At the end of the year, annual review and outlook reports from various institutions are being released.

Adhering to the principle of being too long to read, we also attempt to provide quick summaries and extracts of these lengthy reports.

This report comes from CoinShares, a leading European digital asset investment management company founded in 2014, headquartered in London, UK, and Paris, France, with assets under management exceeding $6 billion.

This 77-page report, "Outlook 2026: The Year Utility Wins," covers core topics such as macroeconomic foundations, Bitcoin mainstreaming, the rise of hybrid finance, smart contract platform competition, and the evolution of the regulatory landscape. It also provides in-depth analysis of细分领域 including stablecoins, tokenized assets, prediction markets, mining transformation, and venture capital.

Below is our提炼 and summary of the report's core content:

I. Core Theme: The Arrival of the Year of Utility

2025 was a turning point for the digital asset industry, with Bitcoin hitting a new all-time high, marking a shift from speculation-driven to utility-value-driven.

2026 is expected to be the "Year Utility Wins," where digital assets no longer attempt to replace the traditional financial system but rather enhance and modernize the existing system.

The report's core view is: 2025 marked a decisive shift for digital assets from speculation-driven to utility-value-driven, and 2026 will be a critical year for the acceleration and implementation of this transformation.

Digital assets are no longer trying to build a parallel financial system but are enhancing and modernizing the existing traditional financial system. The integration of public blockchains, institutional liquidity, regulated market structures, and real economic use cases is progressing at a pace exceeding optimistic expectations.

II. Macroeconomic Foundations and Market Outlook

Economic Environment: A Soft Landing on Thin Ice

Growth Expectations: The economy may avoid a recession in 2026, but growth will be weak and fragile. Inflation continues to ease but not decisively; tariff disruptions and supply chain restructuring keep core inflation at levels not seen since the early 1990s.

Fed Policy: Cautious rate cuts are expected, potentially bringing the target rate to the mid-3% range, but the process will be slow. The Fed, remembering the 2022 inflation surge, is reluctant to pivot quickly.

Three Scenario Analyses:

· Optimistic Scenario: Soft Landing + Productivity Surprise, Bitcoin could break $150,000

· Baseline Scenario: Slow Expansion, Bitcoin trading range $110,000 - $140,000

· Bear Market Scenario: Recession or Stagflation, Bitcoin could fall to the $70,000 - $100,000 range

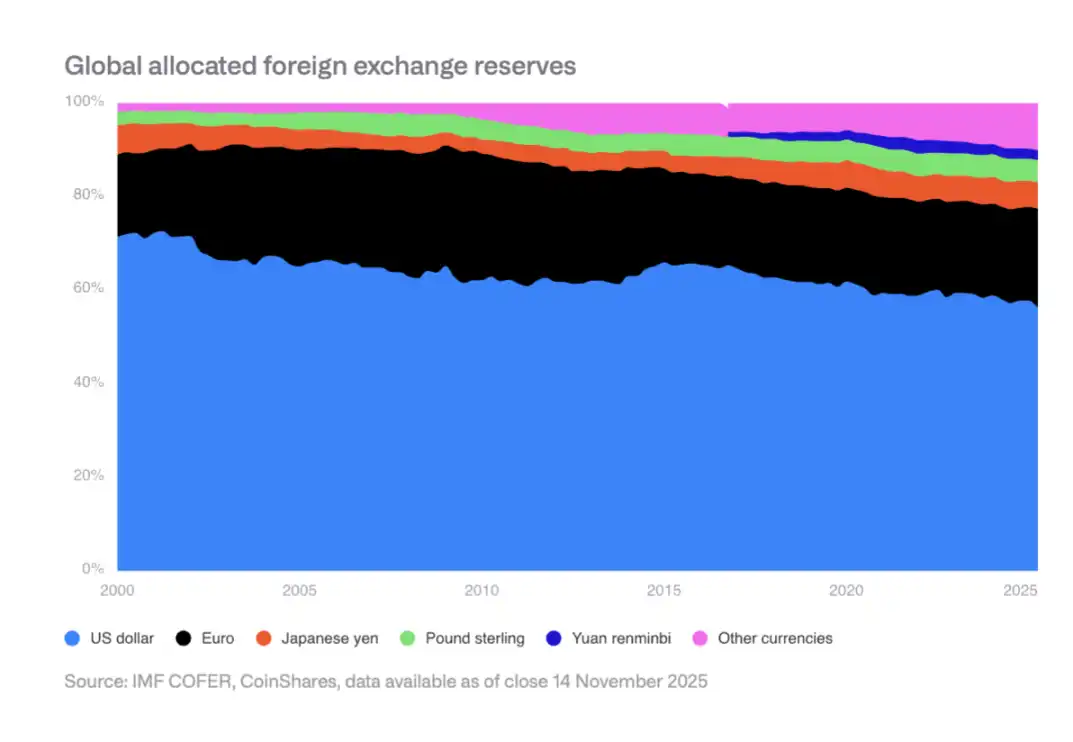

Slow Erosion of the Dollar's Reserve Status

The US dollar's share of global foreign exchange reserves has fallen from 70% in 2000 to the mid-50% range currently. Emerging market central banks are diversifying, increasing holdings of assets like the Renminbi and gold. This creates a structural tailwind for Bitcoin as a non-sovereign store of value.

