TL;DR

If you regularly follow the price fluctuations of NVIDIA, Microsoft, Bitcoin, or Ethereum, you typically focus on tracking core variables such as U.S. inflation data, the Federal Reserve's interest rate policy path, AI-related revenue realization, and on-chain capital flows. But this week, the market's attention has been captured by what seems like a more distant variable: the direction of the Bank of Japan's interest rates.

The reason is not complicated. For many years, the yen has been one of the cheapest funding currencies in the world. Investors could borrow low-interest yen, convert it into dollars or other currencies, and then buy higher-yielding, faster-appreciating assets. This is the yen carry trade, simply put, borrowing low-interest yen to buy high-yield assets.

It may not directly appear on a particular AI stock or a specific Bitcoin address, but it can affect global risk appetite and leverage costs. Now, the Bank of Japan is exiting its long-term ultra-low interest rate environment, and the market is beginning to recalculate how much longer this 'low-interest credit card' can be swiped.

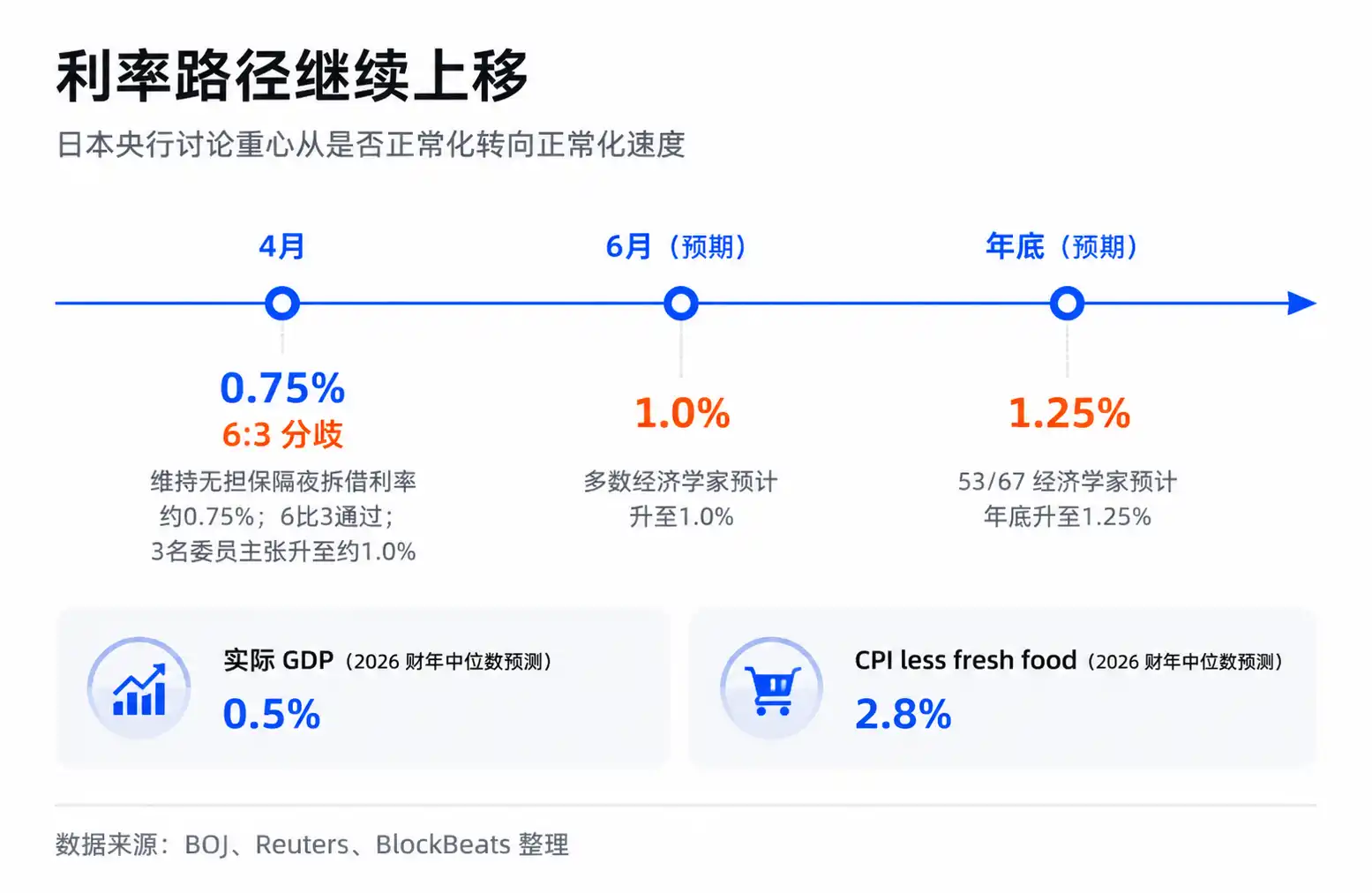

According to a Reuters report on June 10, 66 out of 70 economists expect the Bank of Japan to raise its policy rate from 0.75% to 1.0% at its June meeting. In another survey, 53 out of 67 economists expect the rate to rise to 1.25% by year-end. This meeting will conclude on June 16th. As of June 15th, 1.0% remains the economists' survey expectation, not an already announced result.

25 basis points may seem small. What the market fears is not the number 'Japanese interest rates reaching 1%', but whether assets that have relied on cheap funding, crowded positions, and high-risk appetites will be repriced after long-term cheap money starts to become more expensive. AI mega-tech and crypto are precisely the most sensitive terminals on this chain.

The Bank of Japan Affects the Global Funding Foundation

Think of the yen carry trade as a low-interest credit card. As long as the borrowing cost is low enough, the exchange rate stable enough, and the target assets rise fast enough, investors are willing to swipe this card to add leverage. The yen has long played the role of this global credit card.

This card is important because it doesn't just serve the Japanese market. Low-interest yen can be converted into dollars, flowing into U.S. stocks, bonds, emerging markets, commodities, and also indirectly affecting the risk appetite in crypto markets. When global asset prices rise, carry trades amplify liquidity. When the yen appreciates or Japanese interest rates rise, this chain works in reverse, forcing some funds to reduce positions, repay loans, and cut leverage.

