Author: Jae, PANews

In 2025, the DeFi (Decentralized Finance) market embarked on a thrilling roller coaster ride. At the beginning of the year, fueled by optimism from Layer 2 performance explosions and institutional capital inflows, the TVL (Total Value Locked) skyrocketed from $182.3 billion to a historic peak of $277.6 billion, painting a seemingly within-reach blueprint for a trillion-dollar ecosystem.

However, a sudden flash crash in Q4, the 10/11 event, poured cold water on this fervor, causing the TVL to shrink sharply to $189.35 billion, wiping out the annual gains to a negligible 3.86%. This剧烈 volatility laid bare the true texture beneath DeFi's glamorous narrative: on one side, the deep evolution of sectors like staking, lending, and RWA; on the other, the fragility built on leverage accumulation and the hidden pain of governance fragmentation.

This was a trial by ice and fire. The market witnessed Lido's松动 (loosening) sovereignty in the staking领域 (domain), Aave's difficult跋涉 (trek) through internal governance wars, Hyperliquid facing fierce challenges from newcomers on the Perp DEX throne, and stablecoins wavering between yield chasing and regulatory frameworks. The DeFi of 2025 is no longer just an experimental field for crypto natives; it is stumbling yet steadfastly striding into the deep waters of global financial infrastructure.

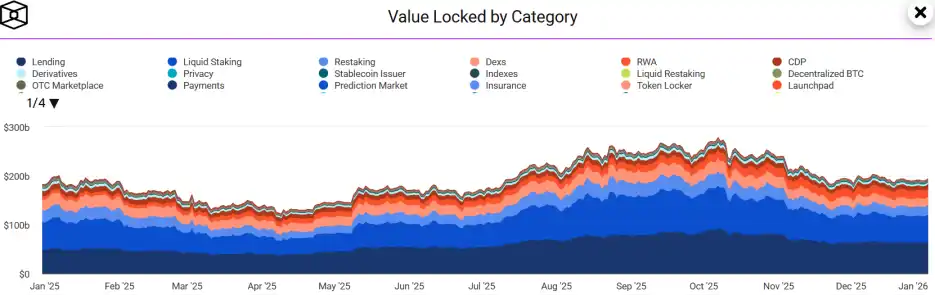

DeFi Market TVL Rises Then Falls, Monopolistic Structure Continues to Solidify

The curve of the DeFi market size in 2025 drew a massive inverted V.

Starting from $182.3 billion at the beginning of the year, the TVL, accompanied by market frenzy and ecological explosion mid-year, once touched a vertex of $277.62 billion. However, the Q4 flash crash brought everything to an abrupt halt, with the year-end figure falling back to $189.35 billion, almost returning to the starting point.

But beneath the surface, the structure of capital underwent profound changes. The RWA (Real World Assets) sector emerged surprisingly, with its TVL surpassing traditional DEXes to become the fifth largest DeFi category. The capillaries of on-chain finance are extending deeper into the real economy.

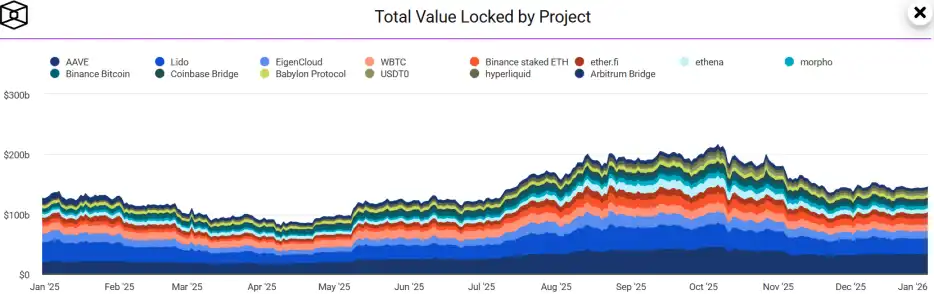

Monopolization became even more solidified. The top 14 protocols, including Aave, Lido, and EigenCloud, accounted for 75.64% of the market share.