III. Bitcoin's Mainstreaming Process in the US

2025 saw several breakthroughs in the US, including:

· Approval and launch of spot ETFs

· Formation of a top-tier ETF options market

· Removal of retirement plan restrictions

· Application of fair value accounting rules for corporations

· The government listing Bitcoin as a strategic reserve

Institutional Adoption Still in Early Stages

Although structural barriers have been removed, actual adoption is still limited by traditional financial processes and intermediaries. Wealth management channels, retirement plan providers, corporate compliance teams, etc., are still gradually adapting.

2026 Expectations

Key progress is expected from the private sector: the big four brokerages opening Bitcoin ETF allocations; at least one major 401(k) provider allowing Bitcoin allocation; at least two S&P 500 companies holding Bitcoin; at least two major custody banks offering direct custody services, etc.

IV. Miner and Corporate Bitcoin Holding Risks

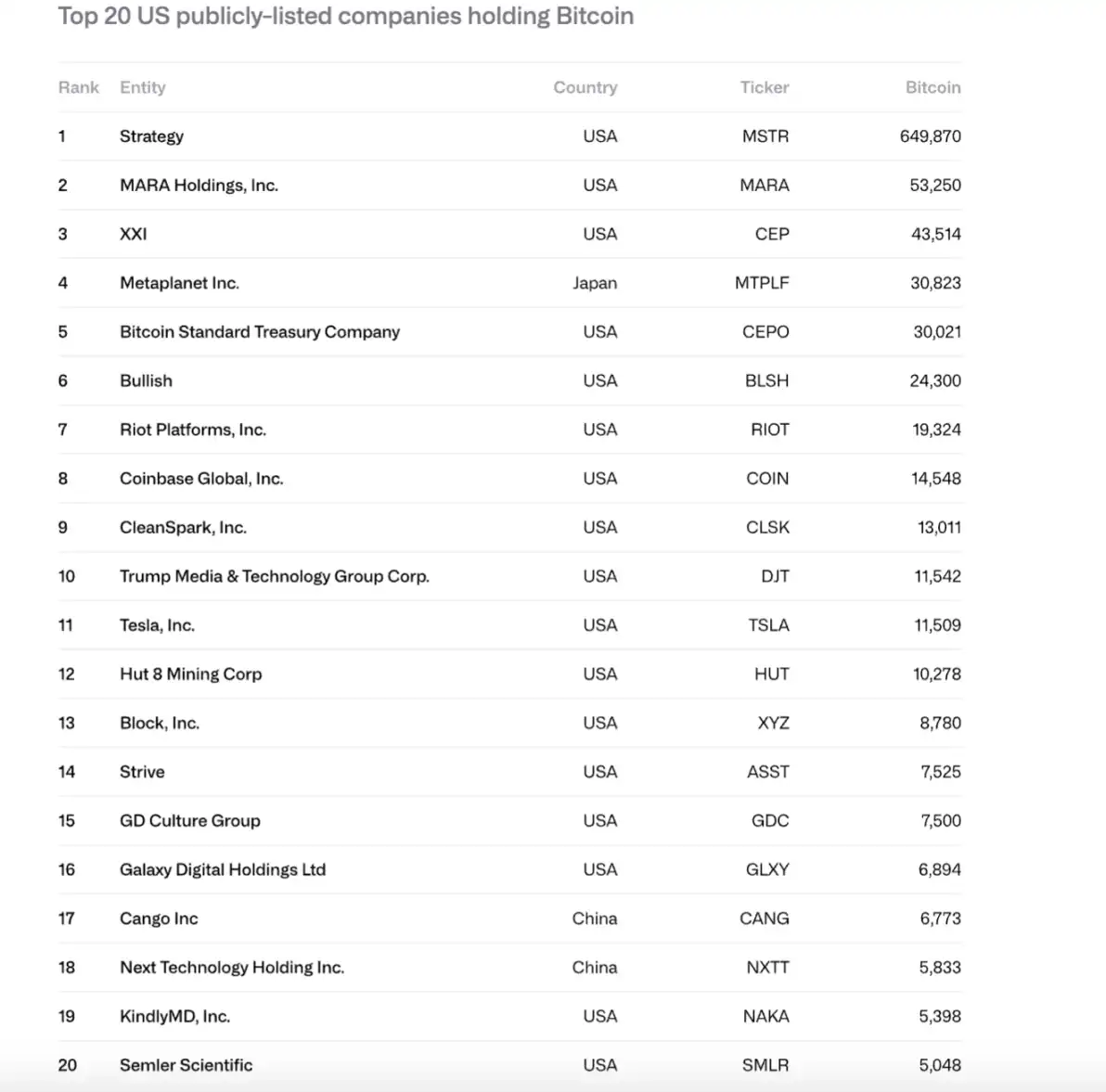

Surge in Corporate Holdings

From 2024-2025, publicly traded companies' Bitcoin holdings increased from 266,000 to 1.048 million coins, with total value rising from $11.7 billion to $90.7 billion. MicroStrategy (MSTR) accounts for 61%, and the top 10 companies control 84%.

