Written by: June, Deep Tide TechFlow

In January 2025, the meme coin market was at the peak of frenzy. As former U.S. President Donald Trump launched the TRUMP coin, an unprecedented wave of speculation swept through, with the wealth-creating myth of "100x coins" capturing the market's attention.

At the same time, a lawsuit against the Pump.fun platform was quietly initiated.

Fast forward to recent days.

Pump.fun co-founder and COO Alon Cohen has not made a sound on social media for over a month. For someone who is usually active and always online "surfing and catching up on gossip," this silence is particularly noticeable. Data shows that Pump.fun's weekly trading volume has plummeted from a peak of $3.3 billion in January to the current $481 million, a drop of over 80%. Meanwhile, the price of PUMP has fallen to $0.0019, down about 78% from its all-time high.

Looking back to July 12 a few months ago, the situation was completely different. Pump.fun's public sale was issued at a uniform price of $0.004 per token, selling out in 12 minutes and raising approximately $600 million, pushing sentiment to a climax.

From the excitement at the beginning of the year to the current chill, the market's attitude has formed a stark contrast.

Amid all these changes, the only thing that hasn't stopped is the buyback plan. The Pump.fun team is still methodically executing its daily buyback plan. As of now, the cumulative buyback amount has reached $216 million, digesting about 15.16% of the circulating supply.

At the same time, the lawsuit that was overlooked during the market frenzy is now quietly expanding.

Everything Started with the Loss on $PNUT

The story begins in January 2025.

