Bitcoin entered March on the back of strong momentum, rallying to a high of $76,000 and positioning for its first bullish monthly close in half a year. However, that narrative has since unraveled.

Early optimism, fueled by geopolitical developments involving the U.S, Iran, and Gulf states, has given way to macro-driven caution. At the time of writing, Bitcoin [BTC] was trading near $66,126, holding key levels but showing signs of vulnerability as sentiment shifts.

Bond yields climb, tightening the screws

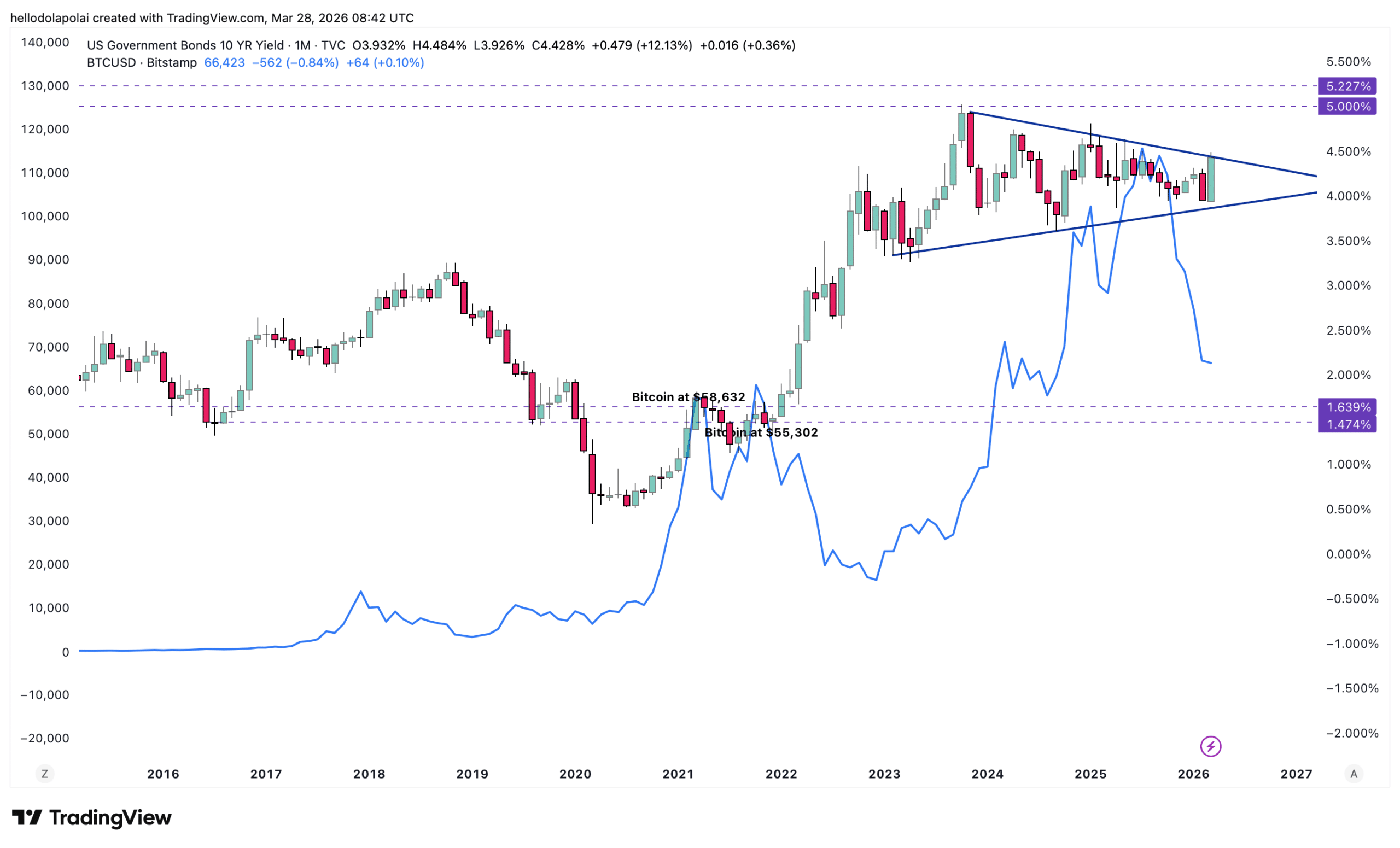

The U.S 10-year Treasury yield has emerged as a central driver of market direction. In fact, the press time price action seemed to suggest that the yield may be consolidating within a bullish flag pattern, typically a precursor to further upside.

A confirmed breakout could push yields towards the 5.0% level or higher, revisiting highs last seen in 2023. Such a move would likely accelerate capital rotation out of risk assets.