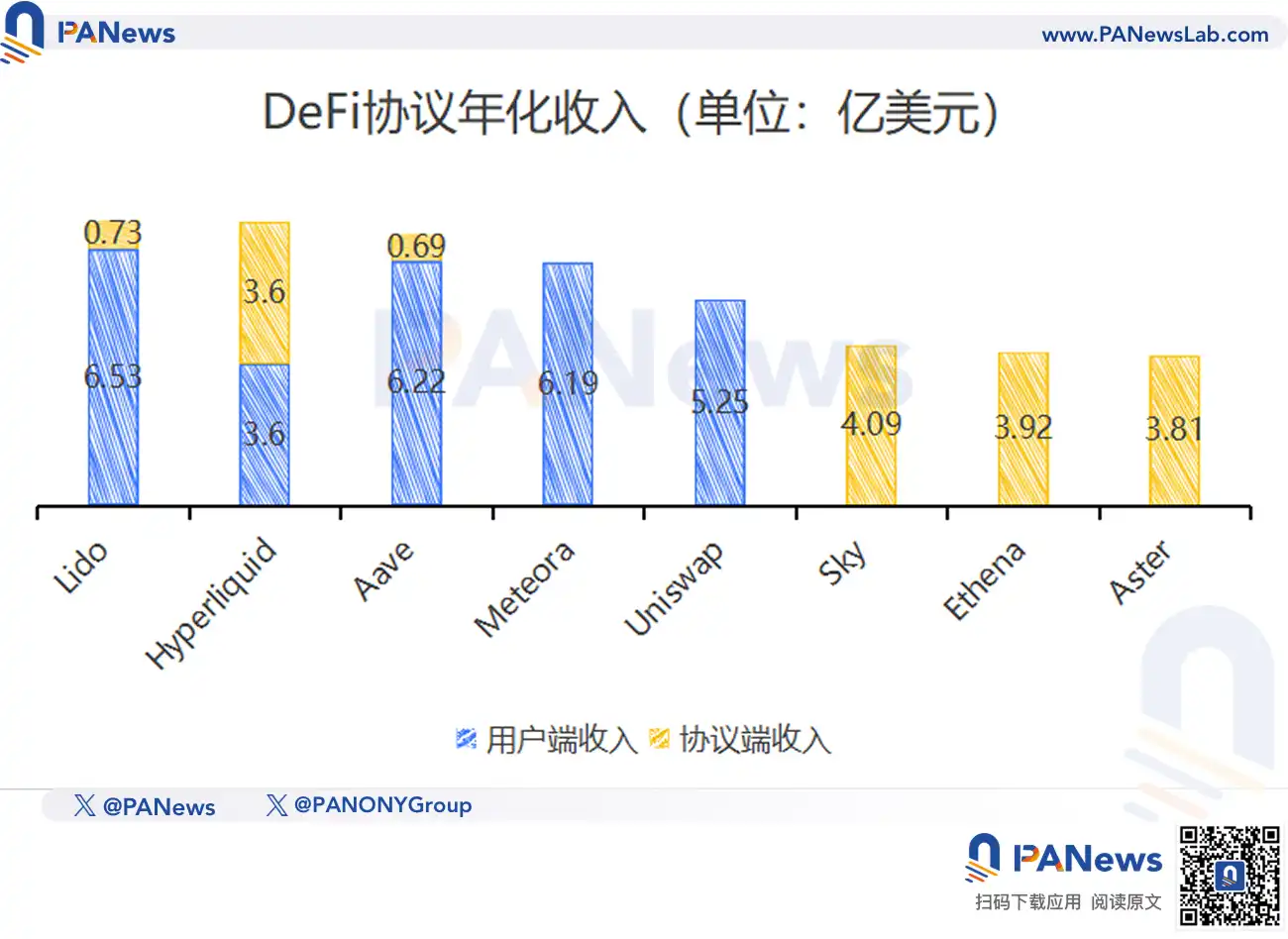

Meanwhile, the profitability of leading protocols soared, with the annual revenue of the top ten protocols doubling from $2.51 billion to $5.02 billion. Capital in the DeFi market is increasingly concentrating towards a few core components.

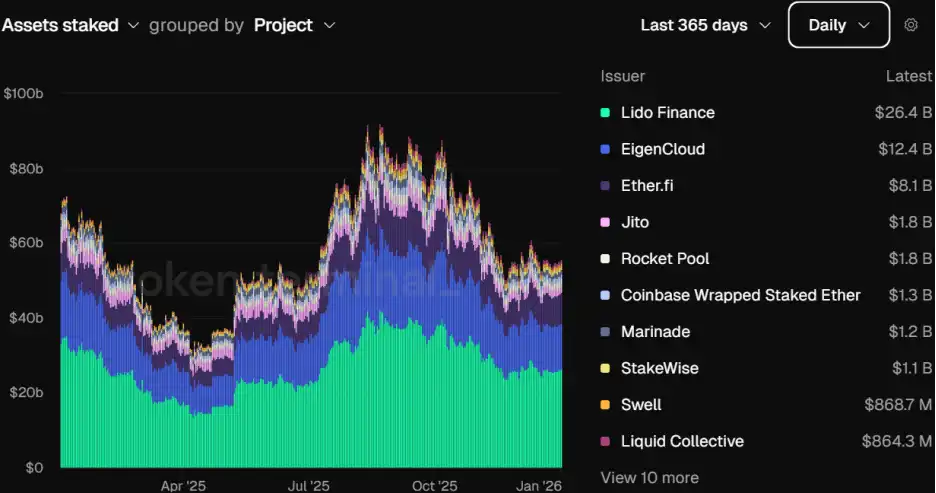

Staking Protocols Shift from Money Printers Back to Security Foundation, Ethereum Ecosystem Still Dominates

Staking was once DeFi's simplest and most brutal yield story. In 2025, this track experienced a value回归 (return) of de-bubbling; staking protocols are evolving from a单纯的 (mere) DeFi yield tool into the economic security engine for public blockchain networks.

The staking sector's TVL fell from a mid-year peak of $92.1 billion to $55.2 billion.

With increasing security demands in the Ethereum ecosystem, over 35 million ETH (about 30% of the total supply) was locked in the validation network. But the dominance of leading staking protocol Lido declined from over 30% at its peak to 24%. This is not a decline, but rather a sign of Ethereum staking maturing, decentralizing, and offering more diverse choices.

The most important change in the staking sector lies in compliant implementation. In May 2025, formal guidance provided by the U.S. Securities and Exchange Commission (SEC) clarified that staking activities do not constitute securities issuance, which will remove obstacles for custodial institutions and pension funds to allocate LSTs (Liquid Staking Tokens) on a large scale. Today, LSTs are no longer just tools for earning staking rewards; they are also penetrating into application scenarios like lending and derivatives as highly liquid, high-quality collateral.