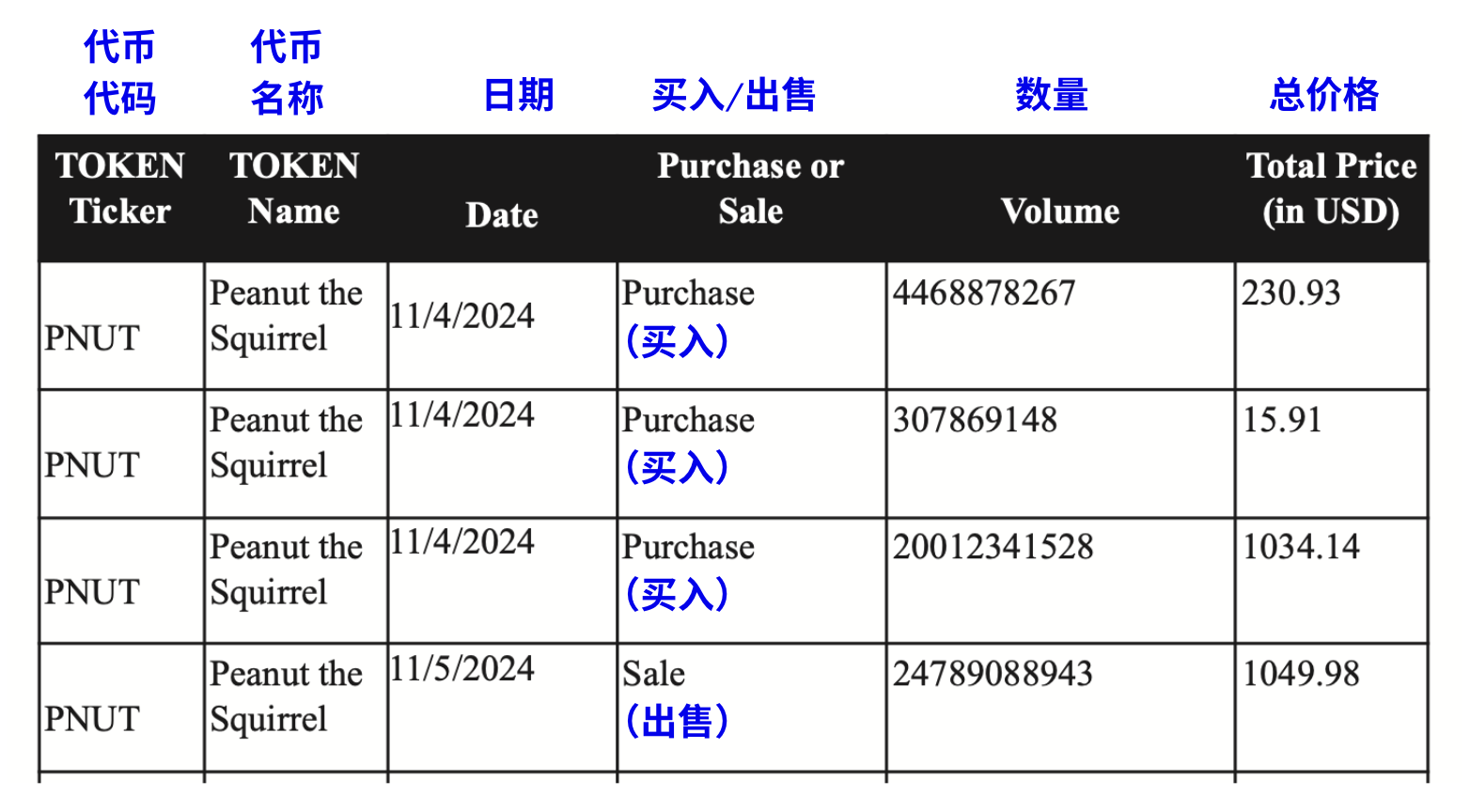

On January 16, investor Kendall Carnahan率先 filed a lawsuit in the Southern District of New York (case number: Carnahan v. Baton Corp.), targeting Pump.fun and its three founders. Carnahan's诉求 was clear: he suffered losses after purchasing $PNUT tokens on the platform and accused Pump.fun of selling unregistered securities, violating the U.S. Securities Act of 1933.

According to the court documents, the investor's actual loss amount was only $231.

Just two weeks later, on January 30, another investor, Diego Aguilar, filed a similar lawsuit (case number: Aguilar v. Baton Corp.). Unlike Carnahan, Aguilar purchased a wider variety of tokens, including $FRED, $FWOG, $GRIFFAIN, and other meme coins issued on the Pump.fun platform. His lawsuit had a broader scope, representing all investors who purchased unregistered tokens on the platform.

At this point, the two cases were proceeding independently, with the same defendants:

Pump.fun operating company Baton Corporation Ltd and its three founders, Alon Cohen (COO), Dylan Kerler (CTO), and Noah Bernhard Hugo Tweedale (CEO).

Cases Consolidated, Plaintiff with $240K Loss Becomes Lead Plaintiff

The two independent lawsuits quickly caught the court's attention. Judge Colleen McMahon of the Southern District of New York, who was presiding over the case, noticed a problem: the two cases targeted the same defendants, the same platform, and the same alleged violations, so why were they being handled separately?

On June 18, 2025, Judge McMahon directly questioned the plaintiffs' legal team:

Why were there two independent lawsuits addressing the same issue? She asked the lawyers to explain why the two cases should not be consolidated.

The plaintiffs' lawyers initially tried to argue, claiming that two separate cases could be maintained—one specifically for the $PNUT token and another for all tokens on the Pump.fun platform—and suggested appointing two separate lead plaintiffs.

But the judge was clearly not buying it. This "divide and conquer" strategy would not only waste judicial resources but could also lead to conflicting rulings in different cases. The key point was that all plaintiffs faced the same core issue: they all accused Pump.fun of selling unregistered securities and considered themselves victims of the same fraudulent system.

On June 26, Judge McMahon ruled to formally consolidate the two cases. At the same time, the judge, in accordance with the provisions of the Private Securities Litigation Reform Act (PSLRA), formally appointed the plaintiff with the largest losses, Michael Okafor, as the lead plaintiff (according to court records, Okafor lost approximately $242,000 in Pump.fun transactions, far exceeding the losses of other plaintiffs).

Thus, the investors, who had been fighting separately, formed a united front.

Targets Shift to Solana Labs and Jito

Just one month after the cases were consolidated, the plaintiffs dropped a bombshell.

On July 23, 2025, the plaintiffs submitted the "Consolidated Amended Complaint," and the list of defendants expanded dramatically. This time, the矛头 was no longer aimed solely at Pump.fun and its three founders but directly targeted core participants in the entire Solana ecosystem.