Potential Selling Risks

MicroStrategy faces two major risks:

· Inability to fund perpetual debt and cash flow obligations (annual cash flow nearly $680 million)

· Refinancing risk (most recent bonds mature Sept 2028)

If mNAV approaches 1x or it cannot refinance at low rates, it may be forced to sell Bitcoin, triggering a vicious cycle.

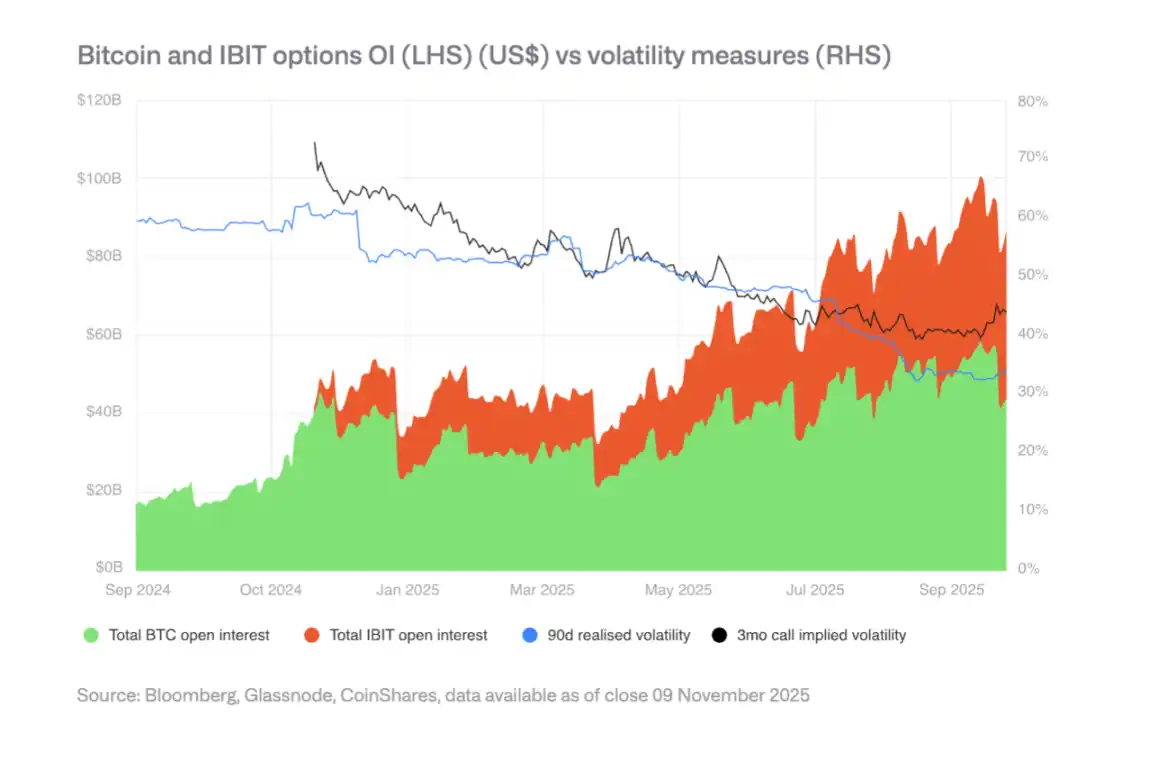

Options Market and Declining Volatility

The development of the IBIT options market has reduced Bitcoin's volatility, a sign of maturation. But lower volatility may weaken demand for convertible bonds, affecting corporate purchasing power. A turning point in volatility decline occurred in Spring 2025.

V. Diverging Regulatory Landscape

EU: MiCA's Clarity

The EU has the world's most comprehensive crypto asset legal framework, covering issuance, custody, trading, and stablecoins. But 2025 exposed coordination limits, with some national regulators potentially challenging the passporting system.

US: Innovation and Fragmentation

The US regained momentum with its deep capital markets and mature VC ecosystem, but regulation remains fragmented across the SEC, CFTC, Fed, and others. Stablecoin legislation (GENIUS Act) has passed, but implementation is ongoing.

Asia: Moving Towards Prudential Regulation

Hong Kong China, Japan, etc., are advancing Basel III crypto capital and liquidity requirements; Singapore maintains a risk-based licensing system. Asia is forming a more coherent regulatory bloc, converging around risk-based, bank-aligned standards.