Therefore, investors cannot judge its market impact solely based on 'the size of the Japanese economy.' The Bank of Japan is changing not the profit outlook of one local industry, but a long-term, low-cost foundation within the global funding map.

The April meeting already signaled this. At that time, the BOJ maintained the uncollateralized overnight call rate at around 0.75%, but the vote was 6 to 3, with 3 members already advocating an immediate hike to around 1.0%. In its Outlook Report that same month, the BOJ lowered its real GDP forecast for fiscal 2026 to 0.5% and raised its core CPI forecast to 2.8%. The policy discussion has shifted from whether to normalize to how fast normalization should be.

The market consensus remains relatively mild: the BOJ will raise rates gradually, with ample policy communication, and part of the yen carry trade has already been unwound during past bouts of volatility. But the risk framework looks at something else. As long as residual leverage remains, what triggers volatility is often not the absolute level of interest rates, but the speed of change in interest rate differentials and exchange rate expectations.

For AI stocks and crypto, this speed matters. They are both high-beta assets, meaning assets with greater price elasticity. They rise more sharply when liquidity is loose and fall faster when risk appetite declines. AI leaders have real revenue and industry trend support, and Bitcoin also has ETFs, the halving cycle, and on-chain structures, but their marginal pricing still highly depends on global risk appetite.

When cheap money diminishes, the market may not immediately reject the AI or crypto narratives, but it may lower the valuation multiples it is willing to pay for future growth.

25bp Amplified by Leverage and Exchange Rates

Looking solely at 25 basis points, a Japanese rate hike shouldn't seem likely to shock global assets. The problem is that carry trades are not simple comparisons of deposits and loans; they are a system layered with leverage, exchange rates, and crowded positions.

A typical yen carry trade has three sources of return: low borrowing cost in yen, high returns on purchased assets, and a stable or depreciating yen. As long as these three hold, the trade is comfortable. Once Japanese rates rise, the first source of return is compressed. If the market begins to expect yen appreciation, the third source becomes a risk. Investors not only earn less but may also lose money on the exchange rate.

That's why 1% itself isn't necessarily scary, but moving from 0.75% towards 1.0%, with the market expecting 1.25% by year-end, changes the calculus for capital. What carry trades fear most is not a slow rise in cost, but everyone simultaneously realizing the same trade is no longer profitable and then rushing to unwind.