The newly added defendants included:

-

Solana Labs, Solana Foundation, and their executives (Solana Defendants): The plaintiffs alleged that Solana was more than just providing blockchain technology. According to the court documents, there was close technical coordination and communication between Pump.fun and Solana Labs, far exceeding an ordinary developer-platform relationship.

-

Jito Labs and its executives (Jito Defendants): The plaintiffs argued that it was Jito's MEV technology that allowed insiders to pay extra fees to ensure their transactions were prioritized, allowing them to buy tokens before ordinary users and achieve risk-free arbitrage.

The plaintiffs' strategy was clear: they试图 to prove that Pump.fun, Solana, and Jito were not operating independently but formed a tight-knit community of interest. Solana provided the blockchain infrastructure, Jito provided the MEV tools, and Pump.fun operated the platform—the three共同构建 a system that appeared decentralized but was actually manipulated.

Core Allegations: More Than Just "Losing Money"

Many might think this is just a group of investors throwing a fit after losing money speculating on coins. But a careful reading of the hundreds of pages of court documents reveals that the plaintiffs' allegations point to a carefully designed fraudulent system.

First Allegation: Sale of Unregistered Securities

This is the legal foundation of the entire case.

The plaintiffs argue that all meme tokens issued on the Pump.fun platform are essentially investment contracts. According to the *Howey Test, these tokens meet the definition of securities. However, the defendants never filed any registration statements with the U.S. Securities and Exchange Commission before publicly selling these tokens to the public, violating Sections 5, 12(a)(1), and 15 of the Securities Act of 1933.

When the platform sold tokens through its "bonding curve" mechanism, it also completely failed to disclose necessary risk information, financial status, or project background to investors—all information that must be provided when issuing securities.

Note: The Howey Test is a legal standard established by the U.S. Supreme Court in the 1946 case SEC v. W.J. Howey Co. to determine whether a specific transaction or plan constitutes an "investment contract." If it meets the criteria of this test, the asset is considered a "security" (Security), must be regulated by the U.S. Securities and Exchange Commission (SEC), and comply with the registration and disclosure requirements of the Securities Act of 1933 and the Securities Exchange Act of 1934.

Second Allegation: Operating an Illegal Gambling Enterprise

The plaintiffs define Pump.fun as a "Meme Coin Casino." They point out that users投入 SOL to buy tokens is essentially "placing a bet," the outcome of which depends primarily on luck and market speculation, not the actual utility of the token. The platform, as the "house," takes a 1% fee from each transaction, just like a casino taking a cut.

Third Allegation: Wire Fraud and False Advertising

Pump.fun表面上宣传 "Fair Launch," "No Presale," "Rug-proof," giving the impression that all participants are on a level playing field. But in reality, this is an outright lie.

The court documents指出 that Pump.fun secretly integrated MEV technology provided by Jito Labs. This means that insiders who knew the "inside story" and were willing to pay extra "tips" could use "Jito bundles" to buy tokens before ordinary users' transactions were executed, then immediately sell for profit after the price rose—this is所谓的 front-running.

Fourth Allegation: Money Laundering and Unlicensed Money Transmission

The plaintiffs accuse Pump.fun of receiving and transferring large amounts of money without obtaining any money transmission licenses. The court documents claim that the platform even assisted the North Korean hacker group Lazarus Group in laundering stolen funds. In a specific case, hackers issued a meme token named "QinShihuang" (秦始皇) on Pump.fun, using the platform's high traffic and liquidity to mix "dirty money" with legitimate trading funds from ordinary retail investors.

Fifth Allegation: Complete Lack of Investor Protection

Unlike traditional financial platforms, Pump.fun has no "Know Your Customer" (KYC) process, anti-money laundering (AML) protocols, or even the most basic age verification.

The plaintiffs' core argument can be summarized in one sentence: This is not a normal investment affected by market fluctuations, but a fraudulent system designed from the outset to make retail investors lose money and insiders profit.

This expansion意味着 the nature of the lawsuit has fundamentally changed. The plaintiffs are no longer satisfied with accusing Pump.fun of acting alone but are describing it as part of a larger "criminal network."

