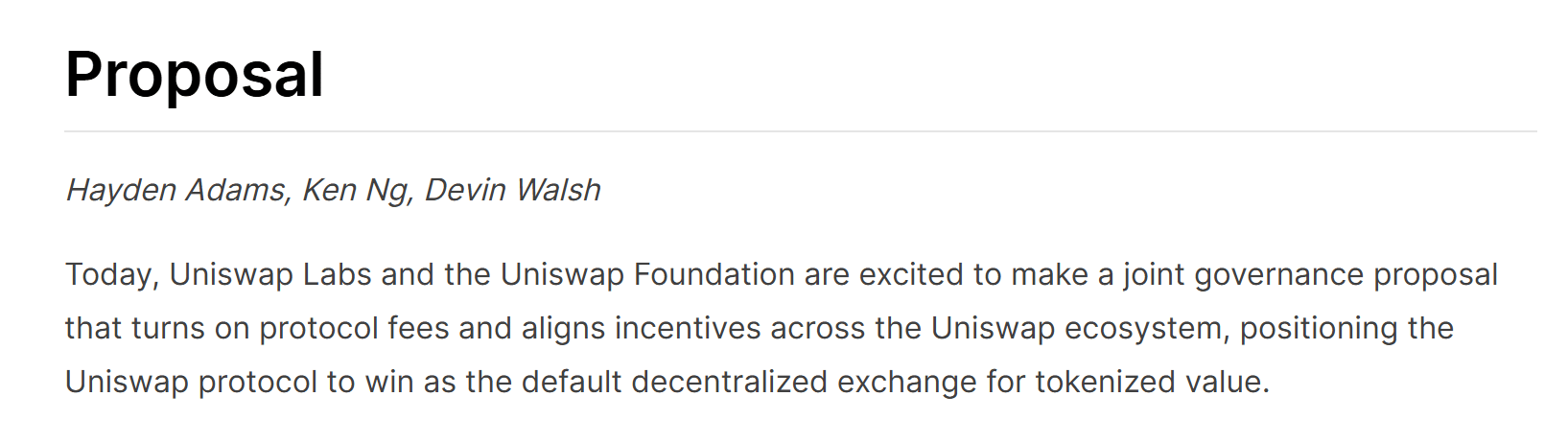

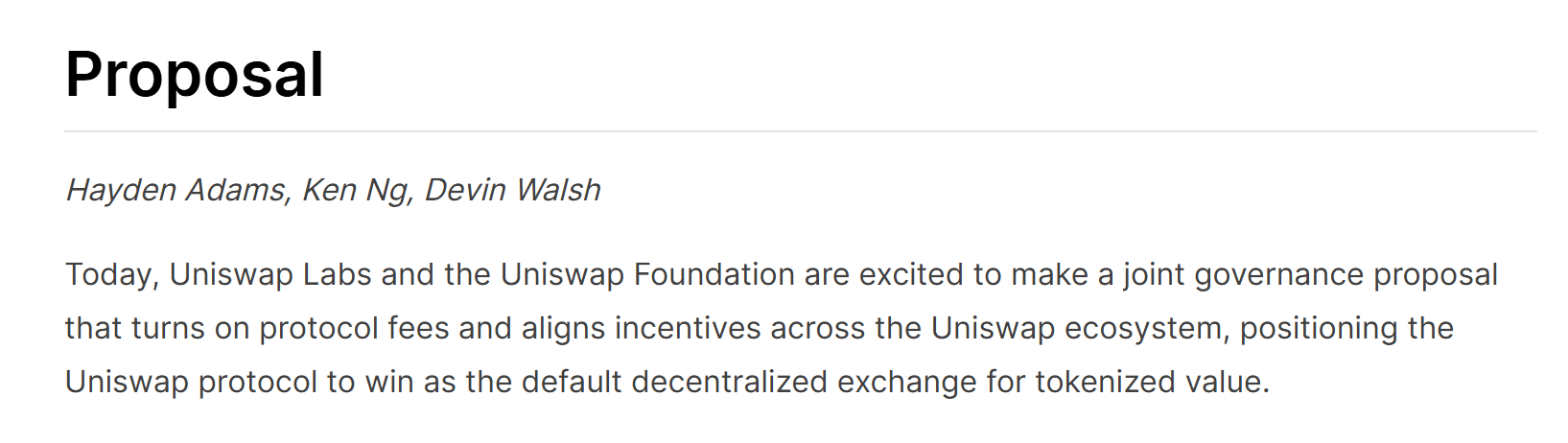

Competition among decentralized exchanges is increasingly forcing protocols to rethink the incentives that originally fueled DeFi’s rapid expansion. In fact, Uniswap [UNI] has become the latest to test that transition after proposing a reduction of up to 33% in V4 liquidity provider fee incentives.