Restaking protocols achieved a leap from concept to a market worth tens of billions of dollars in 2025, their essence being an exponential improvement in capital efficiency. EigenLayer's transformation into EigenCloud saw its TVL break through $22 billion, making it the second-largest staking protocol. EigenCloud allows already staked ETH to be reused, providing security for multiple Active Validation Services (AVS) simultaneously, thus creating multi-layered yields for holders.

Ether.fi achieved a TVL of over $8.5 billion and cumulative protocol revenue exceeding $73 million, consolidating its position as a top-tier liquid restaking protocol.

Restaking protocols not only changed the staking logic of ETH but also pioneered a new "shared security" business model. However, the staking sector experienced a significant capital rotation in 2025.

As airdrop expectations materialized and early incentives phased out, capital shifted from protocols lacking real utility towards leading platforms with actual service revenue, marking that the staking sector has completed its transformation from speculation-driven to business-driven.

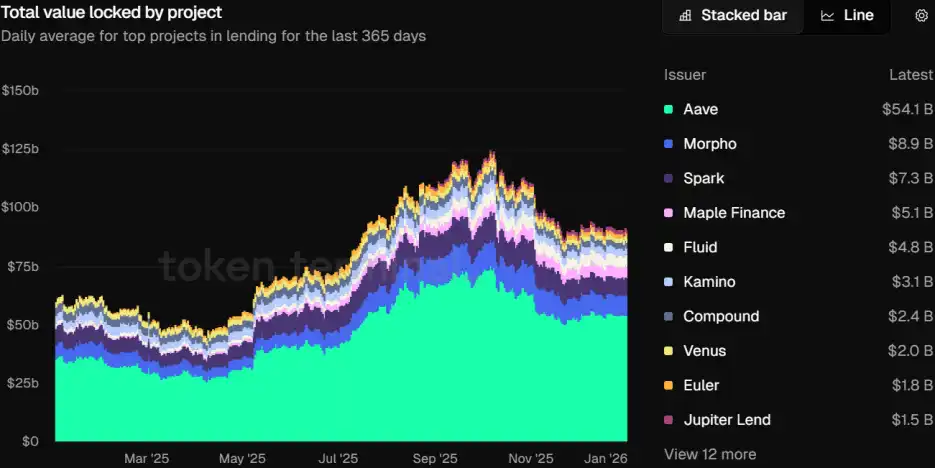

Lending Sector Scales New Heights, Enters Professional Layering Stage

Lending is the cornerstone of DeFi. The sector's TVL hit a historic high of $125 billion, stabilizing at $91.6 billion by year-end.

Aave firmly holds the top spot with over 50% market share. Even amidst a "sovereignty争夺" (struggle) governance civil war at year-end, its TVL remained above $54 billion, demonstrating the deep底蕴 (reserves) of the leader.

Related reading: Token Price Drops, Whales Sell Off and Exit, Looking at DeFi Governance Dilemma from the Aave Power Struggle

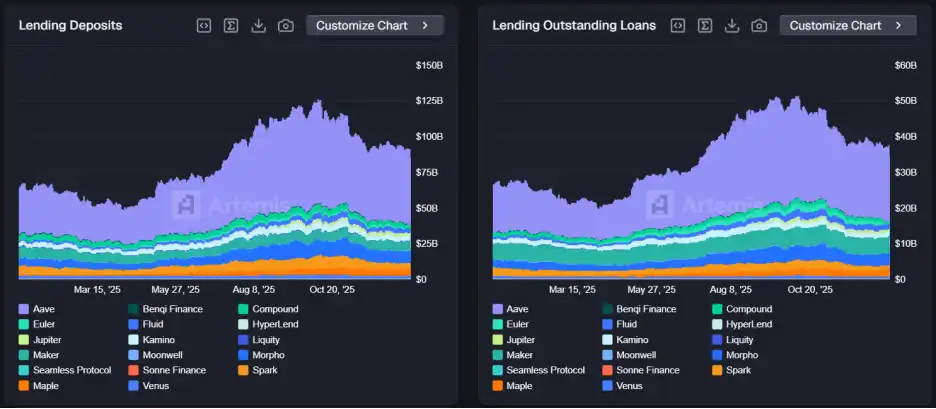

In terms of on-chain lending scale, deposit size increased from $64.1 billion to $90.9 billion, a year-on-year growth of about 42%; outstanding loan size rose from $26.6 billion to $37.6 billion, a year-on-year growth of about 41%.

Notably, the peak deposit size during the year was $126.1 billion, and the peak outstanding loan size was $51.5 billion, both setting new historical records.

The capital utilization rate remained above 40% throughout the year, at a relatively可观 (considerable) level.

A silent migration is happening within the lending sector: market preference is shifting massively from CDP (Collateralized Debt Position) protocols represented by MakerDAO towards money market protocols represented by Aave. Research released by Galaxy Research shows a seesaw dynamic, with money market protocols capturing over 80% of the on-chain credit scale, while CDP's share has shrunk to below 20%. This reflects that users prefer accessing funds in lending pools with high liquidity depth rather than establishing抵押债仓 (collateralized debt positions) with relatively lower capital efficiency.

Simultaneously, modular protocols like Morpho and Euler V2 meet the customized needs of professional users by creating risk-isolated lending vaults. The lending sector is saying goodbye to the 'big pot meal' and entering a refined, layered professional era.

However, uncollateralized lending, which pursues higher capital efficiency, remained an unconquered challenge in 2025, although experiments based on user identity and credit scores like 3Jane are underway.

