观环境以及需求能否在未来几个月内趋于稳定。

持续流出表明山寨币需求疲软

分析师指出,近期链上数据表明加密货币市场参与结构发生转变,而非暂时性回调。零售活动似乎已显著消退,而传统上被归类为"聪明钱"的资金已大量撤离山寨币领域。值得注意的是,目前山寨币领域几乎没有出现有意义的机构积累迹象,这强化了风险偏好降低的市场认知。

过去13个月内,排除比特币和以太坊的山寨币累计买卖差额已达到约-2090亿美元。重要的是,该数据反映的是中心化交易所现货市场的持续性净卖出,而非孤立的清算事件。这种流出的持续性使当前阶段区别于通常由杠杆清洗或偶发性恐慌驱动的短暂回调。

如此持续的派发表明边际买家的流动性支撑已显著减弱。实际上,这并不自动预示市场底部,而是表明需求尚未与供应重新建立平衡。

从历史经验看,复苏阶段往往只有在新增买家果断回归后才会开始。在这一转变实现之前,山寨币价格走势可能保持低迷,盘整或进一步下跌风险依然存在。