VI. The Rise of Hybrid Finance (HyFi)

Infrastructure and Settlement Layer

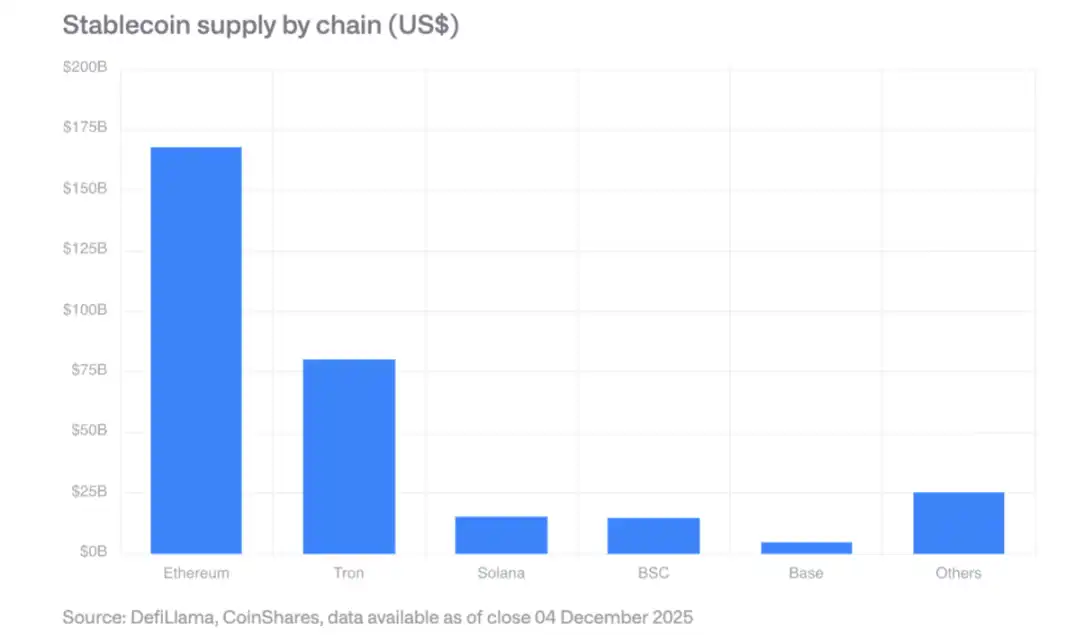

Stablecoins: Market size exceeds $300 billion, Ethereum holds the largest share, Solana is growing fastest. The GENIUS Act requires compliant issuers to hold US Treasury reserves, creating new demand for Treasuries.

Decentralized Exchanges (DEXs): Monthly trading volume exceeds $600 billion; Solana handles $40 billion in daily volume.

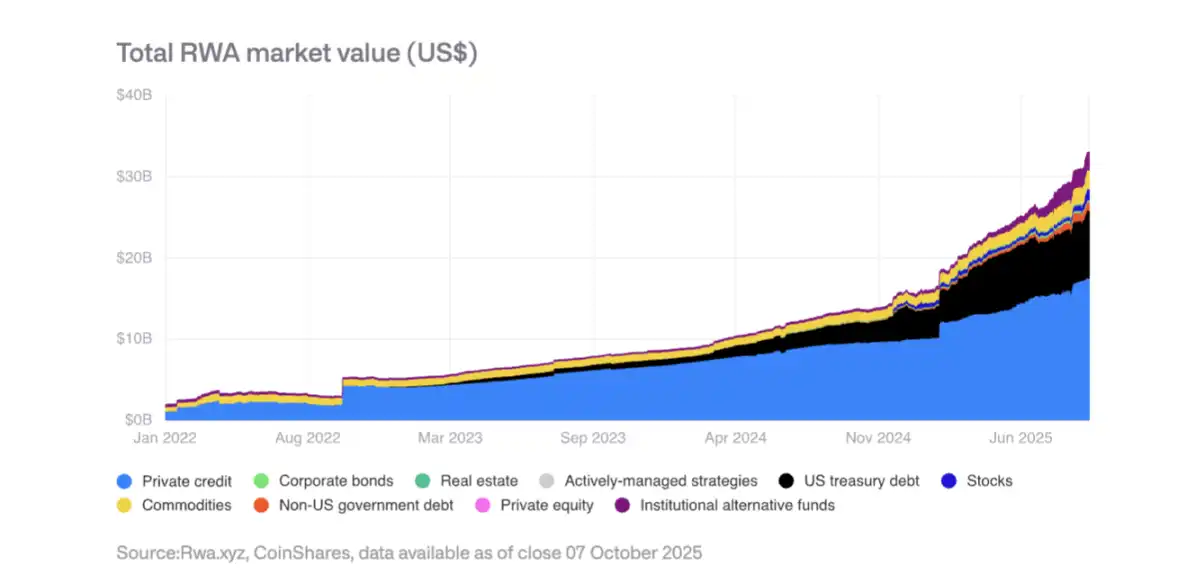

Tokenized Real World Assets (RWA)

The total value of tokenized assets grew from $15 billion at the start of 2025 to $35 billion. Private credit and US Treasury tokenization grew fastest; gold tokenization exceeds $1.3 billion. BlackRock's BUIDL fund assets expanded significantly; JPMorgan launched JPM Coin tokenized deposits on Base.