Higher yields tend to strengthen the appeal of fixed-income instruments, drawing liquidity away from speculative markets. For Bitcoin, this dynamic has historically translated into downside pressure.

Between October 2021 and December 2022, for instance, yields rose from 1.45% to 3.90%. All while Bitcoin fell from $67,000 to $16,256 over the same period.

If yields extend towards 5%, Bitcoin could retrace towards its next demand zone between $58,632 and $55,302.

ETF flows flip as U.S investors de-risk

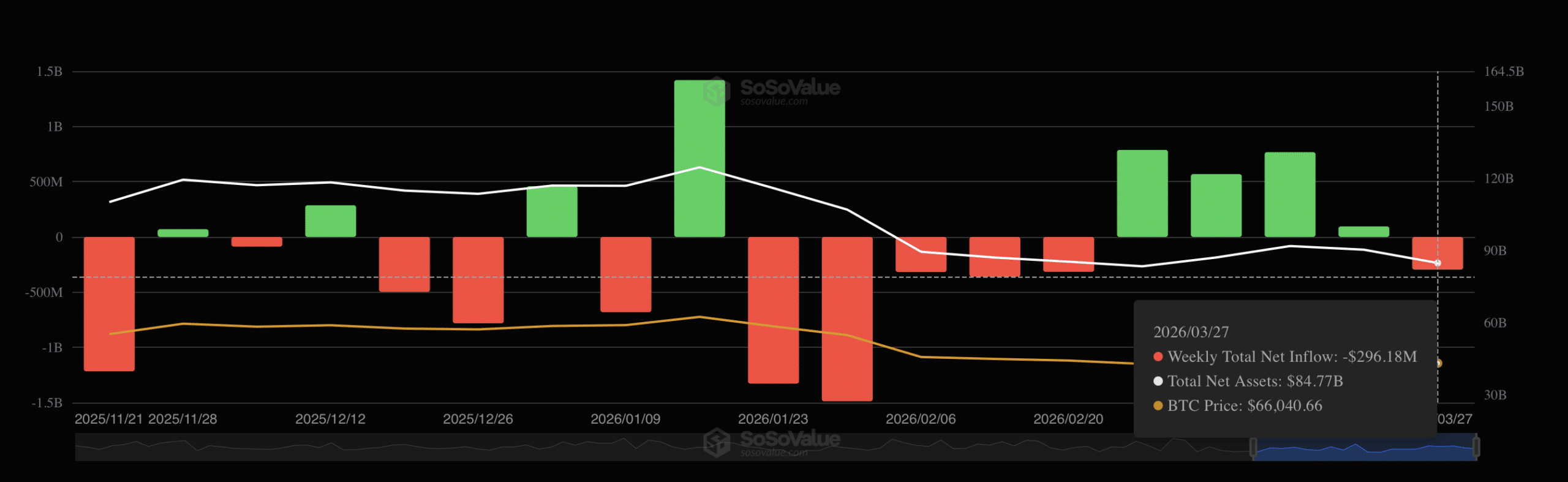

Institutional sentiment in the U.S is beginning to turn too. In fact, Spot Bitcoin exchange-traded funds have recorded their first meaningful outflows in five weeks – Signaling a shift towards a risk-off posture.

Roughly $296 million exited these funds over the past week, reversing part of the $2.12 billion accumulated over the previous four weeks. The shift suggested that recent buyers may be beginning to unwind positions as macro risks intensify.

Late-February data reflected this trend best. Between 26-27 February alone, outflows reached approximately $396.7 million, highlighting how quickly sentiment can reverse.

With only a few trading sessions left in March, sustained selling could now cement the bearish monthly close.

Oil surge fuels inflation concerns

Here, the inflation backdrop remains a key variable. Crude oil prices have surged sharply, adding pressure to an already fragile macro environment.

Brent crude has already climbed from around $75 at the start of the month to approximately $106, while WTI crude was trading near $101 at press time. The move alluded to supply disruptions and geopolitical tensions, both of which risk sustaining inflation at elevated levels.

Persistently high energy prices limit the likelihood of near-term monetary easing, keeping yields elevated and financial conditions tight.

In fact, recent analysis pointed to oil-driven inflation as a direct headwind for Bitcoin, particularly amid disruptions tied to the Strait of Hormuz. While market analysts argue that Bitcoin could act as a hedge, current price action suggests it remains closely tied to broader liquidity conditions.

Final Summary

- The U.S 10-year Treasury yield is approaching a breakout, raising the risk of a broader market repricing.

- U.S investors have begun offloading Bitcoin, as oil-driven inflation continues to complicate the macro outlook.