Related reading: Paradigm Leads Investment Bet, How Will 3Jane Unlock the Trillion-Dollar DeFi Uncollateralized Credit Market?

Yield Protocols Become DeFi Infrastructure, Competitive Landscape Gradually Diversifies

2025 was the year the yield sector leaped from a niche market to DeFi infrastructure. Its TVL rose from $8.1 billion to $9.1 billion, a year-on-year increase of 12.5%, with a yearly high of around $18.8 billion.

In traditional finance, the fixed income market far surpasses the stock market. The maturation of protocols like Pendle finally filled this critical piece of the puzzle for the DeFi market: interest rate trading.

Pendle establishes a predictable interest rate discovery mechanism on-chain by splitting assets into PT (Principal Token) and YT (Yield Token). The protocol not only achieved an order-of-magnitude leap in asset scale but also filled the gap in the on-chain fixed income curve with its interest rate products.

In 2025, Pendle's TVL decreased from $4.3 billion to $3.7 billion, a year-on-year decline of about 13%. However, its cumulative revenue steadily increased from $17.99 million to $61.56 million, a year-on-year growth of 242%, demonstrating the resilience of the protocol's fundamentals. Even during the market downturn, Pendle maintained stable revenue generation capability.

The protocol's new product, Boros, further extended its business reach into the funding rate trading market, providing a利器 (sharp tool) for derivatives players to hedge holding costs, seen as the protocol's second growth curve.

Related reading: Pendle's Strategic Expansion: Boros Emerges, Funding Rate Trading Paradigm Innovation

The competitive landscape of the yield sector shows characteristics of evolving from a single hegemon to diversification. Although Pendle still holds the major market share, new entrants like Spark Savings are also expanding rapidly.

In the long run, yield protocols may become an important link connecting DeFi and institutional capital.

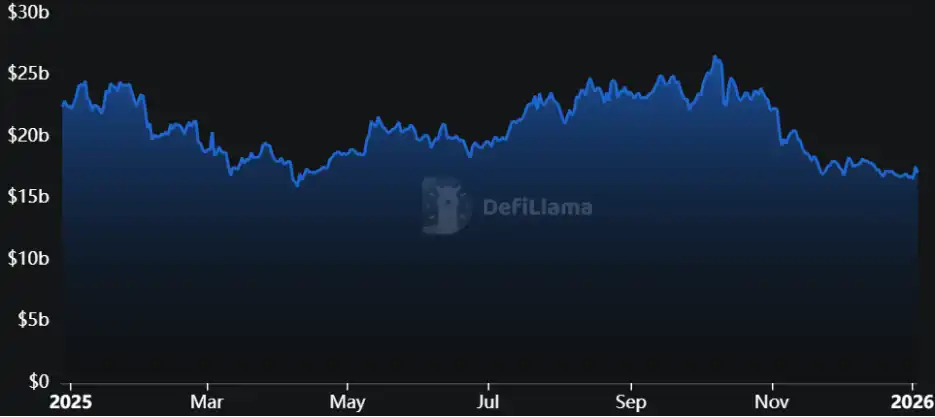

DEX User Stickiness Increases Significantly, Participating Players Gradually Diversify

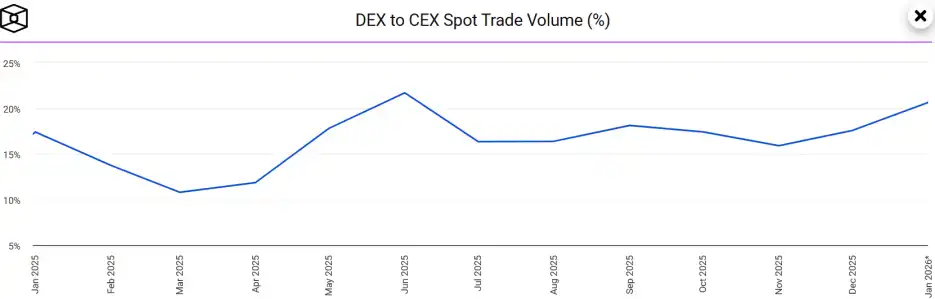

In 2025, DEXes continued to accelerate their catch-up with CEXes (Centralized Exchanges) in terms of user experience and liquidity efficiency. The sector's TVL decreased from $22.3 billion to $16.8 billion, a year-on-year decline of about 25%, with a yearly high of $26.6 billion.

Driven by Memecoin speculation frenzy and ecosystem booms on Solana, Base, and others, the share of DEXes in cryptocurrency spot trading reached a staggering 21.71% in June.

In 2025, user stickiness on DEXes increased significantly. For eight consecutive months, the trading share of DEXes versus CEXes remained above 15%, breaking the pattern of only briefly spiking during bull market peaks in previous years.

Artemis data shows that the spot trading volume on Solana DEXes reached a whopping $1.7 trillion in 2025, accounting for 11.92% of the global spot market total, surpassing Bybit, Coinbase, and Bitget, second only to Binance. Since 2022, Solana's on-chain share has jumped from 1% to 12%, while Binance's market share has dropped from 80% to 55%, indicating that spot trading activity is gradually migrating on-chain.