Revenue-Generating On-Chain Applications

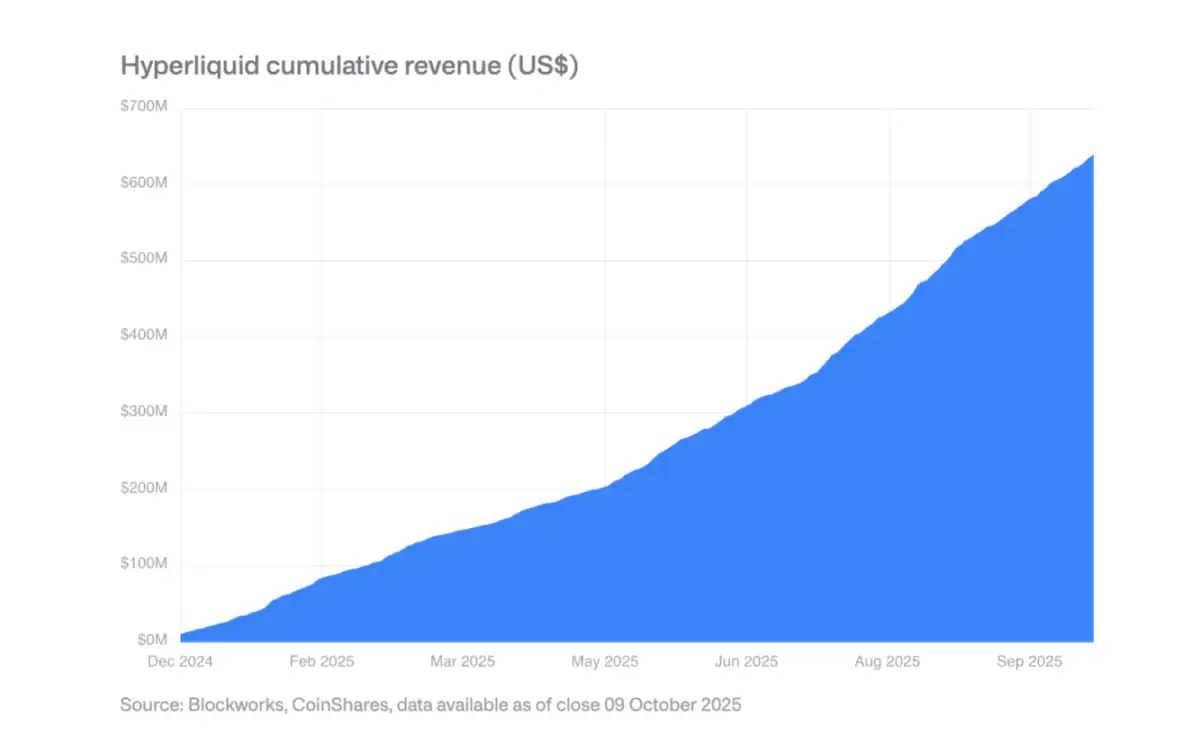

More protocols are generating hundreds of millions in annual revenue distributed to token holders. Hyperliquid uses 99% of revenue for daily token buybacks; Uniswap and Lido have launched similar mechanisms. This marks a shift for tokens from purely speculative assets to equity-like assets.

VII. Stablecoin Dominance and Corporate Adoption

Market Concentration

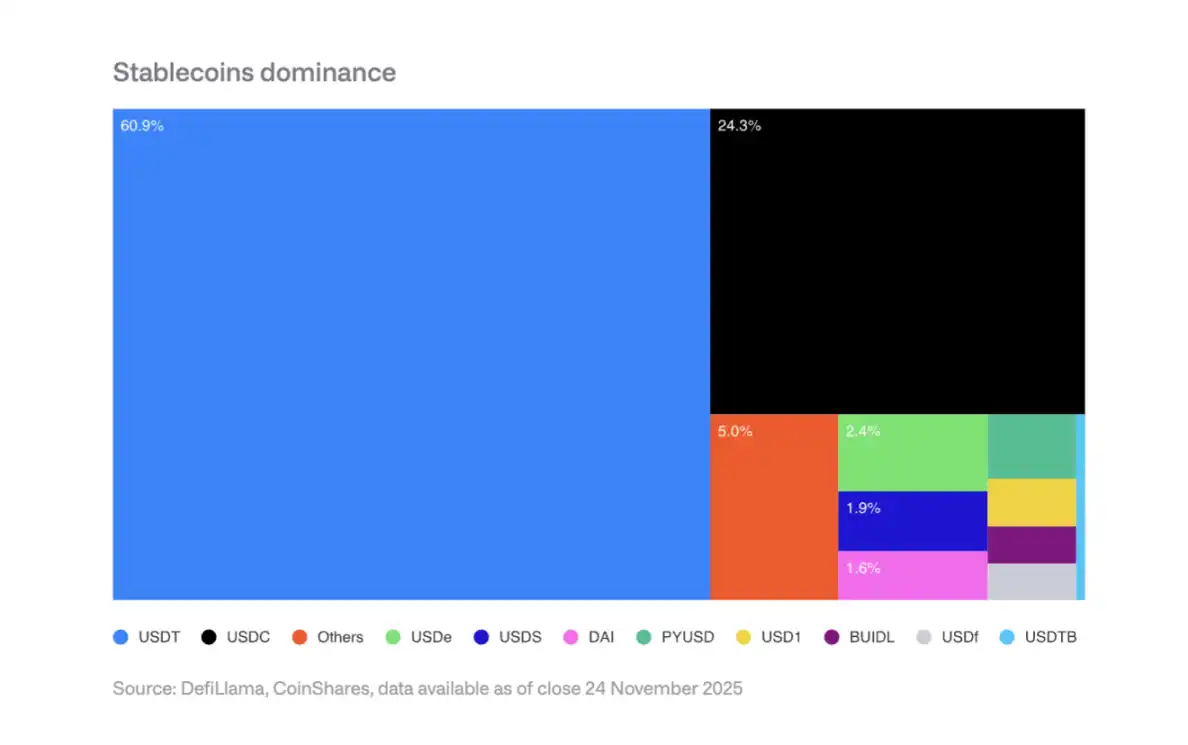

Tether (USDT) holds 60% of the stablecoin market, Circle (USDC) holds 25%. New entrants like PayPal's PYUSD face network effect challenges, finding it difficult to shake up the duopoly.