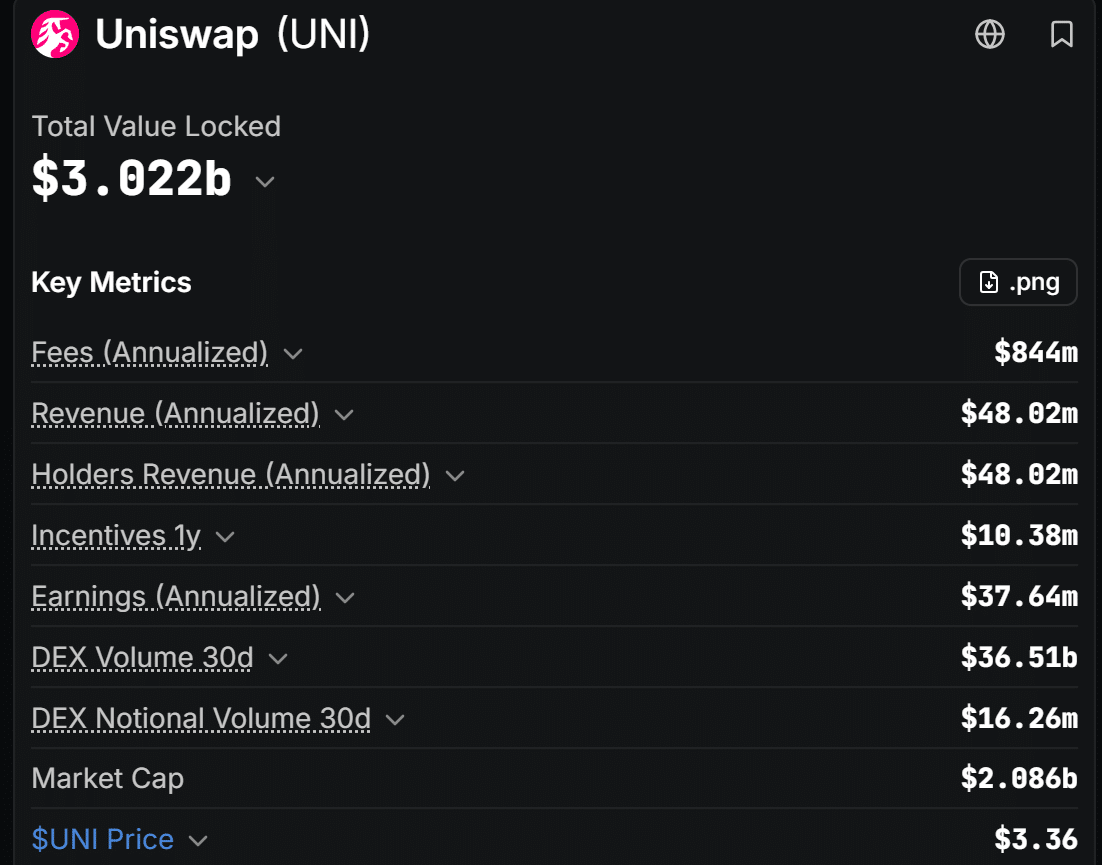

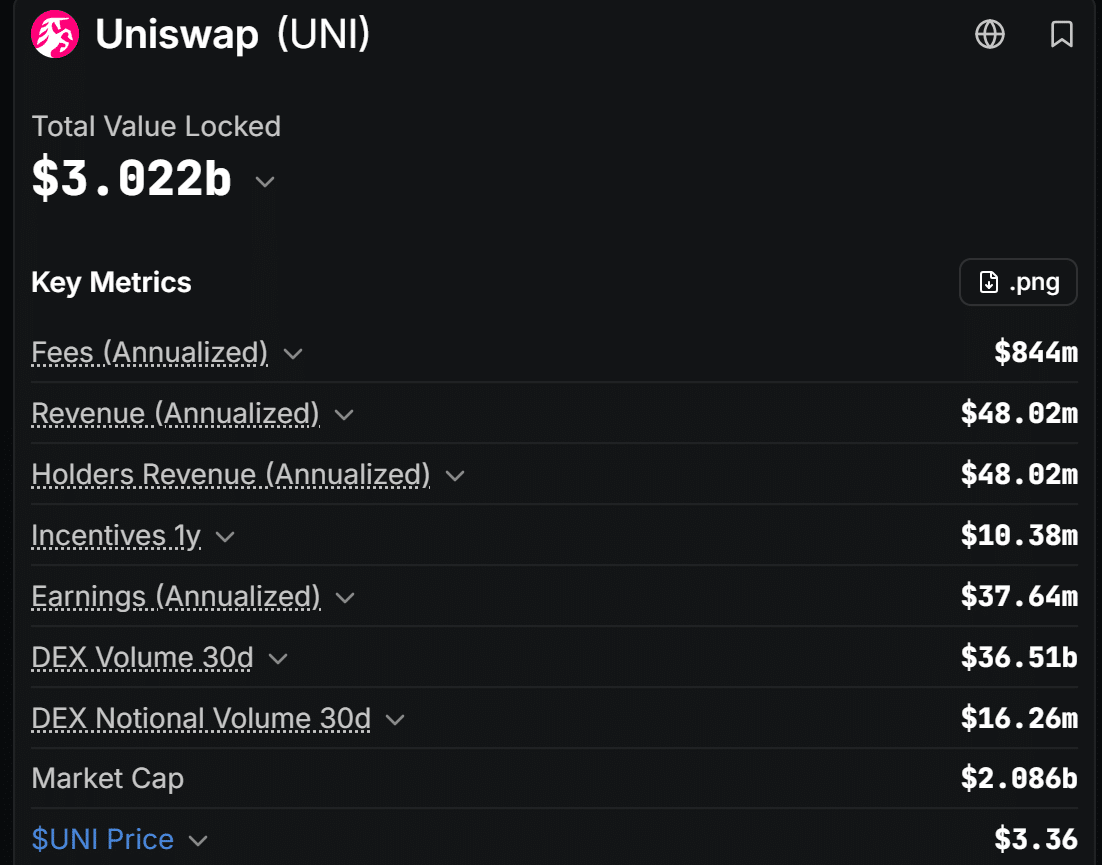

More importantly, Uniswap’s TVL stood at $3.02 billion while its monthly volume hovered near $36 billion at press time. This hinted at strong market leadership, despite intensifying competition from rival decentralized exchanges.

The proposal marks a clear departure from previous models. The V3 model used much higher percentages of each trade to incentivize early liquidity providers to quickly capitalize on its platform.

Instead, the protocol believes that a lower cost of trading, tighter spreads, and better capital usage will result in a sufficient increase in volume to offset reduced LP returns.

That calculation carries meaningful risk. This, because liquidity providers can easily move capital to competing protocols offering stronger yields. If trading activity rises fast enough, the new model could strengthen Uniswap’s long-term competitiveness.

And yet, weakening LP participation may pressure liquidity depth and reshape incentive structures across the wider DeFi ecosystem.

Uniswap strengthens stablecoin liquidity

That strategy is already taking shape through Uniswap’s integration of Sky’s LitePSM.

Rather than relying solely on liquidity provider rewards, the peg stability module enables zero-slippage routing between USDS, DAI, and USDC. The integration deepens liquidity, reduces execution costs, and allows larger trades to settle with minimal price impact.

Also, it enhances Sky’s FX Layer by converting parity-based stablecoin routing into operational infrastructure. While these enhancements improve competitive positioning for Uniswap, infrastructure alone may not be sufficient to generate greater trading volumes.

However, lasting success will ultimately depend on whether lower execution friction attracts enough users and volume to offset reduced liquidity provider incentives.

Still, the real test for Uniswap now lies in market adoption rather than protocol design. Success will depend on whether stronger execution and higher trading volumes offset lower liquidity provider rewards.

If traders embrace the model, Uniswap could reinforce its leadership. Otherwise, rival DEXs may attract liquidity through more competitive incentives instead.

Final Summary

- Uniswap [UNI] has proposed prioritizing execution over higher liquidity incentives.

- Uniswap’s success now depends on trading volume, not liquidity incentives alone.