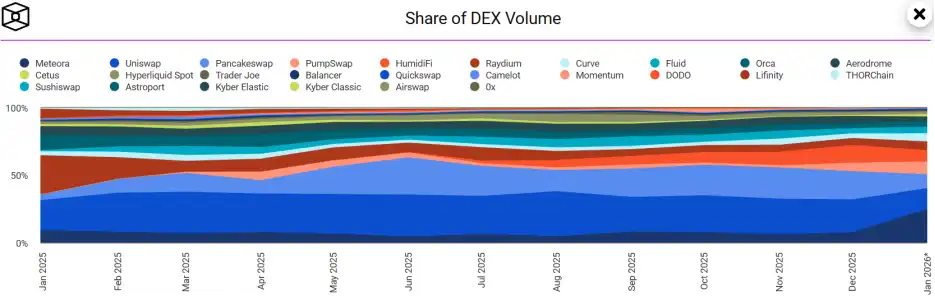

In terms of market share, Uniswap continues to maintain its leading position in the sector, especially in decentralized governance and value capture.

In September, the Uniswap Foundation registered Uniswap Governance as a Decentralized Unincorporated Nonprofit Association (DUNA) in Wyoming, serving as the legal structure for protocol governance, and named the entity "DUNI". This move can provide Uniswap with a compliant governance facade while paving the way for activating the protocol fee mechanism.

Related reading: Uniswap's Compliant Breakthrough: How DUNA Paves the Way for Fee Switch and Token Empowerment?

In December, Uniswap passed the UNIfication governance proposal, officially turning on the protocol fee switch and burning 100 million UNI tokens.

Related reading: Uniswap Heavyweight Proposal Launched: Fee Switch and Burn Mechanism Activated, Competitors Call it a "Strategic Mistake"

Although Uniswap remains the sector leader, the technical route of DEXes has seen a structural change衍生 (derivative) from traditional AMM (Automated Market Maker) to Prop AMM (Proprietary Automated Market Maker).

It is worth mentioning that the low-slippage dark pool model of the emerging Solana DEX HumidiFi is reshaping trader behavior patterns. HumidiFi contributed 36%-50% of Solana's network spot trading volume, with its daily SOL/USD trading volume多次 (multiple times) surpassing CEX giants like Binance. Although HumidiFi's ultra-low fee of 0.001% sparked widespread debate about its sustainability, the protocol's excellent performance in anti-MEV, front-running prevention, and private execution has made it the preferred DEX for professional institutions and whale大户 (large holders).

Furthermore, cross-border giants like Opensea, seeking a second growth curve, have also launched spot trading businesses.

Related reading: Token Trading Becomes OpenSea's New Growth Engine, Can It Successfully Transform Under Token Issuance Expectations?

The diversification of players has further promoted the overall prosperity of the DEX sector. cryptodiffer data shows that in 2025, among DeFi protocols ranked by fees, Meteora, Jupiter, and Uniswap were the top three, all exceeding $1 billion.

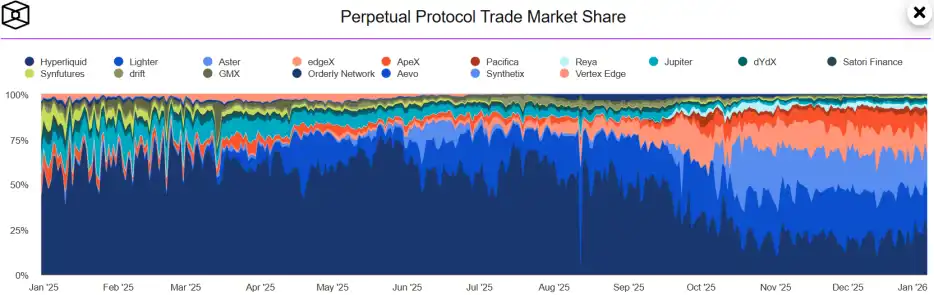

Perp DEX Challenges CEX, From One Dominant Player to Warlords Contending

If 2024 was the experimental period for Perp DEX, then 2025 was its爆发期 (outbreak period), beginning to take shape to challenge CEX. Relying on customized Layer 1 and high-performance ZK-Rollups, the execution speed and trading depth of on-chain derivatives achieved qualitative breakthroughs.

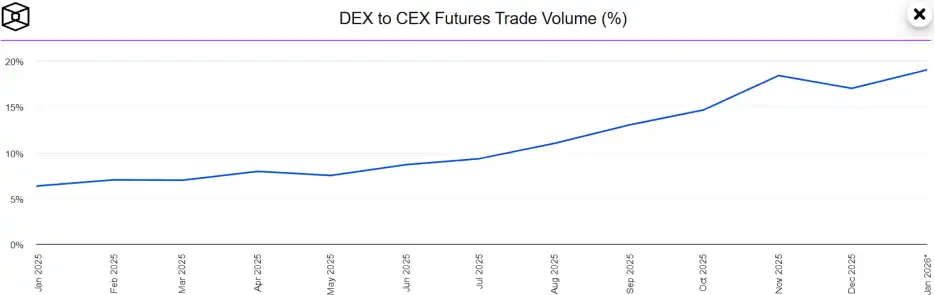

In 2025, the Perp DEX sector's open interest exceeded $16 billion, and its trading volume share relative to CEX jumped from 6.34% to 17%.