2026 Corporate Adoption Expectations

Payment Processors: Visa, Mastercard, Stripe, etc., have structural advantages and can switch to stablecoin settlement without changing the front-end experience.

Banks: JPMorgan's JPM Coin has demonstrated potential; Siemens reported FX savings of up to 50%, settlement times reduced from days to seconds.

E-commerce Platforms: Shopify already accepts USDC checkout; Asian and Latin American markets are piloting stablecoin supplier payments.

Revenue Impact

Stablecoin issuers face interest rate decline risks: If the Fed rate drops to 3%, they would need to issue an additional $88.7 billion in stablecoins to maintain current interest income.

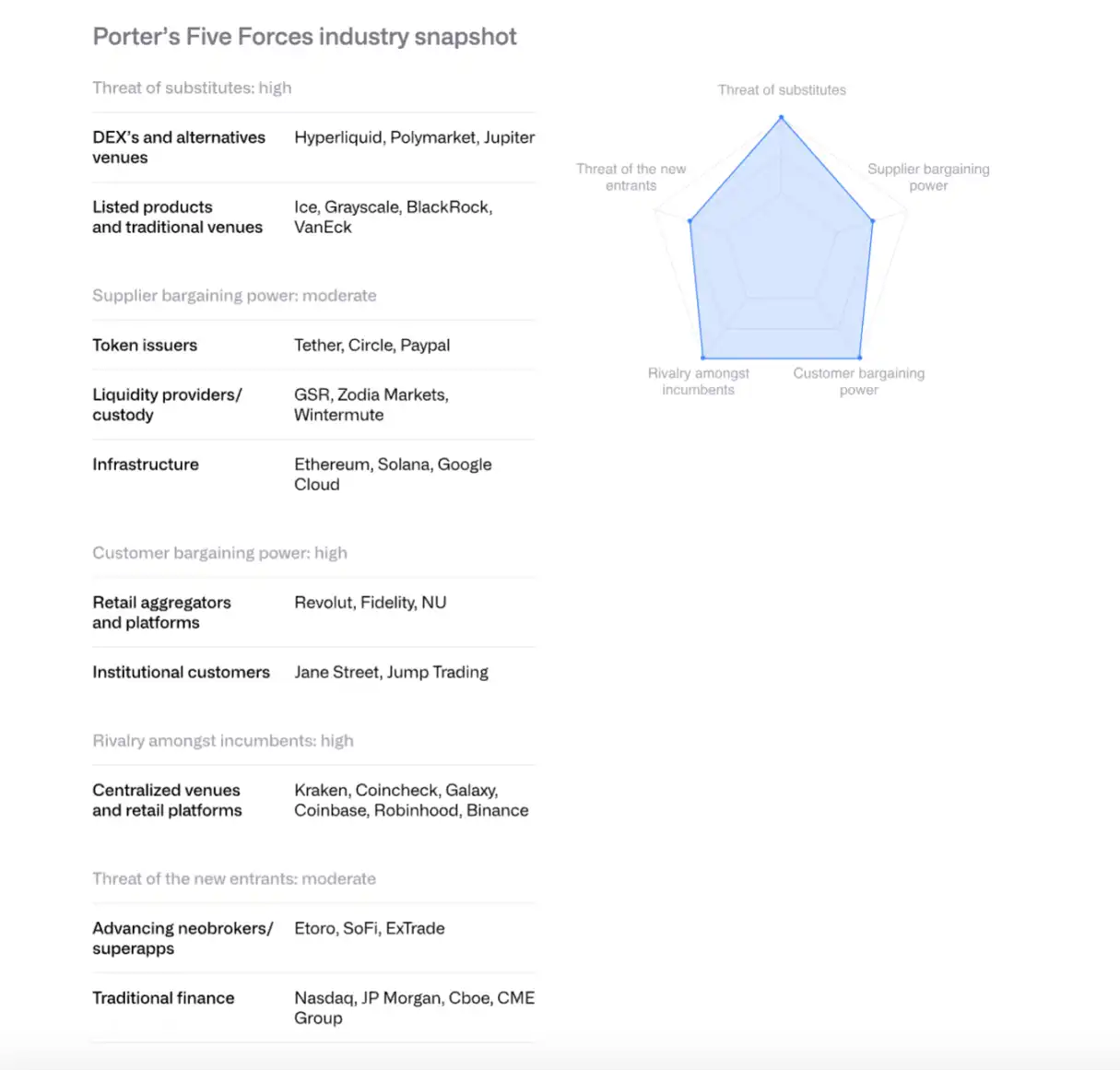

VIII. Analyzing Exchange Competition with Porter's Five Forces

Existing Competitors: Competition is fierce and intensifying, with fee rates dropping to low single-digit basis points.

