Author: Ma He, Foresight News

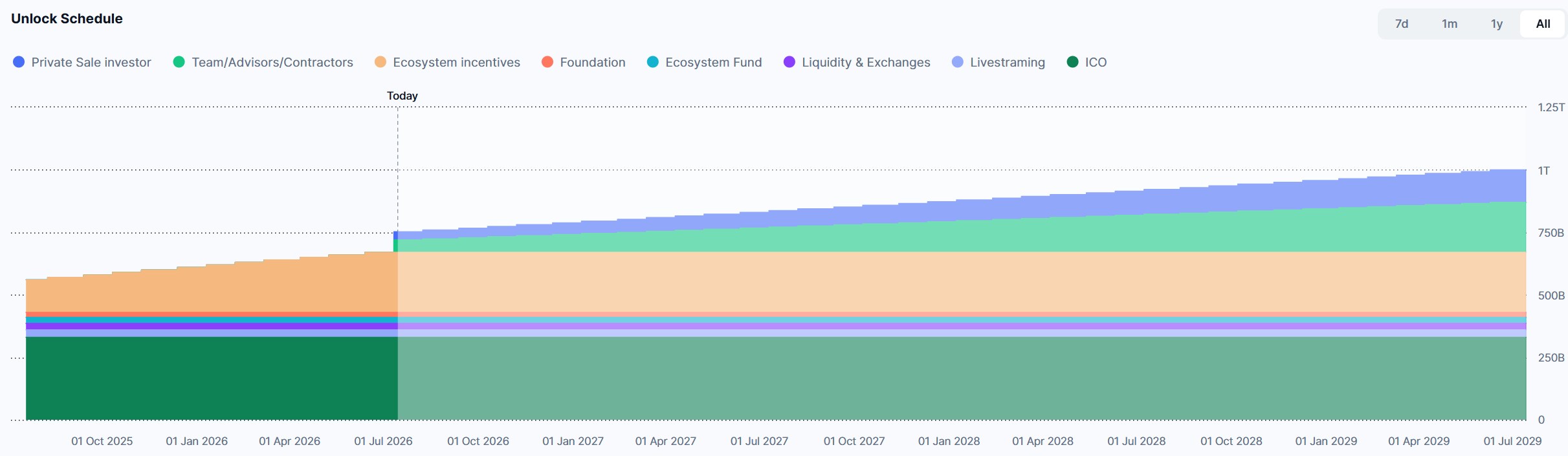

On July 14, 2026, the native token PUMP of Pump.fun experienced its first large cliff unlock after TGE. According to cross-verification from Tokenomist, on-chain monitoring, and multiple data platforms, the theoretical maximum number of tokens unlocked on that day was 82.5 billion, accounting for 8.25% of the total supply (1 trillion tokens), valued at approximately $131.35 million (calculated at the price of about $0.00159 at the time), equivalent to about 20.23% of the circulating supply before the unlock.

This was the first unlock for two major allocation categories: team/advisors and private investors, with private investors unlocking 32.5 billion tokens, and the team and advisors unlocking 50 billion tokens.

In the early hours of July 15, according to on-chain tracking data from Arkham, 57.279 billion tokens were unlocked and distributed to 121 wallets. PUMP's current market cap is approximately $650 million, with an FDV of about $1.6 billion.