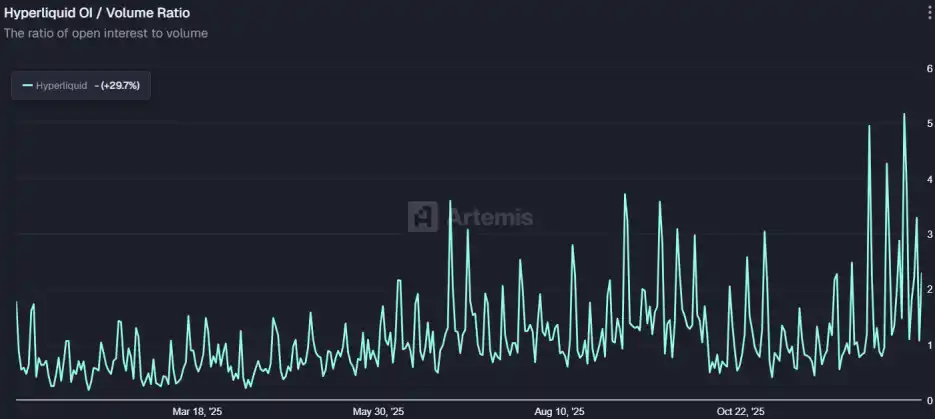

Hyperliquid is the vanguard of the Perp DEX sector. Supporting 200,000 TPS and sub-second settlement, its performance is already on par with mainstream CEXes. Its annual trading volume exploded from $617.5 billion to $3.55 trillion. The protocol's OI/Vol (Open Interest/Volume) ratio长期 (long-term) remained at a high level around 2, indicating that its trades are mostly genuine hedging and trend positions, rather than mere volume farming.

Hyperliquid's success lies not only in technology but also in its "No VC, Community First" tokenomics model, which has won huge trust premiums in the current market environment普遍 (generally) averse to VC tokens.

However, Hyperliquid's market share has been halved from 43% to 22%. This shows that the competitive landscape of the Perp DEX sector is evolving from Hyperliquid's dominance to a situation of群雄并起 (multiple heroes rising together).

Related reading: Perp DEX New and Old Contest: Hyperliquid Faces Hundred-Billion Unlock Pressure, New Platforms Grab Traffic with Incentives

Challenges mainly come from two strong competitors: one is Aster, backed by the Binance ecosystem and skilled in social裂变 (fission/viral growth); the other is Lighter, using ZK-proof technology as its spear and pioneering a zero-fee model. Together, they snatched away half of the market share in 2025, quickly diverting retail funds.

Related reading: Aster's 'Trojan Horse': How to Sneak Attack via BNB Chain, Aiming for the Hyperliquid Throne?

Airdropping $675 Million but Sparking Distribution Controversy, Lighter Faces User Retention Challenge Post-Token Launch

Hyperliquid responded with institutional-grade features like "Portfolio Margin". The Perp DEX war is no longer just about who is faster; it's a comprehensive对决 (showdown) of technical routes, traffic strategies, and capital efficiency.

Related reading: Hyperliquid to Launch Portfolio Margin, Killer Move or Dangerous Weapon?

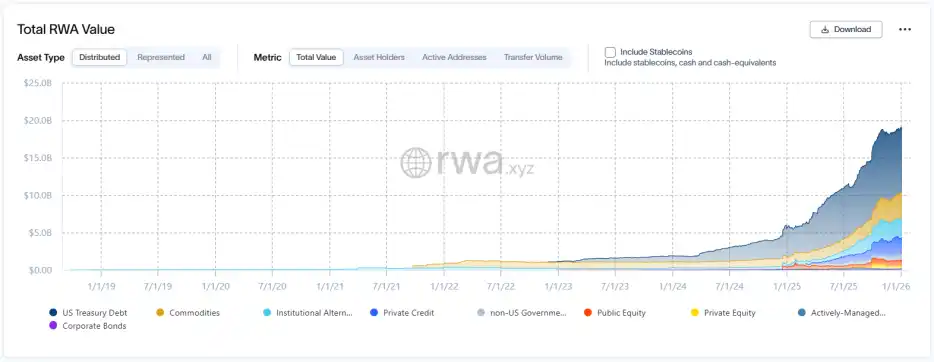

RWA Deeply Penetrates On-Chain Market, Achieves Scalable Expansion

In 2025, the wall between the on-chain market and real-world assets was pushed down faster; it was the year RWA achieved scale. The market capitalization of tokenized assets (excluding stablecoins) soared from $5.6 billion to over $20 billion.

Against the backdrop of the full launch of the RWA narrative and the accelerated onboarding of global assets, traditional giants like the Swiss precious metals group MKS PAMP also successively重启 (restarted) or explored tokenized products, marking the deep convergence of on-chain finance and physical assets.

Related reading: Swiss Gold Giant MKS PAMP 'Returns', Re-enters Gold Tokenization Track

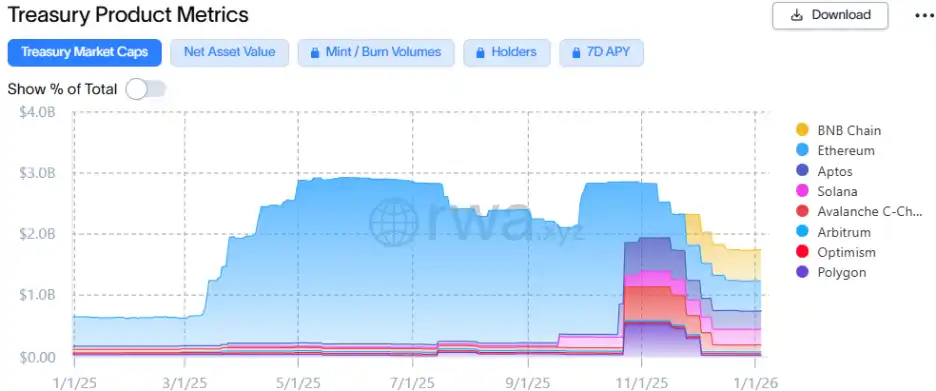

Tokenized U.S. Treasuries are becoming a conveyor belt connecting traditional risk-free yields and on-chain strategies. BlackRock's BUIDL fund achieved textbook-like expansion in 2025, growing rapidly from $650 million to $1.75 billion, further consolidating its position as a leader among tokenized U.S. Treasury products. BlackRock brought not only capital but also brand endorsement, allowing BUIDL tokens to serve as underlying collateral in protocols like Aave and Euler, and through cross-chain distribution, connect U.S. Treasury yields to the DeFi market.