Threat of New Entrants: Traditional financial institutions like Morgan Stanley's E*TRADE, Charles Schwab are preparing to enter but短期内 rely on partners.

Supplier Bargaining Power: Stablecoin issuers (e.g., Circle) enhance control through networks like Arc. Coinbase's revenue-sharing agreement with Circle for USDC is crucial.

Customer Bargaining Power: Institutional clients account for over 80% of Coinbase's volume and have strong bargaining power. Retail users are price-sensitive.

Threat of Substitutes: Decentralized exchanges like Hyperliquid, prediction markets like Polymarket, and CME crypto derivatives pose competition.

Industry consolidation is expected to accelerate in 2026, with exchanges and large banks acquiring customers, licenses, and infrastructure through M&A.

IX. Smart Contract Platform Competition

Ethereum: From Sandbox to Institutional Infrastructure

Ethereum achieved scaling through its rollup-centric roadmap; Layer-2 throughput increased from 200 TPS a year ago to 4800 TPS. Validators are pushing to increase the base layer Gas limit. The US spot Ethereum ETF attracted approximately $13 billion in inflows.

In institutional tokenization, BlackRock's BUIDL fund and JPMorgan's JPM Coin demonstrate Ethereum's potential as an institutional-grade platform.

Solana: The High-Performance Paradigm

Solana stands out with its monolithic, highly optimized execution environment, accounting for ~7% of total DeFi TVL. Stablecoin supply exceeds $12 billion (up from $1.8B in Jan 2024), RWA projects are expanding; BlackRock's BUIDL grew from $25M in Sept to $250M.

Technical upgrades include the Firedancer client, DoubleZero validator communication network, etc. The spot ETF launched on Oct 28 attracted $382 million in net inflows.

Other High-Performance Chains

New generation Layer-1s like Sui, Aptos, Sei, Monad, Hyperliquid compete through architectural differentiation. Hyperliquid focuses on derivatives trading, accounting for over a third of blockchain revenue. But market fragmentation is severe, and EVM compatibility is a competitive advantage.

X. Mining's Transformation to HPC (High-Performance Computing)

2025 Expansion

Listed miners' hash rate grew by 110 EH/s, primarily from Bitdeer, HIVE Digital, and Iris Energy.

HPC Transformation

Miners announced HPC contracts worth $65 billion; the share of Bitcoin mining revenue is expected to drop from 85% to below 20% by the end of 2026. HPC business operating margins are 80-90%.

Future Mining Models

Future mining is expected to be dominated by: ASIC manufacturers, modular mining, intermittent mining (coexisting with HPC), sovereign nation mining. Long-term, mining may return to small-scale, decentralized operations.

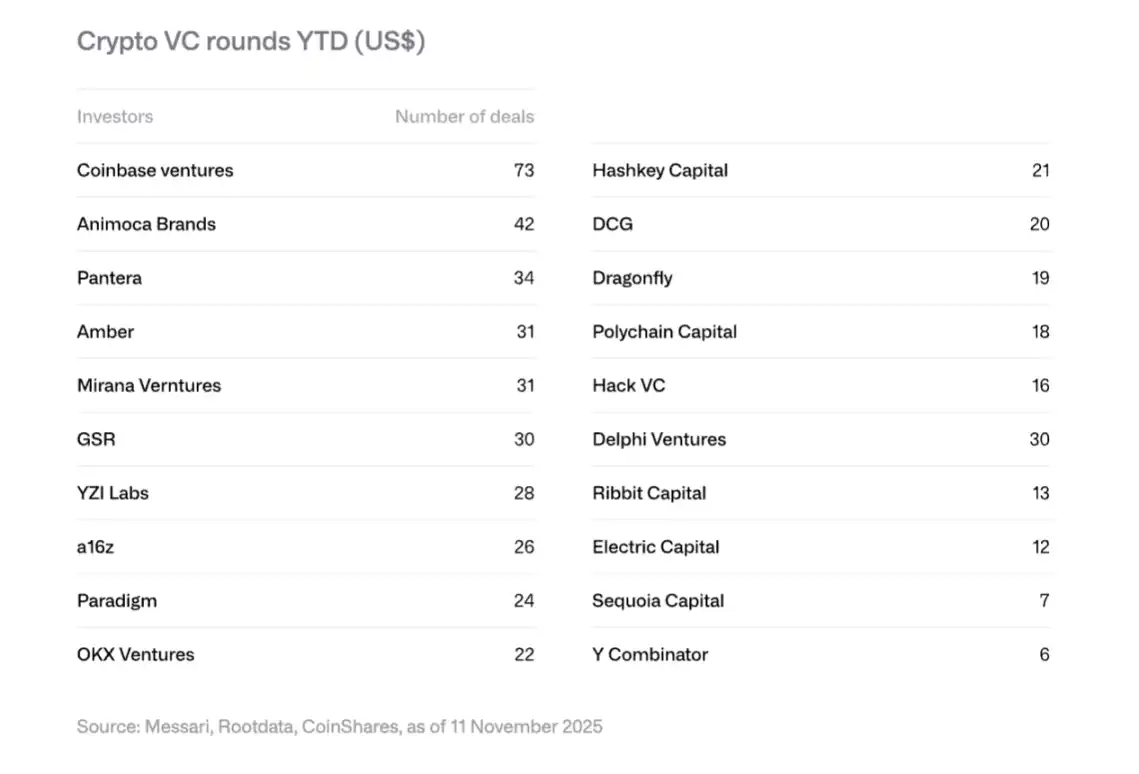

XI. Venture Capital Trends

2025 Recovery

Crypto VC funding reached $18.8 billion, exceeding the full year 2024 ($16.5 billion). Driven mainly by large deals: Polymarket's $2B strategic investment (from ICE), Stripe's Tempo raising $500M, Kalshi raising $300M.