Earning $20 Million Monthly, $940,000 Daily

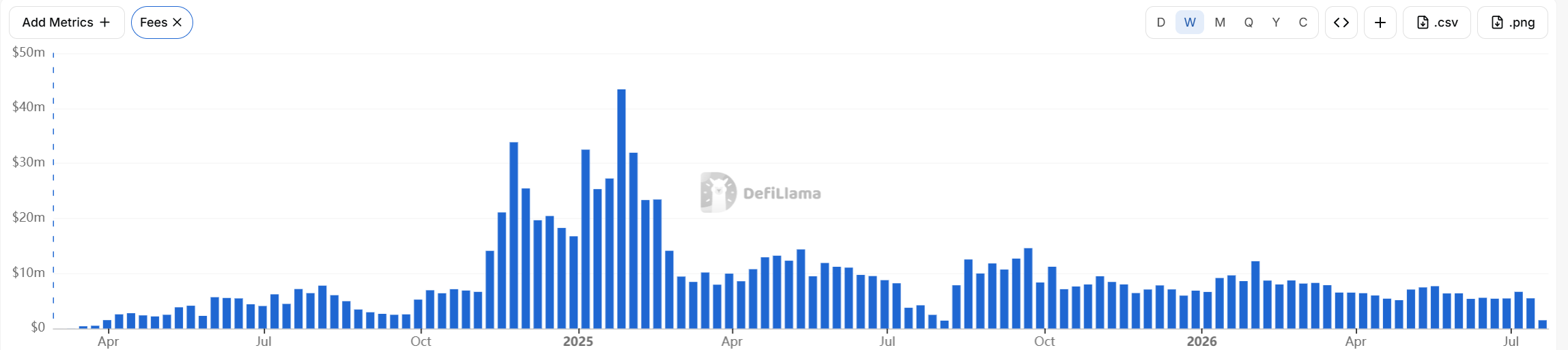

This event occurred against the backdrop where Pump.fun has become one of the most profitable applications on Solana and even in the entire Web3 ecosystem. Over the past 30 days, the platform's protocol revenue reached $24.52 million (DefiLlama data), second only to Hyperliquid's $43.93 million and higher than Polymarket's $22 million. Cumulative revenue has exceeded $1.05 billion, with over 12 million tokens issued.

Even in a deep bear market environment, Pump.fun's weekly revenue currently remains around $5 million.

However, such substantial revenue does not seem to have created a positive cycle for its token price. PUMP has fallen from a peak of $0.008980 to around $0.001628, where it has been fluctuating.

What is the real issue?