Unwinding transmits local Japanese policy to global risk assets. Investors need to buy back yen to repay debt, potentially selling dollar-denominated assets, tech stocks, crypto, commodities, or emerging market positions. If many funds act similarly at the same time, price declines can trigger more risk controls, margin calls, and volatility model adjustments, creating secondary amplification.

The IMF noted in its April 2026 Global Financial Stability Report that carry trade unwinding could amplify market volatility through channels like capital flows, bond yield volatility, leveraged ETFs, and non-bank financial institution deleveraging. The key point here is not that a particular downturn is solely caused by the BOJ, but that this mechanism exists and can exacerbate shocks when liquidity is tight.

Over the past two years, the market has repeatedly seen similar phenomena: momentum stocks, AI tech stocks, and Bitcoin experiencing synchronized volatility without clear new Fed signals or a sudden deterioration in single-company fundamentals. Institutional analysis often cites yen carry trade unwinding as one explanation. Strictly speaking, this can only prove a high temporal coincidence and a plausible mechanism, not sole causation. But for trading, correlation and transmission mechanisms are sufficient to constitute a risk variable.

The Market Is Trading on Higher Funding Hurdles

More precisely, the market is not trading on 'Japan's rate hike destroying AI,' but on 'higher funding hurdles for global risk assets.' These are two different things.

The AI rally still has its own main drivers. Cloud provider capital expenditures, GPU demand, model application deployment, enterprise software revenue—these are the long-term fundamentals for companies like NVIDIA and Microsoft. Bitcoin also has its own main drivers, including ETF inflows, regulatory frameworks, macro hedging narratives, and on-chain supply structure. The BOJ will not replace these variables.

But at high valuation stages, fundamentals answer whether there is long-term value, while liquidity answers what multiple the market is willing to pay for that future. When global low-cost funding is more abundant, investors are more willing to pay a high price for future growth. When funding costs rise and risk appetite falls, the same growth story may be discounted more heavily.

This is the meaning of implicit funding cost. It may not manifest as a rise in a specific company's loan rate, nor does it necessarily mean a specific fund directly borrowed yen. It's more like the overall leverage temperature of the market: when money is cheap, investors chase high-volatility assets. When money becomes expensive, the market's tolerance for losses, distant profits, and valuation bubbles declines.

Therefore, the market significance of this BOJ meeting does not lie in whether 1% is a high interest rate. In the U.S. or many emerging markets, 1% is certainly not high. But in the history of the yen as a global funding currency, it represents a change in direction. A pipeline of capital that has long provided cheap leverage is moving from extremely low cost towards normal cost.

'Most carry trades have already been unwound' also does not mean the risk disappears. Some trades have indeed been reduced in past volatility, and the market has also digested the June hike expectation in advance. But as long as residual exposure remains within the banking system, offshore yen lending, and non-bank leverage, prices will remain sensitive to the speed of normalization.

More importantly, the yen is just one visible anchor point. Global risk assets in recent years have not relied solely on the Fed but also on various low-cost funding currencies, offshore liquidity, and cross-market leverage. When these funding sources simultaneously become less cheap, a dovish Fed pivot may not fully offset the marginal tightening from other currency systems.

Post-Decision, Watch Linkage Between Yen, JGBs, and High-Beta Assets

The verification point for this narrative is clear: after the Bank of Japan's decision on June 16th, does the market just 'buy the rumor, sell the fact,' or does it begin repricing a faster normalization path?

If the BOJ raises to 1.0% as per the economists' survey expectation, but its tone is dovish, USD/JPY reacts calmly, and U.S. tech stocks and crypto do not come under synchronized pressure, then this looks more like a digested policy event. The market will continue to refocus on AI revenue, the Fed's path, and the U.S. earnings cycle, with Japan being a short-term disturbance.

If the decision or subsequent remarks lead the market to price in a year-end 1.25% or even higher path earlier, with the yen appreciating rapidly and Japanese bond yields rising, while NVIDIA, other momentum tech stocks, BTC, and ETH experience synchronized volatility, it would indicate investors are starting to trade not the 25 basis points, but a renewed contraction in the yen leverage chain.

Next, watch the linkage between prices: does yen strength accompany weakness in high-beta assets, does volatility rise without new U.S. negatives, do leveraged ETFs and crowded momentum stocks bear the brunt first. As long as these signals appear together, the Bank of Japan is no longer just the Bank of Japan—it is reminding the market that the map of global cheap money is becoming more expensive.