One month later, on August 21, the plaintiffs further submitted the "RICO Case Statement," formally accusing all defendants of共同 constituting a "racketeering enterprise" that, through Pump.fun's表面上 "fair launch platform,"实际上 operated a manipulated "Meme Coin Casino."

The plaintiffs' logic is clear: Pump.fun did not operate independently. Behind it, Solana provided the blockchain infrastructure, and Jito provided the MEV technology tools. The three formed a tight-knit community of interest, collectively defrauding ordinary investors.

But what evidence do the plaintiffs have to support these allegations? The answer was revealed a few months later.

Key Evidence: Mysterious Informant and Chat Records

After September 2025, the nature of the case underwent a fundamental转变.

Because the plaintiffs obtained hard evidence.

A "confidential informant" provided the plaintiffs' legal team with the first batch of internal chat records, numbering about 5,000. These chat records are alleged to come from internal communication channels within Pump.fun, Solana Labs, and Jito Labs, documenting technical coordination and business dealings among the three parties.

The emergence of this evidence was a treasure trove for the plaintiffs. Because all previous allegations—about technical collusion, MEV manipulation, and insider优先交易—were still at the speculative level, lacking direct evidence.

And these internal chat records, it is alleged, can prove the "conspiratorial relationship" among the three parties.

One month later, on October 21, this mysterious informant provided a second batch of files, this time even more staggering: over 10,000 chat records and related documents. These materials are alleged to detail:

-

How Pump.fun coordinated technical integration with Solana Labs

-

How Jito's MEV tools were embedded into Pump.fun's trading system

-

How the three parties discussed "optimizing" the trading process (which the plaintiffs believe is a euphemism for market manipulation)

-

How insiders traded using informational advantages

The plaintiffs' lawyers stated in court documents that these chat records "reveal a精心设计的欺诈网络," proving that the relationship between Pump.fun, Solana, and Jito was far more than just表面上的 "technical partners."

Motion for Second Amended Complaint

Faced with such a massive amount of new evidence, the plaintiffs needed time to organize and analyze it. On December 9, 2025, the court granted the plaintiffs' request to file a "Second Amended Complaint," allowing them to incorporate this new evidence into the lawsuit.

But a problem arose: over 15,000 chat records needed to be逐一 reviewed,筛选, translated (some可能 be in non-English languages), and analyzed for their legal significance—a huge workload.加上 the upcoming Christmas and New Year holidays, the plaintiffs' legal team明显 didn't have enough time.

On December 10, the plaintiffs filed a motion with the court requesting an extension of the deadline for submitting the "Second Amended Complaint."

Just one day later, on December 11, Judge McMahon approved the extension request. The new deadline was set for January 7, 2026. This means that after the New Year, a "Second Amended Complaint" that may contain even more explosive allegations will be presented to the court.

Current Status of the Case

As of now, this lawsuit has been ongoing for nearly a year, but the real battle is just beginning.

On January 7, 2026, the plaintiffs will submit the "Second Amended Complaint" containing all the new evidence, at which point we will see what those 15,000 chat records actually reveal. Meanwhile, the defendant side has been unusually quiet. Pump.fun co-founder Alon Cohen has not spoken on social media for over a month, and executives from Solana and Jito have not made any public response to the lawsuit.

Interestingly, despite the lawsuit's growing scale and influence, the cryptocurrency market doesn't seem to care much. Solana's price has not experienced剧烈波动 due to the lawsuit, and while the $PUMP token's price continues to fall, it's more due to the collapse of the overall meme coin narrative than the impact of the lawsuit itself.

Epilogue

This lawsuit, which began over losses from trading meme coins, has evolved into a class action lawsuit against the entire Solana ecosystem.

The case has also gone beyond the scope of "a few investors维权 over losing money." It touches on the core issues of the cryptocurrency industry: Is decentralization real, or is it an精心包装的幻象? Is a fair launch truly fair?

However, many key questions remain unanswered:

-

Who exactly is that mysterious informant? A former employee? A competitor? Or an undercover agent from a regulatory agency?

-

What exactly is in those 15,000 chat records? Is it conclusive evidence of collusion, or is it normal business communication taken out of context?

-

How will the defendants defend themselves?

In 2026, with the submission of the "Second Amended Complaint" and the advancement of the case审理, we may get some answers.