Four 2026 Trends

RWA Tokenization: Securitize's SPAC, Agora's $50M Series A, etc., show institutional interest.

AI & Crypto Convergence: Applications like AI agents, natural language trading interfaces accelerating.

Retail Investment Platforms: Rise of platforms like Echo (acquired by Coinbase for $375M), Legion for decentralized angel investing.

Bitcoin Infrastructure: Layer-2 and Lightning Network related projects gaining attention.

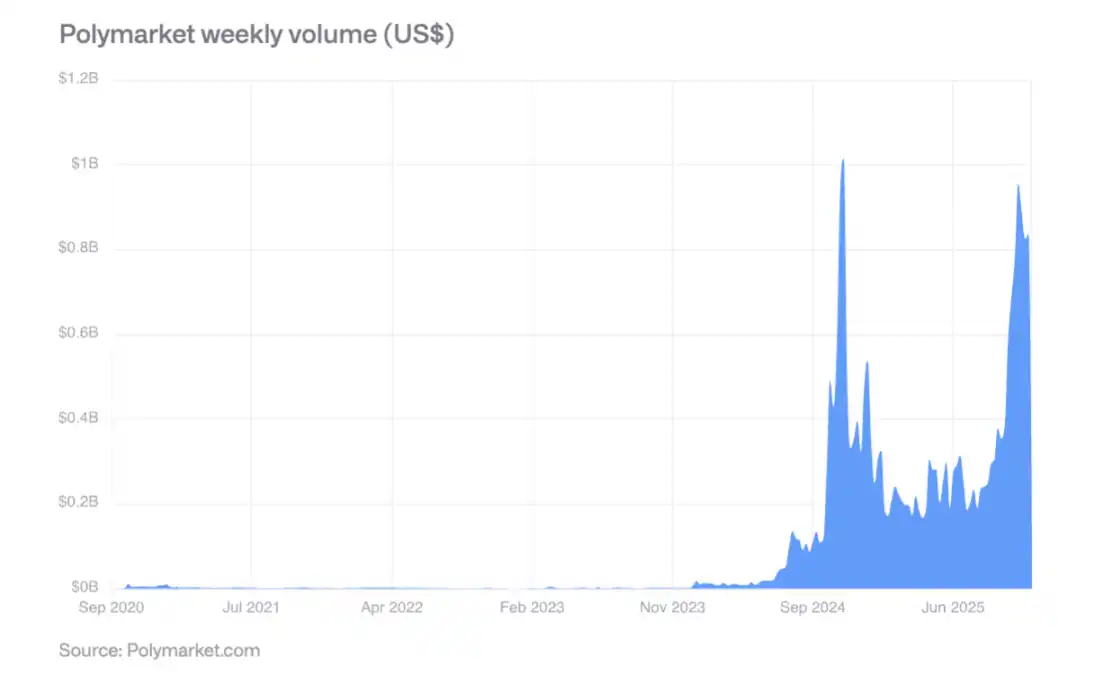

XII. The Rise of Prediction Markets

Polymarket saw weekly trading volumes exceed $800 million during the 2024 US election, with strong activity persisting post-election. Its predictive accuracy was validated: events with a 60% probability occurred ~60% of the time; events with an 80% probability occurred ~77-82% of the time.

In October 2025, ICE made a strategic investment of up to $2 billion in Polymarket, marking mainstream financial institution recognition. Weekly volumes could potentially break $2 billion in 2026.

XIII. Key Conclusions

Accelerating Maturation: Digital assets are shifting from speculation-driven to utility and cash flow-driven; tokens are increasingly resembling equity assets.

Rise of Hybrid Finance: The fusion of public blockchains with traditional financial systems is no longer theoretical but visible through strong growth in stablecoins, tokenized assets, and on-chain applications.

Increasing Regulatory Clarity: The US GENIUS Act, EU's MiCA, and Asia's prudential frameworks lay the foundation for institutional adoption.

Gradual Institutional Adoption: Although structural barriers are removed, actual adoption will take years; 2026 will be a year of incremental progress in the private sector.

Reshaped Competitive Landscape: Ethereum maintains dominance but faces challenges from high-performance chains like Solana; EVM compatibility is a key advantage.

Risks and Opportunities Coexist: High concentration of corporate Bitcoin holdings poses selling risks, but emerging areas like institutional tokenization, stablecoin adoption, and prediction markets offer huge growth potential.

Overall, 2026 will be a critical year for digital assets moving from the fringe to the mainstream, from speculation to utility, and from fragmentation to integration.