RWA may be becoming a counter-cyclical tool. When the crypto market experienced a pullback in March 2025 due to tariff policies, the tokenized U.S. Treasury market反而 (instead) added $1 billion in market capitalization in one month, an increase of about 33%.

The same situation occurred again in November 2025. Driven by macro factors such as rising precious metal prices and geopolitical turmoil, the market capitalization of tokenized gold and silver products突破 (broke through) $3.5 billion, reflecting the demand and trend for capital seeking safe havens on-chain.

Related reading: After Gold and Silver Go Crazy, On-Chain Sparks a Boom in Commodity Trading

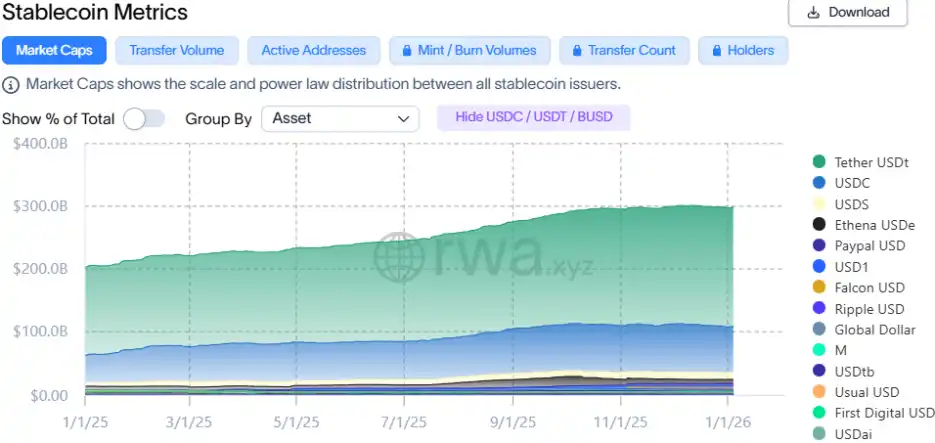

Stablecoin Sector Sees Landing, Welcomes Dual Evolution of Scale and Structure

The stablecoin sector, meanwhile, tore forward amidst compliance and innovation. In the 2025 DeFi landscape, stablecoins evolved into the monetary base layer connecting payments, trading, and collateral. The maturity of this sector is mainly reflected in the implementation of compliance and model innovation.

2025 was a turning point where global stablecoin regulatory frameworks moved from theory to practice. With the advancement of the U.S. GENIUS Act, a federal-level stablecoin framework began to take shape, allowing traditional banks like JPMorgan Chase and Citigroup to participate more deeply in stablecoin issuance and reserve management.

Related reading: U.S. Banking Industry Jointly Opposes the 'GENIUS Act', Stablecoin Shockwaves Shake Traditional Giants

The full生效 (effectiveness) of Europe's Markets in Crypto-Assets Regulation (MiCA)强制 (forced) Crypto Asset Service Providers (CASPs) to switch to compliant stablecoins, leading to a significant liquidity rotation in the European market.

Related reading: USDT Exits, EURC Fills the Gap, Euro Stablecoin Surges Over 170% Against the Trend

Regulatory transparency directly translated into an entry ticket for institutions. Stripe acquired Bridge and integrated the dollar stablecoin USDB; PayPal issued PYUSD; Klarna launched KlarnaUSD. A DeFiLlama report pointed out that the settlement volume of regulated stablecoins exceeded $50 trillion in 2025, and their monthly processing volume surpassed that of Visa and PayPal in multiple months, proving the superiority of blockchain as a payment infrastructure.