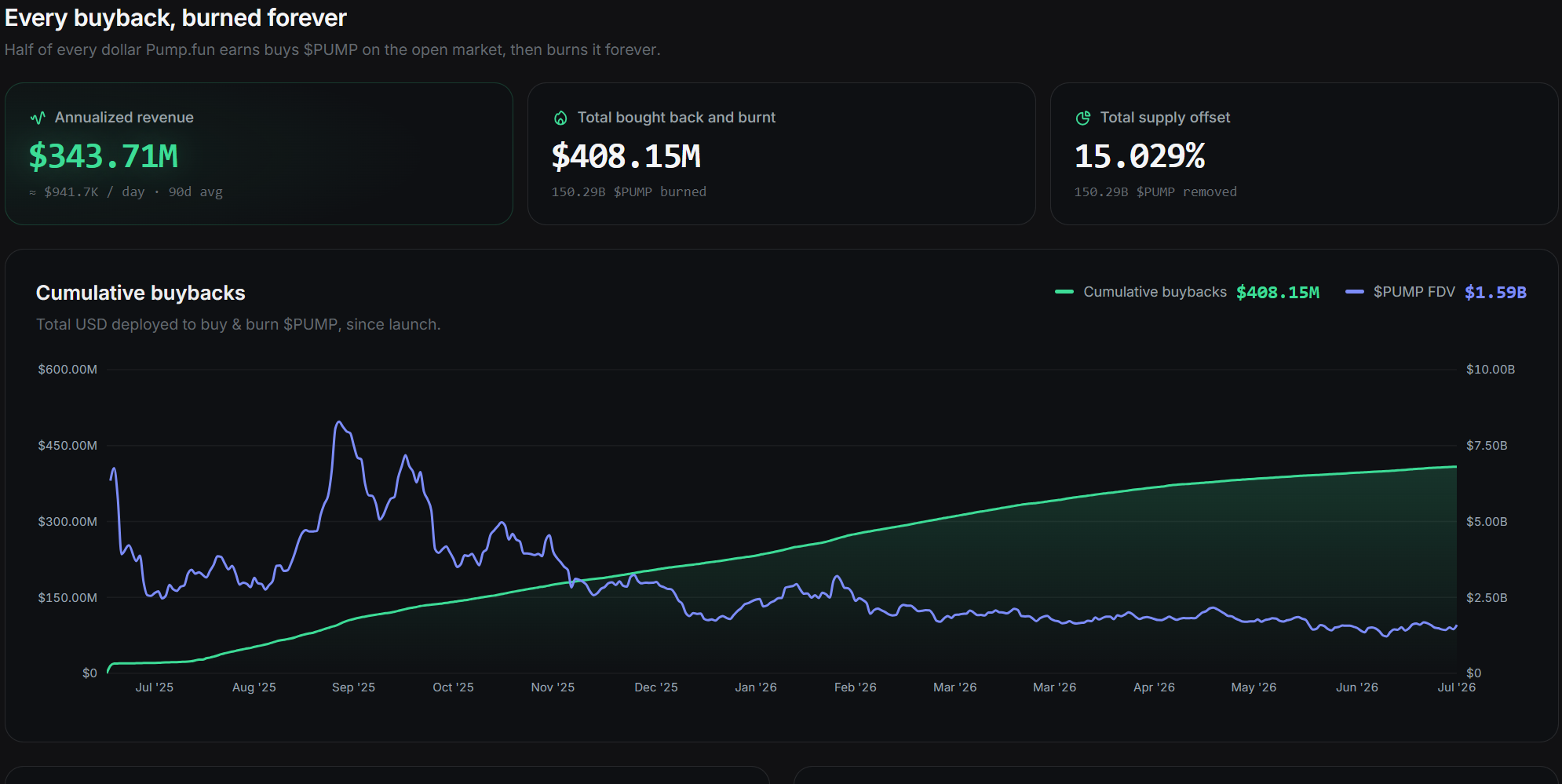

The core value capture mechanism of Pump.fun is the use of protocol fees to buy back and permanently burn PUMP tokens. According to its official platform data, its annualized revenue currently stands at $343.71 million, with an average daily revenue of $941,700 over the past 90 days. The cumulative buyback and burn amount has reached $408.15 million, with the cumulative number of tokens burned accounting for 15.029% of the total supply.

Pump started after its TGE in July 2025: Initially, 100% of net protocol fees (revenue from bonding curve, PumpSwap, Terminal cross-chain, etc., minus referral fees and cashback) were used to buy back and burn PUMP on the open market.

Adjusted on April 28, 2026: Switched to programmatically locking 50% of net revenue for buyback and burn, lasting one year; the other half is used for recruitment, marketing, and product development. All repurchased tokens are permanently burned, not locked. This constitutes PUMP's core flywheel, distinguishing it from most meme or platform tokens—the more profitable the platform, the scarcer the token supply.

However, the scale and duration of the buyback have sparked significant controversy. PUMP now allocates only 50% of net revenue for buyback and burn, a sharp reduction from the previous 100%, leading to a dramatic drop in buying support. Compared to HYPE, which uses nearly 99% of fees for buyback, and Lighter, which recently started using all revenue for buyback and burn, PUMP's buyback appears insufficient given a similar revenue scale, making it difficult to offset unlocking selling pressure, and consequently, the price remains weak.

Additionally, Pump.fun is currently facing a class-action lawsuit. U.S. plaintiffs have characterized it as an "illegal digital casino." Under such intense compliance pressure, cutting the buyback by 50% and reallocating significant funds to the treasury for hiring a "$5 million salary Chief Legal Officer" represents the team sacrificing the interests of secondary token holders to fund compliance costs for their own political risk mitigation.

Furthermore, after the one-year period ends, whether the buyback will continue remains a huge question mark.

A deeper reason lies in PUMP's "casino DNA." It is essentially a Meme launch platform, filled with PVP gambling and casino culture, characterized by extreme volatility, lowbrow narratives, and almost zero willingness from institutional funds to buy or HODL long-term. Compliance risks, reputational pressures, and a lack of real utility keep mainstream capital at bay. Relying solely on retail and speculative funds to support the price, any major unlock inevitably reveals weak liquidity and buying capacity.

Can the Market and Buyback Absorb the Massive Selling Pressure?

On-chain observations show that on the day of the unlock and the following day, some distribution wallets have already seen transfers. While this hasn't triggered a crash, short-term volatility and liquidity tests are inevitable. Moreover, PUMP's utility remains relatively weak (primarily for ecosystem incentives and potential governance). The market views it more as a "revenue-sharing certificate" rather than a strictly utility token, which amplifies sensitivity to selling pressure in a bearish market sentiment.

Compared to similar high-revenue protocols: Hyperliquid has higher monthly revenue but a market cap of nearly $15 billion (about 20+ times that of PUMP); Polymarket has similar revenue but hasn't issued a token, with a funding valuation already at the $15 billion level. The sustainable revenue capabilities of these two have been proven, while Pump.fun's revenue could sharply decline if the market turns bearish and meme coins wither.

However, this unlock is not a "one-time death sentence." The team and investors have a three-year vesting period, meaning tokens are not all sold immediately. Historical experience shows that some project teams and early investors may choose to hold or sell slowly to maintain reputation and long-term interests. Meanwhile, tokens unlocked for ecosystem incentives and the foundation can be used for growth rather than purely for selling pressure. Pump.fun has expanded from a single launchpad to include PumpSwap, multi-chain support, livestreaming, etc., forming a more complete ecosystem. As its native token, PUMP directly benefits from platform expansion.

The 82.5 billion token unlock is the real stress test for PUMP transitioning from the "100% buyback honeymoon phase" to a "sustainable but more restrained" stage. In the short term (weeks to 1-2 months), the struggle between selling pressure and buyback intensity will determine price volatility. If the market can absorb it well without liquidity drying up, it might even strengthen the narrative of high-revenue protocol tokens.

Long-term, what determines PUMP's fate is not a single unlock event, but whether Pump.fun can consistently generate revenue as a core infrastructure for the meme economy. As long as the revenue flywheel keeps turning, buybacks and burns will continue to compress supply. Conversely, any significant drop in revenue would make future unlocks a real burden.