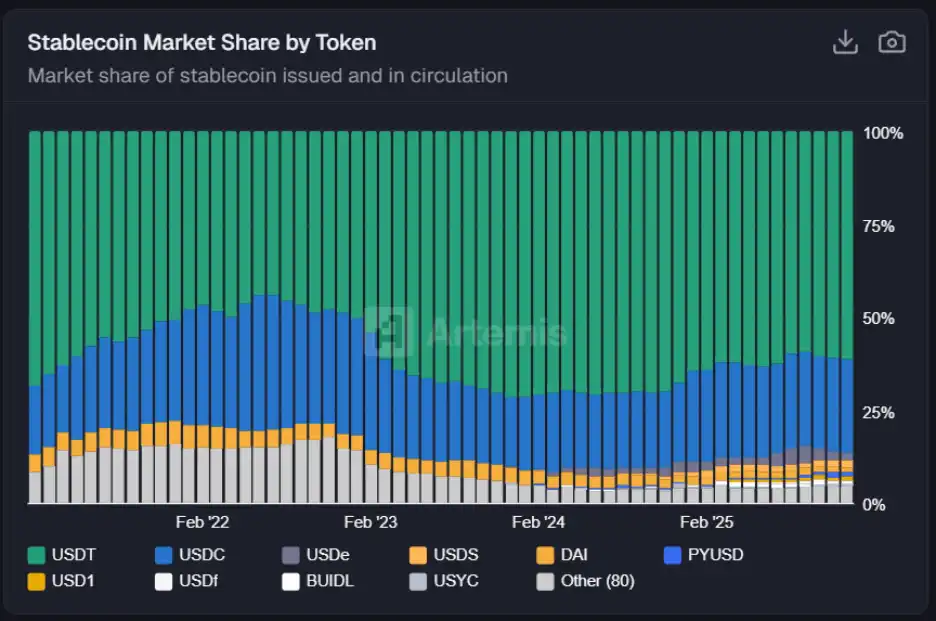

As the lifeblood of DeFi, stablecoins welcomed a dual evolution of scale and structure in 2025. The total market capitalization once climbed to $3 trillion, while the competitive landscape showed "internal innovation under bipolar monopoly".

USDT still maintains an absolute lead with over 60% share, while USDC ranks second凭借 (relying on) transparency and compliance.

The升温 (heating up) of interest rate cut expectations催生 (spawned) a strong demand for on-chain yield-bearing assets, and user preference for yield-bearing stablecoins一度 (once) surpassed traditional payment-focused stablecoins. A DeFiLlama report noted that the scale of yield-bearing stablecoins surged from $9.5 billion to over $20 billion in 2025, a year-on-year increase of over 110%.

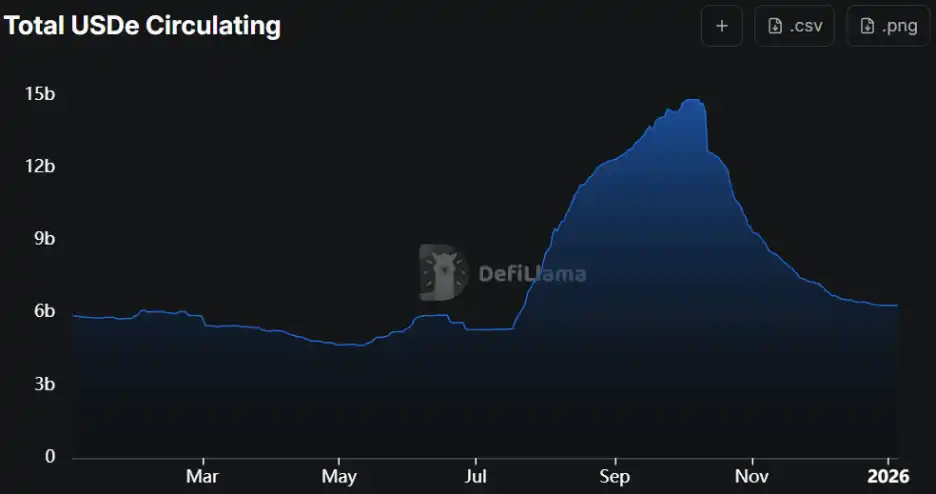

The synthetic dollar USDe, issued by Ethena, emerged surprisingly in 2025. The protocol does not rely on fiat reserves but achieves delta neutrality by establishing an equal and opposite perpetual contract short position on yield-bearing asset positions like ETH.

Benefiting from high-leverage循环 (recycling) leverage on Aave and Pendle, the supply of USDe approached 15 billion. However, the flash crash on October 11 caused USDe to脱锚 (depeg) to $0.65 on the Binance spot market at one point. These aftershocks caused USDe's TVL to plummet to $6.3 billion, a 58% shrinkage from its historical high.

Related reading: Crypto Flash Crash Day Revelation: The Triple Contagion Chain of the Market Crash, How Can the Industry Rebuild a More Robust Foundation?

Subsequently, Ethena launched a white-label platform attempting to create a second growth engine.

Related reading: Ethena After the Depeg Crisis: TVL Halved, Ecosystem Setback, How to Open a Second Growth Curve?

Misfortune never comes singly. In November, a崩盘危机 (collapse crisis) occurred where Stream and Elixir's externally managed funds blew up, causing their issued yield-bearing stablecoins xSUD and deUSD to双双归零 (both go to zero). This event dealt a heavy blow to the market and also sounded an alarm: even seemingly safe stablecoins must be wary of their underlying complex strategy issues, and systemic risk has migrated from the code layer to the counterparty layer.

Related reading: DeFi Reflection: Four Stablecoins Go to Zero in a Week, Resolutely Say NO to 'Black Box Operations'

In contrast, MakerDAO grew steadily after rebranding to Sky. Although the expansion of its protocol stablecoin USDS once encountered bottlenecks, by integrating RWA assets and directly incorporating Treasury yields, it provided a stable and sustainable native yield rate, pushing the USDS market capitalization past USDe to become third in the sector.

The evolution of these seven细分 (segmented) markets means the 2025 DeFi market is no longer an isolated experiment. It demonstrated powerful financial engineering capabilities, turning staking, lending, yields, and even government bonds into programmable Lego bricks. But at the same time, it did not摆脱 (escape) human greed: governance conflicts, leverage collapses, black box operations... The "10/11 Flash Crash" was like a mirror, reflecting the cracks behind the prosperity.

However, the暴跌 (plunge) did not lead to systemic collapse. Leading protocols showed resilience in the storm, and real application scenarios are沉淀 (precipitating/settling). And this, perhaps, is the price of the DeFi market's coming-of-age ceremony.